Blind Spot Solutions Market Size, Share, and Trends Analysis Report

CAGR :

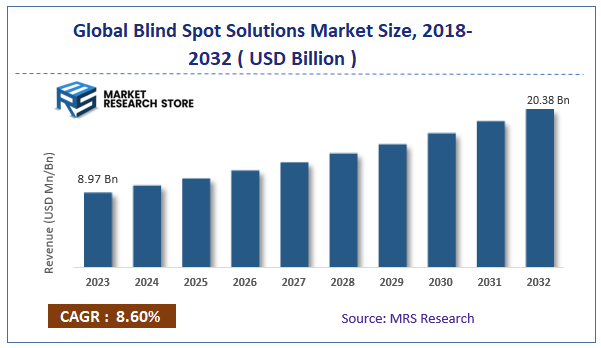

| Market Size 2023 (Base Year) | USD 8.97 Billion |

| Market Size 2032 (Forecast Year) | USD 20.38 Billion |

| CAGR | 8.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

According to Market Research Store, the global blind spot solutions market size was valued at around USD 8.97 billion in 2023 and is estimated to reach USD 20.38 billion by 2032, to register a CAGR of approximately 8.60% in terms of revenue during the forecast period 2024-2032.

To Get more Insights, Request a Free Sample

The blind spot solutions report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Blind Spot Solutions Market: Overview

Blind spot solutions refer to technologies and systems designed to detect areas around a vehicle that are not visible to the driver, commonly known as "blind spots." These systems enhance safety by alerting drivers to the presence of obstacles or other vehicles in these areas, reducing the risk of collisions during lane changes or other maneuvers.

Common blind spot solutions include radar-based sensors, cameras, ultrasonic sensors, and advanced driver-assistance systems (ADAS), which often integrate with other vehicle safety features.

Key Highlights

- The blind spot solutions market is anticipated to grow at a CAGR of 8.60% during the forecast period.

- The global blind spot solutions market was estimated to be worth approximately USD 8.97 billion in 2023 and is projected to reach a value of USD 20.38 billion by 2032.

- The growth of the blind spot solutions market is being driven by the increasing focus on vehicle safety, stringent regulations, and rising consumer demand for advanced safety features.

- Based on the product type, the Blind Spot Detection (BSD) system segment is growing at a high rate and is projected to dominate the market.

- On the basis of technology, the camera-based segment is projected to swipe the largest market share.

- In terms of Vehicle type, the passenger cars segment is expected to dominate the market.

- Based on the end-user, the OEM segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Blind Spot Solutions Market: Dynamics

Key Growth Drivers

- Increasing consumer awareness: As more people become aware of the dangers of blind spots and the benefits of blind spot solutions, demand for these technologies is expected to rise.

- Government regulations: Many governments are implementing stricter safety standards for vehicles, which often include mandates for blind spot detection systems.

- Advancements in technology: The development of more advanced and affordable blind spot solutions, such as radar and camera-based systems, is driving market growth.

- Growing popularity of electric vehicles: Electric vehicles often come equipped with advanced safety features, including blind spot detection, which is contributing to market expansion.

Restraints

- High initial cost: The initial cost of installing blind spot solutions can be a barrier for some consumers.

- Complexity of installation: Installing these systems can be complex and may require professional expertise, which can add to the overall cost.

- Potential for false alarms: Some blind spot solutions may trigger false alarms, leading to driver frustration and reduced trust in the technology.

- Limited effectiveness in certain conditions: The effectiveness of blind spot solutions can be limited in adverse weather conditions, such as heavy rain or snow.

Opportunities

- Integration with other advanced driver assistance systems (ADAS): Blind spot solutions can be integrated with other ADAS features, such as lane departure warning and adaptive cruise control, to provide a more comprehensive safety package.

- Development of new and innovative solutions: There is potential for the development of new and innovative blind spot solutions, such as those that can detect pedestrians and cyclists.

- Expansion into new markets: The market for blind spot solutions is still relatively untapped in some regions, presenting opportunities for growth.

- Increasing demand for autonomous vehicles: Autonomous vehicles will require advanced safety features, including blind spot detection, to operate safely on public roads.

Challenges

- Competition from low-cost alternatives: There are low-cost alternatives to blind spot solutions available, such as blind spot mirrors, which can compete with more advanced technologies.

- Technical limitations: There are still some technical limitations to blind spot solutions, such as their ability to detect objects in certain conditions.

