Healthcare Information System Market Size, Share, and Trends Analysis Report

CAGR :

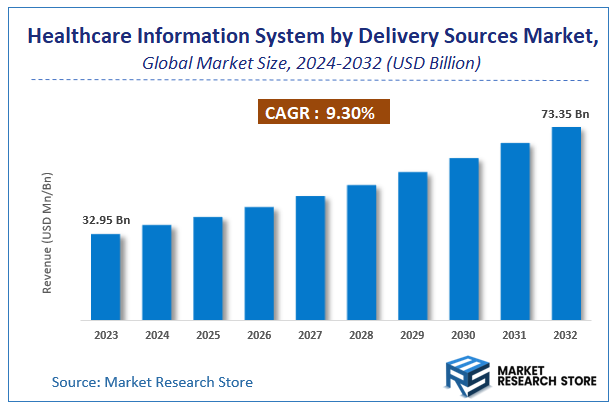

| Market Size 2023 (Base Year) | USD 32.95 Billion |

| Market Size 2032 (Forecast Year) | USD 73.35 Billion |

| CAGR | 9.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Healthcare Information System Market Insights

According to Market Research Store, the global healthcare information system market size was valued at around USD 32.95 billion in 2023 and is estimated to reach USD 73.35 billion by 2032, to register a CAGR of approximately 9.3% in terms of revenue during the forecast period 2024-2032.

The healthcare information system report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Healthcare Information System Market: Overview

Healthcare Information System (HIS) is an integrated framework designed to manage and streamline the collection, storage, retrieval, and exchange of healthcare data within hospitals, clinics, and other healthcare settings. It encompasses a variety of digital solutions including Electronic Health Records (EHRs), Hospital Information Systems (HIS), Laboratory Information Systems (LIS), Radiology Information Systems (RIS), and billing or administrative platforms. These systems enable healthcare providers to document patient histories, coordinate care, manage resources, ensure regulatory compliance, and improve overall operational efficiency.

The growth of the healthcare information system market is driven by the increasing digitization of healthcare, rising demand for efficient patient care delivery, and the need to manage growing volumes of medical data. Governments and healthcare organizations are investing in health IT infrastructure to enhance clinical decision-making, reduce medical errors, and facilitate interoperability across providers. Advancements in cloud computing, big data analytics, artificial intelligence, and mobile health applications are further expanding the capabilities and adoption of HIS. As the industry continues to prioritize patient-centric care, data security, and cost-effectiveness, healthcare information systems are becoming central to the modernization and sustainability of global healthcare delivery.

Key Highlights

- The healthcare information system market is anticipated to grow at a CAGR of 9.3% during the forecast period.

- The global healthcare information system market was estimated to be worth approximately USD 32.95 billion in 2023 and is projected to reach a value of USD 73.35 billion by 2032.

- The growth of the healthcare information system market is being driven by increasing need for efficient healthcare management, improved patient care, and streamlined administrative operations across hospitals, clinics, and other healthcare facilities.

- Based on the application, the hospital information system segment is growing at a high rate and is projected to dominate the market.

- On the basis of deployment, the web-based segment is projected to swipe the largest market share.

- In terms of component, the hardware segment is expected to dominate the market.

- Based on the end use, the hospitals & ambulatory services segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Healthcare Information System Market: Dynamics

Key Growth Drivers:

- Growing Need for Efficient Healthcare Operations and Data Management: Healthcare organizations are constantly seeking ways to streamline administrative tasks, reduce operational costs, and improve the efficiency of patient care delivery. HIS centralizes patient data, automates workflows, and provides real-time access to information, leading to reduced manual errors, faster processes, and better resource allocation, directly driving its adoption.

- Rising Adoption of Electronic Health Records (EHR) and Electronic Medical Records (EMR): The shift from paper-based records to digital EHR/EMR systems is a fundamental driver. EHRs improve data accuracy, accessibility, and sharing among healthcare providers, leading to better coordinated care, reduced medical errors, and enhanced patient safety. Government initiatives and mandates often encourage or require their implementation.

