Micro Flute Paper Market Size, Share, and Trends Analysis Report

CAGR :

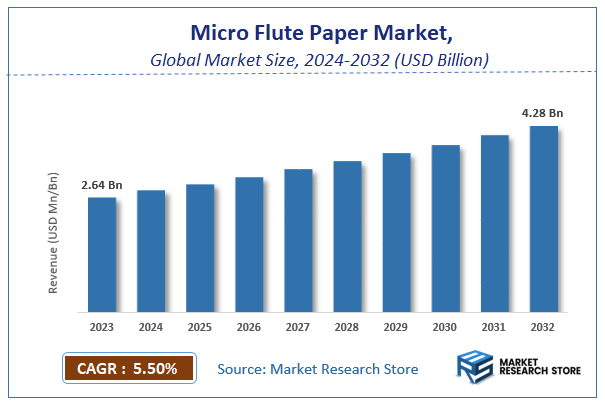

| Market Size 2023 (Base Year) | USD 2.64 Billion |

| Market Size 2032 (Forecast Year) | USD 4.28 Billion |

| CAGR | 5.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Micro Flute Paper Market Insights

According to Market Research Store, the global micro flute paper market size was valued at around USD 2.64 billion in 2023 and is estimated to reach USD 4.28 billion by 2032, to register a CAGR of approximately 5.5% in terms of revenue during the forecast period 2024-2032.

The micro flute paper report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Micro Flute Paper Market: Overview

Micro flute paper refers to a type of corrugated cardboard characterized by its fine, small flutes (waves) that provide enhanced strength, durability, and printability while maintaining a lightweight profile. The most common types of micro flutes include E-flute, F-flute, and N-flute, with flute heights ranging from 0.6 mm to 1.5 mm. These flutes are smaller than traditional corrugated flutes, making micro flute paper ideal for applications requiring a smooth surface for high-quality printing, such as packaging for retail, cosmetics, electronics, and food industries. Its compact structure also offers excellent cushioning and stacking strength, making it a popular choice for both protective and aesthetic packaging solutions.

Key Highlights

- The micro flute paper market is anticipated to grow at a CAGR of 5.5% during the forecast period.

- The global micro flute paper market was estimated to be worth approximately USD 2.64 billion in 2023 and is projected to reach a value of USD 4.28 billion by 2032.

- The growth of the micro flute paper market is being driven by increasing demand for sustainable, lightweight, and visually appealing packaging solutions across various industries.

- Based on the flute type, the E-flute segment is growing at a high rate and is projected to dominate the market.

- On the basis of end-use, the food & beverage segment is projected to swipe the largest market share.

- By region, Asia-Pacific is expected to dominate the global market during the forecast period.

Micro Flute Paper Market: Dynamics

Key Growth Drivers:

- Rising Demand for Sustainable Packaging: Micro flute paper is a highly recyclable and biodegradable material, making it an attractive alternative to traditional packaging materials like plastic. Growing environmental awareness and stricter regulations on packaging waste are driving demand for eco-friendly solutions.

- Growth of E-commerce: The rapid expansion of e-commerce has increased the need for protective packaging to ensure products arrive safely. Micro flute paper provides excellent cushioning and protection, making it ideal for shipping a wide range of goods.

- Lightweight and Cost-Effective: Micro flute paper is lightweight, which helps reduce shipping costs. It also offers a good balance of strength and cost-effectiveness compared to other packaging materials.

- Versatility and Customization: Micro flute paper can be easily customized in terms of size, shape, and printing, making it suitable for a variety of applications and branding needs.

- Increasing Use in Food and Beverage: Micro flute paper is used in food and beverage packaging due to its ability to protect products from damage and maintain freshness. It is also increasingly used for takeaway containers and other food service applications.

Restraints:

- Competition from Other Materials: Micro flute paper faces competition from other packaging materials, such as corrugated cardboard, plastic, and paperboard. These materials may offer certain advantages in terms of cost, strength, or specific applications.

