Medical Telemetry Market Size, Share, and Trends Analysis Report

CAGR :

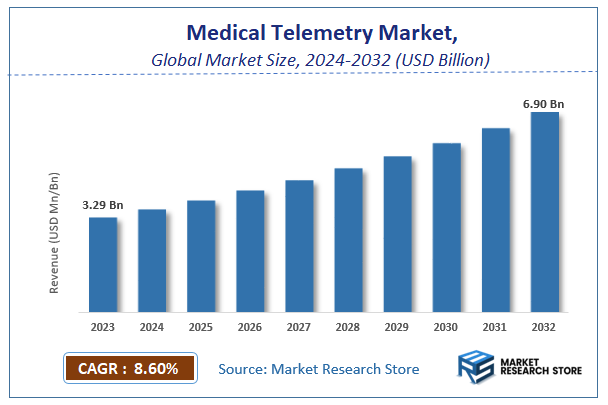

| Market Size 2023 (Base Year) | USD 3.29 Billion |

| Market Size 2032 (Forecast Year) | USD 6.90 Billion |

| CAGR | 8.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Medical Telemetry Market Insights

According to Market Research Store, the global medical telemetry market size was valued at around USD 3.29 billion in 2023 and is estimated to reach USD 6.90 billion by 2032, to register a CAGR of approximately 8.6% in terms of revenue during the forecast period 2024-2032.

The medical telemetry report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Medical Telemetry Market: Overview

Medical telemetry is a remote monitoring technology used in healthcare to track patients' vital signs, such as heart rate, blood pressure, oxygen levels, and other physiological parameters, in real time. This technology is widely used in hospitals, outpatient settings, and home healthcare to provide continuous patient monitoring without the need for wired connections. It enhances patient mobility, improves early detection of critical conditions, and allows healthcare providers to make timely interventions, ultimately leading to better patient outcomes.

Key Highlights

- The medical telemetry market is anticipated to grow at a CAGR of 8.6% during the forecast period.

- The global medical telemetry market was estimated to be worth approximately USD 3.29 billion in 2023 and is projected to reach a value of USD 6.90 billion by 2032.

- The growth of the medical telemetry market is being driven by increasing prevalence of chronic diseases, the rising geriatric population, and the growing demand for remote patient monitoring.

- Based on the type, the hardware segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the cardiology segment is projected to swipe the largest market share.

- In terms of end user, the providers segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Medical Telemetry Market: Dynamics

Key Growth Drivers:

- Rise of Telehealth and Remote Patient Monitoring: The growing adoption of telehealth and remote patient monitoring (RPM) solutions is a major driver. Medical telemetry enables continuous monitoring of patients' vital signs and other health parameters remotely, improving patient care and reducing healthcare costs.

- Aging Population: The aging population, with an increased prevalence of chronic diseases, necessitates continuous monitoring and management of health conditions. Medical telemetry provides a valuable tool for managing chronic diseases like heart failure, diabetes, and respiratory conditions.

- Technological Advancements: Advancements in wireless communication technologies, miniaturization of sensors, and the development of AI/ML-powered analytics are driving innovation in medical telemetry systems, leading to improved accuracy, efficiency, and patient outcomes.

- Focus on Preventive Care: The increasing emphasis on preventive healthcare and early disease detection is driving the demand for remote patient monitoring solutions, including those enabled by medical telemetry.

Restraints:

- Data Security and Privacy Concerns: Concerns about data security and privacy related to the transmission and storage of sensitive patient data can hinder the widespread adoption of medical telemetry systems.

- Interoperability Challenges: Ensuring interoperability between different medical devices, software platforms, and healthcare systems can be a significant challenge.

- Regulatory Hurdles: Navigating regulatory hurdles related to data privacy, device approval, and reimbursement can be complex and time-consuming.

- Limited Access to Technology: Access to reliable internet connectivity and affordable devices can be a barrier for some patients, particularly in underserved communities.

