On the Go Packaging Market Size, Share, and Trends Analysis Report

CAGR :

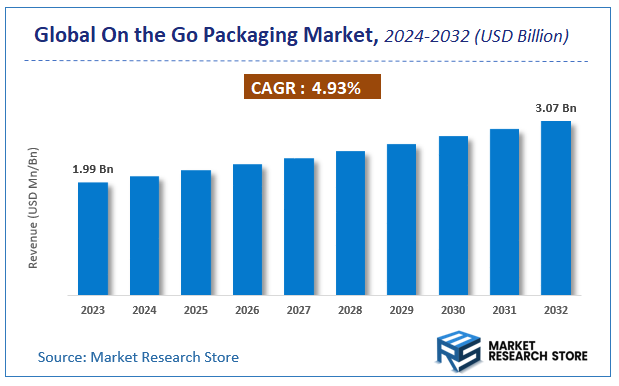

| Market Size 2023 (Base Year) | USD 1.99 Billion |

| Market Size 2032 (Forecast Year) | USD 3.07 Billion |

| CAGR | 4.93% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

On the Go Packaging Market Insights

According to Market Research Store, the global on the go packaging market size was valued at around USD 1.99 billion in 2023 and is estimated to reach USD 3.07 billion by 2032, to register a CAGR of approximately 4.93% in terms of revenue during the forecast period 2024-2032.

The on the go packaging report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global On the Go Packaging Market: Overview

On-the-go packaging refers to convenient, portable, and easy-to-use packaging solutions designed to cater to modern consumers’ busy lifestyles. It is widely used in food and beverage products such as ready-to-eat meals, snacks, and drinks, as well as in takeaway and food delivery services. The packaging is typically lightweight, secure, and designed for single servings, making it suitable for consumption while commuting, traveling, or working. Common formats include pouches, bags, bottles, cups, and trays, often made from plastics, paper, or hybrid materials, with growing adoption of eco-friendly and biodegradable alternatives in response to sustainability concerns.

Key Highlights

- The on the go packaging market is anticipated to grow at a CAGR of 4.93% during the forecast period.

- The global on the go packaging market was estimated to be worth approximately USD 1.99 billion in 2023 and is projected to reach a value of USD 3.07 billion by 2032.

- The growth of the on the go packaging market is being driven by rising disposable incomes, and the expanding food delivery and quick-service restaurant sectors.

- Based on the flexible packaging, the zip pouches segment is growing at a high rate and is projected to dominate the market.

- On the basis of paperboard packaging, the folding cartons segment is projected to swipe the largest market share.

- In terms of end user, the food and beverage segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

On the Go Packaging Market: Dynamics

Key Growth Drivers

- Convenience & lifestyle shift – Rising demand for single-serve and ready-to-eat/ready-to-drink products as urban, time-pressed consumers prefer portable packaging.

- E-commerce and food delivery growth – Rapid expansion of takeaway/delivery and online shopping increases need for durable, tamper-proof on-the-go formats.

- Product innovation (lightweight & barrier materials) – Improvements in films, laminates and insulated formats enable safer, longer-lasting portable packs.

- Brand marketing & portion control – Single-serve packs support portion control, create new consumption occasions, and allow premium positioning.

Restraints

- Sustainability regulation & consumer pressure – Bans and taxes on single-use plastics, along with consumer demand for eco-friendly solutions, restrict conventional formats.

- Raw-material price volatility – Fluctuating costs of polymers, aluminium and paper impact margins and pricing strategies.

- Food-safety and labelling compliance – Stringent rules on safety, traceability, and labeling increase costs for manufacturers.

Opportunities

- Sustainable-material substitutes – Rising interest in recyclable, compostable, and mono-material packaging creates growth opportunities.

- Closed-loop & reusable systems – Deposit-return and reusable packaging initiatives open new business models.

- Smart / functional packaging – Features like freshness indicators, tamper evidence, and QR traceability enhance value.

- Emerging markets & urbanization – Growing disposable incomes and fast-paced lifestyles in developing regions expand demand.

Challenges

- Balancing functionality with recyclability – Multi-layer packs deliver strong performance but hinder recyclability, while mono-materials may reduce efficiency or raise costs.

- Regulatory & health concerns – Scrutiny of certain chemicals in plastics forces reformulation and limits material choices.

- Consumer perception & activism – Growing environmental activism and retailer commitments against single-use packaging shift market demand.

