Phenolic Resins Market Size, Share, and Trends Analysis Report

CAGR :

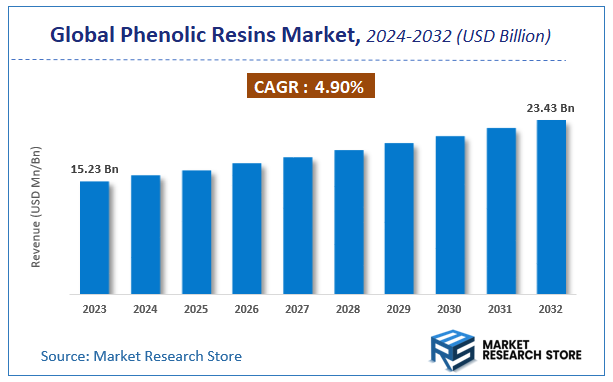

| Market Size 2023 (Base Year) | USD 15.23 Billion |

| Market Size 2032 (Forecast Year) | USD 23.43 Billion |

| CAGR | 4.9% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Phenolic Resins Market Insights

According to Market Research Store, the global phenolic resins market size was valued at around USD 15.23 billion in 2023 and is estimated to reach USD 23.43 billion by 2032, to register a CAGR of approximately 4.9% in terms of revenue during the forecast period 2024-2032.

The phenolic resins report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Phenolic Resins Market: Overview

Phenolic resins are synthetic polymers produced by the reaction of phenol (or substituted phenols) with formaldehyde. They are among the earliest synthetic resins developed and are known for their excellent thermal stability, flame resistance, mechanical strength, and dimensional stability. Phenolic resins are broadly classified into two types: resols (produced under basic conditions) and novolacs (produced under acidic conditions and typically requiring a curing agent). These resins are widely used in applications such as adhesives, molded components, laminates, coatings, foundry binders, insulation foams, and friction materials.

The growth of the phenolic resins market is driven by rising demand from end-use industries such as automotive, construction, electronics, aerospace, and industrial manufacturing. In the automotive sector, phenolic resins are crucial for brake pads, clutch facings, and under-the-hood components due to their heat resistance and durability. In construction, they are used in plywood adhesives and thermal insulation materials.

Key Highlights

- The phenolic resins market is anticipated to grow at a CAGR of 4.9% during the forecast period.

- The global phenolic resins market was estimated to be worth approximately USD 15.23 billion in 2023 and is projected to reach a value of USD 23.43 billion by 2032.

- The growth of the phenolic resins market is being driven by a powerful confluence of factors, primarily the escalating demand from key end-use industries such as automotive, construction, and electronics.

- Based on the product, the novolac segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the wood adhesives segment is projected to swipe the largest market share.

- In terms of end user, the abrasives segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Phenolic Resins Market: Dynamics

Key Growth Drivers:

- Robust Growth in the Automotive Sector: Phenolic resins are extensively used in the automotive industry for various components, including brake linings, clutch facings, engine parts, and electrical components, due to their excellent heat resistance, friction properties, and dimensional stability. The increasing global vehicle production, especially the demand for lightweight and high-performance components, drives the market.

- Increasing Demand from Building and Construction: Phenolic resins are crucial for manufacturing insulation materials (e.g., phenolic foam), plywood, particleboard, and fire-resistant laminates. The booming construction industry, particularly in residential and commercial sectors, coupled with stringent fire safety regulations, fuels the demand for these resins.

- Rising Adoption in Abrasives and Friction Materials: Their high heat resistance and excellent bonding capabilities make phenolic resins ideal binders for abrasives (e.g., grinding wheels, sandpaper) and friction materials (e.g., brake pads, clutch plates). The growth in manufacturing and industrial applications drives this segment.

Restraints:

- Volatility of Raw Material Prices: The primary raw materials for phenolic resins are phenol and formaldehyde. The prices of these chemicals are largely dependent on crude oil and natural gas prices. Fluctuations in these petrochemical feedstocks directly impact the manufacturing cost of phenolic resins, leading to price instability and affecting profit margins for manufacturers.

- Environmental Concerns and Regulations Regarding Formaldehyde: Formaldehyde, a key raw material, is classified as a hazardous substance due to its potential health effects (e.g., carcinogen). Increasingly stringent environmental regulations and health concerns regarding formaldehyde emissions (especially from wood products) are driving the demand for low-formaldehyde or formaldehyde-free resins, which can be challenging to produce and might have different performance characteristics.

