Low Voltage Switchgear Market Size, Share, and Trends Analysis Report

CAGR :

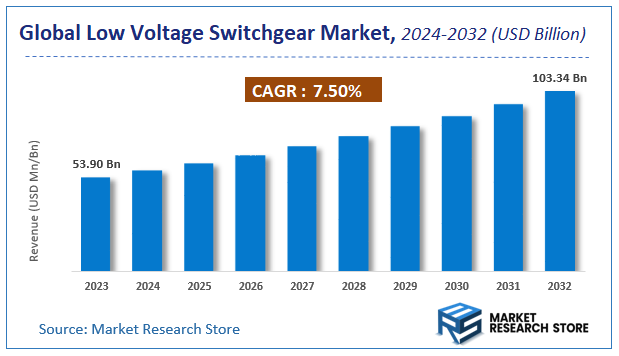

| Market Size 2023 (Base Year) | USD 53.90 Billion |

| Market Size 2032 (Forecast Year) | USD 103.34 Billion |

| CAGR | 7.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Low Voltage Switchgear Market Insights

According to Market Research Store, the global low voltage switchgear market size was valued at around USD 53.90 billion in 2023 and is estimated to reach USD 103.34 billion by 2032, to register a CAGR of approximately 7.5% in terms of revenue during the forecast period 2024-2032.

The low voltage switchgear report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Low Voltage Switchgear Market: Overview

Low voltage switchgear refers to electrical devices and systems designed to manage, protect, and isolate electrical equipment operating at voltages up to 1,000 volts AC or 1,500 volts DC. These systems include components such as circuit breakers, fuses, switches, and relays that are responsible for controlling the flow of electricity and protecting circuits from overloads, faults, and short circuits. Low voltage switchgear is critical in ensuring electrical safety and efficiency across a wide range of applications, including commercial buildings, industrial facilities, residential complexes, and public infrastructure. These systems can be mounted in panels or enclosures and are typically located close to the load to minimize voltage drops and improve system reliability.

Key Highlights

- The low voltage switchgear market is anticipated to grow at a CAGR of 7.5% during the forecast period.

- The global low voltage switchgear market was estimated to be worth approximately USD 53.90 billion in 2023 and is projected to reach a value of USD 103.34 billion by 2032.

- The growth of the low voltage switchgear market is being driven by increasing demand for safe and efficient electrical distribution systems across various sectors such as manufacturing, utilities, transportation, and construction.

- Based on the protection, the circuit breaker segment is growing at a high rate and is projected to dominate the market.

- On the basis of product, the fixed mounting segment is projected to swipe the largest market share.

- In terms of rated current, the ≤1,000 ampere segment is expected to dominate the market.

- Based on the voltage, the 251V to 750V segment is expected to dominate the market.

- In terms of end-user, the T&D Utility segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Low Voltage Switchgear Market: Dynamics

Key Growth Drivers:

- Growing Demand for Electricity Worldwide: Rapid urbanization, industrialization, and population growth are increasing electricity demand, thereby driving the need for reliable low voltage distribution systems.

- Rising Investments in Infrastructure Development: Government and private sector investments in residential, commercial, and industrial infrastructure globally are boosting demand for low voltage switchgear systems.

- Expansion of Renewable Energy Projects: The increasing integration of renewable energy sources such as solar and wind into the grid requires advanced low voltage switchgear for efficient energy distribution and safety.

- Modernization of Power Grids: The global trend toward upgrading aging grid infrastructure with smart technologies is supporting the adoption of intelligent and compact low voltage switchgear solutions.

- Focus on Energy Efficiency and Safety: Rising concerns about energy efficiency and electrical safety in buildings and industrial setups are encouraging the deployment of advanced low voltage switchgear.

Restraints:

- High Cost of Advanced Switchgear Systems: The initial investment required for installing modern, automated switchgear can be high, especially for small and medium enterprises (SMEs) or budget-constrained markets.

- Limited Awareness in Underdeveloped Regions: In certain developing or rural areas, a lack of awareness and technical expertise may hinder the adoption of modern low voltage switchgear technologies.

- Complexity in Integration with Legacy Systems: Upgrading or replacing traditional switchgear with advanced systems can pose compatibility issues and demand additional investments in system integration.

Opportunities:

- Smart Grid Development and Automation: The global move toward smart grid infrastructure offers significant growth opportunities for intelligent, automated low voltage switchgear systems with monitoring and control capabilities.

- Technological Advancements in Switchgear Design: Innovations such as modular, compact, and environmentally friendly switchgear designs are expanding market potential across various applications.

- Growing Demand in Emerging Economies: Rapid industrial growth and increasing electrification in Asia-Pacific, Africa, and Latin America present substantial market opportunities for switchgear manufacturers.

- Emphasis on Industrial Safety and Standards Compliance: Stricter safety regulations and electrical standards are pushing industries to upgrade to compliant low voltage switchgear systems.

