SCM Ultrafine Mill Market Size, Share, and Trends Analysis Report

CAGR :

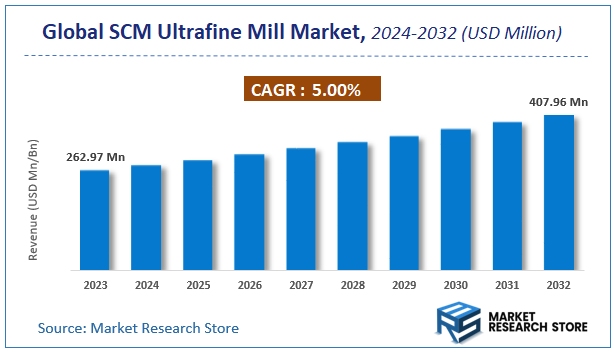

| Market Size 2023 (Base Year) | USD 262.97 Million |

| Market Size 2032 (Forecast Year) | USD 407.96 Million |

| CAGR | 5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

SCM Ultrafine Mill Market Insights

According to Market Research Store, the global SCM ultrafine mill market size was valued at around USD 262.97 million in 2023 and is estimated to reach USD 407.96 million by 2032, to register a CAGR of approximately 5.00% in terms of revenue during the forecast period 2024-2032.

The SCM ultrafine mill report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global SCM Ultrafine Mill Market: Overview

SCM Ultrafine Mill is a high-efficiency grinding machine designed to produce fine powder products from materials such as minerals, chemicals, and other raw materials. It is widely used in industries like construction, mining, and manufacturing for applications requiring powders with a fine particle size, particularly in areas like the production of super fine powders for coatings, pharmaceuticals, and other products. This mill is designed to be energy-efficient and provides a high level of output. The SCM Ultrafine Mill features a state-of-the-art grinding mechanism that includes a classifier to ensure consistent particle size distribution, making it ideal for producing materials with fine and ultra-fine particles.

Key Highlights

- The SCM ultrafine mill market is anticipated to grow at a CAGR of 5.00% during the forecast period.

- The global SCM ultrafine mill market was estimated to be worth approximately USD 262.97 million in 2023 and is projected to reach a value of USD 407.96 million by 2032.

- The growth of the SCM ultrafine mill market is being driven by increasing demand for ultra-fine powders in various industries.

- Based on the application, the mining industry segment is growing at a high rate and is projected to dominate the market.

- On the basis of product type, the dry type SCM ultrafine mill segment is projected to swipe the largest market share.

- In terms of end-user industry, the mining & metallurgical industry segment is expected to dominate the market.

- Based on the distribution channel, the direct sales segment is expected to dominate the market.

- In terms of operational mode, the automated operation segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

SCM Ultrafine Mill Market: Dynamics

Key Growth Drivers:

- Rising Demand for Fine Powder Products: The increasing demand across various industries (such as chemicals, mining, and pharmaceuticals) for fine powder products drives the need for efficient milling technologies like SCM ultrafine mills.

- Growth in the Construction and Mining Industries: The demand for fine grinding in the construction and mining industries, especially for materials like cement and minerals, contributes to the adoption of ultrafine mills.

- Technological Advancements in Milling Systems: Continuous innovations in milling technologies are improving the efficiency, capacity, and performance of SCM ultrafine mills, thus driving market growth.

- Increased Use of Ultrafine Grinding in the Pharmaceutical Industry: The pharmaceutical industry's growing focus on producing ultra-fine powders for drug formulations is pushing the demand for SCM ultrafine mills.

- Environmental Regulations on Emissions: Stringent environmental regulations related to emissions from traditional milling equipment are encouraging the adoption of cleaner, more energy-efficient SCM ultrafine mills.

Restraints:

- High Initial Investment Costs: The high capital cost required for purchasing and setting up SCM ultrafine mills can be a major deterrent, particularly for small and medium-sized enterprises.

- Maintenance and Operating Costs: The maintenance and operating costs associated with ultrafine mills can be relatively high due to their complex mechanisms and continuous usage, which can limit their widespread adoption.

