Natural Refrigerants Market Size, Share, and Trends Analysis Report

CAGR :

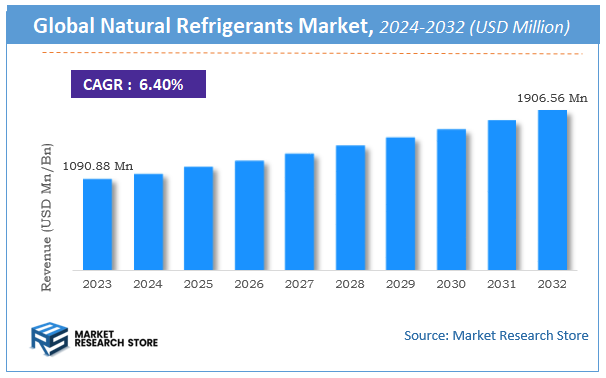

| Market Size 2023 (Base Year) | USD 1090.88 Million |

| Market Size 2032 (Forecast Year) | USD 1906.56 Million |

| CAGR | 6.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Natural Refrigerants Market Insights

According to Market Research Store, the global natural refrigerants market size was valued at around USD 1090.88 million in 2023 and is estimated to reach USD 1906.56 million by 2032, to register a CAGR of approximately 6.4% in terms of revenue during the forecast period 2024-2032.

The natural refrigerants report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Natural Refrigerants Market: Overview

Natural refrigerants are environmentally friendly substances used in cooling and refrigeration systems that occur naturally in the environment. These include carbon dioxide (CO₂), ammonia (NH₃), hydrocarbons such as propane (R-290) and isobutane (R-600a), water (H₂O), and air. Unlike many synthetic refrigerants, particularly hydrofluorocarbons (HFCs), natural refrigerants have minimal or zero ozone depletion potential (ODP) and very low global warming potential (GWP), making them a sustainable alternative for refrigeration and air conditioning applications.

The growth of the natural refrigerants market is driven by tightening environmental regulations, rising global emphasis on climate change mitigation, and growing demand for energy-efficient cooling systems. Governments and industries are phasing down high-GWP refrigerants under agreements like the Kigali Amendment to the Montreal Protocol, prompting the transition to greener alternatives. Natural refrigerants are increasingly used in commercial refrigeration, industrial cooling, residential heat pumps, and automotive air conditioning systems. Technological advancements in system design and safety have also improved the viability of these refrigerants, particularly for managing the flammability or toxicity of some types. As the cooling sector strives for sustainability, natural refrigerants are becoming central to achieving low-carbon and eco-friendly refrigeration solutions.

Key Highlights

- The natural refrigerants market is anticipated to grow at a CAGR of 6.4% during the forecast period.

- The global natural refrigerants market was estimated to be worth approximately USD 1090.88 million in 2023 and is projected to reach a value of USD 1906.56 million by 2032.

- The growth of the natural refrigerants market is being driven by increasing global emphasis on environmental sustainability, climate regulations, and the phase-out of synthetic refrigerants with high global warming potential (GWP) and ozone depletion potential (ODP).

- Based on the type, the carbon dioxide segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the refrigeration segment is projected to swipe the largest market share.

- In terms of end use, the residential segment is expected to dominate the market.

- Based on the system type, the single stage segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Natural Refrigerants Market: Dynamics

Key Growth Drivers:

- Stringent Environmental Regulations and Phase-Down of Synthetic Refrigerants: This is the most significant driver. International agreements like the Kigali Amendment to the Montreal Protocol and regional regulations (e.g., EU F-Gas Regulation) are mandating the phase-down of high-GWP hydrofluorocarbons (HFCs) and hydrochlorofluorocarbons (HCFCs). This forces industries to transition to environmentally friendly alternatives, with natural refrigerants being the leading solution.

- Growing Environmental Consciousness and Sustainability Initiatives: Increasing awareness among consumers and businesses about climate change and the environmental impact of traditional refrigerants is driving the demand for greener cooling solutions. Companies are actively seeking natural refrigerants to reduce their carbon footprint, achieve sustainability targets, and enhance their brand image.

