Mining Chemicals Market Size, Share, and Trends Analysis Report

CAGR :

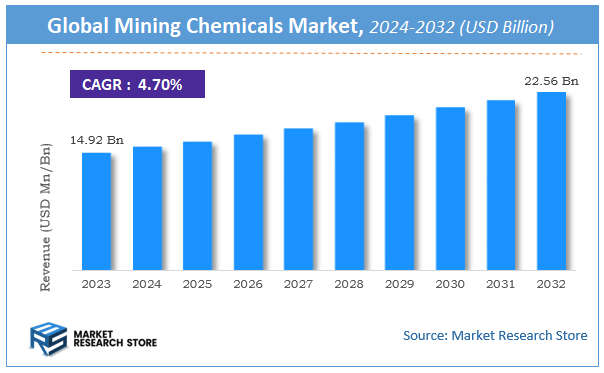

| Market Size 2023 (Base Year) | USD 14.92 Billion |

| Market Size 2032 (Forecast Year) | USD 22.56 Billion |

| CAGR | 4.7% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Mining Chemicals Market Insights

According to Market Research Store, the global mining chemicals market size was valued at around USD 14.92 billion in 2023 and is estimated to reach USD 22.56 billion by 2032, to register a CAGR of approximately 4.7% in terms of revenue during the forecast period 2024-2032.

The mining chemicals report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Mining Chemicals Market: Overview

Mining chemicals are specialized reagents and compounds used throughout the mineral extraction and processing chain to enhance the efficiency, selectivity, and environmental performance of mining operations. These chemicals play a critical role in processes such as mineral flotation, solid-liquid separation, leaching, grinding, and tailings management. Common types include collectors, frothers, flocculants, depressants, dispersants, solvent extractants, and pH modifiers. They are essential for extracting metals like copper, gold, nickel, zinc, and rare earth elements from complex ores, improving yield and purity while reducing energy and water consumption.

The growth of the mining chemicals market is driven by increasing demand for metals and minerals from industries such as construction, electronics, automotive, and renewable energy. As ore grades decline and mining becomes more geologically and environmentally challenging, the use of highly efficient and selective chemical solutions is becoming critical to maintain productivity and compliance.

Key Highlights

- The mining chemicals market is anticipated to grow at a CAGR of 4.7% during the forecast period.

- The global mining chemicals market was estimated to be worth approximately USD 14.92 billion in 2023 and is projected to reach a value of USD 22.56 billion by 2032.

- The growth of the mining chemicals market is being driven by increasing global demand for minerals and metals, coupled with the rising complexity of ore bodies that require advanced chemical solutions for efficient extraction and processing.

- Based on the product type, the grinding aids segment is growing at a high rate and is projected to dominate the market.

- On the basis of mineral type, the non-metallic minerals segment is projected to swipe the largest market share.

- In terms of application, the mineral processing segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Mining Chemicals Market: Dynamics

Key Growth Drivers:

- Growing Demand for Minerals and Metals: The increasing global demand for various minerals and metals (e.g., copper for electrification, lithium for EV batteries, iron ore for steel, gold for investment) driven by population growth, urbanization, industrialization, and the energy transition, is the primary force behind the mining chemicals market. As mining output increases, so does the consumption of chemicals needed for extraction and processing.

- Declining Ore Grades: As high-grade ore deposits become depleted, mining companies are increasingly processing lower-grade ores. This necessitates the use of more sophisticated and higher volumes of mining chemicals to effectively extract minerals from less concentrated raw materials, driving market demand.

- Focus on Enhanced Mineral Recovery and Efficiency: Mining companies are continuously seeking ways to optimize their operations, improve mineral recovery rates, and reduce operational costs. Mining chemicals are critical for achieving these goals by improving flotation efficiency, facilitating separation processes, and reducing energy consumption in grinding.