Opportunities:

- Integration with AI and Machine Learning: Integrating AI and machine learning algorithms can enable predictive analytics, early detection of health deterioration, and personalized treatment plans.

- Development of Wearable Technologies: The development of advanced wearable devices that seamlessly integrate with medical telemetry systems can enhance patient comfort and improve data collection.

- Expansion of Applications: Exploring new applications for medical telemetry, such as in mental health, geriatrics, and rehabilitation, can expand the market and improve patient care across a wider range of conditions.

- Focus on Home Healthcare: The increasing emphasis on home healthcare and the need to reduce hospital readmissions provide significant opportunities for the growth of home-based medical telemetry solutions.

Challenges:

- Ensuring Data Accuracy and Reliability: Ensuring the accuracy and reliability of data collected by medical telemetry devices is crucial for making informed clinical decisions.

- Addressing Patient Acceptance and Engagement: Ensuring patient acceptance and engagement with remote monitoring technologies is critical for successful implementation.

- Maintaining Data Integrity and Security: Protecting patient data from cyber threats and ensuring the integrity of data transmission and storage are critical challenges.

- Skilled Workforce: The need for skilled professionals to manage and interpret data generated by medical telemetry systems is growing.

Medical Telemetry Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Medical Telemetry Market |

| Market Size in 2023 | USD 3.29 Billion |

| Market Forecast in 2032 | USD 6.90 Billion |

| Growth Rate | CAGR of 8.6% |

| Number of Pages | 140 |

| Key Companies Covered | Siemens AG, GE Healthcare, Astro-Med, Philips Healthcare, Lindsay Corporation, Honeywell International, IBM Corp, Finmeccanica SPA., Medtronic, BioTelemetry, Applied Cardiac Systems, Medicomp, Preventice Services, The Scottcare Corporation, Medi-Lynx, Zoll Medical Corporation, Welch Allyn, Telerhythmics |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Medical Telemetry Market: Segmentation Insights

The global medical telemetry market is divided by type, application, end user and region.

Segmentation Insights by Type

Based on type, the global medical telemetry market is divided into hardware, software, and service.

In the medical telemetry market, hardware emerges as the most dominant segment. This segment includes a wide range of devices such as patient monitoring systems, telemetry transmitters, ECG telemetry units, and wireless communication modules. The increasing adoption of advanced medical devices in hospitals and healthcare facilities, coupled with the rising demand for real-time patient monitoring, drives the dominance of hardware in this market. Additionally, advancements in wireless technology and miniaturization of telemetry devices have further propelled the growth of this segment.

Following hardware, the software segment holds a significant position in the medical telemetry market. Software solutions are essential for processing and analyzing the vast amounts of patient data collected through telemetry devices. These solutions include data management systems, real-time monitoring platforms, and cloud-based analytics tools that help healthcare professionals make informed decisions. The growing integration of artificial intelligence (AI) and machine learning (ML) in telemetry software has enhanced predictive analytics, enabled early detection of health complications and improved patient outcomes.

The service segment, while essential, remains the least dominant in comparison to hardware and software. This segment comprises installation, maintenance, consulting, and training services that support the efficient functioning of medical telemetry systems. The demand for services is driven by the increasing adoption of telemetry systems in healthcare settings and the need for ongoing system upgrades, technical support, and compliance with evolving healthcare regulations. However, since services are often bundled with hardware and software solutions, their standalone market share remains relatively lower than the other segments.

Segmentation Insights by Application

On the basis of application, the global medical telemetry market is bifurcated into radiology, cardiology, remote ICU, psychology, dermatology.

In the medical telemetry market, cardiology stands as the most dominant application. The high prevalence of cardiovascular diseases (CVDs), including heart attacks, arrhythmias, and hypertension, has significantly increased the demand for telemetry systems in cardiology. These systems allow continuous cardiac monitoring, helping healthcare professionals detect abnormalities in real time, improving patient outcomes, and reducing the risk of severe complications. The widespread adoption of ECG telemetry, Holter monitors, and wearable heart monitors in hospitals and homecare settings further strengthens the dominance of this segment.