- Competition from Alternative Resins: Phenolic resins face competition from other polymer resins like epoxy resins, polyurethane resins, and polyester resins in various applications. While phenolics have specific advantages, alternatives might be preferred based on cost, processing requirements, or specific end-use performance needs.

Opportunities:

- Development of Bio-based Phenolic Resins: Significant opportunities exist in the research and commercialization of phenolic resins derived from bio-based feedstocks (e.g., lignin from biomass, tannin). This aligns with global sustainability trends, reduces reliance on fossil fuels, and addresses environmental concerns.

- Lightweighting in Automotive and Aerospace: The continuous drive for lightweight materials in automotive (for fuel efficiency and EV range) and aerospace (for performance) presents opportunities for advanced phenolic composites and foams that offer high strength-to-weight ratios.

- High-Performance and Specialty Applications: Focus on developing specialty phenolic resins for niche, high-value applications requiring extreme performance, such as aerospace components, specialized electronics, and advanced friction materials, can yield higher profit margins.

Challenges:

- Addressing Formaldehyde Emission Concerns: The paramount challenge is to continuously innovate and develop cost-effective, high-performance phenolic resins with ultra-low or zero formaldehyde emissions, to meet evolving regulatory standards and consumer demands for healthier indoor environments.

- Disposal and Recycling of Thermoset Products: As thermosetting polymers, phenolic resins are challenging to recycle once cured. Developing viable and economic recycling methods for phenolic resin-based products remains a significant technical and environmental challenge.

- Competition from Other Sustainable Materials: The market faces competition from other sustainable materials or alternative resin systems that might offer better environmental profiles or easier recyclability, pushing phenolic resin manufacturers to innovate continually.

Phenolic Resins Market: Report Scope

This report thoroughly analyzes the Phenolic Resins Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Phenolic Resins Market |

| Market Size in 2023 | USD 15.23 Billion |

| Market Forecast in 2032 | USD 23.43 Billion |

| Growth Rate | CAGR of 4.9% |

| Number of Pages | 160 |

| Key Companies Covered | BASF SE, Georgia Pacific Chemicals LLC, Chang Chun Plastics Co. Ltd., Sumitomo Baketile, Mitsui Chemicals Inc., Momentive Specialty Chemicals Inc. SI Group Sumitomo Bakelite Co., Ltd Kolon Industries, Inc. and certain other |

| Segments Covered | By Product, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Phenolic Resins Market: Segmentation Insights

The global phenolic resins market is divided by product, application, end user, and region.

Based on product, the global phenolic resins market is divided into novolac, resol, and others. Novolac resins dominate the phenolic resins market in terms of volume and application versatility. These thermoplastic phenolic resins are typically produced by reacting phenol with formaldehyde in the presence of an acid catalyst and require a curing agent (usually hexamethylenetetramine) for cross-linking. Novolac resins offer excellent thermal stability, mechanical strength, and chemical resistance, making them ideal for use in molded components, laminates, abrasives, and adhesives. Their widespread usage in industrial applications—particularly in automotive brake linings, refractory products, and electronics—has solidified their market leadership. The demand for high-performance materials in extreme conditions, particularly in manufacturing and metallurgy industries in North America, further drives the growth of this segment.

On the basis of application, the global phenolic resins market is bifurcated into wood adhesives, molding, insulations, laminates, paper impregnation, coatings, and others. Wood Adhesives are the dominant application segment in the phenolic resins market, accounting for the largest share due to their extensive use in bonding engineered wood products such as plywood, oriented strand boards (OSB), laminated veneer lumber (LVL), and particle boards. Phenolic resins offer exceptional water resistance, heat stability, and structural integrity, making them ideal for interior and exterior construction applications. Their widespread use in the construction and furniture sectors, particularly in North America and Europe, is driven by the need for durable and formaldehyde-emission-compliant bonding agents. Additionally, the demand for cost-effective, long-lasting materials in infrastructure and housing projects continues to sustain the dominance of phenolic resins in wood adhesive formulations.

In terms of other applications, the global phenolic resins market is bifurcated into abrasives, composites, carbon binders, friction materials, sound-proof bonding felt, and tires & rubber. Abrasives are the dominant application among the other uses of phenolic resins due to their critical role as binding agents in bonded and coated abrasive products such as grinding wheels, cutting discs, sanding belts, and polishing pads. Phenolic resins provide excellent thermal resistance, mechanical strength, and dimensional stability under high friction and pressure, making them essential in heavy-duty industrial applications. Their ability to hold abrasive grains firmly while withstanding high temperatures generated during machining operations has solidified their position in the global abrasives market. The growth of metal fabrication, automotive manufacturing, and construction sectors—particularly in North America and Asia-Pacific—continues to fuel demand for phenolic resin-based abrasive solutions.