Restraints:

- Volatility of Commodity Prices: The prices of mined commodities (e.g., copper, gold, iron ore) are highly volatile. When commodity prices decline, mining companies tend to reduce their operational expenditures, including chemical purchases, directly impacting the demand for mining chemicals.

- Environmental Regulations and Disposal Challenges of Chemicals: While some regulations drive demand for greener chemicals, others impose strict limits on the use and disposal of certain chemical compounds, increasing compliance costs and potentially restricting the use of some traditional reagents.

- High Capital Expenditure for Mining Projects: Setting up new mining operations requires massive capital investment. Economic uncertainties, geopolitical risks, and fluctuating commodity prices can lead to delays or cancellations of new projects, thereby restraining the demand for new chemical supplies.

- Supply Chain Disruptions and Logistics: The global nature of the mining chemicals supply chain makes it vulnerable to geopolitical tensions, trade restrictions, and logistical challenges (e.g., transportation to remote mining sites), impacting availability and pricing.

Opportunities:

- Development of Sustainable and Eco-Friendly Mining Chemicals: The strongest opportunity lies in the innovation and commercialization of greener mining chemicals. This includes biodegradable reagents, non-toxic flocculants, and chemicals that reduce water consumption or enable more effective waste treatment, aligning with ESG (Environmental, Social, and Governance) goals.

- Increasing Adoption of Digitalization and Automation: Integrating digital technologies (e.g., AI, IoT, advanced analytics) with chemical dosing and process optimization can lead to more precise chemical usage, reduced waste, and improved efficiency in mineral processing, creating opportunities for "smart" chemical solutions.

- Tailored Chemicals for Complex Ore Bodies: As mining moves to more complex and polymetallic ore bodies, there's a growing need for highly specialized and customized chemical formulations that can selectively extract target minerals from challenging matrices, offering high-value niche opportunities.

Challenges:

- Balancing Performance with Environmental and Safety Standards: The most significant challenge is to continuously develop mining chemicals that offer superior performance (e.g., higher recovery, better selectivity) while simultaneously meeting increasingly stringent environmental and safety regulations, often at competitive costs.

- Managing the Environmental Footprint of Chemical Usage: Despite advancements, the overall environmental footprint of chemical usage in mining (e.g., consumption, residue, disposal) remains a challenge, requiring continuous efforts towards greener chemistry and responsible waste management.

Mining Chemicals Market: Report Scope

This report thoroughly analyzes the Mining Chemicals Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Mining Chemicals Market |

| Market Size in 2023 | USD 14.92 Billion |

| Market Forecast in 2032 | USD 22.56 Billion |

| Growth Rate | CAGR of 4.7% |

| Number of Pages | 150 |

| Key Companies Covered | BASF SE, Georgia Pacific Chemicals LLC, Chang Chun Plastics Co. Ltd., Sumitomo Baketile, Mitsui Chemicals Inc., Momentive Specialty Chemicals Inc. SI Group Sumitomo Bakelite Co., Kolon Industries, Inc. and certain other |

| Segments Covered | By Product, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Mining Chemicals Market: Segmentation Insights

The global mining chemicals market is divided by product type, mineral type, application industry, and region.

Based on product type, the global mining chemicals market is divided into grinding aids, flocculants, frothers, collectors, depressants, and others. Grinding Aids are the dominant segment in the Mining Chemicals Market, primarily due to their indispensable function in enhancing ore comminution during mineral processing. These chemicals reduce the surface tension of the grinding media, thereby preventing the agglomeration of fine particles and improving the efficiency of particle size reduction. This results in better liberation of minerals from ore, which is critical for downstream recovery processes such as flotation or leaching. Grinding aids are especially vital in processing hard ores like iron, copper, and gold, where high grinding energy is required. Their use leads to increased throughput, reduced energy consumption, lower wear on grinding equipment, and improved overall plant productivity. The growing demand for energy efficiency in mining operations and the depletion of high-grade ore reserves are driving the continued adoption of grinding aids across both open-pit and underground mining environments.

