Polyols Market Size, Share, and Trends Analysis Report

CAGR :

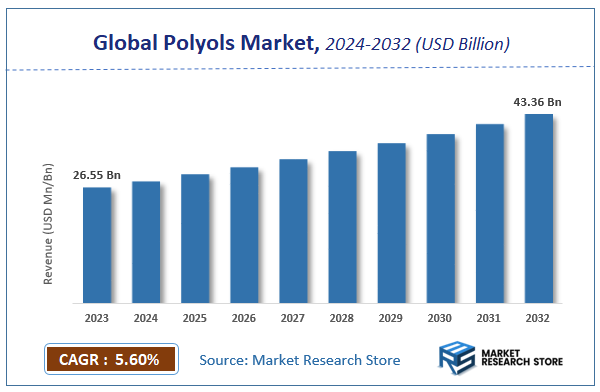

| Market Size 2023 (Base Year) | USD 26.55 Billion |

| Market Size 2032 (Forecast Year) | USD 43.36 Billion |

| CAGR | 5.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Polyols Market Insights

According to Market Research Store, the global polyols market size was valued at around USD 26.55 billion in 2023 and is estimated to reach USD 43.36 billion by 2032, to register a CAGR of approximately 5.6% in terms of revenue during the forecast period 2024-2032.

The polyols report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Polyols Market: Overview

Polyols are a group of organic compounds containing multiple hydroxyl (–OH) functional groups and are primarily classified into two categories: sugar alcohols and polymeric polyols. Sugar alcohols, such as sorbitol, mannitol, and xylitol, are used as low-calorie sweeteners in food and pharmaceutical applications. Polymeric polyols, on the other hand, are key raw materials used in the production of polyurethanes, where they react with isocyanates to form foams, elastomers, adhesives, sealants, and coatings. These polyols can be derived from petrochemical sources (polyether and polyester polyols) or renewable sources (natural oil polyols).

The growth of the polyols market is driven by expanding demand in construction, automotive, furniture, packaging, and footwear industries, where polyurethane-based materials offer durability, insulation, comfort, and flexibility. Increasing consumer preference for energy-efficient buildings and lightweight vehicles is boosting the use of rigid and flexible polyurethane foams.

Key Highlights

- The polyols market is anticipated to grow at a CAGR of 5.6% during the forecast period.

- The global polyols market was estimated to be worth approximately USD 26.55 billion in 2023 and is projected to reach a value of USD 43.36 billion by 2032.

- The growth of the polyols market is being driven by increasing demand across industries such as construction, automotive, furniture, and packaging, primarily due to the rising consumption of polyurethane-based products.

- Based on the product, the polyether segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the rigid foam segment is projected to swipe the largest market share.s

- By region, North America is expected to dominate the global market during the forecast period.

Polyols Market: Dynamics

Key Growth Drivers:

- Soaring Demand for Polyurethane Foams: This is the most significant driver. Polyols are the primary building blocks for polyurethane foams, which are extensively used in rigid foam (for insulation in construction, refrigeration, and appliances) and flexible foam (for furniture, bedding, automotive seating, and packaging). The global push for energy-efficient buildings and increasing comfort demands in consumer goods directly fuel this growth.

- Expansion in Construction and Automotive Industries: The booming construction sector globally, particularly in emerging economies, drives demand for rigid polyols in insulation materials, roofing, and sealants. Concurrently, the automotive industry's focus on lightweighting vehicles for improved fuel efficiency and enhanced safety features (e.g., in seating, dashboards, and interior trim) significantly increases the consumption of flexible polyols.

- Technological Advancements and Product Innovation: Continuous research and development in polyol chemistry lead to the creation of new polyols with enhanced properties, such as improved thermal insulation, better mechanical strength, and increased sustainability. Innovations in catalysts and polymerization methods also enable more efficient and cost-effective production processes, further driving adoption.

- Growing Emphasis on Sustainability and Bio-based Solutions: Increasing environmental regulations and consumer demand for eco-friendly products are pushing the industry towards sustainable polyols. The development and commercialization of bio-based polyols derived from renewable resources like vegetable oils, agricultural waste, and even CO2, offer a significant growth avenue, reducing reliance on petrochemicals and lowering carbon footprints.

Restraints:

- Volatile Raw Material Prices: The production of traditional polyols heavily relies on petrochemical-derived raw materials like propylene oxide and ethylene oxide. Fluctuations in crude oil prices and the supply-demand dynamics of these chemical precursors directly impact the production costs of polyols, leading to price volatility and affecting manufacturers' profit margins.