Phenolic Resins Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the phenolic resins market due to strong demand from the automotive, construction, electrical, and aerospace industries. The United States is the largest consumer in the region, driven by its highly developed industrial base and the extensive use of phenolic resins in brake pads, insulation materials, and adhesives. In construction, phenolic resins are widely used in laminated panels, plywood, and oriented strand boards (OSB) for their excellent thermal stability, fire resistance, and bonding strength. The automotive industry uses these resins in friction materials and molded parts due to their heat resistance and dimensional stability. Major manufacturers such as Hexion and DIC Corporation operate significant production facilities in the region. North America also leads in research and development of low-emission and bio-based phenolic resins to meet stringent environmental and occupational safety standards, particularly from the EPA and OSHA.

Europe holds a significant share in the phenolic resins market, with Germany, France, and the United Kingdom as key contributors. The region is known for high-performance applications in transportation, electronics, and building materials, where phenolic resins are used in circuit boards, structural laminates, and insulation foams. European regulations, such as REACH, drive innovation in low-formaldehyde and environmentally friendly phenolic formulations. Demand is particularly strong in countries with well-established automotive and aerospace manufacturing industries. Germany leads in the production of engineered wood products and friction materials, while Scandinavia and Central Europe are key markets for thermal insulation applications. Despite environmental restrictions, Europe continues to invest in product enhancements focused on flame retardancy, recyclability, and high-temperature resistance.

Asia-Pacific is the fastest-growing region in the phenolic resins market, with China, Japan, South Korea, and India at the forefront. The region benefits from a rapidly expanding construction industry, increasing automotive production, and growing demand for electronics. China is the largest consumer and producer, supported by large-scale manufacturing of wood panels, automotive components, and electrical laminates. Japan and South Korea lead in high-tech applications such as semiconductor encapsulation and advanced composites. India is witnessing increased demand for phenolic-based adhesives and insulation products, especially in residential and commercial construction. Regional growth is supported by competitive production costs, rising urbanization, and growing infrastructure investments. However, environmental concerns and regulatory pressures are pushing the market toward the development of low-emission and formaldehyde-free phenolic resin technologies.

Latin America presents a moderately growing market for phenolic resins, with Brazil and Mexico as major contributors. The market is driven by demand from the wood panel, automotive, and construction sectors. In Brazil, the furniture and plywood industries use phenolic resins extensively due to their moisture resistance and bonding properties. Mexico, with its strong automotive manufacturing base, contributes through the use of phenolic resins in brake linings, clutch facings, and under-the-hood components. Despite growing applications, the region faces challenges such as reliance on imported raw materials, economic instability, and limited investment in advanced resin technologies. Nonetheless, increasing infrastructure development and gradual adoption of sustainable materials are likely to support market expansion in the medium term.

Middle East & Africa represent an emerging market for phenolic resins, with growth centered in the UAE, Saudi Arabia, South Africa, and Egypt. In the Middle East, construction and industrial insulation drive demand, particularly for phenolic foams used in HVAC and pipeline insulation. The region’s focus on fire-safe building materials and energy-efficient construction solutions supports the adoption of phenolic resin-based products. In Africa, South Africa leads in wood product manufacturing and automotive components, where phenolic resins are used in adhesives and friction materials. However, limited local manufacturing, high import dependence, and slower technological adoption restrict the pace of market development. With increasing investment in construction, industrial infrastructure, and regulatory modernization, the region holds long-term potential for growth in specialized phenolic applications.

Phenolic Resins Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the phenolic resins market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global phenolic resins market include:

- DIC CORPORATION

- Kolon Industries, Inc.

- Sumitomo Bakelite Co., Ltd.

- Hexcel Corporation

- Georgia-Pacific Chemicals

- KRATON CORPORATION

- Hexion

- Bostik, Inc.

- SI Group, Inc.