- Energy Consumption: SCM ultrafine mills can consume significant amounts of energy, which is a concern for businesses aiming to reduce operational costs and carbon footprints.

- Limited Availability of Skilled Operators: There is a lack of skilled operators who are proficient in handling advanced ultrafine milling equipment, which can hamper the efficient use of SCM ultrafine mills.

Opportunities:

- Rising Applications in Nanotechnology: The growing field of nanotechnology, which requires extremely fine powders, offers significant opportunities for SCM ultrafine mills in creating products with nano-sized particles.

- Expansion in Emerging Markets: Rapid industrialization in emerging economies, particularly in Asia-Pacific and Latin America, creates an opportunity for SCM ultrafine mill adoption in sectors like mining, chemicals, and construction.

- R&D for Energy-Efficient Mills: There is an opportunity for innovation in developing energy-efficient ultrafine mills that can address both the energy consumption and environmental concerns while maintaining high performance.

- Increasing Demand for High-Quality Pigments and Coatings: Industries such as paint, coatings, and pigments require fine particle sizes for quality control, offering growth opportunities for SCM ultrafine mills in the production of fine powders for these sectors.

Challenges:

- High Competition from Alternative Milling Technologies: Other milling technologies, such as jet mills or ball mills, may present lower costs or better efficiency, posing competition to SCM ultrafine mills in certain applications.

- Complexity of Scale-Up Processes: Scaling up the use of SCM ultrafine mills for large-scale production can be challenging due to the technical complexities involved in maintaining consistent product quality and milling efficiency.

- Raw Material Variability: The variability in the characteristics of raw materials used in milling can lead to inconsistent results in fine powder production, which may affect product quality.

- Regulatory Challenges: Adhering to local and international regulations, especially regarding environmental impact and safety standards, can pose compliance challenges for manufacturers and operators of SCM ultrafine mills.

SCM Ultrafine Mill Market: Report Scope

This report thoroughly analyzes the SCM Ultrafine Mill Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | SCM Ultrafine Mill Market |

| Market Size in 2023 | USD 262.97 Million |

| Market Forecast in 2032 | USD 407.96 Million |

| Growth Rate | CAGR of 5% |

| Number of Pages | 177 |

| Key Companies Covered | Shanghai SBM Company, GBM, Thaim Trading Company, YCM MINING MACHINERY, Shanghai SYM Company, ZAQ Industry & Technology Group, TQMC Company, Shanghai Hmard Company, Shanghai MCG Company, CCM Industry and Technology Group |

| Segments Covered | By Application, By Product Type, By End-User Industry, By Distribution Channel, By Operational Mode, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

SCM Ultrafine Mill Market: Segmentation Insights

The global SCM ultrafine mill market is divided by application, product type, end-user industry, distribution channel, operational mode, and region.

Segmentation Insights by Application

Based on application, the global SCM ultrafine mill market is divided into mining industry, chemical industry, construction industry, pharmaceutical industry, and other applications.

In the SCM ultrafine mill market, the Mining Industry stands as the most dominant segment. This is due to the significant demand for ultrafine milling processes in mining, where minerals, ores, and raw materials are ground into finer particles for better processing, extraction, and refining. The ultrafine mill plays a crucial role in reducing particle size, improving the efficiency of subsequent stages like flotation, leaching, and smelting, making it a key piece of equipment in mining operations.

The Chemical Industry follows closely behind as a prominent segment. The chemical industry requires ultrafine milling for producing fine powders used in the formulation of various chemicals, paints, pigments, fertilizers, and specialty products. The need for precise particle size control in chemical formulations and the increasing demand for fine chemicals in diverse sectors drive the adoption of SCM ultrafine mills.

Next in line is the Construction Industry, where ultrafine mills are primarily used for processing materials like cement, aggregates, and other construction-related products. In particular, ultrafine grinding is essential for producing high-quality concrete, cement, and other materials that meet specific strength and durability standards. This makes it an essential technology in modern construction practices, though slightly less dominant than mining and chemicals.

