Energy Retrofit Systems Market Size, Share, and Trends Analysis Report

CAGR :

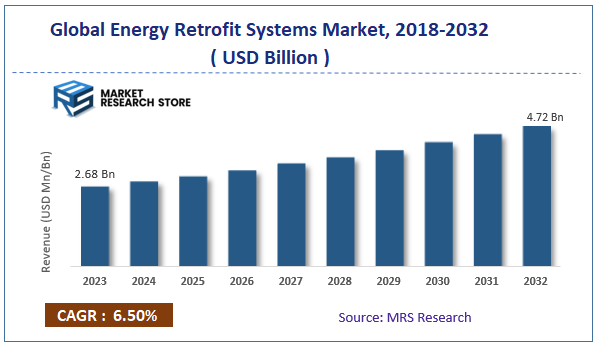

| Market Size 2023 (Base Year) | USD 2.68 Billion |

| Market Size 2032 (Forecast Year) | USD 4.72 Billion |

| CAGR | 6.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

According to Market Research Store, the global energy retrofit systems market size was valued at around USD 2.68 billion in 2023 and is estimated to reach USD 4.72 billion by 2032, to register a CAGR of approximately 6.50% in terms of revenue during the forecast period 2024-2032.

To Get more Insights, Request a Free Sample

The energy retrofit systems report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Energy Retrofit Systems Market: Overview

Energy retrofit systems refer to the process of upgrading or improving existing buildings or infrastructure to increase energy efficiency, reduce energy consumption, and lower carbon emissions. These systems typically involve installing energy-efficient technologies, such as insulation, advanced heating, ventilation, and air conditioning (HVAC) systems, lighting upgrades, energy management systems, and renewable energy sources like solar panels. The goal is to enhance the overall energy performance of buildings, making them more sustainable and cost-effective in the long run.

Key Highlights

- The energy retrofit systems market is anticipated to grow at a CAGR of 6.50% during the forecast period.

- The global energy retrofit systems market was estimated to be worth approximately USD 2.68 billion in 2023 and is projected to reach a value of USD 4.72 billion by 2032.

- The growth of the energy retrofit systems market is being driven by the increasing emphasis on sustainability, energy savings, and government regulations aimed at reducing energy consumption.

- Based on the type, the HVAC retrofit segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the commercial segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Energy Retrofit Systems Market: Dynamics

Key Growth Drivers

- Rising Energy Costs: Escalating energy prices are compelling businesses and individuals to seek cost-effective solutions, making energy retrofits an attractive option.

- Increasing Environmental Concerns: Growing awareness of climate change and the need for sustainable practices is driving the adoption of energy-efficient technologies.

- Stringent Government Regulations: Governments worldwide are implementing stricter regulations to reduce carbon emissions and promote energy conservation, incentivizing energy retrofits.

Restraints

- High Initial Investment Costs: The upfront costs of energy retrofit projects can be significant, hindering adoption, especially for small businesses and individual homeowners.

- Technical Complexity: Implementing energy retrofits often requires specialized knowledge and expertise, which can be a barrier for some.

- Uncertainty in Return on Investment (ROI): While energy retrofits offer long-term benefits, the ROI can be uncertain and difficult to quantify, especially for complex projects.

Opportunities

- Emerging Technologies: Advancements in energy-efficient technologies, such as smart building systems and renewable energy integration, present new opportunities for innovative retrofit solutions.

- Growing Focus on Building Efficiency: The increasing emphasis on building efficiency and sustainability standards is creating a demand for retrofit solutions that improve building performance.

- Expanding Green Building Market: The expanding green building market is driving the adoption of energy-efficient retrofit solutions to achieve sustainability certifications.

Challenges

- Lack of Awareness: Many businesses and individuals are still unaware of the benefits and potential cost savings of energy retrofits.

- Financing Constraints: Access to affordable financing options can be a challenge for many, hindering the adoption of energy retrofit projects.

- Building Code and Permitting Hurdles: Navigating complex building codes and permitting processes can delay and complicate energy retrofit projects.

Energy Retrofit Systems Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Energy Retrofit Systems Market |

| Market Size in 2023 | USD 2.68 Billion |

| Market Forecast in 2032 | USD 4.72 Billion |

| Growth Rate | CAGR of 6.50% |

| Number of Pages | 213 |

| Key Companies Covered | AECOM Energy, Daikin Industries, Johnson Controls, Orion Energy Systems, Schneider Electric, Ameresco, Chevron Energy Solutions, Eaton, Philips Lighting, Trane, Ballard Power Systems, Plug Power Inc, ITM Power PLC, Intelligent Energy Limited, ElringKlinger AG, Infinity Fuel Cell and Hydrogen Inc., Doosan Fuel Cell Co. Ltd., Toshiba Corporation, Loop energy, Pragma Industries, SFC Energy AG, Shanghai Shenli Technology Co. Ltd., W. L. Gore & Associates, PowerCell Sweden AB, Cummins Inc., AVL, Nedstack Fuel Cell Technology BV, Horizon Fuel Cell Technologies, Altergy, NUVERA FUEL CELLS LLC, and others. |

| Segments Covered | By Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Energy Retrofit Systems Market: Segmentation Insights

The global energy retrofit systems market is divided by type, application, and region.

