Radiator Grilles Market Size, Share, and Trends Analysis Report

CAGR :

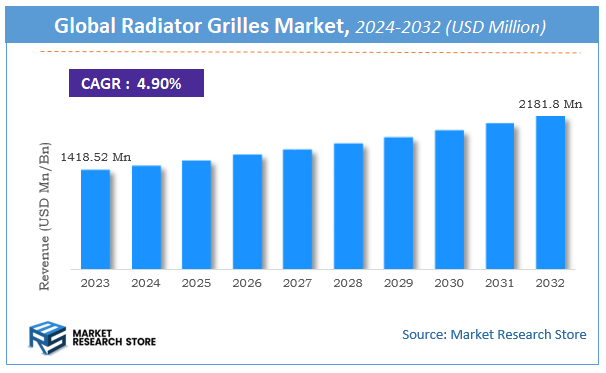

| Market Size 2023 (Base Year) | USD 1418.52 Million |

| Market Size 2032 (Forecast Year) | USD 2181.8 Million |

| CAGR | 4.9% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Radiator Grilles Market Insights

According to Market Research Store, the global radiator grilles market size was valued at around USD 1418.52 million in 2023 and is estimated to reach USD 2181.8 million by 2032, to register a CAGR of approximately 4.9% in terms of revenue during the forecast period 2024-2032.

The radiator grilles report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Radiator Grilles Market: Overview

Radiator grilles are critical automotive components mounted at the front of vehicles, primarily designed to allow air to flow into the engine compartment to maintain optimal engine temperatures. Besides their functional role in cooling, radiator grilles contribute significantly to the vehicle’s aesthetic appeal, serving as a prominent design element that often reflects brand identity. Grilles are manufactured using materials such as aluminum, ABS plastic, stainless steel, and carbon fiber, depending on durability and design preferences. Their design can vary from classic slatted patterns to intricate mesh or geometric styles, depending on the vehicle category—ranging from passenger cars to commercial trucks and luxury automobiles.

Key Highlights

- The radiator grilles market is anticipated to grow at a CAGR of 4.9% during the forecast period.

- The global radiator grilles market was estimated to be worth approximately USD 1418.52 million in 2023 and is projected to reach a value of USD 2181.8 million by 2032.

- The growth of the radiator grilles market is being driven by increasing demand for automotive personalization, advancements in lightweight materials, and the growing focus on vehicle aesthetics and aerodynamics.

- Based on the material type, the plastic segment is growing at a high rate and is projected to dominate the market.

- On the basis of vehicle type, the passenger cars segment is projected to swipe the largest market share.

- In terms of design style, the modern grilles segment is expected to dominate the market.

- Based on the manufacturing process, the injection molding segment is expected to dominate the market.

- In terms of end-user, the OEM (original equipment manufacturer) segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Radiator Grilles Market: Dynamics

Key Growth Drivers:

- Increasing Vehicle Production Worldwide: Rising demand for passenger and commercial vehicles, especially in emerging economies, is directly driving the demand for radiator grilles as a standard vehicle component.

- Growing Popularity of Aesthetic and Customizable Auto Parts: Consumers are increasingly seeking personalized vehicles, and radiator grilles are a prominent feature for visual enhancement, boosting demand for customized and stylish grille designs.

- Advancements in Material Technology: The development of lightweight, durable, and corrosion-resistant materials like ABS plastic and aluminum is enabling the production of high-performance radiator grilles.

- Rising Demand for Electric and Hybrid Vehicles: As EV manufacturers strive to improve aerodynamics and brand identity, uniquely styled grilles are being integrated into vehicle designs, especially for cooling and brand differentiation.

- Expansion of the Automotive Aftermarket: A growing aftermarket industry allows consumers to replace or upgrade radiator grilles, fueling continuous demand beyond initial vehicle sales.

Restraints:

- High Cost of Advanced Grille Materials and Designs: Premium materials and intricate grille designs often come with high manufacturing costs, which can limit adoption, especially in price-sensitive markets.

- Design Complexity and Compatibility Issues: The increasing complexity in grille designs and the need for vehicle-specific fittings can pose challenges in manufacturing and aftermarket applications.

- Fluctuating Raw Material Prices: Volatility in prices of key raw materials like plastics and metals can increase production costs, affecting profitability for grille manufacturers.

Opportunities:

- Growth in Luxury and Premium Vehicle Segments: Luxury carmakers place significant emphasis on front-end styling, creating strong demand for high-end, branded radiator grilles with distinctive aesthetics.

- Integration of Smart and Active Grilles: The emergence of active grille shutters and smart grilles that improve aerodynamics and thermal management offers innovation opportunities for OEMs and suppliers.

