Organic Ceramic Binders Market Size, Share, and Trends Analysis Report

CAGR :

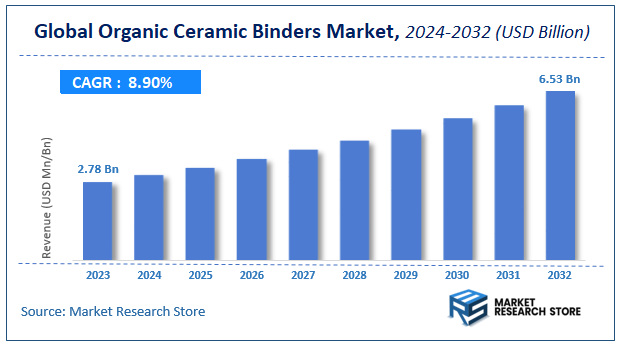

| Market Size 2023 (Base Year) | USD 2.78 Billion |

| Market Size 2032 (Forecast Year) | USD 6.53 Billion |

| CAGR | 8.9% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Organic Ceramic Binders Market Insights

According to Market Research Store, the global organic ceramic binders market size was valued at around USD 2.78 billion in 2023 and is estimated to reach USD 6.53 billion by 2032, to register a CAGR of approximately 8.9% in terms of revenue during the forecast period 2024-2032.

The organic ceramic binders report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Organic Ceramic Binders Market: Overview

Organic ceramic binders are specialized polymer-based materials used in the ceramic industry to enhance the shaping, binding, and mechanical strength of ceramic components before sintering. These binders help improve the green strength of ceramic bodies, ensuring better handling and precision in manufacturing processes such as pressing, extrusion, and casting. They decompose during the firing process, leaving behind a structurally intact ceramic material with minimal residue. Organic ceramic binders are commonly used in applications like advanced ceramics, electronic components, coatings, and refractory materials.

Key Highlights

- The organic ceramic binders market is anticipated to grow at a CAGR of 8.9% during the forecast period.

- The global organic ceramic binders market was estimated to be worth approximately USD 2.78 billion in 2023 and is projected to reach a value of USD 6.53 billion by 2032.

- The growth of the organic ceramic binders market is being driven by increasing demand in various end-use industries such as electronics, automotive, aerospace, and construction.

- Based on the type, the epoxy resin system segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the advanced ceramics segment is projected to swipe the largest market share.

- In terms of end-user industry, the electronics segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Organic Ceramic Binders Market: Dynamics

Key Growth Drivers:

- Increasing Demand for Advanced Ceramics: Advanced ceramics, with their superior properties, are used in various applications like electronics, aerospace, and biomedical devices. This drives the demand for high-quality organic binders used in their manufacturing.

- Growing Construction and Infrastructure Development: The construction industry uses ceramics in tiles, sanitary ware, and other applications. Ongoing infrastructure development projects contribute to the demand for organic binders in this sector.

- Rising Automotive Production: Ceramics are increasingly used in automotive components for their durability and heat resistance. The growth of the automotive industry drives the demand for organic binders used in ceramic manufacturing.

- Technological Advancements: Innovations in organic binder technology, such as improved binding strength, burnout properties, and compatibility with different ceramic materials, are contributing to market growth.

Restraints:

- Cost of High-Performance Binders: High-quality organic binders with specialized properties can be expensive, which can be a barrier for some ceramic manufacturers, especially smaller companies.

- Challenges in Binder Removal: Removing the organic binder completely during the firing process without leaving residues or affecting the ceramic properties can be challenging.

- Environmental Concerns: Some organic binders may contain volatile organic compounds (VOCs) or other chemicals that can raise environmental concerns.

Opportunities:

- Development of Bio-Based Binders: There is a growing opportunity to develop organic binders derived from renewable resources, such as plant-based materials, to address environmental concerns and meet the demand for sustainable products.

- Specialized Binders for Additive Manufacturing: The increasing use of additive manufacturing (3D printing) in ceramics creates opportunities for developing specialized organic binders that are compatible with these processes.

- Improved Binder Efficiency: Research and development efforts can focus on improving the binding efficiency of organic binders, allowing for lower usage rates and cost savings for ceramic manufacturers.

Challenges:

- Maintaining Quality and Consistency: Ensuring consistent quality and performance of organic binders is crucial, as variations in properties can affect the final ceramic product.

- Compatibility with Different Ceramic Materials: Organic binders need to be compatible with a wide range of ceramic materials and processing techniques, which can be a challenge.

- Meeting Specific Application Requirements: Ceramic manufacturers have specific requirements for organic binders depending on the application and desired properties of the final ceramic product, which can be challenging to meet.

