LNG Tanker Market Size, Share, and Trends Analysis Report

CAGR :

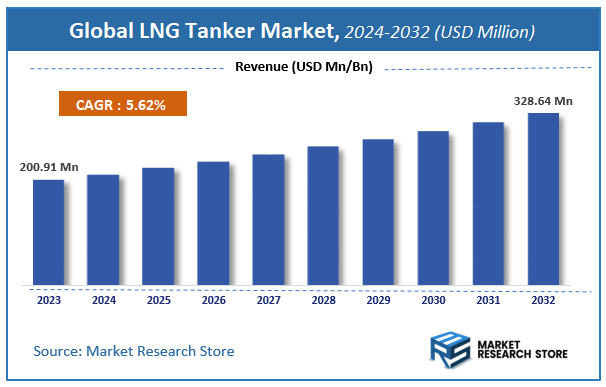

| Market Size 2023 (Base Year) | USD 200.91 Million |

| Market Size 2032 (Forecast Year) | USD 328.64 Million |

| CAGR | 5.62% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

LNG Tanker Market Insights

According to Market Research Store, the global LNG tanker market size was valued at around USD 200.91 million in 2023 and is estimated to reach USD 328.64 million by 2032, to register a CAGR of approximately 5.62% in terms of revenue during the forecast period 2024-2032.

The LNG tanker report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global LNG Tanker Market: Overview

An LNG (Liquefied Natural Gas) tanker is a specialized marine vessel designed for the safe and efficient transportation of liquefied natural gas across long distances. LNG is natural gas that has been cooled to approximately -162°C (-260°F), turning it into a liquid to reduce its volume by about 600 times for easier storage and transport. LNG tankers are equipped with cryogenic tanks, typically made of special materials like aluminum or stainless steel, and insulated to maintain the extremely low temperatures required. These vessels come in different types such as Moss-type (spherical tanks), membrane-type (integrated with the hull), and more recently, hybrid or advanced containment systems that offer improved efficiency and safety. The operation of LNG tankers is highly regulated due to the flammable nature of the cargo, requiring advanced navigation systems, safety protocols, and trained personnel.

Key Highlights

- The LNG tanker market is anticipated to grow at a CAGR of 5.62% during the forecast period.

- The global LNG tanker market was estimated to be worth approximately USD 200.91 million in 2023 and is projected to reach a value of USD 328.64 million by 2032.

- The growth of the LNG tanker market is being driven by rising global demand for cleaner energy alternatives and increased natural gas production.

- Based on the vessel type, the conventional LNG tankers segment is growing at a high rate and is projected to dominate the market.

- On the basis of cargo capacity, the large-scale LNG carriers (160,000–220,000 cubic meters) segment is projected to swipe the largest market share.

- In terms of end user, the LNG export & import terminals segment is expected to dominate the market.

- Based on the application, the transportation of LNG segment is expected to dominate the market.

- In terms of ownership type, the charter owned LNG carrier segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

LNG Tanker Market: Dynamics

Key Growth Drivers:

- Rising Global Demand for Natural Gas: As countries shift toward cleaner energy sources, natural gas consumption is increasing, boosting the need for LNG transportation via tankers.

- Expansion of LNG Export Facilities: Growth in LNG production and export facilities, particularly in the U.S., Qatar, and Australia, is driving demand for more LNG tankers.

- Improved LNG Infrastructure Worldwide: Development of LNG import terminals in Asia and Europe supports the growth of global LNG trade, necessitating more shipping capacity.

- Technological Advancements in Tanker Design: Modern LNG tankers are more efficient and safer, making them attractive investments for shipping companies and boosting fleet growth.

Restraints:

- High Construction and Operational Costs: LNG tankers are expensive to build and operate, which can limit fleet expansion and deter new entrants.

- Stringent Environmental Regulations: Emission and safety regulations increase operational complexity and compliance costs for LNG tanker operators.

- Limited Availability of Skilled Workforce: Operating and maintaining LNG tankers requires specialized skills, and workforce shortages can pose operational challenges.

Opportunities:

- Emerging LNG Import Markets: Growing energy needs in countries like India, China, and Southeast Asian nations create new demand for LNG shipments and tanker deployment.

- Fleet Modernization and Retrofitting: The need to replace aging vessels with modern, eco-friendly designs opens up opportunities for shipbuilders and LNG logistics firms.

- Growth in Floating LNG Projects: Development of floating LNG production and storage units is creating new logistics needs, boosting demand for specialized LNG tankers.

Challenges:

- Market Volatility and Geopolitical Risks: Fluctuating LNG prices and political instability in key supply regions can disrupt trade routes and affect tanker utilization.

- Port Infrastructure Limitations: Not all ports are equipped to handle large LNG tankers, limiting route flexibility and increasing transit time.