- Price Fluctuations of Raw Materials: The price of raw materials used to produce micro flute paper, such as pulp and recycled paper, can fluctuate, affecting the overall cost of production.

- Limited Strength for Heavy Products: While micro flute paper offers good protection for lightweight to medium-weight items, it may not be suitable for packaging very heavy or bulky products.

- Challenges in Recycling: Although micro flute paper is recyclable, the recycling process can be challenging due to the presence of adhesives and coatings. This can limit the recyclability of some micro flute paper products.

Opportunities:

- Development of New Applications: Ongoing research and development are leading to new applications for micro flute paper, such as in the pharmaceutical, cosmetic, and electronics industries.

- Innovation in Manufacturing Processes: Advancements in manufacturing technologies are improving the quality and performance of micro flute paper, while also reducing production costs and environmental impact.

- Growing Demand for Premium Packaging: Micro flute paper can be used to create high-quality, visually appealing packaging that enhances the perceived value of products, particularly in the luxury goods and consumer electronics sectors.

- Expansion in Emerging Markets: The demand for micro flute paper is expected to grow in developing countries due to rising disposable incomes, increasing urbanization, and the expansion of e-commerce.

Challenges:

- Maintaining Quality and Consistency: Ensuring consistent quality and performance of micro flute paper can be challenging due to variations in raw materials and manufacturing processes.

- Meeting Stringent Environmental Regulations: The packaging industry is subject to increasingly stringent environmental regulations regarding recyclability, waste reduction, and the use of sustainable materials. Micro flute paper manufacturers need to comply with these regulations.

- Managing Supply Chain Disruptions: Global supply chain disruptions, such as those caused by the COVID-19 pandemic, can impact the availability and cost of raw materials and finished products.

- Addressing Consumer Perceptions: Some consumers may not be familiar with the benefits of micro flute paper, and there may be a perception that it is less durable or protective than other packaging materials. Manufacturers need to educate consumers about the advantages of micro flute paper.

Micro Flute Paper Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Micro Flute Paper Market |

| Market Size in 2023 | USD 2.64 Billion |

| Market Forecast in 2032 | USD 4.28 Billion |

| Growth Rate | CAGR of 5.5% |

| Number of Pages | 140 |

| Key Companies Covered | Smurfit Kappa Group, Van Genechten Packaging, Stora Enso Oyj, Netpak Packaging Inc, WestRock Company, Novolex Holdings, DS Smith Plc, Mayr-Melnhof Packaging International GmbH, Cascades Sonoco, Mondi Group, Shanghai DE Printed Box, International Paper Company, Nine Dragons Paper (Holdings) Limited, Georgia-Pacific LLC, Oji Holdings Corporation, Lee & Man Paper Manufacturing Ltd., Nippon Paper Industries Co. Ltd., Shandong Bohui Paper Industry Co. Ltd., Vinda International Holdings Limited, Shenzhen YUTO Packaging Technology Co. Ltd., Rengo Co. Ltd., Grigeo AB, Honeywell International Inc, Sonoco Products Company, Dingxin Group Co. Ltd., Prowell Paper LLC, Guangzhou Huatian Paper Co. Ltd., Horizon Pulp & Paper Ltd., Cheng Loong Corp., Evergreen Packaging Inc., Kishu Paper Co. Ltd., Cartiere del Garda S.p.A., Visy Industries |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Micro Flute Paper Market: Segmentation Insights

The global micro flute paper market is divided by flute type, end-use, and region.

Segmentation Insights by Flute Type

Based on flute type, the global micro flute paper market is divided into A-Flute, B-Flute, C-Flute, E-Flute, F-Flute, and Others.

E-Flute is the most dominant segment due to its versatility and widespread use in various industries. E-Flute is characterized by its thin profile, high compression strength, and excellent printability, making it ideal for retail packaging, cosmetics, and consumer electronics. Its lightweight nature reduces shipping costs while maintaining durability, which aligns with the growing demand for sustainable and cost-effective packaging solutions. The segment’s dominance is further reinforced by its suitability for high-quality graphics, which is crucial for branding and marketing in competitive markets.

