Industrial Fasteners Market Size, Share, and Trends Analysis Report

CAGR :

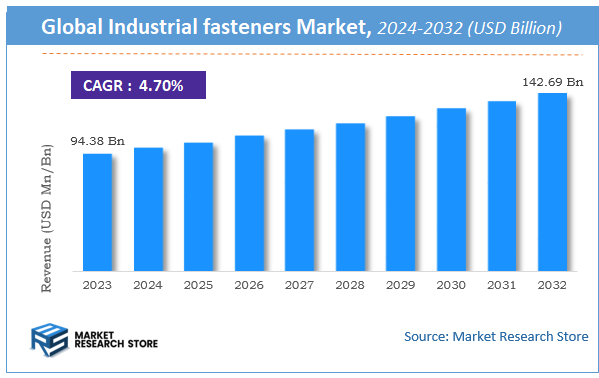

| Market Size 2023 (Base Year) | USD 94.38 Billion |

| Market Size 2032 (Forecast Year) | USD 142.69 Billion |

| CAGR | 4.7% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Industrial fasteners Market Insights

According to Market Research Store, the global industrial fasteners market size was valued at around USD 94.38 billion in 2023 and is estimated to reach USD 142.69 billion by 2032, to register a CAGR of approximately 4.7% in terms of revenue during the forecast period 2024-2032.

The industrial fasteners report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Industrial Fasteners Market: Overview

Industrial fasteners are mechanical components used to securely join or affix two or more objects together in a non-permanent or semi-permanent manner. These include a wide range of devices such as bolts, nuts, screws, washers, rivets, anchors, and pins, made from materials like carbon steel, stainless steel, brass, aluminum, and plastic. They are essential for ensuring the structural integrity, alignment, and functionality of machinery, equipment, buildings, and assemblies across industries such as automotive, aerospace, construction, electronics, energy, and manufacturing.

The growth of the industrial fasteners market is driven by increasing demand from automotive and construction sectors, rising infrastructure development, and advancements in industrial machinery. As modern manufacturing processes become more sophisticated, the need for high-performance, corrosion-resistant, and application-specific fastening solutions has intensified. Lightweight and custom-designed fasteners are gaining traction, particularly in automotive and aerospace applications where weight reduction and high strength are critical.

Key Highlights

- The industrial fasteners market is anticipated to grow at a CAGR of 4.7% during the forecast period.

- The global industrial fasteners market was estimated to be worth approximately USD 94.38 billion in 2023 and is projected to reach a value of USD 142.69 billion by 2032.

- The growth of the industrial fasteners market is being driven by rising demand across key sectors such as automotive, construction, aerospace, machinery, and electronics, where fasteners play a critical role in assembling components and ensuring structural integrity.

- Based on the raw material, the metal fasteners segment is growing at a high rate and is projected to dominate the market.

- On the basis of fasteners type, the bolts segment is projected to swipe the largest market share.

- In terms of product, the externally threaded fasteners segment is expected to dominate the market.

- Based on the application, the automotive segment is expected to dominate the market.

- In terms of distribution channel, the direct segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Industrial Fasteners Market: Dynamics

Key Growth Drivers:

- Booming Automotive and Aerospace Production: Both the automotive and aerospace industries are major consumers of industrial fasteners. The increasing global production of vehicles, especially the rising demand for electric vehicles (EVs) that require lightweight and specialized fasteners, as well as the continuous growth in aircraft manufacturing and maintenance, significantly drives demand for high-performance and customized fastening solutions.

- Strong Growth in Construction and Infrastructure Development: Massive investments in infrastructure projects (roads, bridges, railways, urban development) and a booming construction sector (residential, commercial, industrial buildings) globally are key drivers. Fasteners are indispensable for structural integrity in these applications, from large-scale civil engineering projects to modular building construction.