- Enhanced Energy Efficiency and Lower Operational Costs: Many natural refrigerants, particularly ammonia and CO2 in specific system designs, offer superior thermodynamic properties, leading to higher energy efficiency compared to synthetic counterparts. This translates into lower electricity consumption and reduced operational costs for refrigeration and air conditioning systems, providing a strong economic incentive for adoption.

Restraints:

- High Initial Investment and Installation Costs: While offering long-term operational savings, the upfront capital expenditure for installing natural refrigerant-based systems can be significantly higher than traditional synthetic systems. This is due to the need for specialized equipment, stronger components (especially for CO2 systems' high pressure), and potentially more complex installation procedures.

- Safety Concerns (Toxicity and Flammability): Some natural refrigerants, such as ammonia (toxic) and hydrocarbons (flammable), pose inherent safety risks. This necessitates stringent safety protocols, specialized system designs, enhanced leak detection, and specific ventilation requirements, which can increase the complexity and cost of installation and operation, particularly for smaller installations or in populated areas.

Opportunities:

- Growth in Emerging Markets and Developing Economies: As developing economies experience rapid urbanization, industrialization, and rising living standards, the demand for refrigeration and air conditioning is surging. These regions have an opportunity to "leapfrog" older synthetic technologies and directly adopt natural refrigerant solutions, particularly with increasing environmental awareness and potential future regulations.

- Expansion into Residential and Small Commercial Applications: While traditionally dominant in industrial refrigeration, there's a growing opportunity for natural refrigerants (especially hydrocarbons like propane/isobutane and smaller CO2 systems) in domestic refrigerators, small commercial display cases, and residential air conditioning units. Innovations are making these applications safer and more efficient.

Challenges:

- Overcoming Perceived Safety Risks and Regulatory Hurdles: Despite advancements, the perception of high safety risks associated with ammonia and flammability of hydrocarbons remains a hurdle. Overcoming this requires continuous education, robust safety standards, and clear regulatory guidelines that build confidence among end-users and ensure safe operation.

- Standardization and Harmonization of Regulations Globally: The lack of fully harmonized standards and regulations for natural refrigerants across different countries can create complexities for global manufacturers and users. Achieving greater standardization can streamline adoption, reduce compliance costs, and facilitate market expansion.

Natural Refrigerants Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Natural Refrigerants Market |

| Market Size in 2023 | USD 1090.88 Million |

| Market Forecast in 2032 | USD 1906.56 Million |

| Growth Rate | CAGR of 6.4% |

| Number of Pages | 140 |

| Key Companies Covered | The Linde Group, Airgas Inc., Engas Australasia, Sinochem Group, Tazzetti S.P.A., Harp International Ltd., Shandong Yueon Chemical Industry Ltd., Puyang Zhongwei Fine Chemical Co. Ltd., Hychill Australia Pvt. Ltd., A-Gas International, A.S. Trust and Holdings and GTS S.P.A. |

| Segments Covered | By Product, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Natural Refrigerants Market: Segmentation Insights

The global natural refrigerants market is divided by type, application, end use, system type, and region.

Based on type, the global natural refrigerants market is divided into carbon dioxide, ammonia, hydrocarbons, water, and air. Carbon Dioxide (CO₂) dominates the Natural Refrigerants Market owing to its non-toxic, non-flammable nature and zero ozone depletion potential (ODP). Also known as R-744, carbon dioxide is widely used in commercial refrigeration, heat pumps, and transport refrigeration systems. It operates efficiently in transcritical and subcritical systems and is particularly favored in supermarkets and cold storage applications due to its high volumetric cooling capacity and low environmental impact. Regulatory restrictions on hydrofluorocarbons (HFCs) and the push toward climate-friendly solutions are accelerating the adoption of CO₂-based systems across Europe, North America, and parts of Asia, reinforcing its leadership position in the market.