Organic Ceramic Binders Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Organic Ceramic Binders Market |

| Market Size in 2023 | USD 2.78 Billion |

| Market Forecast in 2032 | USD 6.53 Billion |

| Growth Rate | CAGR of 8.9% |

| Number of Pages | 140 |

| Key Companies Covered | KYOEISHA CHEMICAL, Bhiwadi Polymers, Polychemistry, Kuraray, Sekisui, Shreejichemicals, Ransom & Randolph, Toagosei, Nantong Mingfeng Adhesive Products, Changxing Haoyang Building Materials |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Organic Ceramic Binders Market: Segmentation Insights

The global organic ceramic binders market is divided by type, application, end-user industry and region.

Segmentation Insights by Type

Based on type, the global organic ceramic binders market is divided into epoxy resin system, organosilicon system, acrylic polymer, and other.

The Epoxy Resin System segment holds the dominant position in the organic ceramic binders market. This dominance is attributed to its excellent thermal and chemical resistance, superior adhesion, and durability, making it highly suitable for applications in electronics, aerospace, and automotive industries. Epoxy-based ceramic binders are widely used in coatings, adhesives, and composites, offering exceptional mechanical strength and long-term stability. Their ability to withstand high temperatures and harsh environmental conditions makes them a preferred choice for high-performance applications.

The Organosilicon System follows as the second most significant segment. Organosilicon ceramic binders are valued for their outstanding heat resistance, water repellency, and electrical insulation properties. These binders are extensively used in advanced coatings, adhesives, and sealants, particularly in industries requiring high-temperature stability, such as construction and electronics. Their flexibility and ability to form strong bonds with ceramics and other materials contribute to their growing demand.

The Acrylic Polymer segment ranks third, primarily due to its versatility and cost-effectiveness. Acrylic-based ceramic binders offer good adhesion, weather resistance, and ease of application, making them ideal for coatings, paints, and construction materials. While they may not provide the same level of heat and chemical resistance as epoxy or organosilicon systems, they are widely used in applications where durability and aesthetics are key factors.

Segmentation Insights by Application

On the basis of application, the global organic ceramic binders market is bifurcated into traditional ceramics, advanced ceramics, abrasives, and others.

The Advanced Ceramics segment is the most dominant in the organic ceramic binders market. This is driven by the increasing demand for high-performance materials in industries such as aerospace, electronics, medical, and energy. Advanced ceramics require binders with superior thermal stability, mechanical strength, and chemical resistance, making organic ceramic binders an essential component in their production. Their usage in applications like semiconductors, biomedical implants, and high-tech engineering components has contributed significantly to their market dominance.

The Traditional Ceramics segment follows closely, supported by the continued use of ceramic binders in pottery, tiles, sanitaryware, and tableware. Organic ceramic binders enhance the mechanical strength and durability of traditional ceramics while aiding in the shaping and molding processes. Although this segment does not demand the same level of performance as advanced ceramics, it still holds a substantial share in the market due to the widespread use of ceramics in construction and household applications.

The Abrasives segment ranks third, as organic ceramic binders play a crucial role in the production of grinding wheels, sandpapers, and cutting tools. These binders help in the adhesion of abrasive particles, ensuring durability and performance in various industrial applications. The demand for abrasives is steady across manufacturing, automotive, and metalworking industries, but it is smaller in scale compared to advanced and traditional ceramics.

Segmentation Insights by End-user Industry

On the basis of end-user industry, the global organic ceramic binders market is bifurcated into automotive, electronics, aerospace, and others.

The Electronics industry holds the dominant position in the organic ceramic binders market. This is due to the increasing demand for high-performance ceramic components in electronic devices, semiconductors, and printed circuit boards (PCBs). Organic ceramic binders are essential in manufacturing dielectric ceramics, multilayer capacitors, and advanced electronic packaging materials. With the rapid expansion of consumer electronics, 5G infrastructure, and miniaturized components, the demand for these binders continues to grow significantly.

The Aerospace industry follows as the second most significant segment. Aerospace applications require materials with exceptional thermal resistance, mechanical strength, and durability, making organic ceramic binders essential in the production of high-temperature ceramics, thermal barrier coatings, and composite materials. These binders contribute to the development of lightweight and heat-resistant components used in jet engines, spacecraft, and other aerospace structures. The continuous advancements in aerospace technology and the push for fuel-efficient aircraft are driving further growth in this segment.

The Automotive industry ranks third, leveraging organic ceramic binders for manufacturing ceramic-based components such as catalytic converters, sensors, and brake pads. With the increasing adoption of electric vehicles (EVs) and stringent emission regulations, ceramic components are playing a crucial role in enhancing vehicle efficiency and sustainability. Although automotive applications rely on these binders, their market share remains smaller compared to electronics and aerospace due to the limited volume of ceramic components in vehicles.