- Scale & cost of new packaging systems – Transitioning to recyclable or reusable solutions requires significant investment in infrastructure and supply chains.

On the Go Packaging Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | On the Go Packaging Market |

| Market Size in 2023 | USD 1.99 Billion |

| Market Forecast in 2032 | USD 3.07 Billion |

| Growth Rate | CAGR of 4.93% |

| Number of Pages | 155 |

| Key Companies Covered | American Packaging, Bemis, Berry Plastics, Amcor, Berry Plastics, Bryce, Coveris, Hood Packaging, InterFlex, Huhtamaki, Mondi, Printpack, 0020Oracle Packaging, Novolex, Pregis, Sealed Air, Proampac, Scholle IPN, Sonoco Products, Sigma Plastics, Winpak, and WestRock among others |

| Segments Covered | By Flexible Packaging, By Paperboard Packaging, By End User, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

On the Go Packaging Market: Segmentation Insights

The global on the go packaging market is divided by flexible packaging, paperboard packaging, end user, and region.

Based on flexible packaging, the global on the go packaging market is divided into clamshells, peel off lids, plastic trays, and zip pouches. Among flexible packaging types, zip pouches dominate the on-the-go packaging market as they offer the highest convenience, portability, and versatility across a wide range of products such as snacks, beverages, ready-to-eat meals, and even non-food items. Their lightweight structure, resealable functionality, and ability to preserve freshness make them highly preferred for modern consumers who prioritize convenience and portion control. Moreover, advancements in materials and barrier technologies have further strengthened their role, enabling longer shelf life and better protection during transportation, which has solidified their position as the leading segment. Plastic trays follow as another significant segment, especially in ready-to-eat meals, bakery products, fresh produce, and meat packaging. Their rigid structure provides stability and protection, making them suitable for products that require safe handling and presentation. They are widely used in supermarkets, convenience stores, and food delivery services, though their bulkier nature compared to pouches makes them less convenient for portability.

On the basis of paperboard packaging, the global on the go packaging market is bifurcated into corrugated boxes, folding cartons, and rigid boxes. Folding cartons are the most dominant segment in paperboard packaging for the on-the-go packaging market due to their versatility, lightweight structure, and cost-effectiveness. They are extensively used for snacks, confectionery, beverages, and fast-food items, offering excellent printability for branding and product information. Their ease of customization, recyclability, and ability to support both single-serve and multi-pack formats make them the go-to choice for foodservice providers and retailers targeting convenience-driven consumers. Sustainability trends have further boosted folding cartons as they are easily recyclable and align with eco-friendly packaging initiatives. Corrugated boxes hold the second-largest share, primarily used in secondary or tertiary packaging for transporting on-the-go products safely through supply chains. Their durability, cushioning, and protective qualities make them ideal for e-commerce, bulk food delivery, and takeaway services, ensuring products remain intact during handling and shipping. While they are not directly consumed as primary packaging by end users, corrugated boxes play a critical role in logistics and distribution, making them indispensable to the overall market despite less visibility at the consumer level.

Based on end user, the global on the go packaging market is divided into food and beverage, healthcare, hygiene products, personal care industries, and pharmaceuticals. Food and beverage is the most dominant end-user segment in the on-the-go packaging market, driven by the rapid rise in demand for ready-to-eat meals, snacks, beverages, and convenience foods. Consumers’ busy lifestyles, coupled with the expansion of quick-service restaurants, cafes, and food delivery platforms, have positioned this segment at the forefront. Packaging formats like zip pouches, plastic trays, folding cartons, and beverage cups are extensively used here, offering portability, freshness retention, and ease of disposal. With growing emphasis on sustainability, brands are also incorporating recyclable and biodegradable materials, further reinforcing the segment’s leadership. Personal care industries follow, benefiting from the increasing consumer demand for travel-friendly and single-use packaging for products like shampoos, lotions, sanitizers, and cosmetics. Compact sachets, pouches, and small cartons dominate this space, allowing convenience and portability for on-the-go usage. Innovation in design and branding has also made packaging a key tool for differentiation in this segment.

On the Go Packaging Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific leads the on-the-go packaging landscape, propelled by rapid urbanization, rising disposable incomes, booming quick-service and delivery platforms, and strong demand for convenient ready-to-eat and ready-to-drink formats. Manufacturers in the region are aggressively adopting flexible formats like pouches and lightweight multi-layer films, while also investing in barrier technologies and biodegradable alternatives to balance shelf life with sustainability pressures. Growth is broad-based across East and Southeast Asia where changing lifestyles and expanding retail and e-commerce ecosystems create high volume demand, but the region also faces challenges around waste management infrastructure and regulatory shifts toward plastic reduction.

