PV Pumping System for Water Market Size, Share, and Trends Analysis Report

CAGR :

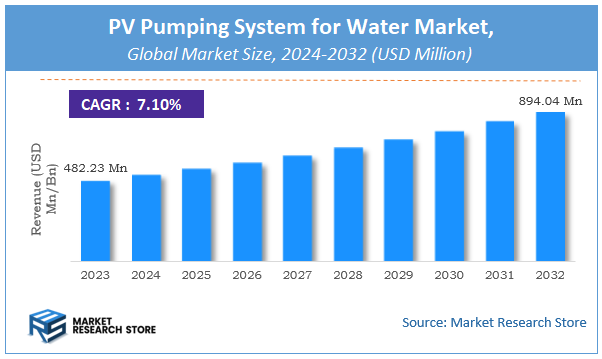

| Market Size 2023 (Base Year) | USD 482.23 Million |

| Market Size 2032 (Forecast Year) | USD 894.04 Million |

| CAGR | 7.1% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

PV Pumping System for Water Market Insights

According to Market Research Store, the global pv pumping system for water market size was valued at around USD 482.23 million in 2023 and is estimated to reach USD 894.04 million by 2032, to register a CAGR of approximately 7.1% in terms of revenue during the forecast period 2024-2032.

The pv pumping system for water report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global PV Pumping System for Water Market: Overview

The PV (Photovoltaic) pumping system for water is a solar-powered water pumping solution that utilizes energy from photovoltaic panels to operate pumps for drawing water from sources such as wells, rivers, or reservoirs. These systems are especially valuable in remote and off-grid areas where access to electricity is limited or unreliable. The core components typically include solar panels, a pump (either submersible or surface), a controller/inverter, and a water storage unit. The system converts solar radiation into electrical energy, which powers the pump to lift or move water for agricultural irrigation, livestock watering, and domestic use.

Key Highlights

- The PV pumping system for water market is anticipated to grow at a CAGR of 7.1% during the forecast period.

- The global PV pumping system for water market was estimated to be worth approximately USD 482.23 million in 2023 and is projected to reach a value of USD 894.04 million by 2032.

- The growth of the PV pumping system for water market is being driven by the rising global demand for sustainable and cost-effective water solutions.

- Based on the product type, the submersible pumps segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the agriculture segment is projected to swipe the largest market share.

- In terms of power rating, the 3.1 to 10 HP segment is expected to dominate the market.

- Based on the distribution channel, the offline segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

PV Pumping System for Water Market: Dynamics

Key Growth Drivers:

- Rising Demand for Sustainable Irrigation: Agriculture accounts for a large portion of water usage globally, and farmers are increasingly adopting PV pumping systems as a cost-effective and eco-friendly alternative to diesel or electric pumps.

- Government Support & Subsidies: Various countries, especially in Asia and Africa, are offering financial incentives and subsidy programs to promote solar-powered irrigation systems.

- Declining Cost of Solar Components: Continuous reduction in the prices of photovoltaic panels and inverters has made solar pumping systems more affordable and accessible to rural and remote communities.

- High Solar Potential in Emerging Markets: Regions with abundant sunlight such as South Asia, Sub-Saharan Africa, and the Middle East are ideal for deploying PV pumping systems, driving adoption in off-grid zones.

Restraints:

- High Initial Installation Cost: Despite lower operational costs, the upfront capital investment for PV pumping systems remains a barrier, especially for small-scale farmers without access to credit or financing.

- Limited Awareness and Technical Know-How: In many developing regions, end-users lack awareness about the long-term benefits of solar pumps and often face difficulty in operating and maintaining the systems.

- Dependence on Weather Conditions: Solar-powered pumps rely heavily on sunlight, and performance can be affected during cloudy days or monsoon seasons, limiting their reliability in certain regions.

Opportunities:

- Integration with Smart Technologies: Combining PV pumping systems with IoT, remote monitoring, and smart sensors can improve water use efficiency, attract commercial users, and expand market scope.

- Untapped Rural and Agricultural Markets: Many remote areas still depend on manual or diesel pumping methods. Introducing solar alternatives in these regions presents a vast opportunity for market expansion.

- Private Sector and NGO Collaboration: Partnerships with micro-financing institutions, agritech firms, and NGOs can boost outreach, funding, and training programs, accelerating adoption across underserved regions.

Challenges:

- Lack of Standardization and Regulation: The absence of standardized system designs, quality certifications, and regulatory frameworks in some markets can lead to unreliable systems and reduced user trust.

- Logistical and Infrastructure Barriers: In remote regions, transporting solar equipment and providing maintenance services can be logistically complex and costly, hindering widespread deployment.

- Financing and Credit Accessibility: Many farmers or rural households face challenges in accessing affordable loans or financial schemes to invest in PV systems, delaying market growth despite demand.