- Increasing Focus on Patient-Centric Care and Engagement: Modern healthcare emphasizes patient involvement in their care. HIS solutions include patient portals, telehealth platforms, and mobile health (mHealth) applications that empower patients to access their health information, schedule appointments, communicate with providers, and manage their health proactively, improving engagement and outcomes.

- Technological Advancements (AI, Big Data, Cloud Computing, IoT): The rapid evolution of technologies like Artificial Intelligence (AI) and Machine Learning (ML) for diagnostics and personalized treatment plans, Big Data analytics for population health management, cloud computing for scalable and accessible data storage, and the Internet of Medical Things (IoMT) for remote patient monitoring are transforming healthcare. These advancements are deeply integrated with and often reliant on robust HIS, propelling market growth.

Restraints:

- High Implementation and Maintenance Costs: The initial investment required for HIS, including software licenses, hardware infrastructure, customization, integration with existing systems, and extensive training for staff, can be substantial. Ongoing maintenance, upgrades, and IT support also contribute to high operational costs, posing a significant financial burden, especially for smaller healthcare facilities.

- Data Security and Privacy Concerns: Healthcare information systems handle highly sensitive patient data, making them prime targets for cyberattacks and data breaches. Concerns about data privacy, compliance with stringent regulations (e.g., HIPAA, GDPR), and the risk of cyber threats (e.g., ransomware) are major restraints. Ensuring robust cybersecurity measures and maintaining patient trust is a continuous challenge.

- Interoperability and Integration Challenges: A major hurdle is the lack of seamless interoperability between different HIS platforms and modules from various vendors, as well as with legacy systems. Sharing patient data effectively across different healthcare providers, departments, and external entities remains complex, hindering comprehensive care coordination and data analytics.

Opportunities:

- Leveraging AI and Machine Learning for Advanced Analytics: The integration of AI and ML within HIS offers immense opportunities for predictive analytics (e.g., identifying patients at risk of chronic diseases, predicting hospital readmissions), clinical decision support, drug discovery, and personalized medicine, leading to more precise diagnoses and effective treatment plans.

- Growth in Cloud-Based HIS Solutions: Cloud-based HIS offers scalability, cost-effectiveness (reduced upfront infrastructure investment), enhanced accessibility, and easier maintenance compared to on-premise solutions. This deployment model is particularly attractive for smaller and medium-sized healthcare facilities and is a significant growth area for vendors.

- Focus on Population Health Management (PHM): HIS is central to effective population health management, which aims to improve the health outcomes of specific patient groups. Opportunities exist in developing advanced analytics and reporting tools within HIS that enable healthcare organizations to identify health disparities, manage chronic diseases, and implement preventive care strategies for entire populations.

Challenges:

- Achieving True Interoperability Across the Healthcare Ecosystem: While efforts are underway, achieving seamless, real-time interoperability among diverse HIS platforms, health information exchanges (HIEs), and external data sources remains a major technical and organizational challenge. This fragmentation hinders comprehensive patient views and data liquidity.

- Ensuring Data Quality and Standardization: The effectiveness of HIS heavily relies on the quality and standardization of the data it collects. Challenges include ensuring consistent data entry, resolving data discrepancies, and adhering to clinical terminologies and coding standards to facilitate accurate analysis and information exchange.

- Managing the Complexity of System Implementation and Optimization: Deploying a new HIS or upgrading an existing one is a complex, time-consuming, and resource-intensive process that can disrupt operations. Optimizing the system to meet the unique workflows of different departments and ensuring user adoption requires meticulous planning, ongoing training, and dedicated support.