Following E-Flute, B-Flute holds a significant share in the market. B-Flute is known for its balanced strength and cushioning properties, making it a preferred choice for packaging applications requiring moderate protection, such as canned goods, furniture, and automotive parts. Its thicker profile compared to E-Flute provides better resistance to crushing, making it suitable for heavier products. The segment’s popularity is also driven by its ability to withstand stacking and handling during transportation, ensuring product safety.

C-Flute is another important segment, widely used in industrial and shipping applications. It offers excellent stacking strength and durability, making it ideal for corrugated boxes used in transporting heavy or bulky items. C-Flute’s thicker profile provides superior protection against impacts, which is essential for long-distance shipping and storage. While it is less dominant than E-Flute and B-Flute, its role in the logistics and manufacturing sectors ensures steady demand.

A-Flute, with its thickest profile among the standard flute types, is primarily used for heavy-duty packaging applications. It provides exceptional cushioning and stacking strength, making it suitable for fragile or high-value items like glassware and machinery. However, its bulkier nature and higher material costs limit its dominance in the market, as industries increasingly prioritize lightweight and eco-friendly solutions.

F-Flute is a niche segment, known for its ultra-thin profile and superior printability. It is commonly used for high-end retail packaging, such as luxury goods and cosmetics, where aesthetics and compactness are critical. While F-Flute offers excellent surface smoothness for printing, its limited strength and higher production costs restrict its widespread adoption compared to other flute types.

Segmentation Insights by End-use

On the basis of end-use, the global micro flute paper market is bifurcated into food & beverage, personal care & cosmetics, industrial, and others.

The Food & Beverage segment is the most dominant, driven by the increasing demand for sustainable and lightweight packaging solutions. Micro flute paper is widely used in packaging for fresh produce, frozen foods, beverages, and ready-to-eat meals due to its excellent strength-to-weight ratio, moisture resistance, and ability to maintain product freshness. The growing emphasis on eco-friendly packaging in the food industry, coupled with stringent regulations on food safety, has further propelled the adoption of micro flute paper. Its ability to be easily printed on also makes it ideal for branding and labeling, which is crucial in the competitive food and beverage sector.

The Personal Care & Cosmetics segment is another significant contributor to the micro flute paper market. This segment benefits from the material’s lightweight, durable, and aesthetically pleasing properties, which are essential for packaging luxury and high-end products. Micro flute paper is commonly used for packaging items such as skincare products, perfumes, and makeup, where visual appeal and product protection are paramount. The increasing consumer preference for sustainable and recyclable packaging in the beauty industry has further boosted the demand for micro flute paper in this segment. Additionally, its ability to support high-quality printing enhances brand visibility and consumer engagement.

The Industrial segment also plays a vital role in the micro flute paper market, particularly in packaging applications that require durability and protection. Industries such as automotive, electronics, and machinery rely on micro flute paper for shipping and storage solutions due to its excellent cushioning and stacking strength. The material’s ability to withstand harsh handling and environmental conditions makes it ideal for protecting heavy or fragile industrial goods. While this segment is not as dominant as Food & Beverage or Personal Care & Cosmetics, it remains a critical area of application, especially in regions with strong manufacturing and export activities.

micro flute paper Market: Regional Insights

- Asia-Pacific is expected to dominates the global market

The micro flute paper market exhibits significant regional variation, with Asia-Pacific emerging as the most dominant region. This dominance is driven by rapid industrialization, expanding e-commerce sectors, and increasing demand for sustainable packaging solutions. Countries like China and India are at the forefront, leveraging their large manufacturing bases and growing consumer markets. The region benefits from cost-effective production capabilities and a strong focus on eco-friendly packaging materials, which align with global trends. Additionally, government initiatives promoting sustainable practices further bolster the market, making Asia-Pacific the largest and fastest-growing region for micro flute paper.