- Stringent Environmental Regulations on Polyurethane Production: The manufacturing of polyurethane foams and other derivatives using polyols often involves certain hazardous air pollutants (HAPs), such as isocyanates. Strict environmental regulations (e.g., NESHAP in the US, REACH in Europe) concerning emissions, waste disposal, and worker safety impose significant compliance costs and can restrict production processes.

- Health and Safety Concerns Related to Isocyanates: While polyols themselves are generally safe, their reaction partners, isocyanates (especially MDI and TDI), are known sensitizers and can pose health risks if not handled properly. This necessitates rigorous safety protocols, ventilation systems, and personal protective equipment, adding complexity and cost to the polyurethane value chain, indirectly impacting polyol demand.

- Competition from Substitute Materials in Niche Applications: In some specific applications, polyurethanes derived from polyols might face competition from alternative materials like traditional plastics, natural rubber, or other insulation materials, particularly if cost is the overriding factor or specific performance attributes are not critical.

Opportunities:

- Further Development and Commercialization of Bio-based Polyols: The strongest opportunity lies in accelerating the research, development, and mass production of bio-based polyols. As sustainability becomes paramount, polyols derived from renewable sources offer a significant competitive advantage and cater to a growing market segment actively seeking greener alternatives.

- Expansion into Emerging and High-Value Applications: Polyols are finding new applications in high-growth sectors such as electric vehicles (for lightweighting, battery insulation), advanced electronics (for specialized coatings and encapsulants), and medical devices (for biocompatible foams and films). These niche, high-value applications offer significant revenue potential.

- Innovation in Functional and Specialty Polyols: Opportunities exist in developing highly specialized polyols that impart unique functionalities to the final polyurethane product, such as enhanced flame retardancy, improved antimicrobial properties, specific adhesion characteristics, or tailored viscoelasticity for advanced materials.

- Growth of Polyols in Adhesives, Sealants, and Coatings (CASE): The demand for high-performance adhesives, sealants, and coatings in the construction, automotive, and general industrial sectors is steadily rising. Polyols play a crucial role in enhancing the durability, flexibility, and adhesion properties of these CASE applications, creating significant growth opportunities.

Challenges:

- Achieving Cost-Competitiveness for Sustainable Polyols: While bio-based polyols offer environmental benefits, a major challenge is to achieve cost-effectiveness and performance parity with conventional petroleum-based polyols, especially at large production scales. High feedstock costs or complex processing can hinder widespread adoption.

- Managing Supply Chain Disruptions and Geopolitical Risks: The global nature of the polyols market means it is susceptible to disruptions in the supply chain of key raw materials due to geopolitical tensions, trade policies, or unforeseen global events, which can impact production schedules and profitability.

- Navigating Complex and Evolving Regulatory Landscapes: Staying compliant with the constantly evolving and increasingly stringent global regulations concerning chemical safety, environmental emissions, and product labeling for both polyols and their polyurethane derivatives is a continuous and complex challenge, requiring significant investment in regulatory affairs.

- Maintaining Product Performance Amidst Innovation: As manufacturers innovate with new formulations and sustainable alternatives, a critical challenge is to ensure that these new products consistently meet or exceed the performance expectations of end-users who rely on the well-established properties of traditional polyol-based polyurethanes.

Polyols Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Polyols Market |

| Market Size in 2023 | USD 26.55 Billion |

| Market Forecast in 2032 | USD 43.36 Billion |

| Growth Rate | CAGR of 5.6% |

| Number of Pages | 140 |

| Key Companies Covered | BASF SE, Mitsui Chemicals, Inc., Bayer AG, Chemtura Corporation, COIM S.P.A., Royal Dutch Shell PLC, Cargill Incorporated, Dow Chemicals, Emery Oleochemicals and Invista B.V. |

| Segments Covered | By Product, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Polyols Market: Segmentation Insights

The global polyols market is divided by product, application, and region.

Based on product, the global polyols market is divided into polyether and polyester. Polyether dominates the polyols market due to its broad application base, cost-efficiency, and favorable physical properties that align with the manufacturing needs of flexible foams and elastomers. Derived primarily from propylene oxide and ethylene oxide, polyether polyols are widely used in the production of flexible polyurethane foams, which find extensive use in furniture, mattresses, automotive seating, and packaging materials. Their advantages include excellent reactivity, consistent performance, low viscosity, and good water solubility. Polyether polyols are also preferred for their superior hydrolytic stability and ease of processing, making them ideal for high-throughput industrial manufacturing. Additionally, their compatibility with various blowing agents and additives enhances their utility in insulation and cushioning applications across commercial and consumer goods.