On the basis of application, the global natural refrigerants market is bifurcated into refrigeration, air conditioning, heat pumps, chillers, and commercial cold storage. Refrigeration dominates the Natural Refrigerants Market, driven by increasing environmental regulations and the phasing out of synthetic refrigerants such as HFCs and HCFCs. Natural refrigerants like carbon dioxide, ammonia, and hydrocarbons are widely used in commercial and industrial refrigeration systems including supermarket refrigeration, food processing, cold chain logistics, and transport refrigeration. CO₂ is particularly popular in transcritical systems for retail cooling, while ammonia is preferred for large-scale cold storage and industrial applications due to its high efficiency and zero global warming potential (GWP). Hydrocarbons, such as isobutane and propane, are increasingly used in domestic and small commercial refrigeration systems. The growing emphasis on energy efficiency and climate-friendly technologies continues to support the strong demand for natural refrigerants in the refrigeration segment.

In terms of end-users, the global natural refrigerants market is bifurcated into residential, commercial, industrial, and transportation. Residential end use dominates the Natural Refrigerants Market in terms of volume, particularly due to the widespread adoption of hydrocarbon-based refrigerants in domestic refrigerators, freezers, and small air-conditioning units. Refrigerants like isobutane (R-600a) and propane (R-290) are increasingly used in household cooling appliances due to their excellent energy efficiency, low global warming potential (GWP), and cost-effectiveness. These refrigerants are also gaining popularity in residential heat pump water heaters, especially in Europe and East Asia, where regulatory policies and energy efficiency standards encourage the use of environmentally friendly alternatives. As energy-efficient housing becomes a priority globally, the residential sector continues to lead in the implementation of natural refrigerants.

On the basis of system type, the global natural refrigerants market is bifurcated into single stage, cascade, and transcritical. Single Stage systems dominate the Natural Refrigerants Market due to their relatively simple design, cost-effectiveness, and suitability for a wide range of small- to medium-capacity applications. These systems operate using a single compression stage and are typically employed in residential, light commercial, and standalone refrigeration and air-conditioning units. Hydrocarbons such as propane (R-290) and isobutane (R-600a) are commonly used in single-stage systems due to their high energy efficiency and compatibility with low charge limits. This configuration is especially prevalent in domestic refrigerators, vending machines, and small-scale cooling applications where performance requirements are moderate, and ease of maintenance is crucial. The widespread availability and ease of integration of single-stage systems support their leading position in the market.

Natural Refrigerants Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the natural refrigerants market, propelled by evolving regulatory frameworks, increasing adoption of low-global warming potential (GWP) solutions, and strong industrial and commercial refrigeration demand. The United States leads usage, driven by efforts to phase down hydrofluorocarbons (HFCs) under the AIM Act and strong backing from state-level programs promoting eco-friendly refrigerants. Carbon dioxide (CO₂), ammonia (NH₃), and hydrocarbons (such as propane and isobutane) are widely used in supermarkets, cold chain logistics, and industrial refrigeration systems. CO₂ transcritical systems are gaining rapid adoption in retail refrigeration, while ammonia remains a key refrigerant in food processing and storage due to its high efficiency and cost-effectiveness. Canada is advancing in parallel with green building codes and sustainability targets that promote the use of natural refrigerants in HVAC and commercial cooling applications. Leading system instegrators and refrigerant manufacturers are focusing heavily on safety systems and technology enhancements to expand adoption across more sectors.

Asia-Pacific is the fastest-growing region in the natural refrigerants market, fueled by rising demand for cold storage, supermarket chains, and industrial refrigeration in rapidly urbanizing economies. China and Japan are the largest markets, with growing regulatory support and strong manufacturing capabilities. China is increasing its adoption of CO₂ and hydrocarbon refrigerants in retail and cold chain sectors, encouraged by energy efficiency policies and the Kigali Amendment. Japan leads in natural refrigerant technologies with wide deployment of CO₂ heat pumps and hydrocarbon-based systems in household appliances and vending machines. India is showing progress through pilot projects and government-backed efforts to curb HFC emissions, especially in cold chains and food preservation. Southeast Asia is an emerging adopter, with Thailand and Indonesia exploring natural refrigerants in commercial refrigeration. However, safety concerns and limited technician training still pose challenges across several countries in the region.

