Fatigue Management Software Market Size, Share, and Trends Analysis Report

CAGR :

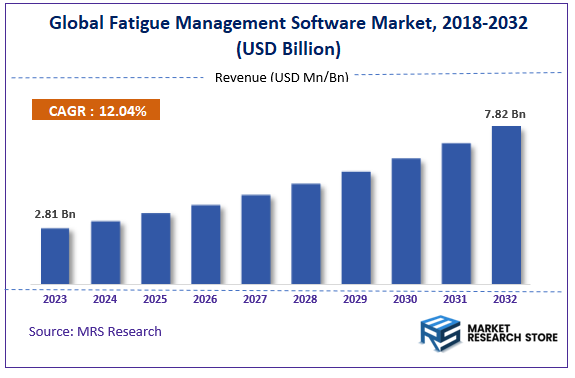

| Market Size 2023 (Base Year) | USD 2.81 Billion |

| Market Size 2032 (Forecast Year) | USD 7.82 Billion |

| CAGR | 12.04% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

According to Market Research Store, the global fatigue management software market size was valued at around USD 2.81 billion in 2023 and is estimated to reach USD 7.82 billion by 2032, to register a CAGR of approximately 12.04% in terms of revenue during the forecast period 2024-2032.

To Get more Insights, Request a Free Sample

The fatigue management software report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Fatigue Management Software Market: Overview

The Fatigue Management Software Market focuses on providing digital solutions designed to monitor, manage, and mitigate fatigue risks among workers, particularly in industries such as transportation, aviation, manufacturing, and healthcare. These software solutions help organizations track employee working hours, rest periods, and overall well-being to reduce fatigue-related accidents and improve safety standards. Fatigue management software typically incorporates features like real-time monitoring, predictive analytics, health assessments, and compliance tracking with legal working hour regulations.

Key Highlights

- The fatigue management software market is anticipated to grow at a CAGR of 12.04% during the forecast period.

- The global fatigue management software market was estimated to be worth approximately USD 2.81 billion in 2023 and is projected to reach a value of USD 7.82 billion by 2032.

- The growth of the fatigue management software market is being driven by the increasing need to improve worker safety, productivity, and overall well-being.

- Based on the product, the cloud-based segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the healthcare and life sciences segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Fatigue Management Software Market: Dynamics

Key Growth Drivers

- Increasing Workplace Fatigue: Rising workload, long work hours, and sedentary lifestyles contribute to increased fatigue, impacting productivity and employee well-being.

- Safety Concerns: Fatigue-related accidents and incidents, particularly in industries like transportation and manufacturing, highlight the need for effective fatigue management.

- Regulatory Compliance: Stringent regulations regarding worker fatigue, such as those in the transportation industry, mandate the use of fatigue management solutions.

- Remote Work and Flexible Schedules: The rise of remote work and flexible schedules can make it difficult to monitor and manage employee fatigue.

Restraints

- High Initial Investment: Implementing fatigue management software can involve significant upfront costs, including hardware, software, and training.

- Data Privacy and Security Concerns: Collecting and storing employee data, especially biometric data, raises privacy and security concerns.

- User Adoption and Resistance: Encouraging employees to use fatigue management tools and wearables can be challenging, especially if they perceive it as intrusive.

- Complex Integration with Existing Systems: Integrating fatigue management software with existing HR, payroll, and safety systems can be complex and time-consuming.

Opportunities

- Real-Time Monitoring and Alerting: Real-time monitoring of employee fatigue levels and alerting managers to potential risks.

- Personalized Fatigue Management: Tailoring fatigue management strategies to individual employee needs and preferences.

- Integration with Wearable Devices: Leveraging wearable devices to track vital signs and physical activity to assess fatigue levels.

- Predictive Analytics: Using AI and machine learning to predict fatigue-related incidents and proactively implement preventive measures.