Segmentation Insights by Type

Based on type, the global energy retrofit systems market is divided into envelope, led retrofit lighting, HVAC retrofit, and appliances.

The HVAC (Heating, Ventilation, and Air Conditioning) retrofit segment dominates the energy retrofit market due to the increasing demand for energy-efficient systems in both residential and commercial buildings. Retrofit systems help improve the energy performance of existing HVAC units by upgrading or replacing outdated components. With rising energy costs and environmental concerns, businesses and homeowners alike are increasingly investing in HVAC retrofitting to reduce energy consumption, lower operational costs, and meet sustainability goals. This segment has a robust compound annual growth rate (CAGR) driven by both government regulations and a growing awareness of energy conservation.

The LED retrofit lighting segment is also a major player in the energy retrofit systems market. LED retrofitting involves replacing conventional lighting systems with energy-efficient LED lights. This segment benefits from the long lifespan, energy efficiency, and cost-saving potential of LEDs, which have become the standard lighting choice for commercial, industrial, and residential spaces. The increasing adoption of LED lighting is driven by the need to reduce energy consumption and lower electricity bills. This segment also enjoys strong support from government energy-saving initiatives and green building certifications, contributing to its high growth rate.

The envelope segment focuses on retrofitting a building's exterior, such as walls, windows, roofs, and insulation, to enhance its energy efficiency. Improving the building envelope helps to reduce heating and cooling costs by preventing energy loss. This segment has seen growing demand due to stricter building codes and the emphasis on reducing carbon footprints. Retrofitting the envelope is an effective way to enhance building performance and reduce reliance on HVAC systems. While this segment is crucial, its growth is slower compared to HVAC retrofit and LED lighting due to the higher initial costs and the complexity of installation.

The appliances segment involves retrofitting or upgrading household and commercial appliances such as refrigerators, washing machines, and ovens with more energy-efficient models. While this segment is significant, it is relatively less dominant compared to HVAC retrofit and LED lighting, mainly due to the slower replacement cycles of large appliances and the higher upfront investment in more energy-efficient versions. However, with the increasing adoption of smart appliances and rising consumer awareness, this segment is seeing gradual growth, supported by energy-saving incentives and programs.

Segmentation Insights by Application

On the basis of application, the global energy retrofit systems market is bifurcated into residential, commercial, and institutional.

The commercial segment is the largest and most dominating application in the energy retrofit systems market. This is due to the substantial energy consumption of commercial buildings, including offices, retail stores, hotels, and other business establishments, which require significant energy to operate. Commercial buildings are under increasing pressure to reduce operating costs and comply with energy efficiency regulations. Retrofitting energy systems like HVAC, lighting, and building envelopes helps businesses lower energy bills, improve sustainability, and enhance building performance. The commercial sector also benefits from government incentives, tax rebates, and green building certifications (such as LEED), which are driving strong demand for energy retrofitting. This segment sees high growth due to the large number of buildings being retrofitted to meet sustainability and operational efficiency goals.

The residential segment is also a key player, though it typically follows the commercial sector in terms of market size and growth. Homeowners are increasingly adopting energy-efficient systems, such as LED lighting, smart appliances, and improved HVAC systems, to reduce their energy bills and improve comfort. Rising awareness of climate change and the benefits of sustainable living are also driving demand in the residential market. Additionally, government initiatives like tax credits and rebates for energy-efficient home improvements are encouraging more consumers to invest in retrofitting. However, the residential market is generally slower to adopt compared to commercial spaces due to the lower frequency of upgrades and the smaller scale of investment.

The institutional segment, which includes schools, hospitals, government buildings, and other public sector facilities, is a smaller but important part of the energy retrofit systems market. This segment often receives public funding or grants for retrofitting projects and is driven by both the need for cost savings and environmental goals. Institutions, especially schools and healthcare facilities, have large energy demands for lighting, heating, cooling, and operational needs, making them prime candidates for energy retrofits. However, the adoption rate is typically slower than the commercial and residential sectors due to budget constraints, complex decision-making processes, and the longer approval times associated with public sector projects.

Energy Retrofit Systems Market: Regional Insights

- North America is expected to dominates the global market

North America leads the energy retrofit systems market, driven by strong government policies promoting energy efficiency, sustainability, and carbon reduction. The United States, in particular, is a key player due to its extensive commercial and residential building stock, which requires retrofitting to meet energy efficiency standards. Additionally, various states have enacted energy efficiency mandates that encourage the adoption of retrofit systems. This region also benefits from significant investments in green building technologies and growing awareness about the long-term cost savings of energy-efficient upgrades.