The global phenolic resins market is segmented as follows:

By Product

- Novolac

- Resol

- Others

By Application

- Wood Adhesives

- Molding

- Insulations

- Laminates

- Paper Impregnation

- Coatings

- Others

By End User

- Abrasives

- Composites

- Carbon Binders

- Friction Materials

- Sound-proof Bonding Felt

- Tires & Rubber

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global phenolic resins market, 2014 – 2020 (Kilo Tons) (USD Million)

- 2.2. Global phenolic resins market : Snapshot

- Chapter 3. Global Phenolic Resins – Market Dynamics

- 3.1. Introduction

- 3.2. Value chain analysis

- 3.3. Market drivers

- 3.3.1. Drivers for global phenolic resins market: Impact analysis

- 3.3.2. Increasing demand for tiers

- 3.3.3. Developing automotive industries

- 3.4. Market restraints

- 3.4.1. Restraints for global phenolic resins market: Impact analysis

- 3.4.2. High cost

- 3.5. Market opportunities

- 3.5.1. Adoption of new nanotechnology

- 3.5.2. Increasing construction industry

- 3.6. Porter’s five forces analysis

- 3.6.1. Bargaining power of suppliers

- 3.6.2. Bargaining power of buyers

- 3.6.3. Threat of new entrants

- 3.6.4. Threat from substitutes

- 3.6.5. Degree of competition

- 3.7. Phenolic resins: Market attractiveness analysis

- 3.7.1. Market attractiveness analysis by product segment

- 3.7.2. Market attractiveness analysis by application segment

- 3.7.3. Market attractiveness analysis by regional segment

- Chapter 4. Global Phenolic Resins Market – Competitive Landscape

- 4.1. Global phenolic resins market: Company market share, 2014

- 4.2. Global phenolic resins market: Production capacity (subject to data availability)

- 4.3. Global phenolic resins market: Raw material analysis

- 4.4. Global phenolic resins market: Price trend analysis

- Chapter 5. Phenolic Resins Market – Product segment analysis

- 5.1. Global phenolic resins market: Product overview

- 5.1.1. Global phenolic resins market volume share, by product, 2014 and 2020

- 5.2. Resol

- 5.2.1. Global resol resins market, 2014 – 2020 (Kilo Tons) (USD Million)

- 5.3. Novolac

- 5.3.1. Global novlac resins market, 2014 – 2020 (Kilo Tons) (USD Million)

- 5.4. Others

- 5.4.1. Global others phenolic resins market, 2014 – 2020 (Kilo Tons) (USD Million)

- 5.1. Global phenolic resins market: Product overview

- Chapter 6. Phenolic Resins Market - Application Analysis

- 6.1. Global phenolic resins market: Application overview

- 6.1.1. Global phenolic resins market volume share, by application, 2014 and 2020

- 6.2. Wood-adhesives

- 6.2.1. Global phenolic resins market for wood-adhesives, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.3. Molding compounds

- 6.3.1. Global phenolic resins market for molding compounds, 2014 - 2020(Kilo Tons) (USD Million)

- 6.4. Laminates

- 6.4.1. Global phenolic resins market for laminates, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.5. Insulation

- 6.5.1. Global phenolic resins market for insulation, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.6. Others

- 6.6.1. Global phenolic resins market for other applications, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.1. Global phenolic resins market: Application overview

- Chapter 7. Phenolic Resins Market - Regional Analysis

- 7.1. Global phenolic resins market: Regional overview

- 7.1.1. Global phenolic resins market volume share, by region, 2014 & 2020

- 7.2. North America

- 7.2.1. North America phenolic resins market volume, by product, 2014- 2020 (Kilo Tons)

- 7.2.2. North America phenolic resins market revenue, by product, 2014- 2020 (USD Million)

- 7.2.3. North America phenolic resins market volume, by application, 2014- 2020 (Kilo Tons)

- 7.2.4. North America phenolic resins market revenue, by application, 2014 - 2020(USD Million)

- 7.2.5. U.S.

- 7.2.5.1. U.S. phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.2.5.2. U.S. phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.2.5.3. U.S. phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.2.5.4. U.S. phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.3. Europe

- 7.3.1. Europe phenolic resins market volume, by product, 2014 - 2020(Kilo Tons)

- 7.3.2. Europe phenolic resins market revenue, by product, 2014 - 2020(USD Million)

- 7.3.3. Europe phenolic resins market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.3.4. Europe phenolic resins market revenue, by application, 2014 – 2020 (USD Million)

- 7.3.5. Germany

- 7.3.5.1. Germany phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.3.5.2. Germany phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.3.5.3. Germany phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.3.5.4. Germany phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.3.6. France

- 7.3.6.1. France phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.3.6.2. France phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.3.6.3. France phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.3.6.4. France phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.3.7. UK