On the basis of application, the global polyols market is bifurcated into rigid foam, flexible foam, coatings, adhesives & sealants, elastomers, and other applications. Rigid Foam dominates the polyols market, primarily due to its extensive use in insulation applications across construction, refrigeration, and industrial sectors. Rigid polyurethane foams, made using polyols particularly polyether and polyester types are known for their excellent thermal insulation, dimensional stability, and low moisture permeability. These characteristics make them essential for building insulation panels, roofing systems, and refrigeration units. The increasing emphasis on energy efficiency in buildings and appliances has driven significant demand for rigid foams, further solidifying their dominance in the polyols landscape. Their high strength-to-weight ratio and thermal resistance make them indispensable in achieving compliance with green building standards and energy codes.

Polyols Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the polyols market, driven by strong demand across key industries including automotive, construction, furniture, and packaging. The United States leads regional consumption, with polyether and polyester polyols extensively used in the production of flexible and rigid polyurethane foams for insulation panels, automotive interiors, sealants, and coatings. Rising energy efficiency regulations have significantly boosted demand for polyurethane-based thermal insulation materials in commercial and residential buildings. The region also benefits from the availability of key feedstocks such as propylene oxide and a mature petrochemical infrastructure. In the furniture sector, flexible foams derived from polyols are widely used in bedding, cushions, and upholstery. Canada contributes to regional demand, particularly in green building materials and high-performance coatings, with increased emphasis on sustainability and bio-based polyols.

Europe holds a significant share in the polyols market, supported by stringent energy efficiency standards, sustainability regulations, and advanced manufacturing technologies. Germany, the UK, France, and Italy are major consumers, using polyols in construction insulation, automotive lightweighting, and consumer comfort applications. The European Green Deal and REACH regulations have accelerated the shift toward bio-based and low-emission polyol products. Demand is particularly strong for rigid foams in cold chain logistics, energy-efficient building panels, and appliances. Europe is also investing in circular economy strategies, promoting the development of recyclable polyurethane foams and renewable polyols derived from natural oils and carbon dioxide. The presence of key global chemical producers and advanced R&D facilities supports continuous innovation in high-performance polyol systems.

Asia-Pacific is the fastest-growing region in the polyols market, driven by rapid industrialization, population growth, and urban development. China dominates regional consumption and production, using polyols in furniture, construction, automotive parts, footwear, and electronics. The country’s expanding infrastructure and real estate sectors demand large volumes of rigid polyurethane foams for insulation and protective coatings. India shows rising demand for polyols in packaging and flexible foams used in mattresses and consumer products. Southeast Asian countries such as Indonesia, Thailand, and Vietnam are also experiencing growing demand in automotive and appliance manufacturing. Japan and South Korea focus on specialty polyols for high-performance electronics, adhesives, and coatings. Abundant availability of feedstock and low production costs make the region a global export hub for polyols and polyurethane precursors.

Latin America is an emerging market for polyols, with Brazil and Mexico being the primary contributors. In Brazil, polyols are used extensively in automotive interiors, refrigeration insulation, footwear soles, and bedding applications. Mexico supports regional demand through its growing manufacturing and construction industries, where flexible and rigid foams are increasingly adopted. The market is supported by gradual economic recovery and foreign direct investment in local production. However, challenges such as volatility in raw material prices and limited technological capabilities affect large-scale adoption. Rising interest in sustainable and bio-based polyols—particularly in response to environmental concerns—is likely to shape the market in the coming years.

Middle East & Africa are developing markets for polyols, with increasing demand in construction, refrigeration, automotive, and footwear applications. In the Middle East, the UAE and Saudi Arabia are investing in infrastructure and smart city projects, which boost demand for rigid polyurethane insulation panels. The region’s hot climate has intensified the need for energy-efficient building materials, driving the use of high-performance polyols. In Africa, South Africa leads demand for flexible polyurethane foams in furniture and bedding, while Nigeria and Kenya show growth in footwear manufacturing. Despite the market’s potential, factors such as limited domestic production, reliance on imports, and underdeveloped regulatory frameworks pose challenges. Nonetheless, increasing industrialization and urban expansion offer long-term growth opportunities.

