Logistics Insurance Market Size, Share, and Trends Analysis Report

CAGR :

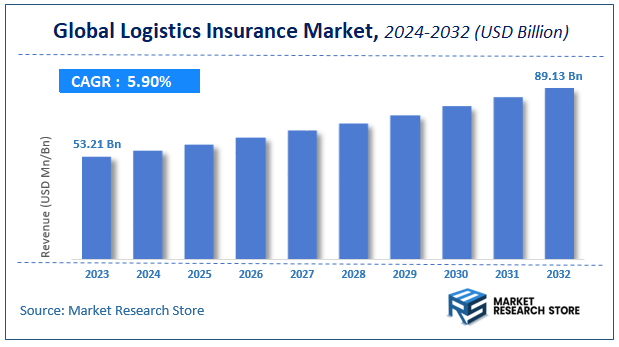

| Market Size 2023 (Base Year) | USD 53.21 Billion |

| Market Size 2032 (Forecast Year) | USD 89.13 Billion |

| CAGR | 5.9% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Logistics Insurance Market Insights

According to Market Research Store, the global logistics insurance market size was valued at around USD 53.21 billion in 2023 and is estimated to reach USD 89.13 billion by 2032, to register a CAGR of approximately 5.9% in terms of revenue during the forecast period 2024-2032.

The logistics insurance report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Logistics Insurance Market: Overview

Logistics insurance is a specialized form of coverage designed to protect businesses involved in the transportation, storage, and handling of goods against potential financial losses resulting from damage, theft, delay, or other disruptions during the logistics process. This type of insurance typically includes cargo insurance, liability insurance for logistics providers, warehouse insurance, and freight forwarders' liability. It can be customized to suit various modes of transport—such as air, sea, road, or rail—and covers a range of risks, including accidents, natural disasters, equipment failure, piracy, or mishandling during transit or warehousing.

The growth of logistics insurance is driven by the increasing complexity and globalization of supply chains, which expose goods to greater risk over longer distances and through multiple handling points. The rise of e-commerce, cross-border trade, and just-in-time delivery models has amplified the need for reliable risk management solutions. Businesses are placing greater emphasis on supply chain resilience, and comprehensive logistics insurance has become an essential component in mitigating financial exposure from unforeseen events. Additionally, advancements in digital logistics platforms and real-time tracking technologies are enabling more precise risk assessment and streamlined claims processing, further boosting the appeal and accessibility of logistics insurance across industries.

Key Highlights

- The logistics insurance market is anticipated to grow at a CAGR of 5.9% during the forecast period.

- The global logistics insurance market was estimated to be worth approximately USD 53.21 billion in 2023 and is projected to reach a value of USD 89.13 billion by 2032.

- The growth of the logistics insurance market is being driven by a confluence of factors, primarily the exponential expansion of global trade and e-commerce.

- Based on the industry, the transportation segment is growing at a high rate and is projected to dominate the market.

- On the basis of end user, the individual segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Logistics Insurance Market: Dynamics

Key Growth Drivers:

- Surge in E-commerce and Online Shopping: The exponential growth of online retail has led to a dramatic increase in the volume and frequency of goods being transported globally. This higher volume of shipments, often with faster delivery expectations, necessitates robust insurance solutions to cover risks associated with transportation, storage, and delivery, driving demand for comprehensive logistics insurance.

- Expansion of International Trade: Globalization and the interconnectedness of supply chains mean more goods are crossing borders than ever before. This expansion of international trade inherently increases exposure to risks such as cargo damage, theft, and geopolitical disruptions, thus boosting the need for specialized logistics insurance.

- Growing Supply Chain Complexities and Risk Awareness: Modern supply chains are intricate, involving multiple modes of transport, diverse geographies, and numerous stakeholders. This complexity, coupled with increased awareness among businesses about the financial losses stemming from unforeseen events like natural disasters, accidents, and geopolitical tensions, is driving a greater demand for comprehensive risk management and insurance solutions.