- Expansion into Emerging Markets: Automotive production and sales are rising in regions like Southeast Asia, Africa, and Latin America, presenting lucrative growth prospects for grille manufacturers.

- Collaborations and OEM Partnerships: Strategic alliances between grille manufacturers and automotive OEMs can lead to long-term supply contracts and co-development of proprietary designs.

Challenges:

- Rising Shift Toward Grille-Less Designs in EVs: Some EV manufacturers are opting for closed-front or grille-less vehicle designs, which could reduce demand for traditional radiator grilles.

- Stringent Environmental Regulations: Regulations aimed at reducing emissions and improving fuel efficiency may impact grille design, particularly with regard to weight and aerodynamics.

- Supply Chain Disruptions: Global disruptions in logistics and raw material supply chains can delay production and inflate costs, impacting overall market growth.

- Intense Market Competition: The presence of numerous global and regional players creates pricing pressure and forces manufacturers to continuously innovate to stay competitive.

Radiator Grilles Market: Report Scope

This report thoroughly analyzes the Radiator Grilles Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Radiator Grilles Market |

| Market Size in 2023 | USD 1418.52 Million |

| Market Forecast in 2032 | USD 2181.8 Million |

| Growth Rate | CAGR of 4.9% |

| Number of Pages | 161 |

| Key Companies Covered | Magna Inteational, Plastic Omnium, Toyoda Gosei, SRG Global, Lacks Enterprises, Sakae Riken Kogyo, Samshin Chemicals, Faltec, Shanghai Ruier Industrial, Changchun Faway Automobile Components |

| Segments Covered | By Material Type, By Vehicle Type, By Design Style, By Manufacturing Process, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Radiator Grilles Market: Segmentation Insights

The global radiator grilles market is divided by material type, vehicle type, design style, manufacturing process, end-user, and region.

Segmentation Insights by Material Type

Based on material type, the global radiator grilles market is divided into plastic, metal, composite, and carbon fiber.

In the radiator grilles market, plastic is the most dominant material segment. Plastic radiator grilles are widely favored due to their lightweight nature, ease of molding into complex shapes, and cost-effectiveness, which aligns well with mass automotive production. They also offer corrosion resistance and are available in various finishes, making them suitable for both functional and aesthetic applications in economy and mid-range vehicles. Automakers increasingly rely on plastic grilles to achieve both aerodynamic performance and visual appeal while keeping manufacturing costs low.

Following plastic, metal radiator grilles hold a significant share of the market. Traditionally used in vehicles, especially in trucks and luxury cars, metal grilles are valued for their strength, rigidity, and premium look. Metals such as aluminum and stainless steel are common, offering durability and heat resistance. However, they tend to be heavier and more expensive to produce, which has led to their gradual decline in favor of lighter alternatives in non-premium segments.

Composite materials are the next in line and are gaining traction due to their ability to blend the benefits of plastic and metal. These materials are engineered to provide improved strength-to-weight ratios and better thermal stability while maintaining design flexibility. Though not yet as widely adopted as plastic or metal, composite radiator grilles are increasingly used in high-performance and electric vehicles, where both weight savings and structural integrity are important.

Carbon fiber, while the least dominant segment, represents a niche yet growing part of the market. Known for its exceptional strength-to-weight ratio and sleek aesthetic, carbon fiber grilles are typically reserved for sports and luxury vehicles. Their high manufacturing cost limits widespread use, but they are sought after in premium automotive circles for both performance enhancement and visual distinction. As lightweighting becomes more critical in vehicle design, this segment may see slow but steady growth.

Segmentation Insights by Vehicle Type

On the basis of vehicle type, the global radiator grilles market is bifurcated into passenger cars, commercial vehicles, SUVs, and motorcycles.

In the radiator grilles market, passenger cars represent the most dominant vehicle type segment. The widespread global demand for passenger vehicles, especially in urban and suburban areas, drives this dominance. Radiator grilles in passenger cars are not only functional—allowing airflow to cool the engine—but are also critical for styling, as they contribute significantly to brand identity and aesthetics. Automakers often customize grille designs for each model to appeal to consumers, further increasing the volume and diversity of grilles used in this segment.

SUVs follow closely behind passenger cars, with growing popularity across both developed and emerging markets. SUVs typically require larger and more robust grilles to accommodate their more powerful engines and aggressive styling preferences. The trend toward luxury and high-performance SUVs also fuels demand for premium grille materials and distinctive designs, making this a rapidly expanding segment with a focus on both functionality and bold design.