Polyols Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the polyols market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global polyols market include:

- BASF SE

- Mitsui Chemicals, Inc.

- Bayer AG

- Chemtura Corporation

- Cargill Incorporated

- Dow Chemicals

- Emery Oleochemicals

- Invista B.V.

- Covestro AG

- Shell Plc

- Huntsman International LLC

- Coim USA Inc

- Stephan Company

- Palmer Holland, Inc

The global polyols market is segmented as follows:

By Product

- Polyether

- Polyester

By Application

- Rigid Foam

- Flexible Foam

- Coatings

- Adhesives & Sealants

- Elastomers

- Other Applications

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

Chapter 2. Executive Summary

- 2.1. Global polyols market, 2014 - 2020 (Kilo Tons) (USD Million)

- 2.2. Global polyols market : Snapshot

Chapter 3. Polyols– Market Dynamics

- 3.1. Introduction

- 3.2. Value chain analysis

- 3.3. Market drivers

- 3.3.1. Global polyols market drivers: Impact analysis

- 3.3.2. Increasing demand from refrigerator and freezer manufacturers

- 3.4. Market restraints

- 3.4.1. Global polyols market restraints: Impact analysis

- 3.4.2. Raw material price volatility

- 3.5. Opportunities

- 3.5.1. Increasing demand and production of bio-based polyols

- 3.6. Porter’s five forces analysis

- 3.6.1. Bargaining power of suppliers

- 3.6.2. Bargaining power of buyers

- 3.6.3. Threat from new entrants

- 3.6.4. Threat from new substitutes

- 3.6.5. Degree of competition

- 3.7. Market attractiveness analysis

- 3.7.1. Market attractiveness analysis, by product segment

- 3.7.2. Market attractiveness analysis, by application segment

- 3.7.3. Market attractiveness analysis, by regional segment

Chapter 4. Global Polyols Market – Competitive Landscape

- 4.1. Company market share, 2014

- 4.2. Price trend analysis

Chapter 5. Global Polyols Market – Product Segment Analysis

- 5.1. Global polyols market: Product overview

- 5.1.1. Global polyols market, by product, 2014 and 2020

- 5.2. Polyester polyol

- 5.2.1. Global polyester polyol market, 2014 – 2020 (Kilo Tons) (USD Million)

- 5.3. Polyether polyol

- 5.3.1. Global polyether polyol market, 2014 – 2020 (Kilo Tons) (USD Million)

Chapter 6. Global Polyols Market – Application Segment Analysis

- 6.1. Global polyols market: Application overview

- 6.1.1. Global polyols market, by application, 2014 and 2020

- 6.2. Rigid Foam

- 6.2.1. Global polyols market for rigid foam, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.3. Flexible Foam

- 6.3.1. Global polyols market for flexible foam, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.4. Coatings

- 6.4.1. Global polyols market for Coatings, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.5. Adhesives

- 6.5.1. Global polyols market for Adhesives, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.6. Sealants

- 6.6.1. Global polyols market for Sealants, 2014 – 2020 (Kilo Tons) (USD Million)

- 6.7. Elastomers

- 6.7.1. Global polyols market for Elastomers, 2014 – 2020 (Kilo Tons) (USD Million)

Chapter 7. Global Polyols Market – Regional Segment Analysis

- 7.1. Global polyols market: Regional overview

- 7.1.1. Global polyols market, by region, 2014 and 2020

- 7.2. North America

- 7.2.1. North America polyols market volume, by product, 2014 – 2020, (Kilo Tons)

- 7.2.2. North America polyols market revenue, by product, 2014 – 2020, (USD Million)

- 7.2.3. North America polyols market volume, by application, 2014 – 2020, (Kilo Tons)

- 7.2.4. North America polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.2.5. U.S.