Natural Refrigerants Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the natural refrigerants market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global natural refrigerants market include:

- Johnson Controls

- Refrigerants Australia

- Frascold

- Daikin

- Carrier

- Bosch

- EarthCare

- SABIC

- Honeywell

- AGas

- LG Electronics

- Safegas

- BASF

- Emerson Electric

- Chemours

- The Linde Group

- Airgas Inc.

- Engas Australasia

- Sinochem Group

- Tazzetti S.P.A.

- Harp International Ltd.

- Shandong Yueon Chemical Industry Ltd.

- Puyang Zhongwei Fine Chemical Co. Ltd.

- Hychill Australia Pvt. Ltd.

- A-Gas International

- A.S. Trust

- Holdings

- GTS S.P.A

The global natural refrigerants market is segmented as follows:

By Type

- Carbon Dioxide

- Ammonia

- Hydrocarbons

- Water

- Air

By Application

- Refrigeration

- Air Conditioning

- Heat Pumps

- Chillers

- Commercial Cold Storage

By End Use

- Residential

- Commercial

- Industrial

- Transportation

By System Type

- Single Stage

- Cascade

- Transcritical

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global market revenue, 2014 - 2020 (USD Million)

- 2.2. Global natural refrigerants market: Snapshot

- Chapter 3. Natural Refrigerants Market – Global and Industry Analysis

- 3.1. Natural refrigerants: Market dynamics

- 3.2. Value chain analysis

- 3.3. Market drivers

- 3.3.1. Drivers of global natural refrigerants market: Impact analysis

- 3.3.2. National Regulations

- 3.3.3. Rising demand for refrigeration and air-conditioning application

- 3.4. Market restraints

- 3.4.1. Restraints of global natural refrigerants market: Impact analysis

- 3.4.2. Requires very large compressors to used as the sole refrigerant

- 3.5. Opportunities

- 3.5.1. Increasing awareness about global warming

- 3.6. Porter’s five forces analysis

- 3.7. Market Attractiveness Analysis

- 3.7.1. Market attractiveness analysis by product segment

- 3.7.2. Market attractiveness analysis by application segment

- 3.7.3. Market attractiveness analysis by regional segment

- Chapter 4. Global Natural Refrigerants Market - Competitive Landscape

- 4.1. Company market share, 2014

- 4.2. Production capacity (subject to data availability)

- 4.3. Raw material analysis

- 4.4. Price trend analysis

- Chapter 5. Global Natural Refrigerants Market – Product Segment Analysis

- 5.1. Global natural refrigerants market: Product overview

- 5.1.1. Global natural refrigerants market share, by product, 2014 - 2020

- 5.2. Ammonia

- 5.2.1. Global ammonia market, 2014 – 2020 (USD Million)

- 5.3. Carbon dioxide

- 5.3.1. Global carbon dioxide market, 2014 – 2020 (USD Million)

- 5.4. Hydrocarbons

- 5.4.1. Global hydrocarbons market, 2014 – 2020 (USD Million)

- 5.5. Others

- 5.5.1. Global other natural refrigerants market, 2014 – 2020 (USD Million)

- 5.1. Global natural refrigerants market: Product overview

- Chapter 6. Global Natural Refrigerants Market – Application Segment Analysis

- 6.1. Global natural refrigerants market: Application overview

- 6.1.1. Global natural refrigerants market share by application, 2014 - 2020

- 6.2. Industrial

- 6.2.1. Global natural refrigerants market for industrial refrigeration, 2014 – 2020 (USD Million)

- 6.3. Commercial

- 6.3.1. Global natural refrigerants market for commercial refrigeration, 2014 – 2020 (USD Million)

- 6.4. Domestic

- 6.4.1. Global natural refrigerants market for domestic refrigeration, 2014 – 2020 (USD Million)

- 6.5. Stationary Air Conditioning

- 6.5.1. Global natural refrigerants market for stationary air conditioning, 2014 – 2020 (USD Million)

- 6.6. Others

- 6.6.1. Global natural refrigerants market for other applications, 2014 – 2020 (USD Million)

- 6.1. Global natural refrigerants market: Application overview

- Chapter 7. Global Natural Refrigerants Market – Regional Segment Analysis

- 7.1. Global natural refrigerants market: Regional overview

- 7.1.1. Global natural refrigerants market share by region, 2014 - 2020

- 7.2. North America

- 7.2.1. North America natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.2.2. North America natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.2.3. U.S.