Europe holds a prominent position in the energy retrofit systems market, with the European Union’s aggressive climate action plans pushing for a reduction in energy consumption and CO2 emissions. The region’s commitment to energy-efficient buildings is supported by favorable regulations, such as the Energy Performance of Buildings Directive (EPBD). Countries like Germany, the UK, and France are particularly advanced in their energy retrofit efforts, incentivizing the installation of energy-saving technologies in both residential and commercial sectors. European cities are seeing high demand for energy-efficient upgrades, especially in aging infrastructure.

Asia-Pacific is experiencing significant growth in the energy retrofit systems market, with China and India being key contributors. The rapid urbanization in countries like China, India, and Japan has led to a growing demand for energy-efficient buildings and retrofitting solutions. Government initiatives and programs focused on sustainability, combined with rising energy prices and environmental concerns, are fueling market growth. This region is expected to witness a surge in retrofit projects, particularly in emerging economies, as governments focus on improving energy consumption patterns in the built environment.

The Middle East and Africa are showing an emerging interest in energy retrofit systems, with increasing adoption in countries such as the UAE and Saudi Arabia. The region's high energy consumption rates, coupled with a strong push for energy efficiency due to economic diversification efforts, are driving market growth. Government incentives and a rising focus on sustainable development are expected to accelerate the retrofitting of buildings, particularly in commercial sectors. However, the market is still in its early stages, with considerable potential for future expansion.

Latin America’s energy retrofit systems market is growing at a slower pace compared to other regions. Countries like Brazil and Mexico are showing interest in retrofitting as part of broader sustainability and climate goals. However, limited funding, regulatory frameworks, and awareness about the benefits of retrofitting have slowed down widespread adoption. Despite these challenges, there is growing potential as energy efficiency becomes a more prominent focus, especially in urban centers looking to reduce energy consumption and emissions.

Recent Developments:

- In January 2024, Danfoss partnered with Google to enhance energy efficiency in data centers. Google will utilize Danfoss' heat reuse modules to capture and repurpose heat from data centers for renewable on-site heating and to supply nearby buildings, communities, and industries.

- In January 2024, Honeywell teamed up with NXP to integrate NXP's neural network-enabled, industrial-grade processors into Honeywell's building management systems (BMS).

Energy Retrofit Systems Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the energy retrofit systems market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global energy retrofit systems market include:

- AECOM Energy

- Daikin Industries

- Johnson Controls

- Orion Energy Systems

- Schneider Electric

- Ameresco

- Chevron Energy Solutions

- Eaton

- Philips Lighting

- Trane

- Ballard Power Systems

- Plug Power Inc

- ITM Power PLC

- Intelligent Energy Limited

- ElringKlinger AG

- Infinity Fuel Cell and Hydrogen, Inc.

- Doosan Fuel Cell Co., Ltd.

- Toshiba Corporation

- Loop energy

- Pragma Industries

- SFC Energy AG

- Shanghai Shenli Technology Co. Ltd.

- W. L. Gore & Associates

- PowerCell Sweden AB

- Cummins Inc.

- AVL

- Nedstack Fuel Cell Technology BV

- Horizon Fuel Cell Technologies

- Altergy

- NUVERA FUEL CELLS LLC

The global energy retrofit systems market is segmented as follows:

By Type

- Envelope

- LED Retrofit Lighting

- HVAC Retrofit

- Appliances

By Application

- Residential

- Single-family

- Apartments / Condominiums

- Commercial

- Food sales & service

- Mercantile

- Office Buildings

- Warehouse

- Others

- Institutional

- Education

- Healthcare

- Worship Buildings

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global energy retrofit systems market size was projected at approximately US$ 2.68 billion in 2023. Projections indicate that the market is expected to reach around US$ 4.72 billion in revenue by 2032.

The global energy retrofit systems market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 6.50% during the forecast period from 2024 to 2032.

North America is expected to dominate the global energy retrofit systems market.

The global energy retrofit systems market is driven by the increasing demand for energy efficiency, rising energy costs, and government regulations promoting sustainability. Additionally, technological advancements in energy-efficient solutions and growing awareness of environmental impact further fuel market growth.

Some of the prominent players operating in the global energy retrofit systems market are; AECOM Energy, Daikin Industries, Johnson Controls, Orion Energy Systems, Schneider Electric, Ameresco, Chevron Energy Solutions, Eaton, Philips Lighting, Trane, Ballard Power Systems, Plug Power Inc, ITM Power PLC, Intelligent Energy Limited, ElringKlinger AG, Infinity Fuel Cell and Hydrogen Inc., Doosan Fuel Cell Co. Ltd., Toshiba Corporation, Loop energy, Pragma Industries, SFC Energy AG, Shanghai Shenli Technology Co. Ltd., W. L. Gore & Associates, PowerCell Sweden AB, Cummins Inc., AVL, Nedstack Fuel Cell Technology BV, Horizon Fuel Cell Technologies, Altergy, NUVERA FUEL CELLS LLC, and others.

Table Of Content

Inquiry For Buying

Energy Retrofit Systems

Request Sample

Energy Retrofit Systems