Remote ICU (Intensive Care Unit) follows as another crucial application in the medical telemetry market. The growing need for critical care monitoring, especially in emergency situations and during post-operative recovery, has fueled the demand for telemetry solutions in ICUs. Remote ICU setups allow healthcare providers to monitor patients' vital signs, respiratory functions, and other critical parameters in real time, enabling timely intervention even from distant locations. The rising adoption of telemedicine and AI-powered monitoring tools further enhances the growth of this segment.

Radiology is another important segment, as medical telemetry plays a key role in transmitting diagnostic imaging data from remote locations to specialists for quick interpretation. With the increasing use of digital imaging, including MRI, CT scans, and X-rays, telemetry solutions help in securely transferring large imaging files between hospitals, radiology labs, and healthcare professionals. The growing demand for teleradiology, especially in regions with limited access to radiologists, is further driving the adoption of telemetry in this field.

Psychology is a growing application in the medical telemetry market, particularly with the rise of mental health monitoring solutions. Wearable devices and mobile applications equipped with telemetry capabilities allow for the continuous tracking of physiological responses related to stress, anxiety, and mood disorders. These tools help psychologists and mental health professionals analyze patient behavior patterns, ensuring more personalized treatment approaches. The increasing awareness and acceptance of digital mental health solutions contribute to the expansion of this segment.

Dermatology is the least dominant application in the medical telemetry market. While remote dermatology consultations and digital imaging solutions are becoming more common, the need for continuous real-time monitoring is comparatively lower than in other medical fields. Teledermatology primarily relies on image-based diagnostics rather than telemetry-driven monitoring. However, the growing adoption of AI-powered skin assessment tools and mobile health applications is expected to gradually expand the role of telemetry in dermatology.

Segmentation Insights by End User

On the basis of end user, the global medical telemetry market is bifurcated into payers, providers, and patients.

In the medical telemetry market, providers are the most dominant end-user segment. This category includes hospitals, clinics, diagnostic centers, and healthcare facilities that rely on telemetry solutions for real-time patient monitoring and diagnostics. The increasing adoption of telemetry in critical care units, cardiology departments, and remote patient monitoring has made providers the primary users of medical telemetry systems. With the growing integration of AI and cloud-based telemetry solutions, healthcare providers can enhance patient care, reduce hospital readmissions, and improve workflow efficiency. The rising demand for remote monitoring solutions, particularly after the COVID-19 pandemic, has further strengthened the dominance of this segment.

Patients represent the second-largest end-user segment, driven by the increasing preference for home-based and remote healthcare solutions. With the rise of wearable telemetry devices, such as heart monitors, glucose monitors, and remote ECG patches, patients are now more actively involved in managing their health conditions. The convenience of continuous health tracking, combined with the growing awareness of chronic disease management, has fueled the demand for telemetry among patients. Additionally, advancements in mobile health apps and smart devices have made it easier for individuals to monitor their vitals and share real-time data with healthcare providers, leading to better preventive care and early disease detection.

Payers, including insurance companies and government healthcare programs, constitute the least dominant end-user segment. While payers do not directly use telemetry solutions, they play a crucial role in reimbursement policies and healthcare financing. The increasing focus on value-based care and cost reduction has encouraged payers to support the adoption of medical telemetry systems, as these solutions help in reducing hospital stays and emergency visits. By promoting remote monitoring and early intervention, payers can help lower overall healthcare costs and improve patient outcomes. However, their role remains more indirect compared to providers and patients.

Medical Telemetry Market: Regional Insights

- North America is expected to dominates the global market

North America dominates the medical telemetry market due to its advanced healthcare infrastructure and widespread adoption of telehealth solutions. The presence of key market players, along with favorable reimbursement policies, has significantly contributed to market expansion. The rising prevalence of chronic diseases has further driven demand for remote patient monitoring, making medical telemetry essential in hospitals and homecare settings. Additionally, ongoing technological advancements and strong investments in research and development continue to enhance market growth in this region.