- Overcapacity Risk: Sudden oversupply of tankers, due to over-ordering during demand booms, can lead to reduced freight rates and idle ships.

LNG Tanker Market: Report Scope

This report thoroughly analyzes the LNG Tanker Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | LNG Tanker Market |

| Market Size in 2023 | USD 200.91 Million |

| Market Forecast in 2032 | USD 328.64 Million |

| Growth Rate | CAGR of 5.62% |

| Number of Pages | 184 |

| Key Companies Covered | Samsung Heavy Industries, Mitsubishi Heavy Industries, Hyundai Heavy Industries, DSME, Mitsui OSK Lines, NYK Lines, Yamal |

| Segments Covered | By Vessel Type, By Cargo Capacity, By End User, By Application, By Ownership Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

LNG Tanker Market: Segmentation Insights

The global LNG tanker market is divided by vessel type, cargo capacity, end user, application, ownership type, and region.

Segmentation Insights by Vessel Type

Based on vessel type, the global LNG tanker market is divided into conventional LNG tankers, floating storage & regasification units (FSRUs), membrane tank LNG carriers, moss type LNG carriers, and semi-submersible LNG carriers.

In the LNG tanker market, Conventional LNG Tankers dominate the segment landscape due to their widespread use in transporting liquefied natural gas across long distances between liquefaction plants and regasification terminals. These vessels have well-established infrastructure, large cargo capacities (typically between 125,000 to 266,000 cubic meters), and are the industry standard for LNG trade. Their reliability, compatibility with most LNG ports, and mature technology contribute to their dominant market share.

Membrane Tank LNG Carriers follow closely as a highly favored design type among new builds due to their efficient use of space, lighter weight, and ability to accommodate more LNG cargo within a given hull size. The membrane containment system, commonly designed by GTT (Gaztransport & Technigaz), offers improved insulation and reduced boil-off rates, making them particularly attractive for modern fleets prioritizing efficiency and performance.

Moss Type LNG Carriers, recognized for their spherical tanks, were once prevalent due to their robustness and high safety margins. However, they occupy more space and have a higher center of gravity compared to membrane tankers, leading to their gradual decline in popularity. Despite this, they still hold a noticeable share of the market, particularly in regions and terminals where infrastructure was designed around their unique specifications.

Floating Storage & Regasification Units (FSRUs) are increasingly significant but remain a niche in comparison to conventional carriers. They combine storage and regasification capabilities onboard, making them ideal for regions lacking onshore infrastructure. Their flexibility and faster deployment make them attractive for emerging markets, though their overall market share remains limited compared to standard transport-focused tankers.

Semi-Submersible LNG Carriers represent the smallest share in the market. These specialized vessels are engineered to carry LNG modules or enable offshore offloading in challenging environments, but they are used in highly specific scenarios. Their high costs, complexity, and limited operational track record restrict their deployment, keeping them as the least dominant segment within the LNG tanker landscape.

Segmentation Insights by Cargo Capacity

On the basis of cargo capacity, the global LNG tanker market is bifurcated into small-scale LNG carriers (up to 30,000 cubic meters), mid-scale LNG carriers (30,000160,000 cubic meters), large-scale LNG carriers (160,000220,000 cubic meters), and ultra large LNG carriers (over 220,000 cubic meters).

In the LNG tanker market segmentation by cargo capacity, Large-Scale LNG Carriers (160,000–220,000 cubic meters) hold the dominant position. These vessels form the backbone of the global LNG transportation fleet due to their optimal balance between cargo volume, operational cost-efficiency, and compatibility with most LNG terminals worldwide. Their large capacity supports long-haul intercontinental routes, making them the go-to choice for major LNG producers and importers.

Mid-Scale LNG Carriers (30,000–160,000 cubic meters) come next in terms of market share. These vessels serve medium-distance trade routes and are often used in regional or niche markets where port infrastructure cannot support larger carriers. Their flexibility and maneuverability make them suitable for emerging LNG markets, island nations, and smaller gas-to-power projects, contributing to their growing importance in the market.

Ultra Large LNG Carriers (over 220,000 cubic meters) are a more recent addition to the market, designed to meet the rising global demand for LNG and enhance economies of scale. Although fewer in number, these vessels are increasingly being adopted on high-volume routes, particularly where port infrastructure has been upgraded to accommodate their immense size. However, their share remains lower due to the limited number of terminals that can handle such large ships and the high capital investment required.

Small-Scale LNG Carriers (up to 30,000 cubic meters) occupy the smallest share of the market. They are primarily used for short-distance, localized supply, including LNG bunkering, distribution to remote or off-grid areas, and supplying smaller industrial or residential customers. Despite their limited cargo capacity, they play a critical role in developing small-scale LNG infrastructure and promoting LNG use in marine and transport sectors. Their growth is steady but remains niche compared to the larger carrier categories.