North America follows as the second-largest market, characterized by advanced packaging technologies and high consumer awareness regarding sustainable packaging. The United States is the key contributor, with its well-established e-commerce industry and stringent regulations favoring recyclable materials. The region’s emphasis on reducing carbon footprints and adopting innovative packaging solutions has significantly driven the demand for micro flute paper. Furthermore, the presence of major players in the packaging industry and a robust logistics network support the market’s growth, making North America a critical hub for micro flute paper applications.

Europe holds a substantial share in the micro flute paper market, driven by stringent environmental regulations and a strong emphasis on circular economy principles. Countries like Germany, France, and the UK are leading the adoption of sustainable packaging materials, including micro flute paper, to meet EU directives on waste reduction and recycling. The region’s well-developed retail and e-commerce sectors further contribute to the demand for lightweight and durable packaging solutions. Europe’s focus on reducing plastic usage and promoting biodegradable materials has positioned it as a key market for micro flute paper, with steady growth expected in the coming years.

Latin America represents a growing market for micro flute paper, fueled by increasing industrialization and rising consumer awareness about sustainable packaging. Brazil and Mexico are the primary contributors, driven by their expanding e-commerce and retail sectors. While the market is still developing compared to other regions, the growing emphasis on eco-friendly packaging and improving economic conditions are expected to accelerate demand. However, challenges such as limited infrastructure and lower adoption rates of advanced packaging technologies may hinder growth in the short term, but the region holds significant potential for future expansion.

The Middle East and Africa region, while currently the smallest market for micro flute paper, is gradually gaining traction due to increasing urbanization and a growing focus on sustainable development. South Africa and the UAE are leading the adoption of eco-friendly packaging solutions, supported by government initiatives and rising consumer awareness. The region’s developing e-commerce sector and improving industrial capabilities are expected to drive demand for micro flute paper in the coming years. However, the market faces challenges such as limited infrastructure and lower awareness levels, which may slow growth compared to other regions. Despite these hurdles, the Middle East and Africa present untapped opportunities for market players willing to invest in the region.

Micro Flute Paper Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the micro flute paper market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global micro flute paper market include:

- Novolex Holdings

- DS Smith Plc

- Olmuksan International Paper

- Stora Enso

- WestRock Paper Llc

- Van Genechten Packaging

- Mondi Group

- Smurfit Kappa

- Netpak

- Hamburger Containerboard

- Acme Corrugated Box Co. Inc.

- MM Group

The global micro flute paper market is segmented as follows:

By Flute Type

- A-Flute

- B-Flute

- C-Flute

- E-Flute

- F-Flute

- Others

By End-use

- Food & Beverage

- Personal Care & Cosmetics

- Industrial

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global micro flute paper market size was projected at approximately US$ 2.64 billion in 2023. Projections indicate that the market is expected to reach around US$ 4.28 billion in revenue by 2032.

The global micro flute paper market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 5.5% during the forecast period from 2024 to 2032.

Asia-Pacific is expected to dominate the global micro flute paper market.

The global micro flute paper market is driven by the increasing demand for sustainable and eco-friendly packaging solutions, growth in e-commerce and retail sectors, and stringent regulations promoting recyclable materials. Additionally, its lightweight, durable, and cost-effective properties make it ideal for diverse applications across industries like food & beverage, personal care, and industrial packaging.

Some of the prominent players operating in the global micro flute paper market are; Novolex Holdings, DS Smith Plc, Olmuksan International Paper, Stora Enso, WestRock Paper Llc, Van Genechten Packaging, Mondi Group, Smurfit Kappa, Netpak, Hamburger Containerboard, Acme Corrugated Box Co. Inc., MM Group, and others.

Table Of Content

Inquiry For Buying

Micro Flute Paper

Request Sample

Micro Flute Paper