Healthcare Information System Market: Report Scope

This report thoroughly analyzes the Healthcare Information System Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Healthcare Information System Market |

| Market Size in 2023 | USD 32.95 Billion |

| Market Forecast in 2032 | USD 73.35 Billion |

| Growth Rate | CAGR of 9.3% |

| Number of Pages | 140 |

| Key Companies Covered | Philips Healthcare, Siemens Healthcare, Carestream Health Inc., Cerner Corporation, Merge Healthcare Incorporated, NextGen Healthcare Information Systems Inc., GE Healthcare and McKesson Corporation |

| Segments Covered | By Delivery Mode, By Components, By Application, By, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Healthcare Information System Market: Segmentation Insights

The global healthcare information system market is divided by application, deployment, component, end use, and region.

Based on application, the global healthcare information system market is divided into hospital information system, pharmacy automation systems, laboratory informatics, revenue cycle management, medical imaging information system, and patient administration system. Hospital Information System (HIS) dominates the Healthcare Information System Market, serving as the backbone of modern healthcare IT infrastructure. HIS encompasses integrated modules that manage clinical, administrative, and financial data across departments, improving workflow efficiency, patient care coordination, and regulatory compliance. Core functionalities include electronic medical records (EMR), computerized physician order entry (CPOE), and decision support systems. Hospitals and healthcare institutions increasingly rely on HIS to streamline operations, reduce medical errors, and ensure continuity of care. With the global push for digital transformation in healthcare and rising demand for centralized, interoperable data systems, HIS remains the primary application driving market growth.

On the basis of deployment, the global healthcare information system market is bifurcated into web-based, on-premises, and cloud-based. Web-based deployment dominates the Healthcare Information System Market, primarily due to its balance of accessibility, scalability, and cost-effectiveness. Web-based systems operate through internet browsers, allowing healthcare providers to access clinical and administrative data from any location without the need for complex software installations. These systems are especially favored by mid-sized hospitals, outpatient facilities, and diagnostic centers where centralized data access, low infrastructure costs, and simplified updates are essential. Web-based solutions also enable easier integration with other healthcare applications such as EHRs, billing systems, and imaging platforms, making them a popular choice for institutions seeking streamlined, user-friendly digital healthcare management.

In terms of component, the global healthcare information system market is bifurcated into hardware, software & systems, and servicese. Hardware dominates the Healthcare Information System Market as it forms the foundational infrastructure enabling all software applications and data processing functions within hospitals, clinics, and diagnostic centers. This segment includes servers, storage devices, networking equipment, display systems, medical monitors, and workstations. Hardware components are critical for managing the growing volumes of patient data, supporting high-resolution imaging, and ensuring system reliability for mission-critical operations. With the increasing digitization of healthcare workflows, the expansion of telehealth services, and integration of medical IoT devices, demand for robust and scalable hardware continues to grow, particularly in medium to large healthcare facilities.

On the basis of end use, the global healthcare information system market is bifurcated into hospitals & ambulatory services, diagnostic centers, and academic & research institutes. Hospitals & Ambulatory Services dominate the Healthcare Information System Market due to their extensive and varied operational needs that require integrated clinical, administrative, and financial solutions. Hospitals utilize comprehensive information systems—including Electronic Health Records (EHR), Patient Administration Systems (PAS), Radiology Information Systems (RIS), and Revenue Cycle Management (RCM)—to manage high patient volumes, optimize care delivery, and meet regulatory requirements. Ambulatory care centers, such as outpatient clinics and urgent care units, benefit from lightweight, web-based systems that enhance scheduling, documentation, and billing efficiency. The growing patient demand for coordinated and cost-effective care, combined with increased digital transformation initiatives and government mandates for health IT adoption, continues to drive market growth in this segment.