- Technological Advancements in Logistics: The adoption of technologies like IoT for real-time tracking, GPS monitoring, and data analytics in logistics provides insurers with better data for risk assessment and pricing, leading to more tailored and efficient insurance products. This technological integration also enables better risk mitigation and faster claims processing, making insurance more appealing.

- Stringent Regulatory Requirements: Various international and national regulations regarding cargo safety, transportation liability, and trade compliance necessitate businesses to secure adequate insurance coverage. This regulatory landscape acts as a foundational driver for the logistics insurance market.

Restraints:

- Lack of Uniformity in Coverage: The absence of standardized insurance coverage across different policies and regions can lead to confusion and perceived inadequacy for clients. This lack of uniformity can make it challenging for businesses to fully understand their coverage and for insurers to offer consistent products.

- High Perceived Costs and Price Sensitivity: Many smaller businesses, or those with limited understanding of potential risks, may view logistics insurance as an unnecessary expense. The high cost of premiums, especially for comprehensive coverage, can deter some potential clients, leading to a focus on basic, limited liability options.

- Complex Claims Processes: Tedious and lengthy claims settlement procedures can be a significant deterrent for businesses. The complexity of documentation, assessment, and dispute resolution can lead to frustration and undermine the perceived value of insurance.

- Limited Awareness in Emerging Markets: Despite rapid economic growth and increasing trade in emerging economies, there's often a lower awareness among businesses, particularly SMEs, about the full scope and benefits of logistics insurance, hindering market penetration.

Opportunities:

- Customized Insurance Solutions: The diverse and evolving needs of various industries (e.g., automotive, pharmaceuticals, retail) present a significant opportunity for insurers to develop highly customized and flexible insurance policies tailored to specific cargo types, transportation modes, and risk profiles.

- Leveraging Data Analytics and AI: The vast amount of data generated by modern logistics operations, combined with AI and machine learning, offers an opportunity for insurers to enhance risk assessment, develop predictive models for claims, improve underwriting accuracy, and offer dynamic pricing, thereby increasing efficiency and profitability.

- Parametric Insurance and Supply Chain Visibility Insurance: Innovations like parametric insurance, which triggers payouts based on predefined events (e.g., port congestion, extreme weather), and supply chain visibility insurance, which rewards businesses for real-time tracking and proactive risk management, present new avenues for growth by offering more predictable and rapid compensation.

- Expansion into Underserved Segments: There's an opportunity to cater to small and medium-sized enterprises (SMEs) and individual shippers who might currently be underinsured or lack comprehensive coverage, by offering more accessible and simplified policy options.

- Focus on Prevention-Based Insurance: As risks become more complex, there's an opportunity for insurers to move beyond just covering losses and instead invest in prevention. This includes offering services and technologies (e.g., real-time monitoring, risk assessment tools) that help clients anticipate and mitigate risks before they escalate, fostering stronger partnerships.

Challenges:

- Escalating Geopolitical Tensions and Supply Chain Disruptions: Ongoing geopolitical conflicts, trade wars, and unexpected events (like the Red Sea crisis) create unpredictable and high-risk environments for logistics. These disruptions can lead to increased shipping costs, longer transit times, and higher claim frequencies, making risk assessment and premium setting more challenging for insurers.

- Impact of Climate Change and Natural Disasters: The increasing frequency and severity of extreme weather events (e.g., floods, hurricanes, droughts affecting canals) directly impact transportation routes and cargo safety. This poses a significant challenge for insurers in accurately assessing and pricing risks, leading to potential premium increases and difficulty in providing stable coverage.

- Cybersecurity Risks in Digitalized Supply Chains: As logistics networks become more digitalized and interconnected, they become more vulnerable to cyberattacks (e.g., hacking of port systems, data breaches). Covering these complex and evolving cyber risks, which can lead to significant financial losses and operational disruptions, is a major challenge for the logistics insurance market.