North America is a mature and high-value market characterized by strong consumption of single-serve and convenience formats driven by established on-the-go eating habits, widespread food service and delivery networks, and active innovation in materials and closures that improve portability and reseal ability. Brands and converters in this region focus heavily on performance preserving freshness and ensuring transport durability while regulators and consumers push for recyclable and compostable options, creating a dual pressure to maintain convenience while improving environmental credentials. The United States is the primary demand center, supported by large retail chains and a sophisticated supply chain ecosystem.

Europe sits between mature consumption and strong regulatory momentum toward sustainability, with demand concentrated in urban centers and driven by on-the-go lifestyles, coffee-to-go culture, and extensive ready-meal consumption. European players emphasize recyclable and mono-material solutions, strict compliance with circularity targets, and packaging designs that meet stringent labeling and composability standards; innovation here often leads global sustainability practices, but higher material and compliance costs can slow adoption of certain formats in price-sensitive segments.

Latin America represents a smaller but steadily expanding market where urbanization and growth in food delivery and modern retail channels are accelerating demand for convenient, portable packaging formats. Growth is concentrated in larger economies with expanding quick-service restaurant and packaged snack sectors, but progress is uneven due to variability in logistics, recycling infrastructure, and the cost sensitivity of many consumers; nonetheless, regional manufacturers and international suppliers are increasingly introducing flexible, lower-cost on-the-go solutions to capture rising consumption.

Middle East & Africa is the least dominated but shows niche strengths demand driven by urban pockets, convenience retailing, and growth in food delivery while governance around single-use plastics and nascent recycling systems shape the competitive landscape. Adoption of on-the-go formats tends to be concentrated in affluent urban areas and tourism corridors, and suppliers are increasingly experimenting with compostable and paper-based alternatives tailored to local regulatory moves and consumer awareness campaigns, even as logistical and cost constraints limit rapid, widespread adoption across the region.

On the Go Packaging Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the on the go packaging market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global on the go packaging market include:

- American Packaging

- Bemis

- Berry Plastics

- Amcor

- Berry Plastics

- Bryce

- Coveris

- Hood Packaging

- InterFlex

- Huhtamaki

- Mondi

- Printpack

- 0020Oracle Packaging

- Novolex

- Pregis

- Sealed Air

- Proampac

- Scholle IPN

- Sonoco Products

- Sigma Plastics

- Winpak

- WestRock

The global on the go packaging market is segmented as follows:

By Flexible Packaging

- Clamshells

- Peel off Lids

- Plastic Trays

- Zip Pouches

By Paperboard Packaging

- Corrugated Boxes

- Folding Cartons

- Rigid Boxes

By End User

- Food and Beverage

- Healthcare

- Hygiene Products

- Personal Care Industries

- Pharmaceuticals

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1.Preface

- 1.1.Report Description

- 1.1.Report Scope

- Chapter 2.Research Methodulogy

- 2.1.Research Methodulogy

- 2.2.Secondary Research

- 2.3.Primary Research

- 2.4.Models

- 2.4.1.Company Share Analysis Model

- 2.4.2.Revenue Based Modeling

- 2.5.Research Limitations

- Chapter 3.Executive Summary

- 3.1.Global On the Go Packaging Market, 2016 – 2026 (USD Million)

- 3.2.Global On the Go Packaging Market: Snapshot

- Chapter 4.On the Go Packaging Market – Industry Analysis

- 4.1.Introduction

- 4.2.Market Drivers

- 4.3.Market Restraints

- 4.3.1.Restraining Factor Analysis

- 4.4.Market Opportunities

- 4.5.Porter’s Five Forces Analysis

- 4.6.COVID 19 Impact Analysis

- Chapter 5.Investment Proposition Analysis

- 5.1.Global On the Go Packaging Market Attractiveness, By Flexible Packaging

- 5.2.Global On the Go Packaging Market Attractiveness, By Paperboard Packaging

- 5.3.Global On the Go Packaging Market Attractiveness, By End User

- 5.4.Global On the Go Packaging Market Attractiveness, By Region

- Chapter 6.Competitive Landscape

- 6.1.Company Market Share Analysis - 2019

- 6.1.1.Global On the Go Packaging Market: Company Market Share, 2019

- 6.2.Strategic Developments

- 7.1.Global On the Go Packaging Market Overview: by Flexible Packaging

- 7.1.1.Global On the Go Packaging Market Revenue Share, by Flexible Packaging, 2019 & 2026