- 7.3.7.1. UK phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.3.7.2. UK phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.3.7.3. UK phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.3.7.4. UK phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific phenolic resins market volume, by product, 2014 - 2020(Kilo Tons)

- 7.4.2. Asia Pacific phenolic resins market revenue, by product, 2014 - 2020(USD Million)

- 7.4.3. Asia Pacific phenolic resins market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.4.4. Asia Pacific phenolic resins market revenue, by application, 2014 – 2020 (USD Million)

- 7.4.5. China

- 7.4.5.1. China phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.4.5.2. China phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.4.5.3. China phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.4.5.4. China phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.4.6. Japan

- 7.4.6.1. Japan phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.4.6.2. Japan phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.4.6.3. Japan phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.4.6.4. Japan phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.4.7. India

- 7.4.7.1. India phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.4.7.2. India phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.4.7.3. India phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.4.7.4. India phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.5. Latin America

- 7.5.1. Latin America phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.5.2. Latin America phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.5.3. Latin America phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.5.4. Latin America phenolic resins market revenue, by application, 2014 - 2020 (USD Million

- 7.5.5. Brazil

- 7.5.5.1. Brazil phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.5.5.2. Brazil phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.5.5.3. Brazil phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.5.5.4. Brazil phenolic resins market revenue, by application, 2014 - 2020 (USD Million)

- 7.6. Middle East and Africa

- 7.6.1. Middle East and Africa phenolic resins market volume, by product, 2014 - 2020 (Kilo Tons)

- 7.6.2. Middle East and Africa phenolic resins market revenue, by product, 2014 - 2020 (USD Million)

- 7.6.3. Middle East and Africa phenolic resins market volume, by application, 2014 - 2020 (Kilo Tons)

- 7.6.4. Middle East and Africa phenolic resins market revenue, by application, 2014 - 2020 (USD Million )

- 7.1. Global phenolic resins market: Regional overview

- Chapter 8. Company Profile

- 8.1. BASF SE

- 8.1.1. Overview

- 8.1.2. Financials

- 8.1.3. Product portfolio

- 8.1.4. Business strategy

- 8.1.5. Recent developments

- 8.2. Georgia Pacific Chemicals LLC

- 8.2.1. Overview

- 8.2.2. Financials

- 8.2.3. Product portfolio

- 8.2.4. Business strategy

- 8.2.5. Recent developments

- 8.3. Chang Chun Plastics Co. Ltd.

- 8.3.1. Overview

- 8.3.2. Financials

- 8.3.3. Product portfolio

- 8.3.4. Business strategy

- 8.3.5. Recent developments

- 8.4. Kolon Industries Inc

- 8.4.1. Overview

- 8.4.2. Financials

- 8.4.3. Product portfolio

- 8.4.4. Business strategy

- 8.4.5. Recent developments

- 8.5. Sumitomo Bakelite Co., Ltd

- 8.5.1. Overview

- 8.5.2. Financials

- 8.5.3. Product portfolio

- 8.5.4. Business strategy

- 8.5.5. Recent developments

- 8.6. SI Group, Inc

- 8.6.1. Overview

- 8.6.2. Financials

- 8.6.3. Product portfolio

- 8.6.4. Business strategy

- 8.6.5. Recent developments

- 8.7. Momentive Specialty Chemicals, Inc.

- 8.7.1. Overview

- 8.7.2. Financials

- 8.7.3. Product portfolio

- 8.7.4. Business strategy

- 8.7.5. Recent developments

- 8.8. Prefere Resins

- 8.8.1. Overview

- 8.8.2. Financials

- 8.8.3. Product portfolio

- 8.8.4. Business strategy

- 8.8.5. Recent developments

- 8.9. Hitachi Chemical Co. Ltd.

- 8.9.1. Overview

- 8.9.2. Financials

- 8.9.3. Product portfolio

- 8.9.4. Business strategy

- 8.9.5. Recent developments

- 8.10. Mitsui Chemicals Inc.

- 8.10.1. Overview

- 8.10.2. Financials

- 8.10.3. Product portfolio

- 8.10.4. Business strategy

- 8.10.5. Recent developments

- 8.11. Sumitomo Bakelite Co., Ltd

- 8.11.1. Overview

- 8.11.2. Financials

- 8.11.3. Product portfolio

- 8.11.4. Business strategy

- 8.11.5. Recent developments

- 8.1. BASF SE

Inquiry For Buying

Phenolic Resins

Request Sample

Phenolic Resins