- Underwriting Complexity and Data Gaps: Assessing risks for highly complex, global, multi-modal logistics operations can be incredibly challenging due to varied regulations, different modes of transport, and potential data silos. Incomplete or inconsistent data can hinder accurate risk assessment and lead to suboptimal pricing.

- Lack of Standardization in Data and Technology Integration: While technology offers opportunities, integrating disparate data systems and technologies across the vast logistics ecosystem can be challenging. A lack of standardization hinders seamless data flow and holistic risk management, making it difficult for insurers to leverage advanced analytics effectively.

Logistics Insurance Market: Report Scope

This report thoroughly analyzes the Logistics Insurance Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Logistics Insurance Market |

| Market Size in 2023 | USD 53.21 Billion |

| Market Forecast in 2032 | USD 89.13 Billion |

| Growth Rate | CAGR of 5.9% |

| Number of Pages | 194 |

| Key Companies Covered | Baozhunniu Sport, Ping An Insurance, China Life Insurance, SADLER & Company Inc, Envious Digital, Life Time Fitness Inc, GEICO, Aston Villa Football, China Pacific Life Insurance., Aviva, Metlife, American International, Allianz, DB Schenker, Dawson, G4S International Logistics, Integrity Transportation Insurance, Liberty Mutual Insurance, Peoples Insurance Agency, UPS Capital, Wells Fargo |

| Segments Covered | By Industry, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Logistics Insurance Market: Segmentation Insights

The global logistics insurance market is divided by industry, end user, and region.

Segmentation Insights by Industry

Based on industry, the global logistics insurance market is divided into transportation, marine, aviation, and others.

Transportation is the dominant segment in the logistics insurance market, accounting for the largest share due to the immense volume and value of goods transported via road, rail, and intermodal systems. This segment covers freight moved through trucking services, cargo trains, and third-party logistics (3PL) providers. Key risk factors—such as road accidents, cargo theft, vehicle breakdowns, delays, and exposure to weather conditions—necessitate robust insurance protection. With the rapid expansion of e-commerce and global trade, the reliance on road and rail transportation has increased significantly, particularly in urban and semi-urban zones. Logistics insurance for transportation typically includes motor truck cargo insurance, liability coverage, and general freight insurance policies, making it critical for shippers, freight forwarders, and logistics operators. Technological integration such as GPS tracking and telematics has also improved risk assessment and claims processing, further boosting the adoption of insurance services in this segment.

Marine segment plays a vital role in insuring international and long-distance freight transportation via sea. It includes ocean marine insurance for containerized cargo, bulk shipments, and breakbulk goods. Key risks covered include sinking, collisions, piracy, water damage, and loading/unloading mishaps. Despite its strategic importance in global trade, marine insurance accounts for a smaller portion of the overall logistics insurance market due to the slower shipping cycles and lower shipment frequency compared to road transport. However, it remains indispensable for industries involved in raw material imports, oil & gas, chemicals, and heavy machinery.

Aviation segment provides insurance for air freight logistics and is essential for high-value, time-sensitive cargo such as electronics, pharmaceuticals, and perishable goods. It includes coverage for cargo loss, delay, mishandling, and damages incurred during air transit. Though its market size is smaller due to limited cargo capacity and high costs associated with air transport, it remains crucial for industries that rely on just-in-time delivery and global reach. Insurance providers in this segment must comply with strict international aviation regulations and often offer specialized policies for charter and scheduled air cargo operations.

Segmentation Insights by End User

On the basis of end user, the global logistics insurance market is bifurcated into individual and enterprises.

The individual end-user segment dominates the logistics insurance market, driven by the growing number of personal shipments and small-scale consignments worldwide. With the surge in e-commerce and online retail, more consumers are shipping products domestically and internationally, creating an increased need for cargo protection. Individuals often insure personal belongings, gifts, and small packages against loss, damage, or theft during transit. The rise of convenient digital platforms and mobile apps has made it easier for individuals to purchase insurance quickly and affordably, contributing to this segment’s expansion. Additionally, increasing awareness about the risks involved in shipping and growing disposable incomes in emerging markets further support the dominance of individual users. Despite the smaller shipment volumes per transaction compared to enterprises, the sheer number of individual shipments cumulatively makes this segment the largest in terms of policy count and overall market share.