PV Pumping System for Water Market: Report Scope

This report thoroughly analyzes the PV Pumping System for Water Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | PV Pumping System for Water Market |

| Market Size in 2023 | USD 482.23 Million |

| Market Forecast in 2032 | USD 894.04 Million |

| Growth Rate | CAGR of 7.1% |

| Number of Pages | 177 |

| Key Companies Covered | Lorentz GmbH, Grundfos, Tata Power Solar Systems Ltd., Shakti Pumps (India) Ltd., Dankoff Solar Pumps, SunEdison, Bright Solar Limited, Solar Power & Pump Co., LLC, Greenmax Technology, JNTech Renewable Energy Co., Ltd., CRI Pumps Pvt. Ltd., Bernt Lorentz GmbH & Co. KG, Symtech Solar, Solar Pumping Solutions Australia, Mono Pumps Limited, American West Windmill & Solar Company, Advanced Power Inc., Solar Water Solutions Ltd., Solar Pumping Pty Ltd., SunCulture |

| Segments Covered | By Product Type, By Application, By Power Rating, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

PV Pumping System for Water Market: Segmentation Insights

The global PV pumping system for water market is divided by product type, application, power rating, distribution channel, and region.

Segmentation Insights by Product Type

Based on product type, the global PV pumping system for water market is divided into surface pumps and submersible pumps.

In the PV pumping system for water market, submersible pumps are the most dominant segment, owing to their efficiency and suitability for deep water extraction. These pumps are installed underwater, typically in wells or boreholes, and are ideal for applications requiring high water lifts and consistent water supply. Submersible pumps are widely used in agricultural irrigation and rural drinking water projects, especially in areas with deep water tables. Their ability to operate efficiently in varying water depths without the risk of cavitation gives them an edge over surface pumps, making them a preferred choice for large-scale and remote installations.

Surface pumps, while less dominant, are still vital in the PV pumping market, particularly in areas where the water source is shallow or on the surface, such as rivers, lakes, or storage tanks. These pumps are installed above the water source and are easier to maintain and repair compared to submersible variants. They are commonly used for small-scale irrigation, livestock watering, and garden applications. Surface pumps are generally more affordable and simpler to install, making them a practical choice for low-lift water transfer in residential or community-based applications. However, their limited applicability in deep water scenarios keeps their market share below that of submersible pumps.

Segmentation Insights by Application

On the basis of application, the global PV pumping system for water market is bifurcated into agriculture, drinking water, industrial, and others.

In the PV pumping system for water market, agriculture stands out as the most dominant application segment, primarily driven by the increasing need for sustainable irrigation solutions in remote and off-grid areas. Solar-powered pumps provide a reliable and cost-effective method for irrigating fields, especially in regions with limited access to electricity. Farmers in developing countries are increasingly adopting PV pumping systems to reduce reliance on diesel pumps, minimize operational costs, and ensure consistent water availability throughout growing seasons.

Drinking water is the second most significant application, particularly in rural and underserved communities where centralized water supply infrastructure is lacking. PV pumping systems offer an efficient way to extract groundwater or surface water for domestic use, ensuring clean water access while reducing dependence on grid electricity or manual effort. These systems are often implemented by governments or NGOs as part of rural development and public health initiatives.

Industrial applications of PV water pumping systems are growing steadily, although they represent a smaller share of the market. Industries that require water for processing, cooling, or cleaning purposes, particularly in remote areas or operations like mining and construction, are exploring solar pumps to reduce energy costs and improve sustainability. However, high water demand and operational complexities limit the widespread adoption of solar pumps in heavy industries.

Segmentation Insights by Power Rating

Based on power rating, the global PV pumping system for water market is divided into up to 3 hp, 3.1 to 10 hp, and above 10 hp.

In the PV pumping system for water market, the 3.1 to 10 HP power rating segment holds the dominant position due to its versatility and suitability for medium- to large-scale agricultural and community water supply applications. Pumps in this range are capable of handling significant water volumes and lifting depths, making them ideal for irrigation of large fields, multi-user rural water supply systems, and livestock watering. Their balance between performance and energy consumption makes them the preferred choice for users seeking efficiency without the complexity or cost of high-capacity systems.

The Up to 3 HP segment is also significant, particularly in small-scale farming, household water supply, and low-lift irrigation applications. These systems are typically more affordable and easier to install, making them attractive for individual farmers, small communities, and residential users. They are ideal for shallow wells or surface water sources and are commonly used in garden irrigation, small vegetable farms, and livestock pens. This segment benefits from widespread adoption in rural areas where budget constraints and lower water demand are key considerations.

The Above 10 HP segment, while less dominant, plays a crucial role in high-demand applications such as large commercial farms, deep borewell operations, and industrial water supply. These high-capacity systems require more robust PV setups and are generally more expensive, limiting their adoption to projects with substantial funding or specific technical needs. However, as solar technology continues to improve and component costs decline, this segment is expected to witness gradual growth in regions with intensive agricultural operations and large-scale water management projects.

