Deployment Automation Market Size, Share, and Trends Analysis Report

CAGR :

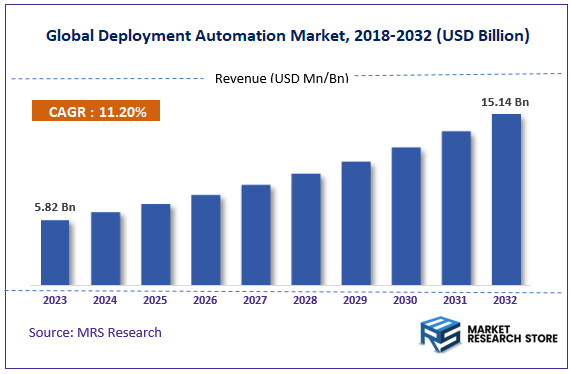

| Market Size 2023 (Base Year) | USD 5.82 Billion |

| Market Size 2032 (Forecast Year) | USD 15.14 Billion |

| CAGR | 11.2% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Deployment Automation Market Insights

According to Market Research Store, the global deployment automation market size was valued at around USD 5.82 billion in 2023 and is estimated to reach USD 15.14 billion by 2032, to register a CAGR of approximately 11.2% in terms of revenue during the forecast period 2024-2032.

To Get more Insights, Request a Free Sample

The deployment automation report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Deployment Automation Market: Overview

Deployment automation refers to the process of automatically deploying software applications and updates to various environments, such as development, testing, staging, or production, without manual intervention. It is a key component of modern DevOps practices and continuous integration/continuous delivery (CI/CD) pipelines. The goal of deployment automation is to streamline and standardize the release process, reduce human error, accelerate delivery times, and ensure consistency across all environments.

Automated deployment tools manage the tasks involved in releasing new code, including compiling code, running tests, configuring environments, and moving applications to their target systems. These tools can be integrated with version control systems, build servers, and cloud platforms to enable end-to-end automation from development to deployment.

Key Highlights

- The deployment automation market is anticipated to grow at a CAGR of 11.2% during the forecast period.

- The global deployment automation market was estimated to be worth approximately USD 5.82 billion in 2023 and is projected to reach a value of USD 15.14 billion by 2032.

- The growth of the deployment automation market is being driven by the increasing need for efficiency, cost reduction, and faster deployment cycles in IT environments across various industries.

- Based on the product, the cloud based segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the SMEs segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Deployment Automation Market: Dynamics

Key Growth Drivers

- Increasing Adoption of DevOps and Agile Methodologies: The core driver is the widespread adoption of DevOps and agile practices, which emphasize frequent and rapid software releases, necessitating automated deployment pipelines.

- Growing Complexity of IT Infrastructure: Modern applications often involve complex microservices architectures, containerization (Docker, Kubernetes), and hybrid or multi-cloud environments, making manual deployment error-prone and time-consuming, thus demanding automation.

- Need for Faster Time-to-Market: Businesses are under constant pressure to release new features and applications quickly to stay competitive. Deployment automation significantly reduces the time required for software releases.

- Demand for Improved Efficiency and Reduced Errors: Automating deployment processes minimizes manual intervention, leading to fewer human errors, increased consistency, and improved overall efficiency.

- Scalability and Reliability Requirements: As applications scale and become more critical, automated deployment ensures consistent and reliable deployments across numerous servers and environments.

- Cloud Adoption and Infrastructure-as-Code (IaC): The increasing adoption of cloud platforms and the use of IaC practices (e.g., Terraform, CloudFormation) create a natural synergy with deployment automation tools.

- Focus on Continuous Integration and Continuous Delivery (CI/CD): Deployment automation is a critical component of CI/CD pipelines, enabling the automated build, test, and release of software.

- Security and Compliance Automation: Automating deployment processes allows for the consistent application of security policies and compliance requirements, reducing the risk of vulnerabilities and audit failures.

Restraints

- High Initial Investment and Implementation Costs: Implementing comprehensive deployment automation solutions can require significant upfront investment in tools, infrastructure, and training.

- Complexity of Integration with Existing Systems: Integrating new automation tools with existing legacy systems, development pipelines, and IT infrastructure can be complex and time-consuming.

- Resistance to Change and Organizational Inertia: Some organizations may face resistance from teams accustomed to manual deployment processes, hindering the adoption of automation.

- Lack of Skilled Personnel and Expertise: Implementing and managing sophisticated deployment automation tools requires specialized skills and expertise, which may be scarce within some organizations.

- Potential for Automation Errors and System Downtime: While automation reduces human error, poorly configured automation scripts can lead to widespread errors and system downtime if not properly tested and managed.

- Security Risks Associated with Automation Tools: If not properly secured, automation tools with privileged access to deployment environments can become targets for malicious actors.

- Cost Justification and ROI Measurement: Quantifying the return on investment (ROI) for deployment automation initiatives can be challenging, especially in the short term.

- Vendor Lock-in Concerns: Choosing a specific deployment automation platform can lead to vendor lock-in, making it difficult to switch to alternative solutions in the future.

