Industry Prospective:

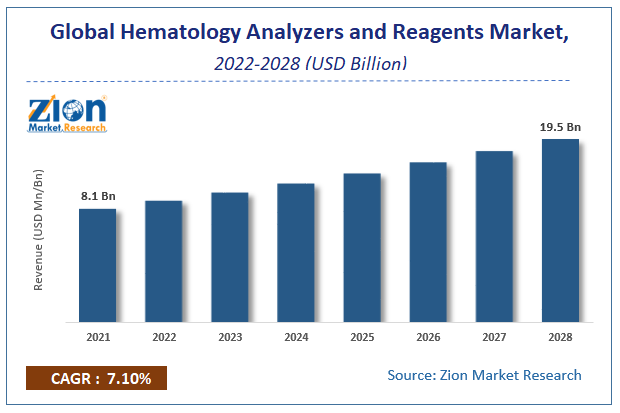

The global hematology analyzers and reagents market was worth around USD 8.1 billion in 2023 and is estimated to grow to about USD 16.5 billion by 2032, with a compound annual growth rate (CAGR) of approximately 7.25% over the forecast period. The report analyzes the hematology analyzers and reagents market’s drivers, restraints/challenges, and the effect they have on the demands during the projection period. In addition, the report explores emerging opportunities in the hematology analyzers and reagents market.

To Get more Insights, Request a Free Sample

Hematology Analyzers and Reagents Market: Overview

Hematology is a field of medicine that deals with the diagnosis, research, treatment, and prevention of blood diseases. Hematology analyzers are equipment that performs tests on blood samples. They're used to do tests like a full blood count, which includes platelet, white, red, and hemoglobin counts, as well as to characterize blood cells to detect a medical condition.

To Get more Insights, Request a Free Sample

COVID-19 Impact:

The COVID-19 pandemic had a substantial influence on the hematology industry, since there is a growing emphasis on hematology parameters for COVID-19 evaluation throughout the world, and many hospitals have begun adopting tools like hematology analyzers to monitor and test COVID-19 patients. The increasing necessity of hematological testing in COVID-19-infected patients is predicted to drive up demand for hematology products and reagents among various end-users, boosting the market's growth during the pandemic period as well as post-pandemic period.

Hematology Analyzers and Reagents Market: Growth Drivers

Growing incidence of blood disorders is predicted to drive the market growth

Red blood cell disorders including anemia, bleeding (platelet) disorders, and white blood cell disorders are all characterized by benign blood diseases. Other blood disorders, such as lymphoma, leukemia, and sickle cell anemia can cause chronic sickness or even death. Sickle cell disease, the most prevalent form of a hereditary blood ailment, affects between 70,000 to 100,000 people in the United States. Further, annually, approximately 1.24 million instances of blood cancer are diagnosed globally, accounting for around 6% of all cases of cancer. Owing to such a huge burden of the disease, the need for blood tests is rising, thereby leading to an increase in demand for hematology analyzers and reagents. In addition to this, advantageous reimbursement policies, rise in spending on health, and developing healthcare infrastructure in developing countries are some of the major factors that are fostering the growth of the global hematology analyzers and reagents market. Furthermore, an increase in blood donation & blood transfusion rate is also booming the market.

Hematology Analyzers and Reagents Market: Restraints

High costs associated with the hematology analyzers may hinder the market growth

Hematology analyzers and reagents are medical products and commodities that are used to identify and count individual blood cells in a time-efficient manner. This equipment has replaced the traditional methods of counting blood cells one by one under magnification, which was formerly provided by research laboratory professionals. Hematology analyzer reagents are scientific, automatic, rapid, and provide greater accuracy in analysis. Flow cytometry is the most advanced and costly approach currently available. All such factors are likely to impede the growth of the market. In addition to this, hematology analyzers require high maintenance costs which may also hinder the market growth. Moreover, less developed healthcare infrastructure and a dearth of skilled professionals to operate the hematology analyzer are also some of the restraining factors of the market.

Hematology Analyzers and Reagents Market: Opportunities

Advanced technology in the field of medical equipment may generate numerous opportunities for the market growth

Some of the important factors are increasing usage of automated hematology equipment, growing technical breakthroughs, and integration of fundamental flow-cytometry techniques in advanced hematology analyzers may lead to beneficial opportunities for the growth of the global hematology analyzer & reagent market during the forecast period. Further, the advent of digital imaging systems in hematological laboratories and the use of microfluidics technology in hematology analyzers might offer up new potential for new market players. Furthermore, heavy investments by the big players for new product launches and the presence of strong distribution chains may also drive market growth in the forecast period.

Report Scope:

Hematology Analyzers and Reagents Market: Challenges.

Quality of the hematology analyzers might be a challenge for the market growth

The phenomenon of a cell count that is too high or too few can also be caused by an automatic blood cell analyzer. Some analyzers, particularly impedance-type counters, may not be able to discriminate between nucleated red blood cells and microscopic platelet aggregation since they only assess the size and quantity of particles. Platelet aggregation can be mistaken for red blood cells or white blood cells, and nucleated red blood cells can be mistaken for white blood cells as well. Lymphocytes are particularly sensitive. Atypical cells that are big or unreadable, immature neutrophils, and toxic reactive lymphocytes are also prone to be misclassified. The major threats include incorrect findings, which might lead to therapy delays or improper treatment. Thus, the quality issues of the hematology analyzers may act as a major challenge for the market growth.

