LMS Market Size, Share, and Trends Analysis Report

CAGR :

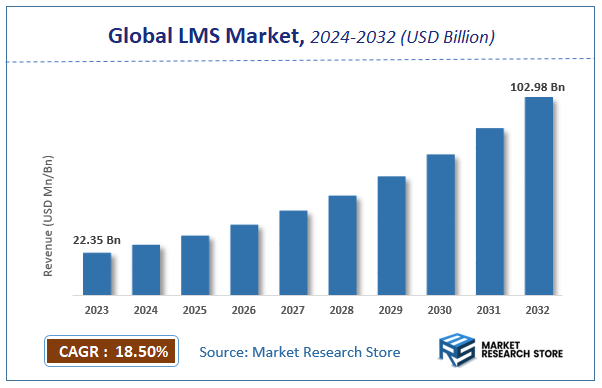

| Market Size 2023 (Base Year) | USD 22.35 Billion |

| Market Size 2032 (Forecast Year) | USD 102.98 Billion |

| CAGR | 18.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

LMS Market Insights

According to Market Research Store, the global LMS market size was valued at around USD 22.35 billion in 2023 and is estimated to reach USD 102.98 billion by 2032, to register a CAGR of approximately 18.5% in terms of revenue during the forecast period 2024-2032.

The LMS report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global LMS Market: Overview

Learning management system (LMS) is a software application or web-based technology used to plan, implement, and assess a specific learning process. Typically used in educational institutions, corporate environments, and government training programs, an LMS provides a centralized platform for content delivery, learner registration, course management, progress tracking, performance evaluation, and certification. It allows instructors to create and deliver content, monitor student participation, and assess performance, while learners can access learning materials anytime, anywhere. Popular LMS platforms include Moodle, Blackboard, Canvas, and SAP Litmos, each offering diverse features such as mobile learning, gamification, analytics, and integration with third-party tools.

Key Highlights

- The LMS market is anticipated to grow at a CAGR of 18.5% during the forecast period.

- The global LMS market was estimated to be worth approximately USD 22.35 billion in 2023 and is projected to reach a value of USD 102.98 billion by 2032.

- The growth of the LMS market is being driven by the increasing demand for e-learning solutions, digital transformation in educational institutions, and corporate upskilling needs.

- Based on the component, the solutions segment is growing at a high rate and is projected to dominate the market.

- On the basis of deployment, the cloud segment is projected to swipe the largest market share.

- In terms of enterprise size, the large enterprises segment is expected to dominate the market.

- Based on the delivery mode, the distance learning segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

LMS Market: Dynamics

Key Growth Drivers

- Increasing Digital Adoption by Educational Institutions and Businesses: Widespread implementation of LMS in corporate training and online education is driving strong demand.

- Cloud-Based and Mobile Learning: Flexibility and easy accessibility via cloud platforms and mobile devices are fueling LMS growth.

- AI-Driven Personalization: Features like adaptive learning and AI-powered analytics enhance user engagement and outcomes.

- Corporate Training & Compliance Needs: Growing remote work and upskilling requirements increase reliance on LMS for employee training.

Restraints

- High Implementation & Maintenance Costs: Initial investments and ongoing integration expenses can be significant barriers for some organizations.

- Security & Privacy Concerns: Potential risks around data protection delay or limit adoption in certain sectors.

- Integration & Infrastructure Limitations: Challenges in connecting LMS with existing IT systems and limited infrastructure in some regions restrict growth.

Opportunities

- Personalized & Gamified Learning: AI-driven adaptive learning, gamification, and microlearning offer engaging experiences that attract users.

- Expansion in Emerging Markets & Mobile Penetration: Rapid internet and smartphone adoption in developing regions open new growth avenues.

- Extended Use of AI and Analytics: Incorporating AI for content recommendations and predictive analytics unlocks further LMS potential.

Challenges

- Vendor Differentiation & Competitive Saturation: High competition requires strong user experience, support, and customization to stand out.

- Rapid Technological Evolution: Constant updates to comply with new standards and features demand sustained investments.

- User Adoption & Change Resistance: Resistance from educators and employees makes training, user-friendly interfaces, and support crucial.