Challenges

- Accuracy of Fatigue Assessment: Accurately measuring and assessing fatigue levels can be challenging, especially in complex work environments.

- Cultural and Individual Differences: Cultural and individual differences in fatigue perception and tolerance can impact the effectiveness of fatigue management strategies.

- Data Privacy and Security: Protecting sensitive employee data, such as biometric information, is essential.

- Continuous Improvement: As workplace dynamics and technology evolve, fatigue management solutions need to be continuously updated and improved.

Fatigue Management Software Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Fatigue Management Software Market |

| Market Size in 2023 | USD 2.81 Billion |

| Market Forecast in 2032 | USD 7.82 Billion |

| Growth Rate | CAGR of 12.04% |

| Number of Pages | 224 |

| Key Companies Covered | Boeing, Ceridian, Circadian, EDP Software, Fatigue Management International, Fatigue Manager, Fatigue Science, InterDynamics, Mosaic Management Systems, Optalert Limited, Quinyx, RITEQ, Signal, Tambla Limited, Work Technology Corporation, WorkForce Software, Zurich, and others. |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Fatigue Management Software Market: Segmentation Insights

The global fatigue management software market is divided by product, application, and region.

Segmentation Insights by Product

Based on Product, the global fatigue management software market is divided into cloud-based, on-premise, and others.

The Cloud-Based segment is the dominant product in the fatigue management software market. This is primarily driven by the increasing adoption of cloud computing, the shift toward digitalization, and the growing demand for flexible, scalable solutions that can be accessed remotely. Cloud-based fatigue management software is hosted on remote servers and accessed via the internet.

While the On-Premise segment holds a notable share in the market, its growth has slowed in recent years due to the increasing preference for cloud-based solutions. However, it still remains popular in industries that prioritize data security and have existing IT infrastructure capable of supporting the software. On-premise fatigue management software refers to solutions that are installed and operated locally on a company’s own servers and IT infrastructure.

Segmentation Insights by Application

On the basis of Application, the global fatigue management software market is bifurcated into healthcare and life sciences, BFSI, it and telecommunications, government and public sector, retail and consumer goods, manufacturing, and others.

The Healthcare and Life Sciences sector dominates the elastomeric closure components market by a significant margin. The primary driver for this dominance is the large-scale use of elastomeric closures in the pharmaceutical, biotechnology, and healthcare industries, where injectable drugs, biologics, and vaccines require airtight and secure seals. The healthcare and life sciences sector holds the largest share in the elastomeric closure components market, driven by the significant demand for injectable drugs and biologic therapies.

The BFSI sector focuses on financial institutions, banking services, insurance, and investment firms. This sector holds a minimal share in the elastomeric closure components market, as it is not a direct end-user of such products, but related applications such as health services or insurance companies’ involvement in medical or pharmaceutical products may indirectly drive some demand.

The IT and Telecommunications sector holds a very small share in this market, as it does not directly use elastomeric closure components for the majority of its applications. In IT and telecommunications, elastomeric closures play a minimal role. However, these industries may indirectly drive demand through the production of medical devices and telemedicine products that require injectable solutions, such as vaccines and biologic drugs for remote treatment or diagnostics.

The Government and Public Sector hold a moderate share in the market, particularly through health initiatives such as immunization programs, government-funded healthcare, and hospital supplies. This sector plays a significant role in the healthcare industry, especially in the provision of vaccines, biologic drugs, and medical supplies for public health initiatives.

The Retail and Consumer Goods sector involves packaged products sold directly to consumers, including health supplements and over-the-counter injectable medications. The market share for retail and consumer goods is moderate but growing, especially with the rise of self-administered health products such as pre-filled syringes and home healthcare devices.

The Manufacturing sector uses elastomeric closure components in various industrial applications, particularly in the pharmaceutical and biotechnology industries. This sector holds a significant share of the market due to its close connection to the production of pharmaceutical products. The growing demand for injectables and biologics boosts the need for elastomeric closures in manufacturing settings.