Healthcare Information System Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the healthcare information system market due to advanced healthcare infrastructure, strong regulatory frameworks, and widespread adoption of electronic health records (EHR), telehealth platforms, and clinical decision support systems. The United States leads regional growth, propelled by federal initiatives such as the HITECH Act, which incentivized healthcare IT integration across hospitals and clinics. Major providers utilize enterprise-wide systems for data interoperability, revenue cycle management, and population health analytics. Additionally, the region is a major hub for innovation in AI-based diagnostics, cloud-based hospital systems, and cybersecurity for medical data. Canada is also progressing rapidly, investing in provincial EHR systems, telemedicine networks, and integrated care platforms, particularly in rural and underserved regions. The presence of major health IT vendors, ongoing digital transformation efforts, and a high patient volume contribute to sustained market leadership in North America.

Asia-Pacific is the fastest-growing region in the healthcare information system market, supported by rising healthcare expenditure, government-backed digitization programs, and increasing demand for efficient healthcare delivery across urban and rural areas. China and India are key growth drivers, with expanding hospital networks and the adoption of EHRs, telemedicine, and digital appointment systems. China is investing heavily in AI-driven diagnostics, remote patient monitoring, and cloud-based clinical data platforms as part of its healthcare modernization plan. India is advancing digital health with its Ayushman Bharat Digital Mission, enabling unified patient records and integrated service delivery across public and private healthcare providers. Japan and South Korea maintain sophisticated health IT infrastructures, using information systems for elderly care, chronic disease management, and clinical research. Southeast Asia is also seeing rapid adoption in urban hospitals and private clinics, particularly for telehealth, insurance management, and digital billing systems.

Europe holds a significant share in the healthcare information system market, driven by coordinated national eHealth strategies, a growing aging population, and rising demand for efficient patient management solutions. Countries such as Germany, the UK, France, and the Netherlands lead adoption of hospital information systems, laboratory systems, and radiology information platforms. The region places strong emphasis on data privacy and security under frameworks like GDPR, encouraging the use of secure, cloud-based platforms for healthcare data exchange. Integration of AI in diagnostics and predictive analytics is gaining momentum in academic and specialized healthcare centers. Public and private investments in health digitization, especially in Scandinavia and Western Europe, support innovation, while Central and Eastern Europe are steadily expanding their digital health infrastructure through EU funding.

Latin America is an emerging market for healthcare information systems, with Brazil and Mexico being the primary contributors. Regional growth is supported by efforts to modernize public healthcare, increase efficiency, and expand access to medical services through digital tools. Brazil has implemented national EHR initiatives and hospital information systems to improve public health coordination, while Mexico is strengthening its digital infrastructure to manage population health data and improve provider workflows. Private hospitals are leading in the adoption of clinical and administrative systems, particularly in urban areas. Despite budgetary constraints and fragmented healthcare delivery models, the push for health system modernization, driven by international support and rising urban healthcare demand, supports long-term market growth.

Middle East & Africa are developing regions in the healthcare information system market, with adoption fueled by healthcare infrastructure development, smart city initiatives, and increasing investment in digital transformation. In the Middle East, the UAE and Saudi Arabia are leading adopters, integrating cloud-based hospital information systems, remote diagnostics, and national EHR networks into their healthcare ecosystems. These countries are also investing in AI-powered decision support tools and telemedicine platforms to enhance specialist access and resource utilization. In Africa, South Africa, Kenya, and Nigeria are key markets where healthcare IT is being used to address systemic challenges such as care coordination, data management, and rural access. However, limited technical infrastructure, workforce training, and funding remain major hurdles across the region. International partnerships and donor-backed initiatives are playing a key role in expanding access to digital healthcare tools.

Healthcare Information System Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the healthcare information system market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global healthcare information system market include:

- Oracle (Cerner)

- GE Healthcare

- Veradigm LLC (formerly known as Allscripts)

- Epic Systems Corporation

- eClinicalWorks

- Greenway Health, LLC

- NextGen Healthcare, Inc.

- Medical Information Technology, Inc. (Meditech)

- TruBridge (CPSI)

- AdvancedMD, Inc.

