LVAD Market Size, Share, and Trends Analysis Report

CAGR :

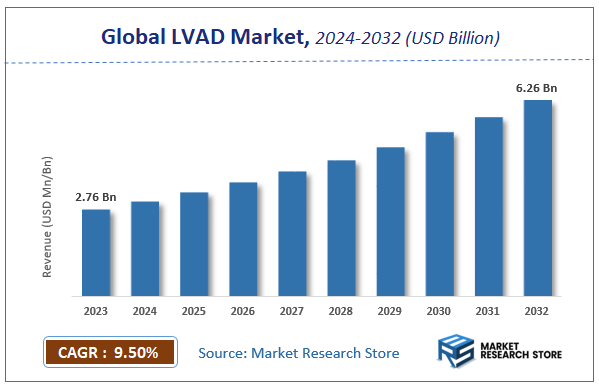

| Market Size 2023 (Base Year) | USD 2.76 Billion |

| Market Size 2032 (Forecast Year) | USD 6.26 Billion |

| CAGR | 9.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

LVAD Market Insights

According to Market Research Store, the global LVAD market size was valued at around USD 2.76 billion in 2023 and is estimated to reach USD 6.26 billion by 2032, to register a CAGR of approximately 9.5% in terms of revenue during the forecast period 2024-2032.

The LVAD report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global LVAD Market: Overview

LVAD Market focuses on mechanical devices that support the function of a failing heart, specifically the left ventricle, which is responsible for pumping oxygenated blood to the body. LVADs are primarily used in patients suffering from end-stage heart failure who are either awaiting heart transplants, ineligible for transplants, or undergoing recovery. These devices help maintain circulatory support, improving patient survival rates and quality of life. The market has grown due to rising incidences of cardiovascular diseases, aging populations, and increasing awareness about advanced heart failure therapies. Technological advancements have led to the development of smaller, more efficient, and durable LVADs that require fewer surgical interventions and offer improved patient mobility and long-term outcomes.

Additionally, continuous-flow devices are increasingly replacing older pulsatile systems due to their greater reliability and ease of implantation. The market is also shaped by ongoing research and innovation, alongside growing healthcare investments and improvements in cardiac care infrastructure across both developed and emerging regions. The LVAD market is competitive, with manufacturers focusing on refining device design, improving battery life, and reducing complications to enhance patient outcomes and extend the use of LVADs beyond traditional indications.

Key Highlights

- The LVAD market is anticipated to grow at a CAGR of 9.5% during the forecast period.

- The global LVAD market was estimated to be worth approximately USD 2.76 billion in 2023 and is projected to reach a value of USD 6.26 billion by 2032.

- The growth of the LVAD market is being driven by the increasing prevalence of heart failure, a shortage of donor hearts for transplantation, and continuous technological advancements in these life-saving devices.

- Based on the application, the bridge-to-transplant segment is growing at a high rate and is projected to dominate the market.

- On the basis of design, the transcutaneous ventricular assist devices segment is projected to swipe the largest market share.

- In terms of age, the adults segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

LVAD Market: Dynamics

Key Growth Drivers:

- Rising Prevalence of Advanced Heart Failure: The increasing incidence and prevalence of advanced heart failure globally, driven by factors such as aging populations, rising rates of cardiovascular diseases (including ischemic heart disease and hypertension), and improved survival rates from initial cardiac events, is the primary driver for LVAD adoption.

- Technological Advancements in LVADs: Continuous innovation in LVAD technology, including smaller and more durable devices, reduced complication rates (such as infection and thrombosis), pulsatile and continuous flow pumps, and less invasive implantation techniques, is expanding the eligible patient pool and improving outcomes, thus driving market growth.

- Growing Adoption of Destination Therapy (DT): Initially primarily used as a bridge to heart transplantation (BTT), LVADs are increasingly being adopted as a long-term or permanent treatment option (Destination Therapy) for patients with advanced heart failure who are not eligible for or are not candidates for heart transplantation. This significantly expands the potential patient population.

- Increasing Awareness and Acceptance Among Cardiologists: As clinical evidence supporting the benefits of LVADs in improving survival and quality of life for advanced heart failure patients accumulates, there is growing awareness and acceptance of these devices among cardiologists and heart failure specialists.

- Improved Patient Selection and Management Protocols: Advances in patient selection criteria, surgical techniques, and post-operative management protocols are leading to better patient outcomes and reduced complication rates, further driving the adoption of LVAD therapy.