Challenges:

- Volatility in Raw Material Prices: Fluctuations in the prices of metals like copper and aluminum, which are essential for switchgear manufacturing, can impact production costs and profitability.

- Highly Fragmented Market Structure: The presence of numerous regional and local players leads to intense competition and price pressure, which can affect margins and market consolidation.

- Cybersecurity Concerns in Smart Systems: With the growing deployment of digital and connected switchgear, cybersecurity risks have become a challenge, particularly in critical infrastructure.

- Supply Chain Disruptions: Global events such as pandemics, geopolitical tensions, or trade restrictions can disrupt the supply chain and delay project implementations.

Low Voltage Switchgear Market: Report Scope

This report thoroughly analyzes the Low Voltage Switchgear Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Low Voltage Switchgear Market |

| Market Size in 2023 | USD 53.90 Billion |

| Market Forecast in 2032 | USD 103.34 Billion |

| Growth Rate | CAGR of 7.5% |

| Number of Pages | 164 |

| Key Companies Covered | ABB, Powell Industries, Siemens, Schneider Electric, Bharat Heavy Electricals, Crompton Greaves, Eaton, Hyosung, Mitsubishi Electric, GE, OJSC Power Machines |

| Segments Covered | By Protection, By Product, By Rated Current, By Voltage, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Low Voltage Switchgear Market: Segmentation Insights

The global low voltage switchgear market is divided by protection, product, rated current, voltage, end-user, and region.

Segmentation Insights by Protection

Based on protection, the global low voltage switchgear market is divided into circuit breaker and fuse.

In the low voltage switchgear market, the circuit breaker segment is the most dominant by protection type. Circuit breakers are widely preferred due to their superior operational features, including automatic shutoff during overloads or short circuits and easy reset mechanisms. They offer reliable protection for electrical equipment and personnel, are more durable than fuses, and require less frequent replacement. Their versatility in both residential and industrial applications, combined with growing adoption in renewable energy infrastructure, has reinforced their market dominance.

On the other hand, the fuse segment holds a smaller share in the market. While fuses are cost-effective and simple in design, they are single-use components that require manual replacement once blown, leading to higher maintenance needs. They are still used in specific applications where simplicity and low cost are prioritized, especially in small-scale or low-budget installations. However, the inability to reset them after a fault and the rise of advanced, smart switchgear systems have contributed to their declining preference compared to circuit breakers.

Segmentation Insights by Product

On the basis of product, the global low voltage switchgear market is bifurcated into fixed mounting, and plug in & withdrawal unit.

In the low voltage switchgear market, the fixed mounting segment is the most dominant by product type. Fixed mounting switchgear is commonly used in applications where frequent rearrangement or removal of components is not required. These systems are robust, cost-effective, and offer a compact design suitable for stable environments such as manufacturing plants, commercial buildings, and utility substations. Due to their permanent installation, they also provide better mechanical strength and are less prone to mechanical wear, making them ideal for heavy-duty operations with minimal configuration changes.

The plug-in and withdrawal unit segment, while gaining traction, accounts for a smaller share of the market. These units allow for easier and quicker maintenance or replacement without interrupting the entire power system, making them highly suitable for environments that require high operational continuity such as data centers, hospitals, and critical infrastructure. Although they provide better flexibility and reduce downtime, their higher cost and complexity limit their widespread adoption compared to fixed mounting systems. Nonetheless, their usage is expected to grow steadily with the advancement of smart grid systems and the increasing emphasis on operational efficiency.

Segmentation Insights by Rated Current

Based on rated current, the global low voltage switchgear market is divided into <=1,000 ampere, 1,000 to 5,000 ampere, and >5,000 ampere.

In the low voltage switchgear market, the ≤1,000 Ampere segment is the most dominant by rated current. This segment caters primarily to residential, commercial, and light industrial applications where the electrical load is relatively low. The widespread use of low-capacity switchgear in buildings, small manufacturing units, and infrastructure projects makes this category the most extensively deployed. Its affordability, compact size, and suitability for mass deployment contribute significantly to its dominance.

Following this, the 1,000 to 5,000 Ampere segment holds a considerable share of the market. This range is commonly used in medium-sized industrial facilities, data centers, and commercial complexes with higher energy demands. It offers a balance between performance and cost, and provides enhanced protection and reliability in more demanding electrical environments. As industrial automation and digital infrastructure expand globally, this segment is witnessing steady growth.

The >5,000 Ampere segment is the least dominant but crucial for heavy industrial applications, large-scale power plants, and utility substations where extremely high electrical loads are common. These switchgear units are highly specialized, expensive, and require more advanced engineering, which limits their use to niche, high-demand sectors. Despite their limited adoption, their role is critical in ensuring uninterrupted power in mission-critical operations.

Segmentation Insights by Voltage

On the basis of voltage, the global low voltage switchgear market is bifurcated into upto 250v, 251v to 750v, and 750v to 1kv.

