Home Health Hubs Market Size, Share, and Trends Analysis Report

CAGR :

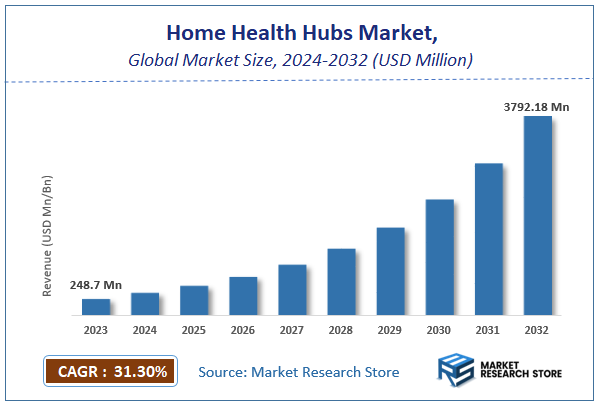

| Market Size 2023 (Base Year) | USD 248.7 Million |

| Market Size 2032 (Forecast Year) | USD 3792.18 Million |

| CAGR | 31.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Home Health Hubs Market Insights

According to Market Research Store, the global home health hubs market size was valued at around USD 248.7 million in 2023 and is estimated to reach USD 3792.18 million by 2032, to register a CAGR of approximately 31.30% in terms of revenue during the forecast period 2024-2032.

The home health hubs report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Home Health Hubs Market: Overview

Home health hubs are centralized systems or devices designed to manage and integrate patient health data in a home setting. These hubs typically connect with medical devices, wearables, and smartphones to collect and transmit real-time health information to healthcare providers. The primary goal of these hubs is to enable remote patient monitoring, improve healthcare outcomes, and reduce hospital visits by providing continuous, personalized care. They often feature capabilities like data analytics, telehealth integration, and reminders for medication adherence, catering to patients with chronic conditions, the elderly, and those in post-operative recovery.

Key Highlights

- The home health hubs market is anticipated to grow at a CAGR of 31.30% during the forecast period.

- The global home health hubs market was estimated to be worth approximately USD 248.7 million in 2023 and is projected to reach a value of USD 3792.18 million by 2032.

- The growth of the home health hubs market is being driven by the increasing prevalence of chronic diseases, a rising aging population, and a growing preference for home-based healthcare solutions.

- Based on the product & service, the remote patient monitoring (RPM) service segment is growing at a high rate and is projected to dominate the market.

- On the basis of type of patient monitoring, the high-acuity patient monitoring segment is projected to swipe the largest market share.

- In terms of end user, the hospital segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Home Health Hubs Market: Dynamics

Key Growth Drivers:

- Aging Population: The increasing elderly population globally, with a higher prevalence of chronic diseases, necessitates accessible and affordable healthcare solutions, making home health hubs a viable option.

- Technological Advancements: Continuous advancements in telemedicine, remote patient monitoring, and wearable technology are enabling better connectivity and data collection, enhancing the effectiveness of home health hubs.

- Rising Healthcare Costs: Home health hubs offer a cost-effective alternative to traditional hospital-based care, reducing healthcare expenditures for both patients and providers.

- Chronic Disease Management: These hubs play a crucial role in managing chronic conditions like diabetes, heart disease, and respiratory disorders, improving patient outcomes and reducing hospital readmissions.

- Patient Preference: Many individuals prefer receiving healthcare in the comfort of their homes, emphasizing the demand for convenient and personalized home-based care solutions.

Restraints:

- Data Security and Privacy Concerns: Ensuring the secure and confidential handling of sensitive patient data is a major challenge, requiring robust cybersecurity measures.

- Reimbursement Models: Limited and inconsistent reimbursement policies from insurance providers can hinder the widespread adoption of home health hubs.

- Lack of Standardization: The absence of standardized protocols and interoperability among different devices and platforms can create challenges in data integration and seamless care delivery.

- Limited Access to Technology: Unequal access to technology and reliable internet connectivity can limit the reach and effectiveness of home health hubs in underserved communities.

- Skilled Workforce Shortage: A shortage of trained healthcare professionals, particularly in remote patient monitoring and telehealth, can impede the growth of this market.

Opportunities:

- Integration with Wearable Technology: Combining home health hubs with wearable devices can provide real-time, continuous monitoring of vital signs, enabling proactive interventions and improved patient care.

- Artificial Intelligence (AI) and Machine Learning (ML): AI and ML algorithms can be utilized to analyze patient data, predict potential health risks, and personalize care plans, enhancing the efficiency and effectiveness of home health hubs.