- Expansion of Industrial Machinery and Manufacturing: The general growth of the manufacturing sector across various industries (e.g., textiles, food & beverage, chemicals, heavy machinery) directly correlates with the demand for industrial fasteners. Fasteners are integral to the assembly, repair, and maintenance of all types of industrial equipment and machinery.

- Technological Advancements in Fastener Design and Materials: Continuous innovation in materials (e.g., high-strength steel, lightweight plastics, titanium alloys), coatings (for corrosion resistance), and design (e.g., self-locking fasteners, hybrid fasteners combining metal and plastic) leads to better performance, durability, and easier installation. These advancements enable fasteners to meet the evolving demands of modern engineering and drive market adoption.

Restraints:

- Volatility in Raw Material Prices: The primary raw materials for metal fasteners (steel, stainless steel, aluminum, brass, copper, titanium) are commodities whose prices can fluctuate significantly due to global supply-demand dynamics, geopolitical events, and energy costs. This volatility directly impacts the production costs of fasteners, affecting manufacturers' profit margins and pricing stability for end-users.

- Competition from Alternative Joining Technologies: While fasteners remain critical, they face increasing competition from alternative joining methods such as welding, adhesives, and advanced bonding techniques (e.g., automotive tapes). In some applications, these alternatives may offer advantages like lighter weight, improved aesthetics, or enhanced vibration dampening, potentially reducing the reliance on traditional mechanical fasteners.

- High Initial Investment for Advanced Manufacturing Technologies: Producing high-quality, precision industrial fasteners, especially those with advanced features or made from specialized materials, requires significant capital investment in sophisticated machinery, automation, and quality control systems. This high entry barrier can limit competition and slow down the adoption of newer production methods.

Opportunities:

- Growth of Lightweight Fasteners (Plastic & Hybrid): The automotive and aerospace industries' relentless pursuit of lightweighting for improved fuel efficiency and reduced emissions presents a significant opportunity for plastic fasteners and hybrid fasteners (combining plastic and metal). These offer advantages like corrosion resistance, lower cost, and reduced weight compared to traditional metal fasteners.

- Rising Demand for Customized and Application-Specific Fasteners: As industries evolve, there is a growing need for fasteners tailored to specific applications, offering unique features like anti-vibration properties, quick installation, or specialized coatings. This trend encourages collaboration between OEMs and fastener manufacturers, fostering innovation and higher-value offerings.

- Expansion in Renewable Energy and Electric Vehicle Manufacturing: The burgeoning renewable energy sector (wind turbines, solar panel mounting) and the rapid growth of electric vehicle (EV) production create new and specialized demand for fasteners. These applications often require fasteners with enhanced durability, corrosion resistance, and lightweight characteristics, providing a fertile ground for market expansion.

Challenges:

- Supply Chain Disruptions and Geopolitical Risks: The global nature of raw material sourcing and finished product distribution makes the industrial fasteners supply chain vulnerable to geopolitical tensions, trade wars, and unexpected events (e.g., pandemics, natural disasters). Ensuring supply chain resilience and security is a continuous challenge for manufacturers.

- Maintaining Consistent Quality and Traceability: With millions of fasteners produced daily for critical applications, ensuring consistent quality, dimensional accuracy, and material properties across all batches is paramount. Additionally, maintaining robust traceability systems to track fasteners from raw material to end-use is a significant logistical and data management challenge.

- Skilled Labor Shortages in Manufacturing: The industrial fastener manufacturing sector, like much of the broader manufacturing industry, faces a shortage of skilled labor, particularly for operating advanced machinery, quality control, and specialized processes. This can impact production capacity, efficiency, and the ability to adopt new technologies.