- 7.2.Global On the Go Packaging Market Analysis/Overview – By Flexible Packaging

- 7.2.1.Clamshells – Overview/Analysis

- 7.2.2.Peel Off Lids – Overview/Analysis

- 7.2.3.Plastic Trays – Overview/Analysis

- 7.2.4.Zip Pouches – Overview/Analysis

- 7.3.Clamshells

- 7.3.1.Global On the Go Packaging Market for Clamshells, Revenue (USD Million) 2016 - 2026

- 7.4.Peel Off Lids

- 7.4.1.Global On the Go Packaging Market for Peel Off Lids, Revenue (USD Million) 2016 - 2026

- 7.5.Plastic Trays

- 7.5.1.Global On the Go Packaging Market for Plastic Trays, Revenue (USD Million) 2016 - 2026

- 7.6.Zip Pouches

- 7.6.1.Global On the Go Packaging Market for Zip Pouches, Revenue (USD Million) 2016 - 2026

- 8.1.Global On the Go Packaging Market Overview: by Paperboard Packaging

- 8.1.1.Global On the Go Packaging Market Revenue Share, by Paperboard Packaging, 2019 & 2026

- 8.2.Global On the Go Packaging Market Analysis/Overview – By Paperboard Packaging

- 8.2.1.Corrugated Boxes – Overview/Analysis

- 8.2.2.Fulding Cartons – Overview/Analysis

- 8.2.3.Rigid Boxes – Overview/Analysis

- 8.3.Corrugated Boxes

- 8.3.1.Global On the Go Packaging Market for Corrugated Boxes, Revenue (USD Million) 2016 - 2026

- 8.4.Fulding Cartons

- 8.4.1.Global On the Go Packaging Market for Fulding Cartons, Revenue (USD Million) 2016 - 2026

- 8.5.Rigid Boxes

- 8.5.1.Global On the Go Packaging Market for Rigid Boxes, Revenue (USD Million) 2016 - 2026

- 9.1.Global On the Go Packaging Market Overview: by End User

- 9.1.1.Global On the Go Packaging Market Revenue Share, by End User, 2019 & 2026

- 9.2.Global On the Go Packaging Market Analysis/Overview – By End User

- 9.2.1.Food Beverage – Overview/Analysis

- 9.2.2.Healthcare – Overview/Analysis

- 9.2.3.Hygiene Products – Overview/Analysis

- 9.2.4.Personal Care Industries – Overview/Analysis

- 9.2.5.Pharmaceuticals – Overview/Analysis

- 9.3.Food Beverage

- 9.3.1.Global On the Go Packaging Market for Food Beverage, Revenue (USD Million) 2016 - 2026

- 9.4.Healthcare

- 9.4.1.Global On the Go Packaging Market for Healthcare, Revenue (USD Million) 2016 - 2026

- 9.5.Hygiene Products

- 9.5.1.Global On the Go Packaging Market for Hygiene Products, Revenue (USD Million) 2016 - 2026

- 9.6.Personal Care Industries

- 9.6.1.Global On the Go Packaging Market for Personal Care Industries, Revenue (USD Million) 2016 - 2026

- 9.7.Pharmaceuticals

- 9.7.1.Global On the Go Packaging Market for Pharmaceuticals, Revenue (USD Million) 2016 - 2026

- 6.1.Company Market Share Analysis - 2019

- Chapter 10.On the Go Packaging Market – Regional Analysis

- 10.1.Global On the Go Packaging Market: Regional Overview

- 10.1.1.Global On the Go Packaging Market Revenue Share, by Region, 2019 & 2026

- 10.1.2.Global On the Go Packaging Market Revenue, by Region, 2016 – 2026 (USD Million)

- 10.2.North America

- 10.2.1.North America On the Go Packaging Market Revenue, 2016 - 2026 (USD Million)

- 10.2.2.North America On the Go Packaging Market Revenue, by Country, 2016 – 2026 (USD Million)

- 10.2.3.North America On the Go Packaging Market Revenue, by Flexible Packaging, 2016 – 2026

- 10.2.4.North America On the Go Packaging Market Revenue, by Paperboard Packaging, 2016 – 2026

- 10.2.5.North America On the Go Packaging Market Revenue, by End User, 2016 – 2026

- 10.2.6. U.S.