Fatigue Management Software Market: Regional Insights

- North America currently leads the global fatigue management software market

North America dominates the fatigue management software market, driven by stringent workplace safety regulations and the high adoption of technology in industries such as transportation, healthcare, and manufacturing. The U.S. is the largest contributor, with organizations focusing on compliance with regulations like the Federal Motor Carrier Safety Administration (FMCSA) hours-of-service rules and Occupational Safety and Health Administration (OSHA) guidelines. The strong presence of key players and the high awareness of the impact of fatigue on workplace safety further propel market growth. Canada also contributes significantly, particularly in the aviation and logistics sectors.

Europe holds a significant share of the market, driven by its strong emphasis on workplace safety and employee health. Countries like Germany, the UK, and France are leading adopters, particularly in industries such as manufacturing, transportation, and energy. The European Union's stringent labor laws and fatigue risk management frameworks encourage the use of software to ensure compliance and reduce risks. The region’s increasing adoption of digital technologies in workplace management also contributes to the market’s growth.

The Asia Pacific region is the fastest-growing market for fatigue management software, with countries like China, India, Japan, and Australia leading the way. The rapid industrialization and growth of sectors like logistics, aviation, and healthcare drive the demand for solutions that enhance workforce safety and productivity. Australia, with its strong mining and transportation industries, has been an early adopter of fatigue management technologies. In emerging economies like China and India, increasing awareness of workplace safety and the adoption of automation and workforce management tools are boosting market growth.

Latin America is an emerging market for fatigue management software, with Brazil and Mexico being the primary contributors. The region’s growing logistics, transportation, and manufacturing sectors are driving the demand for tools to ensure worker safety and operational efficiency. However, the market is still in its nascent stages due to limited awareness and slower adoption of advanced workforce management technologies.

The Middle East and Africa (MEA) region is gradually adopting fatigue management software, especially in sectors like oil & gas, mining, and transportation. The Middle East, particularly the UAE and Saudi Arabia, is investing in workforce safety technologies as part of broader efforts to modernize industries. In Africa, the focus is on improving safety in mining and transportation, though adoption rates are hindered by infrastructural challenges and budget constraints.

Fatigue Management Software Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the fatigue management software market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global fatigue management software market include:

- Boeing

- Ceridian

- Circadian

- EDP Software

- Fatigue Management International

- Fatigue Manager

- Fatigue Science

- InterDynamics

- Mosaic Management Systems

- Optalert Limited

- Quinyx

- RITEQ

- Signal

- Tambla Limited

- Work Technology Corporation

- WorkForce Software

- Zurich

The global fatigue management software market is segmented as follows:

By Product

- Cloud-Based

- On-Premise

By Application

- Healthcare and Life Sciences

- BFSI

- IT and Telecommunications

- Government and Public Sector

- Retail and Consumer Goods

- Manufacturing

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global fatigue management software market size was projected at approximately US$ 2.81 billion in 2023. Projections indicate that the market is expected to reach around US$ 7.82 billion in revenue by 2032.

The global fatigue management software market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 12.04% during the forecast period from 2024 to 2032.

North America is expected to dominate the global fatigue management software market.

The global fatigue management software market is primarily driven by factors such as increasing safety concerns in industries like transportation, healthcare, and manufacturing, stringent government regulations regarding work hours and fatigue-related accidents, and the growing need to improve employee productivity and well-being.

Some of the prominent players operating in the global fatigue management software market are; Boeing, Ceridian, Circadian, EDP Software, Fatigue Management International, Fatigue Manager, Fatigue Science, InterDynamics, Mosaic Management Systems, Optalert Limited, Quinyx, RITEQ, Signal, Tambla Limited, Work Technology Corporation, WorkForce Software, Zurich, and others.

Table Of Content

Inquiry For Buying

Fatigue Management Software

Request Sample

Fatigue Management Software