- Value-Based Care Models: Aligning reimbursement models with value-based care principles can incentivize the adoption of home health hubs by rewarding providers for improved patient outcomes and reduced costs.

- Expanding Telehealth Services: Expanding the scope of telehealth services beyond basic consultations to include remote diagnostics, monitoring, and treatment can further enhance the capabilities of home health hubs.

- Global Market Expansion: The home health hubs market has significant growth potential in emerging economies with growing healthcare needs and a rising elderly population.

Challenges:

- Regulatory Hurdles: Navigating complex regulatory landscapes and obtaining necessary approvals for new technologies and services can be a significant challenge.

- Patient Education and Engagement: Educating patients about the benefits of home health hubs and ensuring their active participation in their care plans is crucial for successful implementation.

- Interoperability and Data Exchange: Achieving seamless data exchange between different healthcare providers, devices, and platforms remains a significant technical challenge.

- Maintaining Patient Trust: Building and maintaining patient trust in the security and privacy of their health data is essential for the long-term success of home health hubs.

- Maintaining Quality of Care: Ensuring the quality and continuity of care delivered through home health hubs requires robust quality assurance mechanisms and ongoing professional development for healthcare providers.

Home Health Hubs Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Home Health Hubs Market |

| Market Size in 2023 | USD 248.7 Million |

| Market Forecast in 2032 | USD 3792.18 Million |

| Growth Rate | CAGR of 31.3% |

| Number of Pages | 140 |

| Key Companies Covered | Qualcomm, Lamprey Networks, Vivify Health, Ihealth Lab, AMC Health, Honeywell International, Ideal Life, Insung Information, MEDM, Onkol |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Home Health Hubs Market: Segmentation Insights

The global home health hubs market is divided by product & service, type of patient monitoring, end user, and region.

Segmentation Insights by Product & Service

Based on product & service, the global home health hubs market is divided into standalone hub, mobile hub, and remote patient monitoring service.

The remote patient monitoring (RPM) service segment dominates the home health hubs market due to the growing demand for real-time health monitoring and chronic disease management. This segment caters to patients with conditions like diabetes, hypertension, and cardiovascular diseases, enabling healthcare providers to track vital signs remotely. The integration of advanced technologies such as IoT, AI, and telehealth further enhances RPM services, making them essential for proactive healthcare management. The convenience and cost-effectiveness of monitoring patients at home also contribute significantly to the dominance of this segment.

The mobile hub segment holds the second position in the market, driven by its portability and ease of use. Mobile hubs are compact devices that connect patients with healthcare providers through smartphones or tablets. These hubs are particularly popular among tech-savvy users and younger populations, offering flexibility in tracking health metrics on the go. The integration of mobile health apps and wearable devices amplifies their functionality, making them a key player in the market.

Lastly, the standalone hub segment, while less dominant, serves as a reliable option for patients requiring robust, stationary health monitoring systems. These hubs are commonly used in households with elderly or critically ill patients who need continuous health assessments. Despite being stationary, standalone hubs are equipped with high-tech features, such as connectivity to multiple medical devices and automated data transmission, ensuring accurate and consistent health monitoring.

Segmentation Insights by Type of Patient Monitoring

On the basis of type of patient monitoring, the global home health hubs market is bifurcated into high, moderate and low acuity.

The high-acuity patient monitoring segment dominates the home health hubs market due to the critical need for continuous, real-time monitoring of patients with severe or life-threatening conditions. These systems are essential for managing patients recovering from surgeries, those with advanced chronic illnesses, or individuals requiring intensive care at home. High-acuity monitoring integrates advanced technologies such as wearable devices, telehealth platforms, and AI-driven analytics to ensure precise tracking of critical parameters like heart rate, oxygen levels, and blood pressure. The increasing demand for hospital-level care at home further boosts the growth of this segment.

The moderate-acuity patient monitoring segment follows, driven by its application in managing patients with stable but chronic conditions, such as diabetes, hypertension, or respiratory illnesses. This segment caters to a significant portion of the aging population who require frequent health assessments without the intensity of high-acuity monitoring. Moderate-acuity solutions often combine wearable technology with mobile apps to provide cost-effective and efficient care, bridging the gap between high and low-acuity systems.

The low-acuity patient monitoring segment holds the smallest market share but remains important for preventive care and general health tracking. This segment typically includes solutions for fitness monitoring, wellness programs, and early detection of potential health issues. Low-acuity systems are commonly used by individuals focused on maintaining health rather than managing existing medical conditions. Despite its smaller share, advancements in consumer health technologies, such as smartwatches and fitness trackers, are driving growth in this segment.