Industrial fasteners Market: Report Scope

This report thoroughly analyzes the Industrial fasteners Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Industrial fasteners Market |

| Market Size in 2023 | USD 94.38 Billion |

| Market Forecast in 2032 | USD 142.69 Billion |

| Growth Rate | CAGR of 4.7% |

| Number of Pages | 150 |

| Key Companies Covered | Standard Fasteners Ltd., Acument Global Technologies, Kova Fasteners Pvt. Ltd., Precision Castparts Corp., Nifco, LISI Group, ITW, Alcoa, Stanley Black & Decker, Hilti, ATF Inc. and MW Industries Inc. |

| Segments Covered | By Product, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Industrial Fasteners Market: Segmentation Insights

The global industrial fasteners market is divided by raw material, fasteners type, product, application, distribution channel, and region.

Based on raw material, the global industrial fasteners market is divided into metal fasteners and plastic fasteners. Metal Fasteners dominate the Industrial Fasteners Market owing to their superior strength, durability, and wide applicability across heavy-duty industries such as automotive, construction, aerospace, machinery, and industrial equipment. These fasteners are typically manufactured using steel, stainless steel, aluminum, brass, or titanium, and are preferred in applications where high mechanical strength, corrosion resistance, and load-bearing capacity are critical. Their use spans structural assembly, engine components, heavy machinery, and infrastructure projects. The rising demand for precision-engineered components and the growing need for high-performance mechanical joining solutions continue to drive the dominance of metal fasteners in the global market.

On the basis of fasteners type, the global industrial fasteners market is bifurcated into bolts, screws, nuts, washers, rivets, and others. Bolts dominate the Industrial Fasteners Market due to their critical role in high-strength, load-bearing applications across industries such as construction, automotive, aerospace, and heavy machinery. Bolts are used in conjunction with nuts and washers to secure parts together, and they offer strong, durable fastening solutions ideal for structures and machines subjected to high stress and vibration. Common variants include hex bolts, carriage bolts, and anchor bolts, each tailored for specific applications. Their ease of assembly and disassembly also supports their continued widespread use in both permanent and temporary structures.

In terms of product, the global industrial fasteners market is bifurcated into externally threaded fasteners, internally threaded fasteners, non-threaded threaded fasteners, and aerospace grade fasteners. Externally Threaded Fasteners dominate the Industrial Fasteners Market, primarily due to their widespread use in structural and mechanical applications across diverse sectors such as construction, automotive, heavy equipment, and infrastructure. These fasteners, which include bolts, screws, and studs, feature external threads designed to mate with internally threaded counterparts like nuts. They provide high tensile strength, ease of installation and removal, and robust clamping force, making them ideal for both permanent and semi-permanent joints. Their adaptability to different load conditions, materials, and environments ensures their critical role in industrial manufacturing and assembly operations.

Based on application, the global industrial fasteners market is bifurcated into automotive, aerospace, building & construction, industrial machinery, home appliances, lawns and gardens, motors and pumps, furniture, plumbing products, renewable energy, silo, and others. Automotive dominates the Industrial Fasteners Market due to the sheer volume of vehicles manufactured globally and the complex assembly processes involved. Fasteners are essential in securing various automotive components, including engines, chassis, interiors, and electronic systems. Both metal and plastic fasteners are used extensively to ensure structural integrity, reduce weight, and improve fuel efficiency. With increasing production of electric vehicles (EVs), the demand for lightweight and corrosion-resistant fasteners is further accelerating, solidifying the automotive sector’s position as the leading application segment.

In terms of distribution channel, the global industrial fasteners market is bifurcated into direct and indirect. Direct distribution dominates the Industrial Fasteners Market, particularly among large-scale manufacturers and industrial end-users who require customized, high-volume, and high-performance fastening solutions. In this channel, fastener producers sell directly to OEMs (Original Equipment Manufacturers) and large contractors, enabling stronger supplier relationships, better pricing control, and tailored logistics. Direct distribution is common in sectors like automotive, aerospace, construction, and heavy machinery, where tight tolerances, quality certifications, and technical support are critical. This model allows manufacturers to provide application-specific solutions, ensure timely delivery, and manage inventory through just-in-time (JIT) systems, enhancing operational efficiency for both parties.