- Regulatory challenges: Ensuring that blind spot solutions comply with different regulatory standards around the world can be a challenge.

- Supply chain disruptions: Disruptions in the supply chain can impact the availability and pricing of blind spot solutions.

Blind Spot Solutions Market: Segmentation Insights

The global blind spot solutions market is divided by product type, technology, vehicle type, end-user, and region.

Segmentation Insights by Product Type

Based on product type, the global blind spot solutions market is divided into Blind Spot Detection (BSD) system, backup camera system, park assist system, surround view system and virtual pillars.

The Blind Spot Detection (BSD) system is the most dominant segment within this market. It is widely adopted due to its critical role in enhancing driver awareness, particularly during lane changes. BSD systems use radar or cameras to monitor the areas alongside and slightly behind the vehicle, alerting drivers to the presence of other vehicles in their blind spots.

This technology has gained significant traction as it improves road safety by reducing the likelihood of collisions, especially in congested traffic or high-speed environments. BSD systems are often integrated into mid-range and high-end vehicles, making them a key product in the automotive safety solutions market.

The Backup Camera System follows closely behind BSD systems in terms of market share. These systems, mandated in many regions for new vehicles, are essential for improving visibility when reversing.

Backup cameras provide a real-time video feed of the area directly behind the vehicle, helping drivers avoid obstacles or pedestrians, particularly in parking lots or tight spaces. Their popularity stems from their effectiveness in reducing the risk of accidents during reversing maneuvers. This technology has become standard in many vehicles, further driving its market growth.

The Park Assist System is another crucial segment of the blind spot solutions market. These systems use a combination of sensors, cameras, and automated steering to help drivers park their vehicles with ease. Park assists systems vary from basic alerts about nearby objects to fully autonomous parking functions, which can control steering while the driver manages acceleration and braking.

This feature is increasingly popular among drivers who seek convenience, particularly in urban environments where parking spaces are limited and difficult to navigate. As consumer demand for automated and semi-automated driving assistance grows, park assist systems continue to expand in adoption.

The Surround View System provides a comprehensive 360-degree view around the vehicle using multiple cameras placed on different sides. This system is valuable in preventing accidents in tight spaces or complex driving conditions. It helps drivers visualize obstacles, pedestrians, and other vehicles that may be hard to detect with standard rearview mirrors or a backup camera alone.

Surround view systems are mostly featured in high-end vehicles, though they are gradually being introduced into more mid-range models due to rising safety standards. Their advanced capabilities make them a preferred option for drivers looking for an extra layer of security.

The Virtual Pillars technology is an emerging and innovative solution aimed at eliminating blind spots caused by the vehicle’s structural pillars. Using cameras and display screens, this system creates a transparent view of the vehicle's surroundings, allowing drivers to see through areas typically obstructed by the A, B, and C pillars.

Although this technology is still in its nascent stages, it has the potential to revolutionize automotive safety by addressing one of the most persistent blind spot issues. Virtual pillars are expected to gain momentum in the coming years as automotive manufacturers work towards more advanced, driver-centric safety features.

Segmentation Insights by Technology

On the basis of technology, the global blind spot solutions market is bifurcated into camera-based, radar-based, ultrasonic-based.

Camera-based technology is one of the leading methods used in blind spot solutions. This technology employs visual sensors strategically positioned around the vehicle to capture real-time images of the surroundings. Camera-based systems can provide a comprehensive view of blind spots, making them ideal for features like backup cameras and surround view systems. The primary advantage of this technology is its ability to offer high-resolution images, allowing for clear visibility of obstacles, pedestrians, and other vehicles.

Additionally, advanced image processing algorithms can enhance visibility in low-light conditions, further increasing safety. As the demand for driver assistance features rises, camera-based technology continues to gain traction in both mid-range and high-end vehicles.

Radar-based technology is another critical component of blind spot solutions, known for its effectiveness in detecting objects in a vehicle's vicinity. Radar sensors emit radio waves to monitor the surrounding area, allowing for accurate distance and speed measurements of nearby vehicles.

This technology is particularly beneficial for blind spot detection systems, as it can identify vehicles in adjacent lanes without being affected by weather conditions, such as rain or fog, which might hinder camera visibility. The reliability of radar-based systems has made them a popular choice among automakers, especially for BSD systems. The growing emphasis on vehicle safety and autonomous driving technologies further propels the adoption of radar-based solutions in the automotive industry.