- 7.2.5.1. U.S. polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.2.5.2. U.S. polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.2.5.3. U.S. polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.2.5.4. U.S. polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.3. Europe

- 7.3.1. Europe polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.3.2. Europe polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.3. Europe polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.3.4. Europe polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.3.5. Germany

- 7.3.5.1. Germany polyols market volume, by product, 2014 – 2020, (Kilo Tons)

- 7.3.5.2. Germany polyols market revenue, by product, 2014 – 2020, (USD Million)

- 7.3.5.3. Germany polyols market volume, by application, 2014 – 2020, (Kilo Tons)

- 7.3.5.4. Germany polyols market revenue, by application, 2014 – 2020, (USD Million)

- 7.3.6. France

- 7.3.6.1. France polyols market volume, by product, 2014 – 2020, (Kilo Tons)

- 7.3.6.2. France polyols market revenue, by product, 2014 – 2020, (USD Million)

- 7.3.6.3. France polyols market volume, by application, 2014 – 2020, (Kilo Tons)

- 7.3.6.4. France polyols market revenue, by application, 2014 – 2020, (USD Million)

- 7.3.7. UK

- 7.3.7.1. UK polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.3.7.2. UK polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.7.3. UK polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.3.7.4. UK polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.4.2. Asia Pacific polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.3. Asia Pacific polyols market volume, by application, 2014 – 2020, (Kilo Tons)

- 7.4.4. Asia Pacific polyols market revenue, by application, 2014 – 2020, (USD Million)

- 7.4.5. China

- 7.4.5.1. China polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.4.5.2. China polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.5.3. China polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.4.5.4. China polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.4.6. Japan

- 7.4.6.1. Japan polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.4.6.2. Japan polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.6.3. Japan polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.4.6.4. Japan polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.4.7. India

- 7.4.7.1. India polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.4.7.2. India polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.7.3. India polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.4.7.4. India polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.5. Latin America

- 7.5.1. Latin America polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.5.2. Latin America polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.3. Latin America polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.5.4. Latin America polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.5.5. Brazil

- 7.5.5.1. Brazil polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.5.5.2. Brazil polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.5.3. Brazil polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.5.5.4. Brazil polyols market revenue, by application, 2014 – 2020 (USD Million)

- 7.6. Middle East and Africa

- 7.6.1. Middle East and Africa polyols market volume, by product, 2014 – 2020 (Kilo Tons)

- 7.6.2. Middle East and Africa polyols market revenue, by product, 2014 – 2020 (USD Million)

- 7.6.3. Middle East and Africa polyols market volume, by application, 2014 – 2020 (Kilo Tons)

- 7.6.4. Middle East and Africa polyols market revenue, by application, 2014 – 2020 (USD Million)

Chapter 8. Company Profile

- 8.1. BASF SE

- 8.1.1. Overview

- 8.1.2. Financials

- 8.1.3. Product portfolio

- 8.1.4. Business strategy

- 8.1.5. Recent developments

- 8.2. Mitsui Chemicals, Inc.

- 8.2.1. Overview

- 8.2.2. Financials

- 8.2.3. Product portfolio

- 8.2.4. Business strategy

- 8.2.5. Recent developments

- 8.3. Bayer AG

- 8.3.1. Overview

- 8.3.2. Financials

- 8.3.3. Product portfolio

- 8.3.4. Business strategy

- 8.3.5. Recent developments

- 8.4. Chemtura Corporation

- 8.4.1. Overview

- 8.4.2. Financials

- 8.4.3. Product portfolio

- 8.4.4. Business strategy

- 8.4.5. Recent developments

- 8.5. COIM S.P.A.

- 8.5.1. Overview

- 8.5.2. Financials

- 8.5.3. Product portfolio

- 8.5.4. Business strategy

- 8.5.5. Recent developments

- 8.6. Royal Dutch Shell PLC

- 8.6.1. Overview

- 8.6.2. Financials

- 8.6.3. Product portfolio

- 8.6.4. Business strategy

- 8.6.5. Recent developments

- 8.7. Cargill Incorporated

- 8.7.1. Overview

- 8.7.2. Financials

- 8.7.3. Product portfolio

- 8.7.4. Business strategy

- 8.7.5. Recent developments

- 8.8. Dow Chemicals

- 8.8.1. Overview

- 8.8.2. Financials

- 8.8.3. Product portfolio

- 8.8.4. Business strategy

- 8.8.5. Recent developments

- 8.9. Emery Oleochemicals

- 8.9.1. Overview

- 8.9.2. Financials

- 8.9.3. Product portfolio

- 8.9.4. Business strategy

- 8.9.5. Recent developments

- 8.10. Invista B.V.

- 8.10.1. Overview

- 8.10.2. Financials

- 8.10.3. Product portfolio

- 8.10.4. Business strategy

- 8.10.5. Recent developments

Inquiry For Buying

Polyols

Request Sample

Polyols