- CureMD Healthcare

- McKesson Corporation

- IQVIA

- Optum, Inc

The global healthcare information system market is segmented as follows:

By Application

- Hospital Information System

- Pharmacy Automation Systems

- Laboratory Informatics

- Revenue Cycle Management

- Medical Imaging Information System

- Patient Administration System

By Deployment

- Web-based

- On-premises

- Cloud-based

By Component

- Hardware

- Software & Systems

- Servicese

By End Use

- Hospitals & Ambulatory Services

- Diagnostic Centers

- Academic & Research Institutes

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global market revenue, 2014 - 2020(USD Billion)

- 2.2. Global healthcare information system market: Snapshot

- Chapter 3. Healthcare Information System Market – Global and Industry Analysis

- 3.1. Healthcare information system: Market dynamics

- 3.2. Market drivers

- 3.2.1. Drivers of global healthcare information system market: Impact analysis

- 3.2.2. Government Support

- 3.3. Market restraints

- 3.3.1. Restraints of global healthcare information system market: Impact analysis

- 3.3.2. Complex process and scarcity of expertise

- 3.4. Opportunities

- 3.4.1. Rising demand from developing countries

- 3.5. Porter’s five forces analysis

- 3.6. Market Attractiveness Analysis

- 3.6.1. Market attractiveness analysis by delivery mode segment

- 3.6.2. Market attractiveness analysis by components segment

- 3.6.3. Market attractiveness analysis by application segment

- 3.6.4. Market attractiveness analysis by regional segment

- Chapter 4. Global Healthcare information system market - Competitive Landscape

- 4.1. Company market share, 2014

- 4.2. Price trend analysis

- Chapter 5. Global Healthcare Information System Market – Delivery Mode Segment Analysis

- 5.1. Global healthcare information system market: delivery mode overview

- 5.1.1. Global healthcare information system market revenue share, by delivery mode, 2014 - 2020

- 5.2. Cloud based technology

- 5.2.1. Global cloud based technology market, by delivery mode, 2014 – 2020 (USD Billion)

- 5.3. On-premises installation

- 5.3.1. Global on-premises installation market, by delivery mode, 2014 – 2020 (USD Billion)

- 5.4. Web Based Technology

- 5.4.1. Global web based technology market, by delivery mode, 2014 – 2020 (USD Billion)

- 5.1. Global healthcare information system market: delivery mode overview

- Chapter 6. Global Healthcare Information System Market – Components Segment Analysis

- 6.1. Global healthcare information system market: components overview

- 6.1.1. Global healthcare information system market revenue share, by components, 2014 - 2020

- 6.2. Software

- 6.2.1. Global software market, by components, 2014 – 2020 (USD Billion)

- 6.3. Hardware

- 6.3.1. Global hardware market, by components, 2014 – 2020 (USD Billion)

- 6.4. Services

- 6.4.1. Global services market, by components, 2014 – 2020 (USD Billion)

- 6.1. Global healthcare information system market: components overview

- Chapter 7. Global Healthcare Information System Market – Application Segment Analysis

- 7.1. Global healthcare information system market: Application overview

- 7.1.1. Global healthcare information system market revenue share by application, 2014 - 2020

- 7.2. Pharmacy Information System

- 7.2.1. Global healthcare information system market for pharmacy information system, 2014 – 2020 (USD Billion)

- 7.3. Laboratory Information System

- 7.3.1. Global healthcare information system market for laboratory information system, 2014 – 2020 (USD Billion)

- 7.4. Hospital Information System

- 7.4.1. Global healthcare information system market for hospital information system, 2014 – 2020 (USD Billion)

- 7.1. Global healthcare information system market: Application overview

- Chapter 8. Global Healthcare Information System Market – Regional Segment Analysis

- 8.1. Global healthcare information system market: Regional overview

- 8.1.1. Global healthcare information system market revenue share by region, 2014 - 2020

- 8.2. North America

- 8.2.1. North America healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.2.2. North America healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.2.3. North America healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.2.4. U.S.