Ultrasonic-based technology utilizes sound waves to detect objects in proximity to the vehicle. This technology is often employed in parking assist systems, where ultrasonic sensors are mounted on the front and rear bumpers to provide information about obstacles during low-speed maneuvers.

The sensors emit high-frequency sound waves and measure the time it takes for the echoes to return after bouncing off nearby objects, enabling the system to calculate their distance. Ultrasonic sensors are particularly effective in detecting stationary objects and are commonly used in conjunction with other technologies for enhanced performance. Although they are primarily used for parking assistance, their reliability in close-range detection makes them an essential part of the blind spot solutions market.

Segmentation Insights by Vehicle Type

In terms of vehicle type, the global blind spot solutions market is categorized into passenger cars, light commercial vehicles and heavy commercial vehicles.

Passenger cars represent the largest segment in the blind spot solutions market. This category encompasses a wide range of vehicles designed primarily for personal transportation. As consumer safety awareness increases, automakers are incorporating advanced blind spot detection systems into their models to enhance driver awareness and minimize the risk of accidents.

Technologies such as blind spot monitoring, backup cameras, and park assist systems are becoming standard features in many mid-range and luxury vehicles. Additionally, regulatory mandates in various regions are pushing manufacturers to adopt these safety features, making passenger cars a primary driver of growth in the blind spot solutions market.

Light commercial vehicles (LCVs), which include vans and small trucks, are another significant segment of the market. These vehicles are often used for business purposes, requiring enhanced safety measures to protect drivers and cargo. LCVs frequently operate in urban environments where maneuverability and visibility are crucial.

Blind spot solutions, such as rearview cameras and radar-based detection systems, are increasingly being integrated to assist drivers in navigating tight spaces and ensuring the safety of pedestrians and other vehicles. The growing demand for delivery services and e-commerce is further fueling the adoption of advanced safety technologies in light commercial vehicles.

Heavy commercial vehicles (HCVs), including buses and large trucks, represent a critical segment of the blind spot solutions market due to their size and operational complexities. These vehicles often face significant blind spots, making them more susceptible to accidents.

The integration of advanced blind spot detection systems is essential for improving safety and operational efficiency. Technologies such as radar-based systems and surround view cameras are particularly valuable in this segment, helping drivers manage their larger blind spots and enhancing overall road safety. As regulations surrounding commercial vehicle safety tighten, the demand for blind spot solutions in heavy commercial vehicles is expected to grow.

Segmentation Insights by End-user

In terms of end-user, the global blind spot solutions market is categorized into OEM and aftermarket.

The OEM segment is a major driver of the blind spot solutions market. OEMs integrate advanced blind spot detection and assistance technologies directly into new vehicles during the manufacturing process. This integration has become increasingly important as consumer demand for safety features rises.

Many automakers offer blind spot monitoring systems, backup cameras, and parking assist technologies as standard or optional equipment in their vehicles.

Additionally, regulatory requirements in various regions are pushing manufacturers to enhance safety features in their new models. The OEM segment benefits from the increasing focus on vehicle safety, with advancements in technology leading to more sophisticated and reliable blind spot solutions being built into vehicles.

The aftermarket segment refers to the installation of blind spot solutions in vehicles after their initial sale. This segment is growing as consumers become more aware of the importance of safety features and seek to upgrade their existing vehicles with advanced technologies.

Aftermarket solutions typically include blind spot detection systems, backup cameras, and parking assistance kits, which can be added to older models that may not come equipped with such features. The growth of the aftermarket segment is driven by factors such as rising vehicle ownership, increasing awareness of road safety, and the availability of affordable and user-friendly aftermarket solutions.

Additionally, advancements in technology have made it easier for consumers to install these systems, further boosting the demand in this segment.

Blind Spot Solutions Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Blind Spot Solutions Market |

| Market Size in 2023 | USD 8.97 Billion |

| USD 20.38 Billion | |

| Growth Rate | CAGR of 8.60% |

| Number of Pages | 220 |

| Key Companies Covered | Schaeffler AG, Ficosa Internacional SA, Autoliv Inc., ZF Friedrichshafen AG, GENTEX CORPORATION, Motherson, Murakami Corporation, Renesas Electronics Corporation., SAMSUNG ELECTRO-MECHANICS, SL Corporation , STONKAM CO.LTD, Gentex, Samvardhana Motherson, Robert Bosch GmbH, Continental AG, DENSO CORPORATION, Valeo, Magna International Inc., Faurecia, HYUNDAI MOBIS, Aptiv, TOYOTA MOTOR CORPORATION, and others. |

| Segments Covered | By Product Type, By Technology, By Vehicle Type, By End-user, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Blind Spot Solutions Market: Regional Insights

- North America is expected to dominates the global market

In the North American region, the blind spot solutions market is dominated by the presence of advanced automotive technology and a strong automotive industry. The high adoption of safety features, such as blind spot detection and monitoring systems, is driven by stringent safety regulations and consumer demand for safer vehicles.

