Polyester Polyols for Flexible Foams Market Size, Share, and Trends Analysis Report

CAGR :

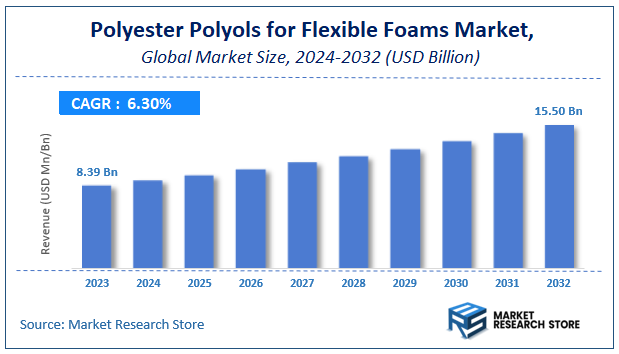

| Market Size 2023 (Base Year) | USD 8.39 Billion |

| Market Size 2032 (Forecast Year) | USD 15.50 Billion |

| CAGR | 6.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Polyester Polyols for Flexible Foams Market Insights

According to Market Research Store, the global polyester polyols for flexible foams market size was valued at around USD 8.39 billion in 2023 and is estimated to reach USD 15.50 billion by 2032, to register a CAGR of approximately 6.3% in terms of revenue during the forecast period 2024-2032.

The polyester polyols for flexible foams report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032

To Get more Insights, Request a Free Sample

Global Polyester Polyols for Flexible Foams Market: Overview

Polyester polyols for flexible foams are key raw materials used in the production of polyurethane foams, which are widely utilized in furniture, bedding, automotive seating, and packaging applications. These polyols are derived from dicarboxylic acids and glycols, offering high resilience, durability, and enhanced mechanical properties compared to polyether-based polyols. Their superior chemical resistance, abrasion resistance, and load-bearing capacity make them suitable for high-performance foam applications.

Key Highlights

- The polyester polyols for flexible foams market is anticipated to grow at a CAGR of 6.3% during the forecast period.

- The global polyester polyols for flexible foams market was estimated to be worth approximately USD 8.39 billion in 2023 and is projected to reach a value of USD 15.50 billion by 2032.

- The growth of the polyester polyols for flexible foams market is being driven by the rising demand for high-quality cushioning materials across multiple industries, particularly in furniture and automotive sectors.

- Based on the type, the polyether polyols segment is growing at a high rate and is projected to dominate the market.

- On the basis of functionality, the conventional polyols segment is projected to swipe the largest market share.

- In terms of processing method, the pouring process segment is expected to dominate the market.

- Based on the application, the furniture segment is expected to dominate the market.

- On the basis of end-user, the consumer goods segment is projected to swipe the largest market share.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Polyester Polyols for Flexible Foams Market: Dynamics

Key Growth Drivers

- Superior Comfort and Durability: Polyester polyols provide excellent resilience, comfort, and durability, making them ideal for flexible foams used in mattresses, furniture, and automotive seating.

- Growing Furniture and Bedding Industry: Increasing demand for comfortable and high-quality foam products in residential and commercial spaces drives market growth.

- Automotive Industry Demand: The use of flexible foams in automotive interiors for seating and cushioning boosts demand for polyester polyols.

- Sustainability Trends: Polyester polyols can be derived from renewable resources, aligning with the global shift toward eco-friendly materials.

Restraints

- High Raw Material Costs: Fluctuations in the prices of raw materials like adipic acid and phthalic anhydride can increase production costs, limiting market growth.

- Competition from Polyether Polyols: Polyether polyols are cheaper and offer better hydrolysis resistance, posing a challenge to polyester polyols in certain applications.

- Processing Challenges: Polyester polyols require precise processing conditions, which can increase manufacturing complexity and costs.

Opportunities

- Emerging Markets: Rapid urbanization and rising disposable incomes in Asia-Pacific and other developing regions create significant growth opportunities.

- Innovation in Bio-based Polyols: Development of bio-based polyester polyols from renewable resources can attract environmentally conscious industries and expand market reach.

- Expanding Automotive Sector: Increasing demand for lightweight and comfortable materials in automotive interiors offers growth potential.

Challenges

- Regulatory Compliance: Stringent environmental and safety regulations may increase production costs and limit market expansion.