Organic Ceramic Binders Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region leads the organic ceramic binders market, driven by rapid industrialization and urbanization in countries like China, India, and Japan. The robust growth in construction, automotive, and electronics sectors in these nations has significantly increased the demand for high-quality ceramics, thereby boosting the market for organic ceramic binders. The region's focus on infrastructure development and technological advancements further propels this demand, positioning Asia Pacific as the dominant player in the market.

North America holds a substantial share in the organic ceramic binders market, primarily due to its well-established automotive and aerospace industries. The United States, in particular, has seen a growing adoption of advanced ceramics in various industrial applications, driven by the need for high-performance materials. Additionally, the region's emphasis on technological innovation and sustainable manufacturing practices contributes to the steady demand for organic ceramic binders.

Europe is another significant market for organic ceramic binders, with countries like Germany, France, and the United Kingdom leading the way. The region's strong automotive and electronics sectors drive the demand for advanced ceramics. Moreover, Europe's commitment to sustainable manufacturing and the development of eco-friendly materials further enhances the market growth for organic ceramic binders.

Latin America is experiencing steady growth in the organic ceramic binders market, supported by expanding construction and manufacturing industries in countries such as Brazil and Argentina. Infrastructure development projects and increasing consumption of ceramic products are key factors driving the demand for organic ceramic binders in this region.

The Middle East and Africa region is witnessing growth in the organic ceramic binders market, driven by infrastructure development projects, urbanization, and industrial growth. The construction sector in countries like the UAE, Saudi Arabia, and South Africa plays a pivotal role in increasing the demand for organic ceramic binders, particularly for applications in tiles, ceramics, and advanced materials.

Organic Ceramic Binders Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the organic ceramic binders market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global organic ceramic binders market include:

- KYOEISHA CHEMICAL

- 3M Company

- Advanced Ceramic Materials (ACM)

- AGC Inc.

- BASF SE

- CeramTec GmbH

- CoorsTek Inc.

- Denka Company Limited

- Dow Inc.

- Elkem ASA

- Ferro Corporation

- H.C. Starck GmbH

- Hitachi Chemical Co. Ltd.

- Bhiwadi Polymers

- Polychemistry

- Kuraray

- Sekisui

- Shreejichemicals

- Ransom & Randolph

- Toagosei

- Nantong Mingfeng Adhesive Products

- Changxing Haoyang Building Materials

- Kyocera Corporation

- Morgan Advanced Materials plc.

- Nippon Electric Glass Co. Ltd.

- Saint-Gobain S.A.

- Schott AG

- Showa Denko K.K.

- Sumitomo Chemical Co. Ltd.

- Zircoa Inc.

The global organic ceramic binders market is segmented as follows:

By Type

- Epoxy Resin System

- Organosilicon System

- Acrylic Polymer

- Other

By Application

- Traditional Ceramics

- Advanced Ceramics

- Abrasives

- Others

By End-User Industry

- Automotive

- Electronics

- Aerospace

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global organic ceramic binders market size was projected at approximately US$ 2.78 billion in 2023. Projections indicate that the market is expected to reach around US$ 6.53 billion in revenue by 2032.

The global organic ceramic binders market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 8.9% during the forecast period from 2024 to 2032.

Asia Pacific is expected to dominate the global organic ceramic binders market.

The global organic ceramic binders market is driven by increasing demand for advanced ceramics in automotive, electronics, and construction industries. Rapid industrialization, infrastructure development, and a growing focus on high-performance and eco-friendly materials further fuel market growth.

Some of the prominent players operating in the global organic ceramic binders market are; KYOEISHA CHEMICAL, 3M Company, Advanced Ceramic Materials (ACM), AGC Inc., BASF SE, CeramTec GmbH, CoorsTek Inc., Denka Company Limited, Dow Inc., Elkem ASA, Ferro Corporation, H.C. Starck GmbH, Hitachi Chemical Co. Ltd., Bhiwadi Polymers, Polychemistry, Kuraray, Sekisui, Shreejichemicals, Ransom & Randolph, Toagosei, Nantong Mingfeng Adhesive Products, Changxing Haoyang Building Materials, Kyocera Corporation, Morgan Advanced Materials plc., Nippon Electric Glass Co. Ltd., Saint-Gobain S.A., Schott AG, Showa Denko K.K., Sumitomo Chemical Co. Ltd., Zircoa Inc., and others.

The global organic ceramic binders market report provides a comprehensive analysis of market definitions, growth factors, opportunities, challenges, geographic trends, and competitive dynamics.

Table Of Content

Inquiry For Buying

Organic Ceramic Binders

Request Sample

Organic Ceramic Binders