Segmentation Insights by Distribution Channel

On the basis of distribution channel, the global PV pumping system for water market is bifurcated into online and offline.

In the PV pumping system for water market, the offline distribution channel is the most dominant segment, largely due to the technical nature of the product and the preference for physical consultation and support during the purchasing process. Customers—particularly farmers, rural households, and government agencies—tend to favor offline channels such as authorized dealers, distributors, and local installers. These channels offer the advantage of in-person demonstrations, site evaluations, installation services, and after-sales support, which are critical for ensuring proper system performance and reliability. Additionally, government-led subsidy programs and procurement tenders often work through offline networks, further strengthening this channel’s dominance.

The online distribution channel, while still emerging, is gaining momentum, especially in urban and semi-urban regions where internet penetration is higher. E-commerce platforms and company websites now offer solar pumping systems, spare parts, and accessories, making it easier for tech-savvy users to research and purchase systems remotely. The online channel provides convenience, wider product selection, and price transparency. However, the lack of hands-on assistance and technical guidance has limited its uptake among less experienced or rural users. As digital literacy and trust in e-commerce continue to improve, the online segment is expected to expand, particularly among small business owners and younger farmers seeking quick and accessible solutions.

PV Pumping System for Water Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific (APAC) region dominates the PV pumping system for water market, driven by the vast agricultural base and a strong push for rural electrification through renewable energy in countries like India, China, and Bangladesh. Government incentives, such as subsidies for solar pumps under schemes like India’s KUSUM program, have significantly accelerated adoption. The region also benefits from high solar irradiance and increasing demand for sustainable irrigation solutions, especially in water-stressed areas. Moreover, rapid industrialization and the need to ensure clean water access in off-grid regions further fuel the growth of PV pumping systems across APAC.

Middle East and Africa (MEA) follows as the second most prominent region in the market due to abundant solar resources and a critical need for water management solutions in arid and semi-arid zones. Countries such as Saudi Arabia, UAE, South Africa, and Kenya are increasingly investing in solar-powered infrastructure to reduce dependency on fossil fuels and address water scarcity. In rural Africa, international development projects and government-backed solar initiatives are enabling the deployment of PV pumping systems for agricultural and drinking water purposes, supporting both community development and environmental sustainability.

Latin America is emerging as a strong market for PV water pumping systems, particularly in countries like Brazil, Mexico, and Chile. The region faces challenges related to water distribution and rural electrification, which solar pumps can effectively address. With favorable solar conditions and increasing investments in clean energy technologies, the demand for solar-powered pumps is steadily rising. Latin American governments are also introducing policies to support off-grid solar solutions, promoting their use in remote farming communities for irrigation and livestock watering.

Europe holds a moderate share in the market, with countries such as Spain, Italy, and Greece adopting PV pumping systems primarily for sustainable agriculture and climate adaptation. Although Europe has strong grid infrastructure, the rising environmental consciousness and policy-driven support for renewable energy integration in farming practices have created a niche demand for solar pumps. The region’s commitment to reducing carbon emissions under EU regulations also supports the use of clean technologies like PV pumping systems.

North America exhibits steady but comparatively lower market penetration. The United States and parts of Canada have seen a rise in the adoption of solar water pumping systems in agriculture, particularly in drought-prone areas. However, the dominance of traditional electric and fuel-based pump systems, combined with a highly electrified rural infrastructure, has limited broader adoption. Nonetheless, growing sustainability awareness and incentives for renewable energy in agriculture are gradually boosting market growth in specific sectors and regions.

PV Pumping System for Water Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the PV pumping system for water market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global PV pumping system for water market include:

- Lorentz GmbH

- Grundfos

- Tata Power Solar Systems Ltd.

- Shakti Pumps (India) Ltd.

- Dankoff Solar Pumps

- SunEdison

- Bright Solar Limited

- Solar Power & Pump Co. LLC

- Greenmax Technology

- JNTech Renewable Energy Co. Ltd.

- CRI Pumps Pvt. Ltd.

- Bernt Lorentz GmbH & Co. KG

- Symtech Solar

- Solar Pumping Solutions Australia

- Mono Pumps Limited

- American West Windmill & Solar Company

- Advanced Power Inc.

- Solar Water Solutions Ltd.

- Solar Pumping Pty Ltd.

- SunCulture

The global PV pumping system for water market is segmented as follows:

By Product Type

- Surface Pumps

- Submersible Pumps

By Application

- Agriculture

- Drinking Water

- Industrial

- Others

By Power Rating

- Up to 3 HP

- 3.1 to 10 HP

- Above 10 HP

By Distribution Channel

- Online

- Offline

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

PV Pumping System for Water

Request Sample

PV Pumping System for Water