- Hydrolysis Sensitivity: Polyester polyols are more susceptible to hydrolysis compared to polyether polyols, which can restrict their use in humid or wet environments.

- Supply Chain Disruptions: Geopolitical issues and raw material shortages can impact production and pricing.

Polyester Polyols for Flexible Foams Market: Report Scope

This report thoroughly analyzes the Polyester Polyols for Flexible Foams Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Polyester Polyols for Flexible Foams Market |

| Market Size in 2023 | USD 8.39 Billion |

| Market Forecast in 2032 | USD 15.50 Billion |

| Growth Rate | CAGR of 6.3% |

| Number of Pages | 150 |

| Key Companies Covered | BASF, DowDuPont, DIC Corporation, Stepan Company, Hunstman, OLEON, Hokoku Corporation, Carpenter, Lyondellbasell, Shell, Sinopec, CNPC, Evonik, Perstorp, INVISTA, AGC Chemicals, Tosoh, Huafeng Group, Shandong Huacheng |

| Segments Covered | By Type, By Application, By Functionality, By End-User, By Processing Method, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Polyester Polyols for Flexible Foams Market: Segmentation Insights

The global polyester polyols for flexible foams market is divided by type, functionality, processing method, application, end-user, and region.

Segmentation Insights by Type

Based on type, the global polyester polyols for flexible foams market is divided into polyester polyols, polyether polyols, and hybrid polyols.

Polyether polyols dominate the polyester polyols for flexible foams market, primarily due to their superior processing characteristics, low viscosity, and excellent hydrolytic stability. These attributes make them the preferred choice for manufacturing flexible polyurethane foams used in bedding, furniture, automotive seating, and packaging. Polyether polyols also offer cost-effectiveness, high resilience, and durability, which further strengthens their demand across various industries. Their compatibility with a broad range of formulations and ability to enhance foam softness and flexibility make them the most widely used type in the market.

Polyester polyols hold the second position in market dominance, mainly due to their excellent mechanical properties, including high tensile strength, abrasion resistance, and chemical stability. These polyols are particularly favored in applications requiring enhanced load-bearing capabilities, such as industrial cushioning and high-resilience foams. However, their higher production cost and susceptibility to hydrolysis compared to polyether polyols limit their widespread adoption in mass-market applications. Despite these challenges, the growing preference for sustainable and bio-based polyester polyols is contributing to their steady demand in specialized applications.

Hybrid polyols, a combination of both polyester and polyether polyols, represent the least dominant segment in this market. They are designed to balance the advantages of both types by offering improved mechanical strength along with better hydrolytic stability. These polyols are used in niche applications that require customized properties, such as high-performance foams and specialty coatings. However, due to their relatively limited adoption and higher formulation complexity, they hold a smaller share compared to pure polyester or polyether polyols.

Segmentation Insights by Functionality

Based on functionality, the global polyester polyols for flexible foams market is divided into conventional polyols, high-performance polyols, and structural polyols.

Conventional polyols dominate the polyester polyols for flexible foams market, primarily due to their widespread use in standard polyurethane foam applications such as bedding, furniture, automotive seating, and packaging. These polyols offer a balance of cost-effectiveness, processability, and mechanical performance, making them the preferred choice for mass-market flexible foams. Their ability to provide good elasticity, resilience, and comfort makes them indispensable in consumer and industrial applications. The well-established production processes and extensive availability further solidify their dominance in the market.

High-performance polyols hold the second-largest market share, driven by their superior properties such as enhanced durability, better load-bearing capacity, and resistance to environmental factors like heat and humidity. These polyols are widely used in applications requiring higher mechanical strength and resilience, such as high-end automotive seating, industrial cushions, and specialty furniture. While they offer significant advantages over conventional polyols, their higher production costs and specialized application requirements limit their adoption to premium and performance-driven segments.

Structural polyols represent the least dominant segment in the market, as their primary function is to provide additional rigidity and support in foam structures. These polyols are used in applications where high load-bearing capacity and dimensional stability are critical, such as rigid or semi-rigid foams used in industrial and construction applications. However, since flexible foam applications primarily require softness and elasticity rather than structural reinforcement, the demand for structural polyols remains limited within this market.