In the low voltage switchgear market, the 251V to 750V segment is the most dominant by voltage range. This range is widely used across industrial, commercial, and large residential applications due to its suitability for medium-scale electrical distribution systems. It offers a balance between power capacity and safety, making it ideal for use in manufacturing plants, office complexes, malls, and hospitals. The flexibility and reliability of switchgear in this voltage range have driven strong demand, especially as urban infrastructure and industrial facilities expand globally.

The 750V to 1KV segment follows, with a smaller yet significant share of the market. This higher voltage range is used in more demanding applications such as large industrial equipment, heavy machinery operations, and grid-connected renewable energy systems. Although the adoption rate is lower compared to the 251V to 750V segment, it is essential in high-load environments where stability and performance are critical. As electrification in heavy industries and energy-intensive sectors grows, this segment is expected to see increased demand.

The up to 250V segment is the least dominant. It is typically used in low-power applications such as residential buildings, small commercial units, and localized circuits. While this segment benefits from high-volume deployment, the lower revenue per unit and limited application scope compared to higher voltage ranges result in a smaller market share. Nonetheless, its role remains vital in basic electrical infrastructure, especially in developing regions.

Segmentation Insights by End-User

On the basis of end-user, the global low voltage switchgear market is bifurcated into T&D utility, commercial, industrial, residential, and others.

In the low voltage switchgear market, the T&D (Transmission & Distribution) utility segment is the most dominant by end-user. Utilities use low voltage switchgear extensively to manage, protect, and control power distribution in substations and local distribution networks. The growing demand for grid modernization, the expansion of renewable energy integration, and the increasing need for reliable electricity supply in urban and rural areas have significantly driven this segment’s growth. Utilities also invest heavily in infrastructure upgrades, which further bolsters demand for robust and efficient switchgear systems.

The industrial segment ranks next in dominance. Manufacturing plants, mining operations, oil & gas facilities, and process industries require reliable low voltage switchgear to handle high electrical loads and ensure operational safety. As industrial automation and electrification continue to rise, especially in developing economies, the demand in this segment remains strong.

Following closely is the commercial segment, which includes offices, shopping centers, hotels, and hospitals. These establishments require uninterrupted power and safety from electrical faults, making low voltage switchgear critical for daily operations. Urbanization, infrastructure development, and the boom in the service sector are contributing factors to its steady growth.

The residential segment, while smaller, still plays a vital role. Switchgear in homes ensures basic circuit protection and load management. Although each installation has a lower capacity, the sheer volume of residential construction projects, especially in emerging markets, ensures continued demand.

Low Voltage Switchgear Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region is the most dominant market for low voltage switchgear, driven by rapid industrialization, urban expansion, and significant investments in renewable energy infrastructure. Countries such as China and India are leading contributors due to their aggressive solar and wind energy programs, government-backed rural electrification initiatives, and rising demand for electricity across urban and semi-urban areas. The expansion of smart grid projects and adoption of distributed energy systems further strengthen the region’s leading position in the market.

North America follows as a strong market, primarily due to modernization of aging power infrastructure and the growing adoption of renewable energy. The United States is at the forefront, investing heavily in grid upgrades, smart distribution networks, and sustainable power generation sources. The region’s commitment to clean energy transition and enhancement of grid resilience drives demand for innovative and efficient low voltage switchgear solutions.

Europe is steadily expanding its low voltage switchgear market, supported by its focus on energy efficiency, sustainability, and emissions reduction. Countries like Germany are emphasizing smart residential energy systems and infrastructure upgrades, promoting the use of reliable switchgear to ensure safety and energy management. The region’s efforts in integrating renewable power sources into national grids have sustained market growth.

Latin America is emerging as a notable market, with countries such as Brazil and Argentina advancing investments in solar and wind power projects. The drive for electrification in underserved areas, along with national goals to reduce carbon footprints, supports the adoption of low voltage switchgear. Infrastructure development and foreign investments in energy networks contribute to increasing regional demand.

Middle East and Africa show steady market potential, largely fueled by infrastructure expansion, urban development, and diversification of energy portfolios. Gulf nations like Saudi Arabia and the UAE are initiating large-scale renewable projects, while African countries are focusing on electrification efforts in rural areas. Although the region currently lags behind others, ongoing strategic developments are expected to boost its market share in the coming years.

Low Voltage Switchgear Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the low voltage switchgear market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global low voltage switchgear market include:

- ABB

- Powell Industries

- Siemens

- Schneider Electric

- Bharat Heavy Electricals

- Crompton Greaves

- Eaton

- Hyosung

- Mitsubishi Electric

- GE

- OJSC Power Machines

The global low voltage switchgear market is segmented as follows:

By Protection

- Circuit Breaker

- Fuse

By Product

- Fixed Mounting

- Plug In and Withdrawal Unit

By Rated Current

- <=1000 Ampere

- 1000 TO 5000 Ampere

- >5000 Ampere

By Voltage

- Up To 250V

- 251V to 750V

- 750v to 1KV

By End-User

- T&D Utility

- Commercial

- Industrial

- Residential

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Low Voltage Switchgear

Request Sample

Low Voltage Switchgear