Major automakers in the U.S. and Canada integrate these systems into a variety of vehicles, ranging from luxury to mid-tier cars, making North America a leading market for blind spot solutions.

Europe follows closely as a dominant market due to the region's robust automotive industry and strict vehicle safety standards, particularly in countries like Germany, the U.K., and France. Many premium automakers, particularly from Germany, lead in integrating sophisticated blind spot solutions in their models.

Additionally, government mandates around vehicular safety are pushing both manufacturers and consumers to prioritize advanced driver-assistance systems (ADAS), including blind spot monitoring.

In the Asia-Pacific region, the blind spot solutions market is rapidly expanding, especially in countries like China, Japan, and South Korea. The growth is fueled by the increasing production of automobiles and a rising focus on vehicle safety due to growing accident rates.

The region's automotive sector is undergoing technological advancements, and governments are promoting safety features as standard in both commercial and passenger vehicles, contributing to the increased adoption of blind spot systems.

The Latin American market for blind spot solutions is growing steadily, driven by rising awareness about vehicle safety features and the modernization of the regional automotive industry. Countries such as Brazil and Mexico are seeing increased adoption of advanced safety technologies as global automakers expand their presence in the region, integrating blind spot detection systems into their vehicle offerings.

In the Middle East and Africa, the market for blind spot solutions is still in its nascent stages, but it is expected to grow as the automotive market in the region expands. Increasing vehicle sales, urbanization, and infrastructure development are driving the demand for improved vehicle safety features. While the adoption rate is slower compared to other regions, there is potential for growth as the region embraces new automotive technologies.

Blind Spot Solutions Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the blind spot solutions market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global blind spot solutions market include:

- Schaeffler AG

- Ficosa Internacional SA

- Autoliv Inc.

- ZF Friedrichshafen AG

- GENTEX CORPORATION

- Motherson

- Murakami Corporation

- Renesas Electronics Corporation.

- SAMSUNG ELECTRO-MECHANICS

- SL Corporation

- STONKAM CO.LTD

- Gentex

- Samvardhana Motherson

- Robert Bosch GmbH

- Continental AG

- DENSO CORPORATION

- Valeo

- Magna International Inc.

- Faurecia

- HYUNDAI MOBIS

- Aptiv

- TOYOTA MOTOR CORPORATION.

The global blind spot solutions market is segmented as follows:

By Product Type

- Blind Spot Detection (BSD) System

- Backup Camera System

- Park Assist System

- Surround View System

- Virtual Pillars

By Technology

- Camera-Based

- Radar-Based

- Ultrasonic-Based

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By End-user

- OEM

- Aftermarket

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global blind spot solutions market size was projected at approximately US$ 8.97 billion in 2023. Projections indicate that the market is expected to reach around US$ 20.38 billion in revenue by 2032.

The global blind spot solutions market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 8.60% during the forecast period from 2024 to 2032.

North America is expected to dominate the global blind spot solutions market.

The global blind spot solutions market is driven by increasing vehicle safety regulations, growing consumer demand for advanced driver-assistance systems (ADAS), and the rising adoption of connected and autonomous vehicle technologies.

Some of the prominent players operating in the global blind spot solutions market are; Schaeffler AG, Ficosa Internacional SA, Autoliv Inc., ZF Friedrichshafen AG, GENTEX CORPORATION, Motherson, Murakami Corporation, Renesas Electronics Corporation., SAMSUNG ELECTRO-MECHANICS, SL Corporation , STONKAM CO.LTD, Gentex, Samvardhana Motherson, Robert Bosch GmbH, Continental AG, DENSO CORPORATION, Valeo, Magna International Inc., Faurecia, HYUNDAI MOBIS, Aptiv, TOYOTA MOTOR CORPORATION., and others.

Table Of Content

Inquiry For Buying

Blind Spot Solutions

Request Sample

Blind Spot Solutions