Commercial vehicles make up the next major segment. These include trucks, vans, and buses that rely on radiator grilles primarily for utility and engine cooling rather than aesthetics. Durability and ease of maintenance are key considerations here, so metal and heavy-duty plastic grilles are common. While the volume of grilles per vehicle may be similar to other segments, the replacement frequency is often higher due to the demanding operational conditions these vehicles face.

Motorcycles are the least dominant segment in the radiator grilles market. Many motorcycles, especially in the commuter and mid-range categories, do not require prominent radiator grilles due to their air-cooled engines. However, in high-performance and sports motorcycles with liquid-cooled engines, compact radiator grilles are used. These are typically small, function-focused components made from lightweight materials, limiting their contribution to overall market volume.

Segmentation Insights by Design Style

Based on design style, the global radiator grilles market is divided into traditional grilles, modern grilles, sport grilles, and custom grilles.

In terms of design style, modern grilles hold the most dominant position in the radiator grilles market. These grilles reflect contemporary automotive design trends, often featuring sleek lines, advanced materials, and integrated technologies like active grille shutters. Automakers use modern grilles to improve aerodynamics, fuel efficiency, and brand identity. Their prevalence across a wide range of vehicle types—from sedans to SUVs—supports their leading market share, especially as consumer preferences shift toward innovative and tech-forward vehicle aesthetics.

Traditional grilles come next and continue to maintain a strong presence, particularly in vehicles that prioritize heritage or a classic design appeal. These grilles are typically simpler in construction, often utilizing metal or basic plastic finishes. They are common in budget-friendly models or brands that emphasize reliability over trendiness. Though less flashy, traditional grilles are valued for their cost-effectiveness and consistent performance, making them a staple in many long-standing vehicle lines.

Sport grilles are gaining traction, especially among performance-oriented vehicles and younger demographics seeking a more aggressive, high-energy look. These grilles often feature bold patterns, mesh structures, and premium materials like carbon fiber or gloss black plastic. They are prominent in sports cars, performance trims of mainstream vehicles, and high-end SUVs, where design and airflow optimization are both essential.

Custom grilles, while the least dominant, occupy a niche but lucrative segment of the market. These are typically found in the aftermarket or specialty vehicle sector and cater to consumers looking to personalize their vehicles. Custom grilles can range from luxurious chrome finishes to intricately cut designs that reflect individual style or brand identity. Although adoption is limited compared to OEM-fitted grilles, this segment is growing in regions where vehicle customization culture is strong.

Segmentation Insights by Manufacturing Process

On the basis of manufacturing process, the global radiator grilles market is bifurcated into Injection molding, stamping, 3d printing, and handcrafted.

In the radiator grilles market, injection molding is the most dominant manufacturing process. This is due to its efficiency, cost-effectiveness, and suitability for mass production. Injection molding allows manufacturers to produce complex shapes with high precision, making it ideal for plastic radiator grilles, which are common in passenger cars and SUVs. It is also capable of producing consistent results across large volumes, which helps keep costs low while maintaining quality, contributing to its widespread use in the automotive industry.

Stamping follows as the second most dominant process, particularly for metal radiator grilles. Stamping is a reliable method for shaping metal sheets into the required grille shapes. It is commonly used for metal grilles in commercial vehicles, trucks, and certain luxury cars. The process is efficient for producing high volumes of grilles with consistent thickness and finish. Stamped metal grilles are highly durable and suited for vehicles that prioritize strength and performance over intricate design details.

3D printing is an emerging technology in the radiator grille market, offering high design flexibility and customization. While not yet widespread for mass production, 3D printing is used for creating prototype grilles, custom designs, and low-volume runs. It allows manufacturers to experiment with complex, intricate designs and lightweight materials without the constraints of traditional tooling. As technology improves and costs decrease, 3D printing could see greater adoption in niche markets like luxury vehicles and electric cars, where unique and customized grille designs are highly valued.

Handcrafted grilles are the least dominant manufacturing method. Typically found in premium, high-end, or custom vehicles, handcrafted grilles are made with a high level of detail and precision. This method is labor-intensive and time-consuming, making it cost-prohibitive for mass-market vehicles. Handcrafted grilles are often made from premium materials like stainless steel or carbon fiber and are prized for their exclusivity and unique designs. This process is mainly used in small-scale production runs or as an aftermarket option for consumers seeking a high level of personalization.

Segmentation Insights by End-User

On the basis of end-user, the global radiator grilles market is bifurcated into OEM (original equipment manufacturer), aftermarket, restoration, and customization.