Segmentation Insights by End User

Based on end user, the global LNG tanker market is divided into power generation companies, industrial utilities, shipping companies, gas distribution companies, and LNG export & import terminals.

In the LNG tanker market segmentation by end user, LNG Export & Import Terminals are the most dominant end users. These facilities form the foundation of the global LNG supply chain, serving as critical nodes for loading and offloading LNG tankers. Export terminals prepare and liquefy natural gas for shipment, while import terminals receive LNG, store it, and often regasify it for further distribution. Their central role in global LNG logistics makes them the largest and most consistent consumers of LNG tanker services.

Power Generation Companies follow as the second most significant end-user group. Many countries rely on LNG for generating electricity, especially those transitioning away from coal and oil. LNG’s relatively lower carbon emissions and stable supply appeal to power utilities aiming to meet both energy demand and regulatory requirements. This segment has grown rapidly in regions like Asia-Pacific, the Middle East, and parts of Europe where LNG-fired power plants are expanding.

Industrial Utilities represent the next largest segment. These include heavy industries such as chemicals, cement, steel, and manufacturing facilities that use LNG as a feedstock or fuel. The flexibility of LNG in providing cleaner, high-efficiency energy for industrial processes has fueled growth in this segment, particularly in areas without access to piped natural gas.

Gas Distribution Companies are increasingly leveraging LNG to extend natural gas supply networks to areas not connected by pipelines. They use LNG tankers to transport gas to satellite storage and regasification units, often serving residential, commercial, and small industrial users. While important for expanding LNG accessibility, this segment is smaller compared to large-scale users like power plants and export terminals.

Shipping Companies, which use LNG tankers for LNG bunkering and as fuel for their own fleets, form the smallest segment. Although the use of LNG as marine fuel is on the rise due to IMO regulations and decarbonization goals, the total number of LNG-fueled vessels is still relatively small. As adoption increases, this segment is expected to grow steadily, but currently remains the least dominant in the LNG tanker market.

Segmentation Insights by Application

On the basis of application, the global LNG tanker market is bifurcated into transportation of LNG, temporary storage of LNG, regasification services, supply to marine fuel, and export & import of LNG.

In the LNG tanker market by application, Transportation of LNG is the most dominant segment. LNG tankers are primarily designed to move liquefied natural gas from production/export terminals to receiving/import terminals across long international routes. This core function supports the entire LNG value chain, facilitating global trade and meeting the energy demands of nations without local gas supplies. The sheer volume of LNG being shipped worldwide ensures this remains the primary application of LNG tankers.

Export & Import of LNG ranks second, closely tied to transportation but emphasizing the logistical operations at both ends of the LNG journey. This application includes loading, offloading, customs processing, and terminal services. As global LNG trade expands, more countries are investing in export and import infrastructure, increasing demand for tankers to serve these functions. It plays a vital role in energy security and international energy commerce.

Temporary Storage of LNG follows next in importance. LNG tankers, particularly Floating Storage Units (FSUs) or Floating Storage and Regasification Units (FSRUs), are increasingly being used as cost-effective temporary storage options when onshore storage is limited or during peak seasonal demand. Their mobility and ability to serve multiple markets over time provide flexibility and strategic value.

Regasification Services represent a more specialized application, typically involving FSRUs that are equipped not just for storage but also for converting LNG back into gaseous form onboard. This application supports quicker deployment of LNG access, especially in regions lacking permanent onshore regasification facilities. While critical for certain markets, the global volume of such applications is comparatively smaller than core transport functions.

Supply to Marine Fuel is currently the least dominant application. While LNG is gaining traction as a cleaner alternative to traditional marine fuels due to stricter emissions regulations, the infrastructure and number of vessels using LNG for propulsion are still developing. LNG bunkering via small-scale LNG tankers is growing, particularly in ports with high traffic and environmental regulations, but remains a niche application in the broader tanker market.

Segmentation Insights by Ownership Type

On the basis of ownership type, the global LNG tanker market is bifurcated into single owned LNG carriers, multi owned LNG carriers, charter owned LNG carriers, fleet management & operations (third-party operators), and joint ventures & partnerships.

In the LNG tanker market by ownership type, Charter Owned LNG Carriers hold the dominant position. These vessels are typically owned by shipowners or leasing companies and are chartered to LNG suppliers, utilities, or traders under long-term or short-term contracts. This model offers flexibility to charterers without bearing the capital-intensive burden of owning and maintaining vessels. It is especially popular among energy companies and utilities that prefer to focus on core operations while ensuring stable LNG supply and logistics.