Opportunities

- Development of More User-Friendly and Low-Code/No-Code Automation Platforms: Platforms that simplify the creation and management of deployment pipelines, making automation accessible to a wider range of users.

- Integration of AI and Machine Learning for Intelligent Automation: Utilizing AI/ML to optimize deployment workflows, predict potential issues, and automate rollback strategies.

- Cloud-Native Deployment Automation Solutions: Tools specifically designed for cloud-native environments, leveraging containerization and orchestration technologies.

- Security-Focused Automation Tools (DevSecOps): Solutions that tightly integrate security checks and compliance enforcement into the automated deployment pipeline.

- Infrastructure-as-Code (IaC) Management and Orchestration Tools: Platforms that provide comprehensive management and orchestration of IaC across multi-cloud environments.

- Hybrid and Multi-Cloud Deployment Automation: Solutions that enable seamless and consistent deployments across hybrid and multi-cloud infrastructures.

- Specialized Automation for Edge Computing and IoT Deployments: Tools tailored for the unique challenges of deploying and managing applications on edge devices and IoT infrastructure.

- Managed Deployment Automation Services: Offering managed services where vendors handle the implementation, configuration, and maintenance of deployment automation pipelines.

Challenges

- Managing the Complexity of Heterogeneous Environments: Ensuring consistent and reliable deployments across diverse operating systems, middleware, and infrastructure platforms.

- Maintaining the Security and Integrity of Automated Deployment Pipelines: Protecting automation tools and credentials from unauthorized access and ensuring the integrity of deployed applications.

- Ensuring Rollback and Disaster Recovery Capabilities: Implementing robust rollback mechanisms and disaster recovery plans within the automated deployment process.

- Monitoring and Troubleshooting Automated Deployments: Developing effective monitoring and logging systems to quickly identify and resolve issues in automated deployments.

- Adapting to Evolving Technologies and Architectures: Continuously updating automation workflows and tools to support new technologies like serverless computing and service mesh.

- Fostering Collaboration and Communication Across Teams: Ensuring that development, operations, and security teams effectively collaborate within the automated deployment process.

- Scaling Automation to Handle Increasing Deployment Frequency and Volume: Designing automation pipelines that can efficiently handle a growing number of deployments across a larger infrastructure.

- Measuring and Demonstrating the Value and ROI of Automation Initiatives: Developing clear metrics and reporting mechanisms to showcase the benefits of deployment automation to stakeholders.

Deployment Automation Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Deployment Automation Market |

| Market Size in 2023 | USD 5.82 Billion |

| Market Forecast in 2032 | USD 15.14 Billion |

| Growth Rate | CAGR of 11.2% |

| Number of Pages | 140 |

| Key Companies Covered | Microsoft, JetBrains, Octopus, GitLab Inc., Appveyor, Atlassian, DeployBot, CircleCI, Amazon, Codeship, Stackify, ElectricFlow, PDQ, Chef, Codeship, and others. |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Deployment Automation Market: Segmentation Insights

The global deployment automation market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global deployment automation market is divided into cloud based and on-premise.

Cloud Based segment dominates the Deployment Automation Market due to its scalability, cost-effectiveness, and ease of integration across diverse IT environments. As organizations increasingly adopt DevOps practices and agile development cycles, cloud-based deployment automation tools enable faster and more reliable software delivery pipelines. These solutions provide real-time monitoring, continuous delivery capabilities, and automatic updates with minimal infrastructure management. Additionally, cloud-based tools are favored by companies looking to reduce on-premise hardware dependencies and support remote or hybrid workforces, making this segment the preferred choice for both large enterprises and small-to-medium businesses.

On-Premise segment holds a significant share, especially among organizations in highly regulated industries such as finance, government, and healthcare, where data sovereignty and compliance requirements necessitate greater control over software infrastructure. On-premise deployment automation tools offer customized security configurations and allow full control over operational environments. While adoption growth is slower compared to cloud-based solutions, this segment remains vital for companies prioritizing data privacy, legacy systems integration, and internal IT governance policies.

Segmentation Insights by Application

On the basis of application, the global deployment automation market is bifurcated into SMEs, large enterprises, and government organizations.

SMEs dominate the Deployment Automation Market by overcome challenges associated with limited IT resources, budget constraints, and the growing complexity of software delivery pipelines. By utilizing automated deployment solutions—particularly cloud-based platforms—SMEs can streamline application rollouts, reduce human intervention, and ensure consistent configuration across development and production environments. The scalability of these tools allows SMEs to start small and expand functionalities as business needs evolve. Automation also enhances their agility, enabling faster iterations, improved customer responsiveness, and reduced downtime, which are crucial for maintaining competitiveness in fast-paced markets.

Large Enterprises are increasingly turning to deployment automation market by application due to their need to manage vast IT ecosystems with multiple interdependent applications and services across global operations. These enterprises often operate in sectors like finance, healthcare, e-commerce, and manufacturing, where uptime, performance, and security are mission-critical. Deployment automation supports continuous integration and continuous deployment (CI/CD) practices, reduces deployment errors, and ensures rapid delivery of updates and patches without disrupting services. Large enterprises also benefit from deep customization capabilities, advanced analytics, and seamless integration with existing DevOps toolchains. These capabilities enable them to optimize workflows, enforce compliance, and meet service-level objectives efficiently.