Europe holds the second-largest market share, driven by the adoption of advanced telemetry devices and increasing government initiatives supporting digital health solutions. Countries such as Germany, the United Kingdom, and France lead the region in healthcare digitization, integrating medical telemetry into hospital networks and outpatient care. The growing elderly population and the increasing burden of chronic diseases have further accelerated the demand for remote monitoring solutions. The region’s regulatory environment and emphasis on patient safety also promote the adoption of medical telemetry technologies.

The Asia-Pacific region is witnessing the fastest growth in the medical telemetry market due to rapid urbanization, increasing healthcare expenditure, and technological advancements. Countries like China, Japan, and India are experiencing a surge in telehealth adoption, supported by improved internet connectivity and rising smartphone penetration. Government policies promoting digital health and the expansion of healthcare services in rural areas are further driving market expansion. The increasing focus on smart hospitals and artificial intelligence-driven healthcare solutions is expected to fuel the demand for medical telemetry in this region.

Latin America is emerging as a promising market, primarily due to efforts to improve healthcare accessibility in remote and underserved areas. Countries such as Brazil and Mexico are investing in telehealth infrastructure, leading to the gradual adoption of medical telemetry solutions. The growing awareness of remote patient monitoring, coupled with increasing healthcare funding, is supporting market growth. As more healthcare providers recognize the benefits of telemetry in managing chronic conditions, the demand for these technologies is expected to rise.

The Middle East and Africa have the smallest market share but present significant growth potential. Economic disparities across the region have impacted the adoption of medical telemetry, but ongoing investments in healthcare infrastructure are fostering market expansion. Countries like the UAE and Saudi Arabia are taking initiatives to promote digital health strategies, improving access to medical telemetry solutions. With increasing government efforts to modernize healthcare facilities and integrate advanced monitoring technologies, the market in this region is expected to witness steady growth in the coming years.

Medical Telemetry Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the medical telemetry market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global medical telemetry market include:

- Siemens AG

- GE Healthcare

- Astro-Med

- Philips Healthcare

- Lindsay Corporation

- Honeywell International

- IBM Corp

- Finmeccanica SPA.

- Medtronic

- BioTelemetry

- Applied Cardiac Systems

- Medicomp

- Preventice Services

- The Scottcare Corporation

- Medi-Lynx

- Zoll Medical Corporation

- Welch Allyn

- Telerhythmics

The global medical telemetry market is segmented as follows:

By Type

- Hardware

- Software

- Service

By Application

- Radiology

- Cardiology

- Remote ICU

- Psychology

- Dermatology

- Other

By End User

- Payers

- Providers

- Patients

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global medical telemetry market size was projected at approximately US$ 3.29 billion in 2023. Projections indicate that the market is expected to reach around US$ 6.90 billion in revenue by 2032.

The global medical telemetry market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 8.6% during the forecast period from 2024 to 2032.

North America is expected to dominate the global medical telemetry market.

The global medical telemetry market is driven by the increasing prevalence of chronic diseases, rising demand for remote patient monitoring, and advancements in wireless and AI-integrated healthcare technologies. Additionally, the expansion of telehealth services, growing geriatric population, and government initiatives supporting digital health solutions further boost market growth.

Some of the prominent players operating in the global medical telemetry market are; Siemens AG, GE Healthcare, Astro-Med, Philips Healthcare, Lindsay Corporation, Honeywell International, IBM Corp, Finmeccanica SPA., Medtronic, BioTelemetry, Applied Cardiac Systems, Medicomp, Preventice Services, The Scottcare Corporation, Medi-Lynx, Zoll Medical Corporation, Welch Allyn, Telerhythmics, and others.

Table Of Content

Inquiry For Buying

Medical Telemetry

Request Sample

Medical Telemetry