Segmentation Insights by End User

In terms of end user, the global home health hubs market is categorized into hospital, payers, and home care agency.

The hospital segment dominates the home health hubs market due to the critical role hospitals play in implementing remote patient monitoring and telehealth solutions. Hospitals leverage these hubs to extend their care beyond traditional settings, particularly for patients with chronic conditions or those transitioning from inpatient to outpatient care. These hubs help hospitals manage patient data in real-time, improve outcomes, and reduce readmissions, which is vital in value-based care models. With access to advanced technology and a broad patient base, hospitals are at the forefront of adopting and integrating home health hubs.

The home care agency segment follows, driven by the increasing demand for in-home healthcare services. These agencies use home health hubs to provide personalized and continuous care to patients, particularly the elderly or those with mobility constraints. By utilizing remote monitoring and communication tools, home care agencies can efficiently manage their patients’ health while maintaining cost-effectiveness. The growth of this segment is further supported by the rising popularity of aging-in-place solutions and the preference for home-based care.

The payer segment, while smaller, is steadily gaining traction as insurance companies and other payers recognize the cost-saving potential of home health hubs. Payers increasingly support these technologies to manage chronic disease costs, prevent hospitalizations, and enhance patient engagement. By subsidizing or reimbursing home health hubs, payers can align with healthcare systems focused on preventive care and value-based reimbursement models.

Home Health Hubs Market: Regional Insights

- North America is expected to dominates the global market

North America dominates the home health hubs market, driven by factors such as a well-established healthcare infrastructure, advanced technological adoption, and a significant aging population with a high prevalence of chronic diseases. This region boasts a robust network of home healthcare providers and a favorable regulatory environment that supports the growth of home-based care solutions.

Europe follows closely behind North America, characterized by a mature healthcare system and a strong emphasis on patient-centered care. The region is witnessing a growing demand for innovative healthcare solutions that can improve accessibility and affordability, making home health hubs an attractive option. Furthermore, government initiatives promoting telemedicine and remote patient monitoring are further propelling the market's growth.

The Asia-Pacific region is projected to exhibit the fastest growth rate, fueled by rapid economic development, a burgeoning elderly population, and increasing healthcare expenditure. The region presents significant untapped potential, with a growing demand for affordable and accessible healthcare solutions, particularly in emerging economies. Moreover, advancements in technology and increasing internet penetration are creating favorable conditions for the expansion of home health hubs.

Latin America is experiencing steady growth in the home health hubs market, driven by factors such as rising healthcare costs, a growing prevalence of chronic diseases, and increasing awareness about the benefits of home-based care. However, challenges such as limited access to technology and healthcare infrastructure in certain regions can hinder market growth.

The Middle East and Africa region presents a diverse landscape with varying levels of market maturity. While some countries in the region are witnessing rapid growth due to increasing investments in healthcare infrastructure and technological advancements, others face challenges such as limited access to healthcare, inadequate infrastructure, and a lack of skilled healthcare professionals.

Home Health Hubs Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the home health hubs market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global home health hubs market include:

- Qualcomm

- Lamprey Networks

- Vivify Health

- Ihealth Lab

- AMC Health

- Honeywell International

- Ideal Life

- Insung Information

- MEDM

- Onkol

- Hicare

The global home health hubs market is segmented as follows:

By Product & Service

- Standalone Hub

- Mobile Hub

- Remote Patient Monitoring Service

By Type of Patient Monitoring

- High

- Moderate

- Low Acuity

End User

- Hospital

- Payers

- Home Care Agency

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global home health hubs market size was projected at approximately US$ 248.7 million in 2023. Projections indicate that the market is expected to reach around US$ 3792.18 million in revenue by 2032.

The global home health hubs market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 31.30% during the forecast period from 2024 to 2032.

North America is expected to dominate the global home health hubs market.

The significant factors driving the global home health hubs market include the rising prevalence of chronic diseases, growing demand for remote patient monitoring, advancements in telehealth technology, and increasing preference for home-based healthcare to reduce hospital admissions and healthcare costs.

Some of the prominent players operating in the global home health hubs market are; Qualcomm, Lamprey Networks, Vivify Health, Ihealth Lab, AMC Health, Honeywell International, Ideal Life, Insung Information, MEDM, Onkol, Hicare, and others.

Table Of Content

Inquiry For Buying

Home Health Hubs

Request Sample

Home Health Hubs