Hematology Analyzers and Reagents Market: Segmentation

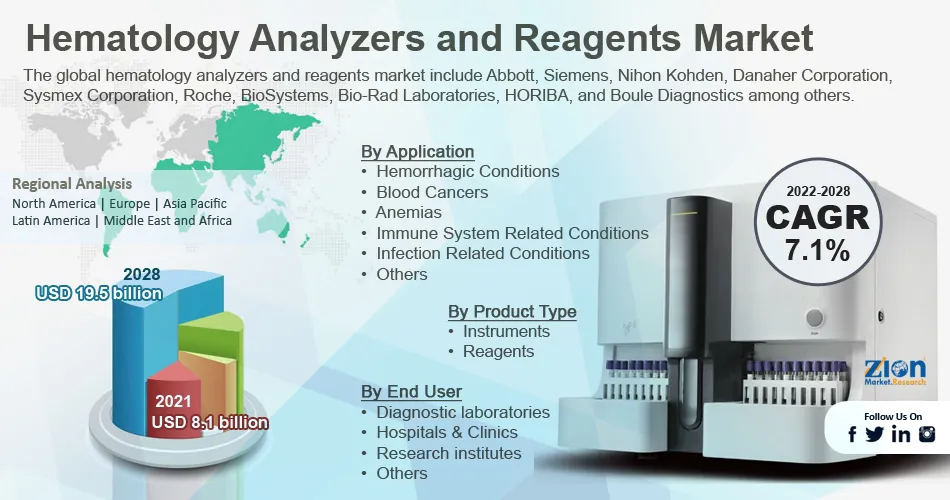

The global hematology analyzers and reagents market is classified into product type, application, end-user, and region.

Based on the product type, the global market is split into reagents and instruments.

The application segment consists of hemorrhagic conditions, blood cancers, anemias immune system-related conditions, infection-related conditions, and others.

By end-user, the market is bifurcated into research institutes, hospitals & clinics, diagnostic laboratories, and others.

Recent Developments

- In April 2022, Sysmex Europe, launched the XQ-320, a three-part differential automated hematology analyzer. The XQ-320 is a reliable instrument that requires little sample volume, bench space, or maintenance.

- In July 2021, PixCell Medical, a pioneer in point-of-care diagnostics, revealed that it has entered a new distribution deal with Gamidor Diagnostics to market PixCell's hematology analyzer, HemoScreen™, all over Israel.

- In January 2021, Roche has renewed a long-standing collaboration with Sysmex to market Sysmex hematological diagnostic products, including instruments and reagents, under a new worldwide commercial partnership agreement.

Hematology Analyzers and Reagents Market: Regional Landscape

North America is projected to dominate the market for hematology analyzers and reagents

North America is expected to dominate the global hematology analyzers and reagents market owing to the strong presence of key companies and rising investment to create innovative and more accurate result-generating medical equipment. Europe is expected to take the lead due to a rise in the number of diagnostic clinics and increased awareness of hematological illnesses in the region. On the other hand, because of the rising frequency of hematological illnesses among the patient population, the worldwide hematology analyzers and reagent market opportunity is expected to be greatest in the undeveloped areas of Asia Pacific and Latin America.

Hematology Analyzers and Reagents Market: Competitive Landscape

The major players operating in the global hematology analyzers and reagents market include:

- Abbott

- Siemens

- Nihon Kohden

- Danaher Corporation

- Sysmex Corporation

- Roche

- BioSystems

- Bio-Rad Laboratories

- HORIBA

- Boule Diagnostics among others.

Global Hematology analyzers and reagents market is segmented as follows:

By Product Type

- Instruments

- Reagents

By Application

- Hemorrhagic Conditions

- Blood Cancers

- Anemias

- Immune System Related Conditions

- Infection Related Conditions

- Others

By End User

- Diagnostic laboratories

- Hospitals & Clinics

- Research institutes

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Growing incidence of blood disorders is predicted to drive market growth. In addition to this, advantageous reimbursement policies, rise in spending on health, and developing healthcare infrastructure in developing countries are some of the major factors that are fostering the growth of the global hematology analyzers and reagents market. Furthermore, an increase in blood donation & blood transfusion rate is also booming the market.

According to the research report, the global hematology analyzers and reagents market was worth about 8.1 (USD billion) in 2023 and is predicted to grow to around 16.5 (USD billion) by 2032, with a compound annual growth rate (CAGR) of around 7.25%.

North America is expected to dominate the global hematology analyzers and reagents market owing to the strong presence of key companies and rising investment to create innovative and more accurate result-generating medical equipment.

The major players operating in the global hematology analyzers and reagents market include Abbott, Siemens, Nihon Kohden, Danaher Corporation, Sysmex Corporation, Roche, BioSystems, Bio-Rad Laboratories, HORIBA, and Boule Diagnostics among others.

Table Of Content

Inquiry For Buying

Hematology Analyzers and Reagents

Request Sample

Hematology Analyzers and Reagents