- Favorable Reimbursement Policies in Some Regions: In certain developed countries, favorable reimbursement policies for LVAD implantation and follow-up care make the therapy more accessible to eligible patients, contributing to market growth.

Restraints:

- High Cost of LVAD Implantation and Maintenance: LVAD therapy involves a significant upfront cost for the device, surgical implantation, and subsequent long-term management, including device maintenance, medications, and regular follow-up. This high cost can be a major barrier to adoption, especially in regions with limited healthcare resources or inadequate reimbursement.

- Risk of Device-Related Complications: Despite technological advancements, LVADs are associated with potential complications such as infection, thromboembolism (blood clot formation), bleeding, pump malfunction, and stroke. These risks can limit the adoption of LVADs, particularly in patients with multiple comorbidities.

- Limited Number of Qualified Implanting Centers and Surgeons: The implantation and management of LVADs require specialized expertise and infrastructure, limiting the availability of qualified implanting centers and surgeons in many regions.

- Strict Patient Selection Criteria: While the indications for LVAD therapy are expanding, strict patient selection criteria are still in place to ensure optimal outcomes and minimize risks. This limits the number of patients who are considered suitable candidates.

- Lack of Long-Term Data in Certain Patient Subgroups: While substantial data exists on the benefits of LVADs, there may be limited long-term data in specific patient subgroups or with newer generation devices, which can influence physician and patient decisions.

- Ethical Considerations and Quality of Life Issues: Decisions regarding LVAD implantation, especially for destination therapy, involve complex ethical considerations and discussions about the patient's quality of life, potential limitations, and long-term prognosis.

Opportunities:

- Development of Minimally Invasive Implantation Techniques: Ongoing research and development focused on less invasive surgical approaches for LVAD implantation could reduce surgical risks, shorten hospital stays, and expand the applicability of the therapy to a broader range of patients.

- Advancements in Remote Monitoring and Management: The development and implementation of sophisticated remote monitoring systems can enable proactive management of LVAD patients, early detection of complications, and improved patient outcomes, potentially driving wider adoption.

- Expansion of Indications for LVAD Therapy: Ongoing clinical trials and research may lead to the expansion of indications for LVAD therapy to include patients with less advanced heart failure or other cardiovascular conditions.

- Development of Fully Implantable Artificial Hearts: The long-term goal of developing a reliable and durable fully implantable artificial heart could potentially replace the need for LVADs in some patients and revolutionize the treatment of end-stage heart failure.

- Growth in Emerging Markets: As healthcare infrastructure improves and awareness of advanced heart failure therapies increases in emerging economies, there is a significant potential for growth in the LVAD market in these regions.

- Personalized LVAD Therapy: Future advancements may focus on tailoring LVAD therapy to individual patient characteristics and disease profiles, optimizing device selection and management strategies for improved outcomes.

Challenges:

- Reducing Device-Related Complications: A major ongoing challenge is to further reduce the incidence of device-related complications such as infection, thrombosis, and bleeding through advancements in device design, materials, and patient management protocols.

- Improving Long-Term Durability and Reliability: Enhancing the long-term durability and reliability of LVADs is crucial to minimize the need for device replacements and improve the overall patient experience.

- Addressing the High Cost of Therapy: Finding ways to reduce the cost of LVAD therapy, including the device itself, implantation procedures, and long-term management, is essential to improve accessibility.

- Optimizing Patient Selection and Timing of Implantation: Identifying the optimal timing for LVAD implantation in the disease progression and selecting the most appropriate patients who will benefit most from the therapy remain critical challenges.

- Ensuring Adequate Training and Expertise: Expanding the availability of well-trained cardiac surgeons, cardiologists, and support staff who can effectively implant and manage LVAD patients is crucial for wider adoption.

- Improving Patient Quality of Life: While LVADs can significantly improve survival, addressing the quality of life issues associated with living with a mechanical circulatory support device, such as dependence on external power sources and lifestyle adjustments, remains a challenge.

LVAD Market: Report Scope

This report thoroughly analyzes the LVAD Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | LVAD Market |

| Market Size in 2023 | USD 2.76 Billion |

| Market Forecast in 2032 | USD 6.26 Billion |

| Growth Rate | CAGR of 9.5% |

| Number of Pages | 155 |

| Key Companies Covered | Evaheart Inc., Abbott Laboratories, CH Biomedical Inc., Bivacor Inc., Abiomed Inc., Berlin Heart GmbH, AdjuCor GmbH, Carmat SA, LivaNova PLC, Fineheart |

| Segments Covered | By Application, By Design, By Age, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

LVAD Market: Segmentation Insights

The global LVAD market is divided by application, design, age, and region.