Industrial Fasteners Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the industrial fasteners market, driven by advanced manufacturing capabilities, a large-scale automotive and aerospace sector, and expanding construction and machinery industries. The United States is the primary contributor, with high demand for a wide variety of fasteners—ranging from standard nuts and bolts to specialty high-strength fasteners used in aviation, defense, and heavy equipment manufacturing. The region also benefits from strict quality standards, which drive demand for precision-engineered fasteners made from stainless steel, titanium, and high-performance alloys. Construction activity, especially in commercial and residential infrastructure, continues to boost demand for anchors, screws, and nails. Canada supports market growth through mining, railway development, and machinery manufacturing. Ongoing investments in renewable energy and EV production are also prompting the adoption of customized and corrosion-resistant fasteners in North America.

Asia-Pacific is the fastest-growing region in the industrial fasteners market, supported by large-scale industrialization, infrastructure expansion, and the strong presence of automotive, electronics, and construction sectors. China dominates regional demand with extensive use of fasteners in consumer electronics, machinery, railways, and construction equipment. Domestic production is robust, and the country serves as a major exporter of standard fasteners globally. India’s market is growing rapidly due to rising infrastructure projects, housing development, and industrial machinery manufacturing. Japan and South Korea contribute significantly through demand for high-precision and high-strength fasteners in automotive assembly and consumer electronics. Southeast Asian countries are emerging as contract manufacturing hubs, further expanding regional demand. Despite cost advantages, the market faces challenges related to quality control and reliance on raw material imports in some nations.

Europe holds a significant share in the industrial fasteners market, supported by a well-developed automotive industry, stringent safety regulations, and growing emphasis on lightweight and durable fastening solutions. Germany, France, Italy, and the UK are major contributors, particularly in the manufacturing of automotive components, aerospace parts, and precision machinery. Demand is high for advanced fastening technologies such as rivets, clinching fasteners, and self-locking nuts that meet EU compliance standards. Lightweight fasteners are increasingly preferred to support emissions targets and fuel efficiency in vehicles. In addition, the renewable energy sector—particularly wind energy—relies heavily on high-performance fasteners capable of withstanding dynamic loads and corrosion. The rise of smart manufacturing and Industry 4.0 initiatives has also led to increased integration of automated fastening systems and digital torque tools.

Latin America is an emerging market for industrial fasteners, led by Brazil and Mexico. The region’s growth is driven by developments in automotive assembly, mining equipment, agriculture machinery, and commercial infrastructure. Mexico benefits from its integration into North American automotive and aerospace supply chains, which demand compliance with international fastener standards. Brazil, with its large construction and industrial equipment sector, uses a variety of fasteners ranging from structural bolts to specialty screws. Regional consumption remains lower compared to North America and Asia-Pacific due to economic constraints and a smaller industrial base, but infrastructure modernization and rising foreign investment in manufacturing are expected to boost demand for high-quality fastening solutions.

Middle East & Africa are developing regions in the industrial fasteners market, with demand driven by expanding construction, oil & gas projects, and energy infrastructure. The Middle East, particularly the UAE and Saudi Arabia, utilizes industrial fasteners in large-scale commercial and industrial construction, petrochemical installations, and mechanical equipment assembly. Investments in smart cities, metro networks, and green energy projects support further growth. In Africa, South Africa, Kenya, and Nigeria are key markets where demand comes from mining, utilities, and transportation infrastructure. However, the market is challenged by limited local manufacturing and heavy reliance on imports. Efforts to localize production and improve distribution networks are gradually improving access to higher-quality fastening products across the region.

Industrial Fasteners Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the industrial fasteners market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global industrial fasteners market include:

- Illinois Tool Works, Inc.

- Arconic Fastening Systems and Rings

- Hilti Corporation

- LISI Group - Link Solutions for Industry

- Nifco Inc

- MW Industries, Inc.

- Birmingham Fastener and Supply, Inc.

- SESCO Industries, Inc.,

- Elgin Fastener Group LLC

- Slidematic

- Dokka Fasteners A S

- Manufacturing Associates, Inc.