Fleet Management & Operations (Third-Party Operators) come next in terms of market presence. These are vessels managed by specialized shipping companies on behalf of owners. Third-party operators handle everything from crewing and technical management to compliance and performance optimization. This structure benefits owners who lack in-house expertise or seek operational efficiency. The growing complexity of LNG shipping, including stricter regulations and technical demands, has led to increased reliance on professional fleet managers.

Joint Ventures & Partnerships are also a significant segment. Many LNG carriers are co-owned by multiple stakeholders such as national oil companies, shipping lines, and energy consortia. These partnerships spread investment risk, ensure strategic alignment (especially in geopolitically sensitive routes), and secure long-term LNG supply chain integration. Such joint structures are particularly common in large-scale LNG projects or between LNG exporters and importers.

Single Owned LNG Carriers represent a smaller portion of the market. These are vessels owned and operated by a single entity, often large, vertically integrated LNG companies or national carriers with sufficient resources. While this allows for tighter control and long-term fleet strategy, the high upfront costs and ongoing operational requirements make it less common for smaller players.

Multi Owned LNG Carriers are the least dominant in the market. These involve more fragmented ownership structures, often with multiple private or institutional investors sharing stakes in a vessel. While such models can reduce individual financial exposure, they can introduce complexities in decision-making, revenue sharing, and operational alignment. As a result, this ownership type is less favored for large-scale or long-term LNG transportation needs.

LNG Tanker Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific is the most dominant region in the global LNG tanker market. This dominance is driven by high LNG import volumes from countries like China, Japan, and South Korea. China’s transition toward cleaner energy sources and Japan’s long-standing reliance on LNG have significantly increased the demand for LNG carriers. Additionally, the region is experiencing rapid industrialization and infrastructure development, including LNG-fueled transportation systems and expanded regasification terminals, which further enhance the need for efficient LNG tanker fleets.

North America follows closely due to its expanding LNG export capabilities, particularly from the United States. The region benefits from abundant shale gas reserves and significant investments in liquefaction terminals along the Gulf Coast. These developments have positioned the U.S. as one of the top LNG exporters globally. LNG carriers from North America are increasingly utilized to meet demand in both Asia and Europe, strengthening the region’s strategic importance in the global LNG supply network.

Europe plays a key role in the LNG tanker market due to its heightened focus on energy diversification and security. The region has accelerated LNG imports as an alternative to pipeline gas, especially amid geopolitical uncertainties. Investment in new LNG terminals and floating storage units reflects Europe’s commitment to bolstering its LNG infrastructure. Although overall gas demand has seen some fluctuations, Europe's LNG import strategies continue to drive tanker utilization.

Middle East and Africa serve as major LNG exporters, with countries like Qatar at the forefront of global supply. The region’s proximity to high-demand markets in Asia and Europe offers logistical advantages. Additionally, emerging African exporters such as Mozambique and Nigeria are increasing their presence through offshore projects and liquefaction capacity expansions. These developments are contributing to higher demand for LNG tankers originating from the region.

Latin America represents a smaller but growing segment of the LNG tanker market. Countries such as Brazil and Argentina rely on LNG imports to supplement domestic energy production, especially during seasonal shortages. Infrastructure upgrades, including regasification terminals and storage facilities, are enabling increased LNG handling capacity. While the region does not match the scale of larger markets, its evolving energy landscape is gradually boosting LNG tanker activity.

LNG Tanker Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the LNG tanker market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global LNG tanker market include:

- Samsung Heavy Industries

- Mitsubishi Heavy Industries

- Hyundai Heavy Industries

- DSME

- Mitsui OSK Lines

- NYK Lines

- Yamal

The global LNG tanker market is segmented as follows:

By Vessel Type

- Conventional LNG Tankers

- Floating Storage and Regasification Units (FSRUs)

- Membrane Tank LNG Carriers

- Moss Type LNG Carriers

- Semi-Submersible LNG Carriers

By Cargo Capacity

- Small-Scale LNG Carriers (up to 30

- 000 cubic meters)

- Mid-Scale LNG Carriers (30

- 000160

- 000 cubic meters)

- Large-Scale LNG Carriers (160

- 000220

- 000 cubic meters)

- Ultra Large LNG Carriers (over 220

- 000 cubic meters)

By End User

- Power Generation Companies

- Industrial Utilities

- Shipping Companies

- Gas Distribution Companies

- LNG Export and Import Terminals

By Application

- Transportation of LNG

- Temporary Storage of LNG

- Regasification Services

- Supply to Marine Fuel

- Export and import of LNG

By Ownership Type

- Single Owned LNG Carriers

- Multi Owned LNG Carriers

- Charter owned LNG Carriers

- Fleet Management and Operations (Third-party Operators)

- Joint Ventures and Partnerships

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

LNG Tanker

Request Sample

LNG Tanker