Segmentation Insights by Application

Based on application, the global LVAD market is divided into bridge-to-transplant, destination therapy, bridge-to-recovery, and bridge to candidacy therapy.

Bridge-To-Transplant dominates the LVAD market as it serves as a critical life-sustaining intervention for patients with end-stage heart failure who are awaiting heart transplantation. LVADs in this application help improve hemodynamic stability, reduce symptoms of heart failure, and enhance patients' quality of life while they are on transplant waiting lists, which can often extend for months or years. The increasing global prevalence of heart failure and the shortage of donor hearts have significantly increased the reliance on LVADs as a bridge-to-transplant solution. Advancements in device miniaturization, durability, and patient outcomes have further solidified this segment’s leading position in the market.

Destination Therapy is the second-largest segment and is gaining momentum, especially among patients who are not eligible for heart transplantation due to age or comorbidities. In this application, LVADs are used as a long-term treatment rather than a temporary support. With the aging population and rising cases of chronic heart failure, the demand for destination therapy is expected to grow. Improvements in LVAD technology, including enhanced battery life, lower infection risk, and better mobility, are making long-term use more feasible and appealing, contributing to this segment’s expanding role in the market.

Bridge-To-Recovery involves the use of LVADs to support heart function temporarily in patients with acute heart failure or reversible myocardial damage, such as those recovering from myocarditis or cardiac surgery. In these cases, LVADs provide mechanical support while the heart heals and regains function. Though smaller in market share, this segment plays an essential role in specific clinical situations where myocardial recovery is anticipated. The demand for this application is supported by its success in reducing long-term dependency on mechanical circulatory support.

Bridge to Candidacy Therapy refers to the interim use of LVADs in patients who are initially deemed ineligible for transplant but may become suitable candidates after stabilization or improvement in comorbid conditions. This segment represents a niche but growing area, especially as clinicians adopt a more personalized approach to heart failure management. LVADs in this role offer a valuable therapeutic option to reevaluate and potentially upgrade patient candidacy for transplantation.

Segmentation Insights by Design

On the basis of design, the global LVAD market is bifurcated into transcutaneous ventricular assist devices and implantable ventricular assist devices.

Transcutaneous Ventricular Assist Devices, hold the dominate share of the LVAD market, primarily because of their ability to provide durable mechanical circulatory support with a lower risk of complications. These devices are generally used in short-term or emergency situations, such as acute cardiogenic shock or as temporary support during cardiac procedures. While they are less commonly used than implantable devices, transcutaneous LVADs serve a vital role in Bridge-To-Recovery scenarios or when implantable options are not feasible due to the patient’s condition. However, their use is limited by higher infection risks, patient discomfort, and restricted mobility, which reduces their adoption for long-term therapy.

Implantable Ventricular Assist Devices on the other hand, involve components that remain outside the body, typically with driveline access through the skin. These devices are surgically placed inside the body and connected to the heart and major blood vessels, offering continuous and reliable support for patients with advanced heart failure. The key advantages include reduced risk of driveline infections, improved patient mobility, and better quality of life compared to external or partially external systems. Implantable LVADs are especially favored in Bridge-To-Transplant and Destination Therapy applications, where long-term support is essential. Technological advancements, such as smaller device size, quieter operation, and enhanced battery life, have further reinforced their dominance in the market.

Segmentation Insights by Age

On the basis of age, the global LVAD market is bifurcated into adults and pediatrics.

Adults represent the dominate segment in the LVAD market, accounting for the majority of implantations globally. The prevalence of chronic conditions such as coronary artery disease, hypertension, and cardiomyopathy increases significantly with age, making adults—particularly those over 50—the primary candidates for LVAD therapy. Most applications of LVADs, including Bridge-To-Transplant, Destination Therapy, and Bridge-To-Recovery, are centered around adult patients. The availability of a wide range of device options tailored to adult physiology, combined with ongoing advancements in implantable LVAD technology, continues to drive adoption in this segment. Additionally, the presence of a larger eligible patient pool and more established treatment protocols further contributes to the segment’s dominance.