- 10.2.7.Canada

- 10.3.Europe

- 10.3.1.Europe On the Go Packaging Market Revenue, 2016 - 2026 (USD Million)

- 10.3.2.Europe On the Go Packaging Market Revenue, by Country, 2016 – 2026 (USD Million)

- 10.3.3.Europe On the Go Packaging Market Revenue, by Flexible Packaging, 2016 – 2026

- 10.3.4.Europe On the Go Packaging Market Revenue, by Paperboard Packaging, 2016 – 2026

- 10.3.5.Europe On the Go Packaging Market Revenue, by End User, 2016 – 2026

- 10.3.6.Germany

- 10.3.7.France

- 10.3.8. U.K.

- 10.3.9.Italy

- 10.3.10.Spain

- 10.3.11.Rest of Europe

- 10.4.Asia Pacific

- 10.4.1.Asia Pacific On the Go Packaging Market Revenue, 2016 - 2026 (USD Million)

- 10.4.2.Asia Pacific On the Go Packaging Market Revenue, by Country, 2016 – 2026 (USD Million)

- 10.4.3.Asia Pacific On the Go Packaging Market Revenue, by Flexible Packaging, 2016 – 2026

- 10.4.4.Asia Pacific On the Go Packaging Market Revenue, by Paperboard Packaging, 2016 – 2026

- 10.4.5.Asia Pacific On the Go Packaging Market Revenue, by End User, 2016 – 2026

- 10.4.6.China

- 10.4.7.Japan

- 10.4.8.India

- 10.4.9.South Korea

- 10.4.10.South-East Asia

- 10.4.11.Rest of Asia Pacific

- 10.5.Latin America

- 10.5.1.Latin America On the Go Packaging Market Revenue, 2016 - 2026 (USD Million)

- 10.5.2.Latin America On the Go Packaging Market Revenue, by Country, 2016 – 2026 (USD Million)

- 10.5.3.Latin America On the Go Packaging Market Revenue, by Flexible Packaging, 2016 – 2026

- 10.5.4.Latin America On the Go Packaging Market Revenue, by Paperboard Packaging, 2016 – 2026

- 10.5.5.Latin America On the Go Packaging Market Revenue, by End User, 2016 – 2026

- 10.5.6.Brazil

- 10.5.7.Mexico

- 10.5.8.Rest of Latin America

- 10.6.The Middle-East and Africa

- 10.6.1.The Middle-East and Africa On the Go Packaging Market Revenue, 2016 - 2026 (USD Million)

- 10.6.2.The Middle-East and Africa On the Go Packaging Market Revenue, by Country, 2016 – 2026 (USD Million)

- 10.6.3.The Middle-East and Africa On the Go Packaging Market Revenue, by Flexible Packaging, 2016 – 2026

- 10.6.4.The Middle-East and Africa On the Go Packaging Market Revenue, by Paperboard Packaging, 2016 – 2026

- 10.6.5.The Middle-East and Africa On the Go Packaging Market Revenue, by End User, 2016 – 2026

- 10.6.6.GCC Countries

- 10.6.7.South Africa

- 10.6.8.Rest of Middle-East Africa

- 10.1.Global On the Go Packaging Market: Regional Overview

- Chapter 11.Company Profiles

- 11.1.Berry Plastics

- 11.1.1.Company Overview

- 11.1.2.Financial Overview

- 11.1.3.Product Portfulio

- 11.1.4.Business Strategy

- 11.1.5.Recent Developments

- 11.2.Amcor

- 11.3.American Packaging

- 11.4.Bemis

- 11.5.Berry Plastics

- 11.6.Bryce

- 11.7.Coveris

- 11.8.Hood Packaging

- 11.9.Huhtamaki

- 11.1.InterFlex

- 11.11.Mondi

- 11.12.Novulex

- 11.13.Oracle Packaging

- 11.14.Pregis

- 11.15.Printpack

- 11.16.Proampac

- 11.17.Schulle IPN

- 11.18.Sealed Air

- 11.19.Sigma Plastics

- 11.2.Sonoco Products

- 11.21.WestRock

- 11.22.Winpak

- 11.1.Berry Plastics

Inquiry For Buying

On the Go Packaging

Request Sample

On the Go Packaging