On the basis of mineral type, the global mining chemicals market is bifurcated into non-metallic minerals, precious metals, rare earth metals, and base metals. Base Metals are the dominant mineral type segment in the mining chemicals market, primarily because of their widespread use in global industrial applications and the scale at which they are mined. This category includes copper, zinc, lead, nickel, and aluminum—metals that are fundamental to construction, electronics, automotive, and manufacturing industries. Mining chemicals are used extensively in base metal extraction processes such as flotation, leaching, and grinding. Reagents such as collectors, frothers, flocculants, and grinding aids are critical in improving recovery efficiency, increasing metal yields, and enhancing process throughput. The increasing demand for copper and nickel—driven by the growth of renewable energy infrastructure, electric vehicles, and energy storage systems—further fuels chemical consumption in this segment.

In terms of application, the global mining chemicals market is bifurcated into mineral processing, explosives & drilling, water & wastewater treatment, and others. Mineral Processing is the dominant application industry in the mining chemicals market due to its central role in extracting valuable metals and minerals from ores. This segment uses a broad array of chemicals—including grinding aids, flocculants, collectors, frothers, depressants, and dispersants—to enhance the efficiency of key stages like comminution, flotation, and leaching. These reagents are essential for improving ore grade, metal recovery rates, and operational cost-efficiency. With global ore grades declining and deposits becoming more complex, mining operations increasingly rely on high-performance and customized chemical formulations to maintain productivity.

Mining Chemicals Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the mining chemicals market, primarily due to its extensive mining operations, well-regulated industry practices, and strong demand for metal recovery agents and process chemicals. The United States and Canada lead regional consumption, with significant production of copper, gold, silver, and other industrial minerals. Mining chemicals are heavily used in processes such as flotation, heap leaching, and solvent extraction to enhance ore recovery and process efficiency. The region benefits from advanced mining technology, skilled labor, and strict environmental regulations that push for the adoption of more sustainable and biodegradable chemical formulations. Major manufacturers like Solvay, Chevron Phillips, and SNF Group maintain a strong presence in this region. North America's leadership is further reinforced by its investments in rare earths and lithium mining to support clean energy and electric vehicle supply chains.

Europe holds a moderate share in the mining chemicals market, with activities focused in countries such as Russia, Sweden, Poland, and Germany. Although mining activity in Western Europe is limited, Eastern and Northern Europe remain active in the extraction of base metals, precious metals, and industrial minerals. Mining chemicals in Europe are used primarily for flotation, grinding aids, and water treatment. Strict EU environmental regulations promote the use of non-toxic, low-impact chemical solutions, with a focus on reducing tailings and improving water reuse in mining operations. Russia, being resource-rich, plays a key role in the region's mining chemical consumption, especially for gold, coal, and iron ore production. Europe is also involved in mining chemical research for greener alternatives and performance-enhancing additives in mineral processing.

Asia-Pacific is the fastest-growing region in the mining chemicals market, driven by large-scale mining activity and expanding mineral processing operations in China, India, Australia, and Indonesia. China is the world’s largest consumer and producer of several minerals, with extensive use of flotation reagents, solvent extractants, and grinding aids in coal, rare earths, and base metal mining. Australia, with its strong focus on gold, copper, and iron ore, extensively uses mining chemicals in leaching and separation processes. India’s increasing production of coal, bauxite, and iron ore is boosting the demand for flocculants, collectors, and frothers. Regional growth is supported by rising investments in mineral exploration and processing, although environmental compliance varies by country. Increasing awareness of sustainable mining and growing export-oriented production further enhance chemical consumption across the region.