LMS Market: Report Scope

This report thoroughly analyzes the LMS Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | LMS Market |

| Market Size in 2023 | USD 22.35 Billion |

| Market Forecast in 2032 | USD 102.98 Billion |

| Growth Rate | CAGR of 18.5% |

| Number of Pages | 174 |

| Key Companies Covered | Cornerstone Ondemand, Docebo, IBM, Netdimensions, SAP SE, Blackboard, SABA Software, Mcgraw-Hill Education, Pearson, D2L |

| Segments Covered | By Component, By Deployment, By Enterprise Size, By Delivery Mode, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

LMS Market: Segmentation Insights

The global LMS market is divided by component, deployment, enterprise size, delivery mode, and region.

Segmentation Insights by Component

Based on component, the global LMS market is divided into solution and services.

The LMS (Learning Management System) market, the Solutions segment holds the most dominant position. This dominance is largely due to the growing demand for robust software platforms that enable organizations, educational institutions, and enterprises to efficiently deliver, track, and manage learning programs. LMS solutions provide essential features such as content management, learner registration, progress tracking, assessments, and reporting, which make them a critical investment for digital learning initiatives. The increasing adoption of e-learning and digital training across various sectors fuels the need for advanced LMS solutions that can support diverse learning needs, scalability, and integration with other enterprise systems.

On the other hand, the Services segment, while smaller in comparison, plays a vital role in supporting LMS deployment, customization, integration, maintenance, and training. Service offerings typically include consulting, implementation, technical support, and managed services, which help organizations maximize the value of their LMS investments by tailoring the systems to their specific needs and ensuring smooth operation. As organizations increasingly recognize the importance of personalized and well-supported LMS environments, the services segment is witnessing steady growth, though it remains secondary to the solutions segment in market share.

Segmentation Insights by Deployment

On the basis of deployment, the global LMS market is bifurcated into cloud and on-premises.

In the LMS market segmentation by deployment, the Cloud segment is the most dominant compared to the On-Premises segment. The rapid growth of cloud-based LMS solutions is driven by their flexibility, scalability, and cost-effectiveness. Cloud deployment allows organizations to access learning platforms remotely without the need for significant upfront infrastructure investment or ongoing maintenance costs. This makes cloud LMS highly attractive, especially for small to medium-sized businesses and educational institutions seeking easy implementation and fast updates. Additionally, cloud LMS offers seamless integration with other cloud services and supports mobile learning, enabling learners to access content anytime, anywhere, which aligns with the increasing demand for remote and hybrid learning environments.

In contrast, the On-Premises deployment segment, while still relevant for organizations with strict data security, privacy requirements, or limited internet access, holds a smaller market share. On-premises LMS solutions require organizations to install and manage the software on their internal servers, leading to higher initial costs and the need for dedicated IT resources for maintenance and upgrades. Despite these challenges, some large enterprises and government institutions prefer on-premises LMS to maintain full control over their data and customization options.

Segmentation Insights by Enterprise Size

Based on enterprise size, the global LMS market is divided into small & medium enterprises and large enterprises.

In the LMS market segmentation by enterprise size, Large Enterprises represent the most dominant segment compared to Small and Medium Enterprises (SMEs). Large enterprises have extensive training and development needs across diverse departments and global locations, which drives their strong demand for comprehensive and scalable LMS solutions. These organizations typically invest heavily in advanced features such as customized learning paths, integration with existing enterprise systems (like HR and ERP), and robust analytics for workforce skill development. The ability to deliver consistent training at scale and comply with industry regulations further solidifies large enterprises as the leading adopters in the LMS market.

On the other hand, Small and Medium Enterprises (SMEs) are a growing segment but still smaller in market share. SMEs are increasingly adopting LMS solutions as digital learning becomes more accessible and affordable through cloud-based offerings. While their budgets and training needs are more limited compared to large enterprises, SMEs benefit from LMS platforms that offer easy deployment, lower costs, and essential features for employee upskilling and compliance training. The rise of flexible, subscription-based pricing models is encouraging more SMEs to adopt LMS solutions to enhance workforce productivity.