Government Organizations are gradually adopting deployment automation as part of broader digital transformation initiatives. Their objectives include improving service delivery, enhancing operational transparency, and strengthening cybersecurity posture. Automation supports consistent and timely deployment of software updates across a wide range of public services, from healthcare management systems to defense infrastructure. It also reduces dependency on legacy systems and manual processes, thereby improving agility and scalability. However, adoption in this segment is often hindered by stringent regulatory requirements, limited budgets, and procurement complexity. Despite these challenges, increasing awareness of the benefits—such as improved disaster recovery and compliance automation—is driving progressive implementation across various departments and agencies.

Deployment Automation Market: Regional Insights

- North America is expected to dominate the global market

North America holds the dominant position in the Deployment Automation Market due to its highly developed IT and cloud infrastructure, along with early adoption of DevOps and agile methodologies. The United States, in particular, is home to many global technology firms and cloud service providers that continuously invest in deployment automation to streamline software delivery pipelines. This region sees heavy demand for advanced automation frameworks that integrate seamlessly with CI/CD tools, allowing organizations to automate code integration, testing, configuration, and deployment across multi-cloud and hybrid environments. In addition to large enterprises, small and medium-sized businesses in North America are adopting automation to reduce time-to-market and enhance scalability. Increasing use of containerized applications and microservices architecture has further intensified the use of deployment automation platforms across sectors such as finance, healthcare, retail, and telecom.

Europe has a well-established and growing market for deployment automation, driven by increasing digitalization, cybersecurity concerns, and regulatory compliance across sectors. Countries such as Germany, the UK, France, and the Netherlands have been at the forefront of adopting DevOps practices and enterprise automation tools. European enterprises often emphasize stability, security, and compliance in their IT operations, which has fueled demand for robust and policy-driven deployment automation tools. The region's strong focus on data privacy (e.g., GDPR) has also encouraged adoption of secure and auditable automation pipelines. Many public and private organizations are leveraging deployment automation to modernize their legacy systems and accelerate digital transformation initiatives while ensuring traceability and control in their software delivery processes.

Asia-Pacific is the fastest-growing region in the Deployment Automation Market, fueled by a rapidly expanding tech ecosystem, significant digital infrastructure investments, and growing cloud adoption across developing economies. Countries like China, India, Japan, South Korea, and Australia are experiencing a surge in enterprise-level adoption of cloud-native technologies, including Kubernetes, containers, and serverless computing, which has increased the demand for deployment automation solutions. In India and Southeast Asia, a growing pool of DevOps professionals and IT startups are integrating automation to achieve faster, error-free deployments and improve software quality. The region is also seeing increasing adoption of AI/ML-driven automation tools, which enhance deployment efficiency by predicting failures, optimizing resources, and improving performance. Governments and large enterprises are investing heavily in IT modernization, which further supports market growth.

Latin America is an emerging market where deployment automation adoption is gaining traction due to growing digitization in sectors such as banking, telecommunications, and e-commerce. Countries like Brazil, Mexico, Argentina, and Chile are seeing increased investment in IT automation to modernize infrastructure and improve service delivery. While deployment automation is still in the early stages of adoption across many organizations in the region, there is increasing awareness of its benefits in improving agility, consistency, and operational efficiency. Regional companies are partnering with global software vendors and cloud service providers to implement scalable deployment automation solutions that help them stay competitive and reduce dependency on manual processes. Government-backed digital initiatives and the growth of fintech and healthtech startups are also contributing to greater demand for streamlined deployment systems.

Middle East & Africa are developing regions in the Deployment Automation Market, with adoption primarily driven by digital transformation efforts in the enterprise and public sectors. In the Middle East, countries like the UAE and Saudi Arabia are actively investing in cloud platforms and automation technologies as part of their smart city and Vision 2030 goals. These initiatives have led to increased implementation of deployment automation in sectors like energy, finance, and government. Enterprises are focusing on improving business continuity, infrastructure agility, and service responsiveness, making automation a strategic priority. In Africa, although adoption is slower, countries such as South Africa, Nigeria, and Kenya are witnessing a rise in cloud adoption and IT modernization projects, leading to gradual uptake of deployment automation tools. The growing presence of international cloud providers and managed service firms is also playing a key role in expanding market reach in this region.

Deployment Automation Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the deployment automation market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global deployment automation market include:

- Microsoft

- JetBrains

- Octopus

- GitLab Inc.

- Appveyor

- Atlassian

- DeployBot

- CircleCI

- Amazon

- Codeship

- Stackify

- ElectricFlow

- PDQ

- Chef

- Codeship

The global deployment automation market is segmented as follows:

By Product

- Cloud Based

- On-Premise

By Application

- SMEs

- Large Enterprises

- Government Organizations

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Deployment Automation

Request Sample

Deployment Automation