- Eastwood Manufacturing

- Acument Global Technologies, Inc.

- ATF, Inc.

- Standard Fasteners Ltd.

- Kova Fasteners Pvt. Ltd.

- Precision Castparts Corp.

- Alcoa

- Stanley Black & Decker

The global industrial fasteners market is segmented as follows:

By Raw Material

- Metal Fasteners

- Plastic Fasteners

By Fasteners Type

- Bolts

- Screws

- Nuts

- Washers

- Rivets

- Others

By Product

- Externally Threaded Fasteners

- Internally Threaded Fasteners

- Non-threaded Threaded Fasteners

- Aerospace Grade Fasteners

By Application

- Automotive

- Aerospace

- Building & Construction

- Industrial Machinery

- Home appliances

- Lawns and gardens

- Motors and pumps

- Furniture

- Plumbing products

- Renewable Energy

- Silo

- Others

By Distribution Channel

- Direct

- Indirect

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global industrial fasteners market , 2014 - 2020 (USD Billion)

- 2.2. Global industrial fasteners market: Snapshot

- Chapter 3. Industrial Fasteners Market – Global and Industry Analysis

- 3.1. Industrial Fasteners: Market dynamics

- 3.2. Market drivers

- 3.2.1. Drivers of global industrial fasteners market: Impact analysis

- 3.2.2. Rapidly expanding construction industry

- 3.2.3. Rising demand from automotive industry

- 3.3. Market restraints

- 3.3.1. Restraints of global industrial fasteners market: Impact analysis

- 3.3.2. High anti-dumping duties

- 3.4. Opportunities

- 3.4.1. Development in railroad fasteners

- 3.5. Porter’s five forces analysis

- 3.6. Market Attractiveness Analysis

- 3.6.1. Market attractiveness analysis by product segment

- 3.6.2. Market attractiveness analysis by application segment

- 3.6.3. Market attractiveness analysis by regional segment

- Chapter 4. Global Industrial Fasteners Market - Competitive Landscape

- 4.1. Company market share, 2014

- 4.2. Production capacity (subject to data availability)

- 4.3. Price trend analysis

- Chapter 5. Global Industrial Fasteners Market – Product Segment Analysis

- 5.1. Global industrial fasteners market: Product overview

- 5.1.1. Global industrial fasteners market share, by product, 2014 and 2020

- 5.2. Externally Threaded

- 5.2.1. Global externally threaded market , by product, 2014 – 2020 (USD Billion)

- 5.3. Aerospace Grade

- 5.3.1. Global aerospace grade market , by product, 2014 – 2020 (USD Billion)

- 5.4. Standard

- 5.4.1. Global standard industrial fasteners market , by product, 2014 – 2020 (USD Billion)

- 5.5. Others

- 5.5.1. Global other industrial fasteners market , by product, 2014 – 2020 (USD Billion)

- 5.1. Global industrial fasteners market: Product overview

- Chapter 6. Global Industrial Fasteners Market – Application Segment Analysis

- 6.1. Global industrial fasteners market: Application overview

- 6.1.1. Global industrial fasteners market share by application, 2014 and 2020

- 6.2. Automotive OEM

- 6.2.1. Global industrial fasteners market for automotive OEM, 2014 – 2020 (USD Billion)

- 6.3. Machinery OEM

- 6.3.1. Global industrial fasteners market for machinery OEM, 2014 – 2020 (USD Billion)

- 6.4. MRO and Construction

- 6.4.1. Global industrial fasteners market for MRO and construction applications, 2014 – 2020 (USD Billion)

- 6.5. Other OEM

- 6.5.1. Global industrial fasteners market for other OEM applications, 2014 – 2020 (USD Billion)

- 6.1. Global industrial fasteners market: Application overview

- Chapter 7. Global industrial fasteners Market – Regional Segment Analysis

- 7.1. Global industrial fasteners market: Regional overview

- 7.1.1. Global industrial fasteners market share by region, 2014 and 2020

- 7.2. North America

- 7.2.1. North America industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.2.2. North America industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.2.3. U.S.