Segmentation Insights by Processing Method

Based on processing method, the global polyester polyols for flexible foams market is divided into pouring process, injection molding, and block molding.

The pouring process is the most dominant segment in the polyester polyols for flexible foams market, primarily due to its simplicity, cost-effectiveness, and widespread use in manufacturing flexible polyurethane foams. This method involves directly pouring liquid polyols into molds or onto a surface, where the foam expands and solidifies. It is widely adopted in industries such as furniture, bedding, and automotive seating, as it allows for the efficient production of large, continuous foam structures with consistent quality. The ability to create customized foam shapes and densities further drives the dominance of this processing method.

Injection molding holds the second-largest market share, as it offers greater precision and efficiency in foam production. This method involves injecting polyester polyol mixtures under controlled pressure into molds, resulting in high-quality foam products with uniform properties. Injection molding is widely used in automotive, medical, and specialty applications where complex shapes and tight tolerances are required. Although this method provides enhanced control over foam characteristics and reduces material waste, its higher equipment costs and longer setup times limit its adoption compared to the pouring process.

Block molding is the least dominant processing method, mainly due to its specialized use in producing large foam blocks that are later cut into desired shapes. This method is often used in the manufacturing of mattress foams, upholstery materials, and packaging solutions. While block molding allows for high-volume production and flexibility in cutting custom foam sizes, its adoption is relatively limited due to the additional processing steps required to shape the final product. Additionally, the inability to produce complex, molded foam parts restrict its application compared to the more versatile pouring and injection molding methods.

Segmentation Insights by Application

On the basis of application, the global polyester polyols for flexible foams market is bifurcated into furniture, automotive, construction, footwear, and packaging.

Furniture is the most dominant application segment in the polyester polyols for flexible foams market, driven by the high demand for polyurethane foams in mattresses, sofas, chairs, and cushions. Polyester polyols provide excellent durability, comfort, and resilience, making them ideal for upholstery and seating applications. The increasing consumer preference for high-quality and ergonomic furniture, coupled with the rising trend of sustainable and eco-friendly foam materials, further strengthens the dominance of this segment.

Automotive follows as the second-largest segment, where polyester polyols are extensively used in car seats, headrests, armrests, and interior padding. The superior mechanical properties of polyester-based flexible foams, such as high load-bearing capacity and resistance to wear and tear, make them well-suited for automotive applications. Additionally, the growing demand for lightweight and energy-efficient vehicles has led to increased use of flexible foams in vehicle interiors, further driving market growth in this sector.

Construction holds the third position, where polyester polyols are used in insulation, soundproofing materials, and cushioning applications. Flexible foams provide excellent thermal and acoustic insulation, making them ideal for residential and commercial buildings. With increasing urbanization and infrastructure development, the demand for high-performance insulation materials is rising, contributing to the steady growth of this segment.

Footwear is another significant but less dominant segment, where polyester polyols are used in shoe soles, insoles, and cushioning materials. The flexibility, shock absorption, and durability of polyester-based foams enhance the comfort and performance of footwear. Although the footwear industry continues to expand, the market size for flexible foams in this application remains smaller compared to furniture and automotive due to the limited material requirements.

Packaging is the least dominant application segment, as flexible polyester polyols are used in protective packaging solutions for fragile goods. While flexible foams provide excellent cushioning and impact resistance, the demand for alternative materials like biodegradable packaging and air-filled plastics has somewhat restricted the market share of polyester-based foams in this segment. However, specialized industries such as electronics and medical devices continue to use these foams for high-value protective packaging applications.

Segmentation Insights by End-User

Based on end-user, the global polyester polyols for flexible foams market is divided into consumer goods, industrial equipment, healthcare, and aerospace.

Consumer goods is the most dominant end-user segment in the polyester polyols for flexible foams market, driven by its extensive use in furniture, bedding, footwear, and packaging. The high demand for polyurethane foams in mattresses, sofas, pillows, and cushions contributes significantly to this segment’s dominance. Additionally, consumer preferences for comfort, durability, and sustainable materials have further propelled the use of polyester-based flexible foams in everyday products. The rising e-commerce sector has also boosted demand for protective packaging solutions, reinforcing the strong market presence of consumer goods.