Enterprises segment, although significant, holds a smaller share compared to individuals in certain regions, especially where the gig economy, small businesses, and consumer-to-consumer shipments are prevalent. Enterprises require tailored logistics insurance for large-scale operations, but the dominance of individuals is increasingly apparent with the rise in last-mile deliveries, peer-to-peer shipments, and consumer-driven logistics.

Logistics Insurance Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Logistics Insurance Market, driven by the region’s well-developed transportation and supply chain infrastructure and high value of goods in transit. The United States leads demand due to its vast network of freight carriers, warehouses, and e-commerce fulfillment centers requiring comprehensive cargo and liability insurance coverage. Increasing regulatory requirements, rising concerns about theft, damage, and loss during transit, and the growth of complex multimodal logistics operations are propelling the adoption of customized insurance products. Canada also contributes with its expanding trade activities and growing emphasis on risk management solutions for perishable and high-value shipments.

Europe holds a significant share of the Logistics Insurance Market, supported by established global trade hubs such as Germany, the Netherlands, and the UK. The region benefits from strict regulatory frameworks mandating insurance coverage for freight and logistics activities, which drives market penetration. European companies are adopting technologically advanced insurance products integrating telematics, IoT sensors, and blockchain for real-time risk assessment and claims processing. Cross-border logistics in the European Union necessitate comprehensive insurance solutions, especially for international freight, customs clearance, and warehousing risks.

Asia-Pacific is witnessing rapid growth in the Logistics Insurance Market, propelled by booming e-commerce, increasing international trade, and investments in infrastructure across countries like China, India, Japan, and Southeast Asia. The region’s complex supply chains and rising volumes of perishable goods highlight the need for robust insurance products. Government initiatives to enhance transport safety and digitization of logistics processes are encouraging adoption. Local insurers are expanding their portfolios to cover emerging risks such as cyber threats and climate-related disruptions impacting logistics.

Latin America is an emerging market for Logistics Insurance, with Brazil, Mexico, and Argentina leading regional demand. The region’s logistics sector is growing due to expanding trade routes, infrastructure projects, and e-commerce penetration. However, challenges such as political instability, fluctuating regulations, and security risks (including cargo theft) increase the importance of specialized insurance policies. Insurers are tailoring products to address risks unique to Latin America, including transit delays and natural disasters, to attract logistics companies seeking risk mitigation.

Middle East and Africa represent developing regions for Logistics Insurance, with the Gulf Cooperation Council (GCC) countries and South Africa at the forefront. The Middle East benefits from strategic geographic positioning as a global trade and logistics hub, leading to higher demand for cargo and liability insurance. Investments in free zones, ports, and multimodal transportation support market expansion. In Africa, limited infrastructure and regulatory challenges constrain growth, but increasing international trade and foreign investments, especially in South Africa and Nigeria, are gradually boosting demand for logistics insurance solutions.

Logistics Insurance Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the logistics insurance market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global logistics insurance market include:

- Baozhunniu Sport

- Ping An Insurance

- China Life Insurance

- SADLER & Company Inc

- Envious Digital

- Life Time Fitness Inc

- GEICO

- Aston Villa Football

- China Pacific Life Insurance.

- Aviva

- Metlife

- American International

- Allianz

- DB Schenker

- Dawson

- G4S International Logistics

- Integrity Transportation Insurance

- Liberty Mutual Insurance

- Peoples Insurance Agency

- UPS Capital

- Wells Fargo

The global logistics insurance market is segmented as follows:

By Industry

- Transportation

- Marine

- Aviation

- Others

By End User

- Individual

- Enterprises

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Logistics Insurance

Request Sample

Logistics Insurance