Pediatrics, while representing a smaller share of the market, plays a crucial role in specific cases involving congenital heart defects or pediatric cardiomyopathies. The use of LVADs in children is more limited due to anatomical and physiological differences, as well as the need for highly specialized devices and surgical expertise. However, advances in miniaturized ventricular assist devices and growing clinical experience are expanding the use of LVADs in pediatric populations, particularly as Bridge-To-Transplant in children awaiting donor hearts. Despite this progress, challenges such as device sizing, long-term management, and fewer FDA-approved pediatric LVADs continue to restrain growth in this segment.

LVAD Market: Regional Insights

- North America is expected to dominate the global market.

North America continues to dominate the global LVAD market due to its high incidence of cardiovascular diseases, especially end-stage heart failure. The U.S. boasts a highly developed healthcare infrastructure with advanced surgical centers capable of implanting LVADs. The presence of leading medical device manufacturers such as Abbott Laboratories and Medtronic fuels innovation and accessibility. North America also benefits from well-established reimbursement structures through private insurance and Medicare/Medicaid, which help offset the high costs of LVAD implantation. Moreover, active clinical research networks and FDA-approved advancements—such as fully implantable devices and improvements in driveline durability—are fostering further market expansion.

Asia-Pacific region is rapidly emerging as a high-growth market for LVADs due to its large and aging population, increasing incidence of heart failure, and ongoing healthcare modernization. Countries such as China, India, Japan, and South Korea are making substantial investments in cardiac care infrastructure, especially in urban hospitals and cardiac specialty centers. Japan, with its strong tradition of cardiovascular innovation, is one of the few APAC countries with relatively established LVAD programs. Meanwhile, China is ramping up the import and localized production of advanced cardiac devices, spurred by government initiatives promoting high-end medical technology. However, high procedure costs, limited skilled personnel, and variable reimbursement frameworks still present challenges across much of the region. Growing awareness of heart failure treatments, along with the expansion of private healthcare providers, is expected to drive sustained market growth.

Europe region represents a mature and steadily growing segment of the LVAD market. Countries like Germany, France, and the United Kingdom have made significant strides in the adoption of LVADs as both a bridge-to-transplant and destination therapy for patients ineligible for heart transplants. European healthcare systems provide widespread access to cardiac care through public health funding, though regional reimbursement models vary and may delay adoption in some markets. Additionally, the European regulatory environment—through entities like the European Medicines Agency (EMA) and MDR (Medical Device Regulation)—emphasizes stringent safety and quality standards. This has prompted manufacturers to prioritize compliance while introducing advanced LVAD models across the continent. Cross-border research collaborations, particularly among EU nations, further support clinical innovation and training programs in mechanical circulatory support.

Latin America region remains in a nascent stage for LVAD adoption but presents considerable future potential. The market here is supported by incremental improvements in public and private healthcare systems in countries like Brazil, Mexico, and Argentina. While overall cardiac care is improving, the high cost of LVAD devices, limited access to specialized cardiac centers, and unequal healthcare distribution are notable barriers. Nonetheless, rising awareness of advanced heart failure therapies and increasing government focus on reducing cardiovascular mortality are creating opportunities. International collaborations and partnerships with multinational device manufacturers are helping local hospitals acquire the expertise and equipment needed for LVAD implantation.

Middle East & Africa region represents the most underpenetrated market for LVADs but holds promise due to rising investment in healthcare infrastructure and growing demand for high-end cardiac treatments. Gulf countries like the UAE and Saudi Arabia are leading in adopting advanced medical technologies, with well-equipped specialty hospitals and a focus on attracting medical tourism. However, across broader MEA, especially in Sub-Saharan Africa, challenges such as lack of skilled cardiac surgeons, limited awareness, and insufficient reimbursement frameworks hinder widespread LVAD use. International partnerships, along with regional health reforms and the establishment of cardiac centers of excellence, are expected to contribute to gradual growth.

LVAD Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the LVAD market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global LVAD market include:

-

Evaheart Inc.

- Abbott Laboratories

- CH Biomedical Inc.

- Bivacor Inc.

- Abiomed Inc.

- Berlin Heart GmbH

- AdjuCor GmbH

- Carmat SA

- LivaNova PLC

- Fineheart

The global LVAD market is segmented as follows:

By Application

- Bridge-To-Transplant

- Destination Therapy

- Bridge-To-Recovery

- Bridge To Candidacy Therapy

By Design

- Transcutaneous Ventricular Assist Devices

- Implantable Ventricular Assist Devices

By Age

- Adults

- Pediatrics

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

LVAD

Request Sample

LVAD