Industrial equipment follows as the second-largest segment, where flexible foams are used in vibration dampening, insulation, and cushioning for machinery and tools. Polyester polyols contribute to improved durability, impact resistance, and thermal stability, making them essential for industrial applications. The growth of the manufacturing sector and increased focus on worker safety and equipment longevity continue to drive demand in this segment.

Healthcare is a growing yet less dominant segment, where polyester polyols are used in medical cushioning, orthopedic supports, and hospital bedding. Flexible foams provide comfort, pressure relief, and antimicrobial properties, making them ideal for wheelchairs, medical mattresses, and surgical pads. With increasing healthcare investments and advancements in medical-grade foams, this segment is expected to expand, but its market size remains smaller than consumer goods and industrial applications.

Aerospace is the least dominant end-user segment, as the use of polyester polyols in flexible foams is limited to specialized applications such as aircraft seating, interior padding, and insulation. While aerospace foams must meet stringent safety and performance standards, the overall demand remains lower due to the relatively small production volume of aircraft compared to other industries. However, innovations in lightweight and high-performance materials could drive future growth in this niche segment.

Polyester Polyols for Flexible Foams Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific leads the polyester polyols for flexible foams market, driven by rapid industrialization and urbanization. Countries like China and India have witnessed significant growth in end-use industries such as construction, automotive, furniture, electronics, appliances, and packaging, which has propelled the demand for polyester polyols in flexible foam applications. The expanding middle-class population and rising disposable incomes in these countries have further boosted the consumption of flexible foams in furniture and bedding products. Additionally, the automotive industry's shift towards lightweight and energy-efficient materials has increased the adoption of polyester polyols in vehicle interiors, contributing to the region's market dominance.

North America holds a significant share in the global polyester polyols for flexible foams market, primarily due to the well-established automotive and construction industries. The region's demand for polyurethane products, including flexible foams, is driven by the need for lightweight and durable materials in automotive applications to enhance fuel efficiency and meet stringent emission regulations. Moreover, the construction sector's focus on energy-efficient buildings has led to increased use of flexible foams for insulation purposes. The presence of major manufacturers and technological advancements in foam production processes further support market growth in this region.

Europe accounts for a substantial portion of the polyester polyols for flexible foams market, with significant demand stemming from the automotive, construction, and furniture industries. The region's emphasis on sustainability and environmental regulations has prompted manufacturers to develop eco-friendly and bio-based polyester polyols, aligning with the growing trend towards sustainable materials. Additionally, Europe's strong automotive sector, known for its focus on high-quality and durable materials, continues to drive the demand for flexible foams in vehicle interiors, contributing to the market's growth.

Latin America holds a smaller share in the polyester polyols for flexible foams market, with growth primarily driven by the expanding construction and automotive sectors. As countries in this region continue to develop infrastructure and urbanize, the demand for flexible foams in furniture, bedding, and insulation applications is expected to rise. However, economic fluctuations and political instability in certain countries may pose challenges to consistent market growth in this region.

The Middle East and Africa represent the smallest share in the global polyester polyols for flexible foams market. The demand in this region is gradually increasing due to growing construction activities and infrastructural developments, leading to a rise in the use of flexible foams for insulation and furniture applications. However, the market's growth is relatively slower compared to other regions, attributed to economic constraints and limited industrialization in certain areas.

Polyester Polyols for Flexible Foams Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the polyester polyols for flexible foams market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global polyester polyols for flexible foams market include:

- BASF

- DowDuPont

- DIC Corporation

- Stepan Company

- Hunstman

- OLEON

- Hokoku Corporation

- Carpenter

- Lyondellbasell

- Shell

- Sinopec

- CNPC

- Evonik

- Perstorp

- INVISTA

- AGC Chemicals

- Tosoh

- Huafeng Group

- Shandong Huacheng

The global polyester polyols for flexible foams market is segmented as follows:

By Type

- Polyester Polyols

- Polyether Polyols

- Hybrid Polyols

By Functionality

- Conventional Polyols

- High-Performance Polyols

- Structural Polyols

By Processing Method

- Pouring Process

- Injection Molding

- Block Molding

By Application

- Furniture

- Automotive

- Construction

- Footwear

- Packaging

By End-User Industry

- Consumer Goods

- Industrial Equipment

- Healthcare

- Aerospace

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Polyester Polyols for Flexible Foams

Request Sample

Polyester Polyols for Flexible Foams