- 7.2.3.1. U.S. natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.2.3.2. U.S. natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.3. Europe

- 7.3.1. Europe natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.2. Europe natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.3.3. Germany

- 7.3.3.1. Germany natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.3.2. Germany natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.3.4. France

- 7.3.4.1. France natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.4.2. France natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.3.5. UK

- 7.3.5.1. UK natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.5.2. UK natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.2. Asia Pacific natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.4.3. China

- 7.4.3.1. China natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.3.2. China natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.4.4. Japan

- 7.4.4.1. Japan natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.4.2. Japan natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.4.5. India

- 7.4.5.1. India natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.5.2. India natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.5. Latin America

- 7.5.1. Latin America natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.2. Latin America natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.5.3. Brazil

- 7.5.3.1. Brazil natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.3.2. Brazil natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.6. Middle East and Africa

- 7.6.1. Middle East and Africa natural refrigerants market revenue, by product, 2014 – 2020 (USD Million)

- 7.6.2. Middle East and Africa natural refrigerants market revenue, by application, 2014 – 2020 (USD Million)

- 7.1. Global natural refrigerants market: Regional overview

- Chapter 8. Company Profile

- 8.1. The Linde Group

- 8.1.1. Overview

- 8.1.2. Financials

- 8.1.3. Product portfolio

- 8.1.4. Business strategy

- 8.1.5. Recent developments

- 8.2. Airgas Inc.

- 8.2.1. Overview

- 8.2.2. Financials

- 8.2.3. Product portfolio

- 8.2.4. Business strategy

- 8.2.5. Recent developments

- 8.3. Engas Australasia

- 8.3.1. Overview

- 8.3.2. Financials

- 8.3.3. Product portfolio

- 8.3.4. Business strategy

- 8.3.5. Recent developments

- 8.4. Sinochem Group

- 8.4.1. Overview

- 8.4.2. Financials

- 8.4.3. Product portfolio

- 8.4.4. Business strategy

- 8.4.5. Recent developments

- 8.5. Tazzetti S.P.A.

- 8.5.1. Overview

- 8.5.2. Financials

- 8.5.3. Product portfolio

- 8.5.4. Business strategy

- 8.5.5. Recent developments

- 8.6. Harp International Ltd.

- 8.6.1. Overview

- 8.6.2. Financials

- 8.6.3. Product portfolio

- 8.6.4. Business strategy

- 8.6.5. Recent developments

- 8.7. Shandong Yueon Chemical Industry Ltd.

- 8.7.1. Overview

- 8.7.2. Financials

- 8.7.3. Product portfolio

- 8.7.4. Business strategy

- 8.7.5. Recent developments

- 8.8. Puyang Zhongwei Fine Chemical Co. Ltd.

- 8.8.1. Overview

- 8.8.2. Financials

- 8.8.3. Product portfolio

- 8.8.4. Business strategy

- 8.8.5. Recent developments

- 8.9. Hychill Australia Pvt. Ltd.

- 8.9.1. Overview

- 8.9.2. Financials

- 8.9.3. Product portfolio

- 8.9.4. Business strategy

- 8.9.5. Recent developments

- 8.10. A-Gas International

- 8.10.1. Overview

- 8.10.2. Financials

- 8.10.3. Product portfolio

- 8.10.4. Business strategy

- 8.10.5. Recent developments

- 8.11. A.S. Trust and Holdings

- 8.11.1. Overview

- 8.11.2. Financials

- 8.11.3. Product portfolio

- 8.11.4. Business strategy

- 8.11.5. Recent developments

- 8.12. GTS S.P.A

- 8.12.1. Overview

- 8.12.2. Financials

- 8.12.3. Product portfolio

- 8.12.4. Business strategy

- 8.12.5. Recent developments

- 8.1. The Linde Group

Inquiry For Buying

Natural Refrigerants

Request Sample

Natural Refrigerants