Latin America is a major region for mining chemicals due to its abundant mineral resources and strong mining sector, with leading contributors including Chile, Peru, Brazil, and Mexico. Chile and Peru are global leaders in copper production, where mining chemicals such as flotation collectors, leaching agents, and pH modifiers are extensively used. Brazil’s iron ore and bauxite sectors also generate strong demand for dispersants and dust control chemicals. Despite infrastructure and regulatory challenges, Latin America benefits from foreign direct investment and technological transfers from global mining corporations, which enhances the use of advanced chemical solutions in mineral beneficiation and water treatment. The region’s increasing focus on environmental sustainability and efficient ore recovery further supports market growth for specialty chemicals.

Middle East & Africa are emerging markets in the mining chemicals sector, with strong mineral extraction activities in South Africa, Democratic Republic of Congo (DRC), Ghana, Zambia, and Saudi Arabia. South Africa leads in the production of platinum group metals (PGMs), gold, and coal, driving demand for collectors, depressants, and pH regulators. In sub-Saharan Africa, chemicals are widely used in gold and copper mining, particularly in heap leaching and tailings treatment. The Middle East, notably Saudi Arabia, is expanding its mining sector under national diversification strategies, increasing the consumption of flotation and processing chemicals. However, limited infrastructure, fluctuating regulatory environments, and chemical handling issues remain barriers to faster growth. Nonetheless, rising investment in mining projects and international partnerships are expected to accelerate regional demand for high-performance and environmentally compatible mining chemicals.

Mining Chemicals Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the mining chemicals market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global mining chemicals market include:

- AECI Mining Chemicals

- BASF SE

- Ashland

- Dow

- Kimleigh Chemicals SA (Pty) Ltd

- Cytec Solvay Group

- Arkema

- Clariant

- Nowata

- Kemira

- Shell Chemicals

- Quaker Chemical Corporation

- Akzo Nobel N.V.

- Solenis

- Sasol

- SNF Group

- AkzoNobel N.V.

- Chevron Phillips Chemical Company

- Orica Limited

- National Aluminium Company

The global mining chemicals market is segmented as follows:

By Product Type

- Grinding Aids

- Flocculants

- Frothers

- Collectors

- Depressants

- Others

By Mineral Type

- Non-Metallic Minerals

- Precious Metals

- Rare Earth Metals

- Base Metals

By Application

- Mineral Processing

- Explosives & Drilling

- Water & Wastewater Treatment

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global mining chemicals market, 2014 - 2020 (Kilo Tons) (USD Million)

- 2.2. Global mining chemicals market : Snapshot

- Chapter 3. Mining Chemicals– Market Dynamics

- 3.1. Introduction

- 3.2. Value chain analysis

- 3.3. Market drivers

- 3.3.1. Drivers for global mining chemicals market: Impact analysis

- 3.3.2. Rapidly depleting proven reserves and deteriorating ore grade

- 3.3.3. Growth of end-user industries in emerging economies

- 3.4. Market restraints

- 3.4.1. Restraints for global mining chemicals market: Impact analysis

- 3.4.2. Environmental concerns and logistic issues

- 3.5. Opportunities

- 3.5.1. Research and development

- 3.6. Porter’s five forces analysis

- 3.6.1. Bargaining power of suppliers

- 3.6.2. Bargaining power of buyers

- 3.6.3. Threat from new entrants

- 3.6.4. Threat from new substitutes

- 3.6.5. Degree of competition

- 3.7. Market attractiveness analysis

- 3.7.1. Market attractiveness analysis, by product segment

- 3.7.2. Market attractiveness analysis, by application segment

- 3.7.3. Market attractiveness analysis, by regional segment

- Chapter 4. Global Mining Chemicals Market – Competitive Landscape

- 4.1. Global mining chemicals: Company market share, 2014

- 4.2. Global mining chemicals market: Production capacity (subject to data availability)

- 4.3. Global mining chemicals: Raw material analysis

- 4.4. Global mining chemicals: Price trend analysis

- Chapter 5. Global Mining Chemicals Market: Product Segment Analysis

- 5.1. Global mining chemicals market: Overview by product

- 5.1.1. Global mining chemicals market volume share, by product, 2014 and 2020

- 5.2. Frothers

- 5.2.1. Global frothers market, 2014 and 2020(Kilo Tons) (USD Million)