Segmentation Insights by Delivery Mode

On the basis of delivery mode, the global LMS market is bifurcated into distance learning, instructor-led training, and blended learning.

In the LMS market segmentation by delivery mode, Distance Learning emerges as the most dominant segment. This is largely due to the growing demand for remote education and training solutions that allow learners to access courses anytime and anywhere, without the constraints of physical location. Distance learning leverages digital platforms to deliver content, assessments, and interactions entirely online, making it highly scalable and flexible for both academic institutions and corporate training programs. The rise of mobile learning, video-based courses, and interactive modules further strengthens this segment's appeal in the evolving digital education landscape.

The Blended Learning segment, which combines online digital learning with traditional instructor-led sessions, holds the second position in market share. Blended learning is popular because it offers the benefits of flexibility while still allowing for personal interaction, collaboration, and hands-on experience. Many organizations and educational institutions prefer this mode as it caters to diverse learner preferences and enhances engagement and knowledge retention by integrating the strengths of both online and face-to-face learning.

The instructor-led training (ILT) segment, though still significant, ranks as the smallest among the three. ILT focuses primarily on traditional classroom or virtual instructor-driven sessions where learners interact directly with trainers. While ILT is preferred for its immediate feedback and personalized guidance, it is limited by logistical challenges, higher costs, and reduced scalability compared to digital modes. However, ILT remains essential for training that requires practical demonstrations, soft skills development, or complex discussions.

LMS Market: Regional Insights

- North America is expected to dominates the global market

The learning management system (LMS) market is most dominant in North America, driven by the early adoption of e-learning platforms, strong digital infrastructure, and the presence of major LMS providers. The region has seen widespread implementation of LMS solutions across both corporate and academic sectors, with a heavy emphasis on personalized learning, mobile-based platforms, and integration with AI-powered analytics. The U.S. leads the region’s demand due to its progressive educational technology ecosystem and high investments in corporate training programs.

Europe follows closely, propelled by the growing need for flexible education and vocational training across countries like Germany, the UK, and France. The European Union’s push for digital transformation in education, combined with language-diverse platform developments, has fueled LMS adoption. The corporate sector, particularly in Western Europe, is increasingly leveraging LMS for upskilling employees, while educational institutions embrace hybrid learning models to increase access and efficiency.

The Asia Pacific region is experiencing rapid growth, largely fueled by rising internet penetration, government-supported digital learning initiatives, and an expanding base of tech-savvy learners in countries such as India, China, Japan, and South Korea. The region is seeing a surge in demand from K–12 institutions and higher education bodies, while startups and SMEs are adopting LMS tools to deliver affordable and scalable learning experiences. Despite challenges in infrastructure in some rural areas, mobile learning and cloud-based LMS are bridging gaps in accessibility.

Latin America is witnessing steady adoption, especially in countries like Brazil, Mexico, and Argentina. The region is focusing on improving education quality and expanding access through online learning platforms. LMS implementation is gradually gaining momentum in public education systems and private organizations. While regulatory and funding challenges persist, partnerships with international LMS vendors are helping local players enhance content delivery and training models.

In the Middle East and Africa, LMS market development is still in its early phases but gaining attention due to increasing digital awareness and the rise of e-learning as a solution for regional education gaps. Countries like the UAE and Saudi Arabia are investing in digital education infrastructure as part of their national visions, leading to increased LMS uptake in schools, universities, and corporate environments. Africa shows potential, especially with mobile-first solutions, but infrastructural and affordability issues slow down widespread adoption.

LMS Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the LMS market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global LMS market include:

- Cornerstone Ondemand

- Docebo

- IBM

- Netdimensions

- SAP SE

- Blackboard

- SABA Software

- Mcgraw-Hill Education

- Pearson

- D2L

The global LMS market is segmented as follows:

By Component

- Solution

- Services

By Deployment

- Cloud

- On-Premises

By Enterprise Size

- Small & Medium Enterprises

- Large Enterprises

By Delivery Mode

- Distance Learning

- Instructor-led Training

- Blended Learning

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

LMS

Request Sample

LMS