- 8.2.4.1. U.S. healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.2.4.2. U.S. healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.2.4.3. U.S. healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.3. Europe

- 8.3.1. Europe healthcare information system market revenue, by a delivery mode, 2014 – 2020 (USD Billion)

- 8.3.2. Europe healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.3.3. Europe healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.3.4. Germany

- 8.3.4.1. Germany healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.3.4.2. Germany healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.3.4.3. Germany healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.3.5. France

- 8.3.5.1. France healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.3.5.2. France healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.3.5.3. France healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.3.6. UK

- 8.3.6.1. UK healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.3.6.2. UK healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.3.6.3. UK healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.4.2. Asia Pacific healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.4.3. Asia Pacific healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.4.4. China

- 8.4.4.1. China healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.4.4.2. China healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.4.4.3. China healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.4.5. Japan

- 8.4.5.1. Japan healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.4.5.2. Japan healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.4.5.3. Japan healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.4.6. India

- 8.4.6.1. India healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.4.6.2. India healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.4.6.3. India healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.5. Latin America

- 8.5.1. Latin America healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.5.2. Latin America healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.5.3. Latin America healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.5.4. Brazil

- 8.5.4.1. Brazil healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.5.4.2. Brazil healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.5.4.3. Brazil healthcare information system market revenue, by application, 2014 – 2020 (USD Billion)

- 8.6. Middle East and Africa

- 8.6.1. Middle East and Africa healthcare information system market revenue, by delivery mode, 2014 – 2020 (USD Billion)

- 8.6.2. Middle East and Africa healthcare information system market revenue, by components, 2014 – 2020 (USD Billion)

- 8.6.3. Middle East and Africa healthcare information system market revenue, by end-use, 2014 – 2020 (USD Billion)

- 8.1. Global healthcare information system market: Regional overview

- Chapter 9. Company Profile

- 9.1. Carestream health Inc

- 9.1.1. Overview

- 9.1.2. Financials

- 9.1.3. Product portfolio

- 9.1.4. Business strategy

- 9.1.5. Recent developments

- 9.2. NextGen healthcare information systems Inc

- 9.2.1. Overview

- 9.2.2. Financials

- 9.2.3. Product portfolio

- 9.2.4. Business strategy

- 9.2.5. Recent developments

- 9.3. Siemens healthcare

- 9.3.1. Overview

- 9.3.2. Financials

- 9.3.3. Product portfolio

- 9.3.4. Business strategy

- 9.3.5. Recent developments

- 9.4. Philips healthcare

- 9.4.1. Overview

- 9.4.2. Financials

- 9.4.3. Product portfolio

- 9.4.4. Business strategy

- 9.4.5. Recent developments

- 9.5. Merge healthcare Inc

- 9.5.1. Overview

- 9.5.2. Financials

- 9.5.3. Product portfolio

- 9.5.4. Business strategy

- 9.5.5. Recent developments

- 9.6. McKesson corporation

- 9.6.1. Overview

- 9.6.2. Financials

- 9.6.3. Product portfolio

- 9.6.4. Business strategy

- 9.6.5. Recent developments

- 9.7. Epic Systems Corporation

- 9.7.1. Overview

- 9.7.2. Financials

- 9.7.3. Product portfolio

- 9.7.4. Business strategy

- 9.7.5. Recent developments

- 9.8. GE healthcare

- 9.8.1. Overview

- 9.8.2. Financials

- 9.8.3. Product portfolio

- 9.8.4. Business strategy

- 9.8.5. Recent developments

- 9.9. Cerner corporation

- 9.9.1. Overview

- 9.9.2. Financials

- 9.9.3. Product portfolio

- 9.9.4. Business strategy

- 9.9.5. Recent developments

- 9.1. Carestream health Inc

Inquiry For Buying

Healthcare Information System

Request Sample

Healthcare Information System