- 5.3. Flocculants

- 5.3.1. Global flocculants market, 2014 and 2020(Kilo Tons) (USD Million)

- 5.4. Collectors

- 5.4.1. Global collectors market, 2014 and 2020(Kilo Tons) (USD Million)

- 5.5. Solvent extractants

- 5.5.1. Global solvent extractants market, 2014 and 2020(Kilo Tons) (USD Million)

- 5.6. Grinding Aids

- 5.6.1. Global grinding aids market, 2014 and 2020 (Kilo Tons) (USD Million)

- 5.7. Others

- 5.7.1. Global other mining chemicals, 2014 and 2020 (Kilo Tons) (USD Million)

- 5.1. Global mining chemicals market: Overview by product

- Chapter 6. Global Mining Chemicals Market: Application Segment Analysis

- 6.1. Global mining chemicals market: Application overview

- 6.1.1. Global mining chemicals market volume share, by application, 2014 and 2020

- 6.2. Mineral Processing

- 6.2.1. Global mining chemicals market for mineral processing, 2014 and 2020 (Kilo Tons) (USD Million)

- 6.3. Explosives and Drilling

- 6.3.1. Global mining chemicals market for explosives and drilling, 2014 and 2020 (Kilo Tons) (USD Million)

- 6.4. Water and Wastewater Treatment

- 6.4.1. Global mining chemicals market for water and wastewater treatment, 2014 and 2020 (Kilo Tons) (USD Million)

- 6.5. Others

- 6.5.1. Global mining chemicals market for other applications, 2014 and 2020 (Kilo Tons) (USD Million)

- 6.1. Global mining chemicals market: Application overview

- Chapter 7. Global Mining Chemicals Market – Regional Segment Analysis

- 7.1. Global mining chemicals market: Regional overview

- 7.1.1. Global mining chemicals market volume share, by region, 2014 and 2020

- 7.2. North America

- 7.2.1. North America mining chemicals market volume, by product, 2014 – 2020, (Kilo Tones)

- 7.2.2. North America mining chemicals market revenue, by product, 2014 – 2020, (USD Million)

- 7.2.3. North America mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tones)

- 7.2.4. North America mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.2.5. U.S.

- 7.2.5.1. U.S. mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.2.5.2. U.S. mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.2.5.3. U.S. mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tones)

- 7.2.5.4. U.S. mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.3. Europe

- 7.3.1. Europe mining chemicals market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.3.2. Europe mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.3. Europe mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.3.4. Europe mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.3.5. Germany

- 7.3.5.1. Germany mining chemicals market volume, by product, 2014 – 2020, (Kilo Tons)

- 7.3.5.2. Germany mining chemicals market revenue, by product, 2014 – 2020, (USD Million)

- 7.3.5.3. Germany mining chemicals market volume, by applications, 2014 – 2020, (Kilo Tones)

- 7.3.5.4. Germany mining chemicals market revenue, by applications, 2014 – 2020, (USD Million)

- 7.3.6. France

- 7.3.6.1. France mining chemicals market volume, by product, 2014 – 2020, (Kilo Tones)

- 7.3.6.2. France mining chemicals market revenue, by product, 2014 – 2020, (USD Million)

- 7.3.6.3. France mining chemicals market volume, by applications, 2014 – 2020, (Kilo Tons)

- 7.3.6.4. France mining chemicals market revenue, by applications, 2014 – 2020, (USD Million)

- 7.3.7. UK

- 7.3.7.1. UK mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.3.7.2. UK mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.7.3. UK mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.3.7.4. UK mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific mining chemicals market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.4.2. Asia Pacific mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.3. Asia Pacific mining chemicals market volume, by applications, 2014 – 2020, (Kilo Tons)

- 7.4.4. Asia Pacific mining chemicals market revenue, by applications, 2014 – 2020, (USD Million)