- 7.2.3.1. U.S. industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.2.3.2. U.S. industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.3. Europe

- 7.3.1. Europe industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.3.2. Europe industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.3.3. Germany

- 7.3.3.1. Germany industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.3.3.2. Germany industrial fasteners market, by application, 2014 – 2020 (USD Million)

- 7.3.4. France

- 7.3.4.1. France industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.3.4.2. France industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.3.5. UK

- 7.3.5.1. UK industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.3.5.2. UK industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.4.2. Asia Pacific industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.4.3. China

- 7.4.3.1. China industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.4.3.2. China industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.4.4. Japan

- 7.4.4.1. Japan industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.4.4.2. Japan industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.4.5. India

- 7.4.5.1. India industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.4.5.2. India industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.5. Latin America

- 7.5.1. Latin America industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.5.2. Latin America industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.5.3. Brazil

- 7.5.3.1. Brazil industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.5.3.2. Brazil industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.6. Middle East & Africa

- 7.6.1. Middle East & Africa industrial fasteners market, by product, 2014 – 2020 (USD Billion)

- 7.6.2. Middle East & Africa industrial fasteners market, by application, 2014 – 2020 (USD Billion)

- 7.1. Global industrial fasteners market: Regional overview

- Chapter 8. Company Profile

- 8.1. Acument Global Technologies

- 8.1.1. Overview

- 8.1.2. Financials

- 8.1.3. Product portfolio

- 8.1.4. Business strategy

- 8.1.5. Recent developments

- 8.2. Standard Fasteners Ltd.

- 8.2.1. Overview

- 8.2.2. Financials

- 8.2.3. Product portfolio

- 8.2.4. Business strategy

- 8.2.5. Recent developments

- 8.3. Precision Castparts Corp.

- 8.3.1. Overview

- 8.3.2. Financials

- 8.3.3. Product portfolio

- 8.3.4. Business strategy

- 8.3.5. Recent developments

- 8.4. Nifco, LISI Group

- 8.4.1. Overview

- 8.4.2. Financials

- 8.4.3. Product portfolio

- 8.4.4. Business strategy

- 8.4.5. Recent developments

- 8.5. ITW

- 8.5.1. Overview

- 8.5.2. Financials

- 8.5.3. Product portfolio

- 8.5.4. Business strategy

- 8.5.5. Recent developments

- 8.6. Alcoa

- 8.6.1. Overview

- 8.6.2. Financials

- 8.6.3. Product portfolio

- 8.6.4. Business strategy

- 8.6.5. Recent developments

- 8.7. Kova Fasteners Pvt. Ltd.

- 8.7.1. Overview

- 8.7.2. Financials

- 8.7.3. Product portfolio

- 8.7.4. Business strategy

- 8.7.5. Recent developments

- 8.8. Hilti

- 8.8.1. Overview

- 8.8.2. Financials

- 8.8.3. Product portfolio

- 8.8.4. Business strategy

- 8.8.5. Recent developments

- 8.9. ATF Inc.

- 8.9.1. Overview

- 8.9.2. Financials

- 8.9.3. Product portfolio

- 8.9.4. Business strategy

- 8.9.5. Recent developments

- 8.10. Stanley Black & Decker

- 8.10.1. Overview

- 8.10.2. Financials

- 8.10.3. Product portfolio

- 8.10.4. Business strategy

- 8.10.5. Recent developments

- 8.11. MW Industries Inc.

- 8.11.1. Overview

- 8.11.2. Financials

- 8.11.3. Product portfolio

- 8.11.4. Business strategy

- 8.11.5. Recent developments

- 8.1. Acument Global Technologies

Inquiry For Buying

Industrial Fasteners

Request Sample

Industrial Fasteners