In the radiator grilles market, OEM (Original Equipment Manufacturer) is the most dominant end-user segment. OEMs are the primary consumers of radiator grilles, as they are used in the production of new vehicles. Automakers rely heavily on OEM grilles to meet the design and functionality requirements of various vehicle models. These grilles are essential for vehicle cooling systems and aesthetic purposes. As the demand for new vehicles continues to grow globally, the OEM segment consistently holds the largest share in the radiator grille market.

The aftermarket segment follows as a significant portion of the market. Aftermarket radiator grilles are purchased by vehicle owners for replacement, repair, or enhancement of their vehicles. Aftermarket grilles are typically available in a wider range of designs, materials, and finishes, offering consumers more options for customization or functionality upgrades. This segment is driven by the demand for vehicle personalization, vehicle maintenance, and repairs, which is particularly strong in regions with a high number of vehicles already on the road. As a result, the aftermarket for radiator grilles continues to expand as consumers seek both aesthetic improvements and more efficient engine cooling.

Restoration is a smaller but important segment, primarily focused on restoring classic or vintage vehicles. Radiator grilles are often replaced or refurbished during vehicle restoration projects to maintain the vehicle’s original design and functionality. This segment requires high-quality, accurate replicas of original grilles for older models, and while it doesn't account for as large a market share as OEM or aftermarket, it is crucial for the preservation of classic vehicles and appeals to a dedicated group of enthusiasts.

The customization segment, while the least dominant, is growing, especially in markets where vehicle personalization is a significant trend. Customization refers to unique, often bespoke grilles created to suit individual tastes or specific brand identities. Consumers in this segment are typically looking for something that reflects their personality or stands out from standard vehicle designs. The demand for custom radiator grilles is especially strong in the luxury, performance, and sports vehicle sectors, where exclusivity and unique design are highly valued. Although this segment remains niche, it is expected to grow as consumers increasingly seek to customize their vehicles.

Radiator Grilles Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region is the most dominant in the global radiator grilles market. This leadership is fueled by a strong concentration of automotive production hubs in countries such as China, Japan, India, and South Korea. The increasing demand for both passenger and commercial vehicles, coupled with rising consumer preference for visually appealing and aerodynamically efficient vehicles, drives market growth. Additionally, technological advancements in lightweight materials and grille design, along with supportive government initiatives for energy-efficient vehicles, further strengthen the region’s market position.

North America follows as the second most dominant region, characterized by a well-established automotive industry and high consumer demand for SUVs, trucks, and customized vehicles. Radiator grilles serve both functional and aesthetic purposes in this region, with many consumers prioritizing style and vehicle personalization. The integration of advanced technologies such as active grille shutters, especially in premium and high-performance vehicles, has boosted demand. Moreover, the region’s strong aftermarket ecosystem contributes significantly to the overall radiator grilles market.

Europe holds the third position in the global market, supported by the presence of several luxury and performance vehicle manufacturers. Countries like Germany, France, and Italy are at the forefront of grille design innovation, particularly for electric and hybrid vehicles that require specialized cooling solutions. The region’s strict regulatory standards on fuel efficiency and emissions further encourage continuous development in grille materials and aerodynamics. European consumers also place high value on vehicle design, which reinforces the market for premium grille components.

Middle East and Africa represent a moderately growing market for radiator grilles, driven by increasing demand for imported vehicles and rising interest in vehicle customization. The region, particularly the Gulf Cooperation Council countries, shows a preference for high-end and durable grilles suited for extreme weather conditions. While local vehicle production remains limited, the aftermarket plays a crucial role in supporting market activity through personalized grille upgrades.

Latin America is the least dominant region in the radiator grilles market. Economic challenges and lower levels of automotive manufacturing contribute to slower market growth. However, gradual increases in vehicle demand, particularly in countries like Brazil and Mexico, are providing some momentum. Growing consumer interest in automotive styling and the expansion of international automakers in the region offer potential for future market development, although at a relatively slower pace compared to other regions.

Radiator Grilles Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the radiator grilles market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global radiator grilles market include:

- Magna Inteational

- Plastic Omnium

- Toyoda Gosei

- SRG Global

- Lacks Enterprises

- Sakae Riken Kogyo

- Samshin Chemicals

- Faltec

- Shanghai Ruier Industrial

- Changchun Faway Automobile Components

The global radiator grilles market is segmented as follows:

By Material Type

- Plastic

- Metal

- Composite

- Carbon Fiber

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- SUVs

- Motorcycles

By Design Style

- Traditional Grilles

- Modern Grilles

- Sport Grilles

- Custom Grilles

By Manufacturing Process

- Injection Molding

- Stamping

- 3D Printing

- Handcrafted

By End-User

- OEM (Original Equipment Manufacturer)

- Aftermarket

- Restoration

- Customization

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Radiator Grilles

Request Sample

Radiator Grilles