- 7.4.5. China

- 7.4.5.1. China mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.4.5.2. China mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.5.3. China mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.4.5.4. China mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.4.6. Japan

- 7.4.6.1. Japan mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.4.6.2. Japan mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.6.3. Japan mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.4.6.4. Japan mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.4.7. India

- 7.4.7.1. India mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.4.7.2. India mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.7.3. India mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.4.7.4. India mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.5. Latin America

- 7.5.1. Latin America mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.5.2. Latin America mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.3. Latin America mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.5.4. Latin America mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.5.5. Brazil

- 7.5.5.1. Brazil mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.5.5.2. Brazil mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.5.3. Brazil mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.5.5.4. Brazil mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.6. Middle East and Africa

- 7.6.1. Middle East and Africa mining chemicals market volume, by product, 2014 – 2020 (Kilo Tones)

- 7.6.2. Middle East and Africa mining chemicals market revenue, by product, 2014 – 2020 (USD Million)

- 7.6.3. Middle East and Africa mining chemicals market volume, by applications, 2014 – 2020 (Kilo Tons)

- 7.6.4. Middle East and Africa mining chemicals market revenue, by applications, 2014 – 2020 (USD Million)

- 7.1. Global mining chemicals market: Regional overview

- Chapter 8. Company Profiles

- 8.1. Ashland Inc

- 8.1.1. Overview

- 8.1.2. Financials

- 8.1.3. Business strategy

- 8.1.4. Product portfolio

- 8.1.5. Recent developments

- 8.2. BASF SE

- 8.2.1. Overview

- 8.2.2. Financials

- 8.2.3. Business strategy

- 8.2.4. Product portfolio

- 8.2.5. Recent developments

- 8.3. Clariant AG

- 8.3.1. Overview

- 8.3.2. Financials

- 8.3.3. Business strategy

- 8.3.4. Product portfolio

- 8.3.5. Recent developments

- 8.4. Nalco Company

- 8.4.1. Overview

- 8.4.2. Financials

- 8.4.3. Business strategy

- 8.4.4. Product portfolio

- 8.4.5. Recent developments

- 8.5. Chevron Phillips Chemical Company LP

- 8.5.1. Overview

- 8.5.2. Financials

- 8.5.3. Business strategy

- 8.5.4. Product portfolio

- 8.5.5. Recent developments

- 8.6. The Dow Chemical Company

- 8.6.1. Overview

- 8.6.2. Financials

- 8.6.3. Business strategy

- 8.6.4. Product portfolio

- 8.6.5. Recent developments

- 8.7. AkzoNobel Performance Additives

- 8.7.1. Overview

- 8.7.2. Financials

- 8.7.3. Business strategy

- 8.7.4. Product portfolio

- 8.7.5. Recent developments

- 8.8. Cheminova A/S

- 8.8.1. Overview

- 8.8.2. Financials

- 8.8.3. Business strategy

- 8.8.4. Product portfolio

- 8.8.5. Recent developments

- 8.9. NASACO International

- 8.9.1. Overview

- 8.9.2. Financials

- 8.9.3. Business strategy

- 8.9.4. Product portfolio

- 8.9.5. Recent developments

- 8.10. Cytec Industries

- 8.10.1. Overview

- 8.10.2. Financials

- 8.10.3. Business strategy

- 8.10.4. Product portfolio

- 8.10.5. Recent developments

- 8.11. Air Products and Chemicals, Inc

- 8.11.1. Overview

- 8.11.2. Financials

- 8.11.3. Business strategy

- 8.11.4. Product portfolio

- 8.11.5. Recent developments

- 8.12. SNF FloMin

- 8.12.1. Overview

- 8.12.2. Financials

- 8.12.3. Business strategy

- 8.12.4. Product portfolio

- 8.12.5. Recent developments

- 8.1. Ashland Inc

Inquiry For Buying

Mining Chemicals

Request Sample

Mining Chemicals