The Pharmaceutical Industry also makes significant use of ultrafine mills, especially for grinding active pharmaceutical ingredients (APIs) into fine powders for better bioavailability and faster dissolution in the body. However, this segment is less dominant in comparison to the mining, chemical, and construction industries due to the specialized nature of its applications and regulatory requirements that limit the scale of operations.

Segmentation Insights by Product Type

On the basis of product type, the global SCM ultrafine mill market is bifurcated into dry type SCM ultrafine mill and wet type SCM ultrafine mill.

In the SCM ultrafine mill market, the Dry Type SCM Ultrafine Mill is the most dominant product type. This dominance is primarily driven by the widespread use of dry grinding processes across various industries, such as mining, chemicals, construction, and even food processing. Dry milling is preferred for materials that do not require the addition of water or solvents, allowing for efficient, cost-effective processing. It is especially popular in the production of powders for cement, ceramics, and various chemicals, where the end product is required to be in a dry form. The dry-type mills also offer advantages like simpler maintenance, lower operational costs, and fewer environmental concerns compared to wet mills.

The Wet Type SCM Ultrafine Mill comes second in terms of market share. Wet grinding is essential when dealing with materials that require a slurry or when finer particle sizes are needed, which may be the case in industries such as pharmaceuticals, chemicals, and paints. Wet milling also enhances the grinding efficiency of certain materials and ensures a more uniform particle size, which is crucial for applications requiring precise formulations and consistency. However, this method involves more complexity in terms of equipment, maintenance, and disposal of waste, which limits its widespread adoption compared to dry-type mills.

Segmentation Insights by End-User Industry

Based on end-user industry, the global SCM ultrafine mill market is divided into mining & metallurgical industry, chemicals & fertilizers industry, energy & power industry, building & construction industry, and pharmaceutical & healthcare industry.

In the SCM ultrafine mill market, the Mining & Metallurgical Industry is the most dominant end-user industry. This is largely due to the heavy reliance on ultrafine milling in the extraction and processing of minerals, ores, and other raw materials. In mining and metallurgy, ultrafine mills are essential for grinding and refining materials into fine powders, which can then be processed for extraction and smelting. The mining industry’s demand for efficient milling technologies to improve material recovery and reduce waste has solidified its position as the leading segment in this market.

The Chemicals & Fertilizers Industry follows closely as the second-largest end-user. The need for ultrafine mills in this sector stems from the production of fine chemicals, pigments, fertilizers, and other specialty chemicals, where precise particle size control is critical. The ability to produce very fine powders, which enhance the dissolution and reactivity of certain chemicals, makes SCM ultrafine mills highly valuable in chemical production processes. The demand for better-performing and more efficient chemical formulations also drives the growth of this segment.

The Energy & Power Industry represents a significant, though smaller, portion of the market. Ultrafine mills are used for grinding materials like coal, biomass, and other fuels in power generation, as well as in the processing of materials for renewable energy applications such as solar panel production. The need for ultra-fine milling in energy production, particularly for efficiency in combustion and energy storage processes, drives its adoption, but it is not as dominant as the mining or chemical sectors.

The Building & Construction Industry also makes substantial use of ultrafine mills, primarily for processing cement, concrete, and other construction materials. The grinding of these materials to a fine consistency is crucial for improving the performance, strength, and durability of construction products. However, this segment is smaller than the mining, chemical, and energy sectors, as it is more focused on specific material processing rather than continuous, widespread industrial milling.

The Pharmaceutical & Healthcare Industry is the least dominant segment in terms of SCM ultrafine mill usage, though still significant. In this industry, ultrafine mills are primarily used for grinding active pharmaceutical ingredients (APIs) and excipients, where particle size control is crucial for bioavailability and efficacy. Despite its importance in drug formulation, the scale of adoption in pharmaceuticals is smaller compared to industries like mining or chemicals, due to the specialized nature of the applications and the high regulatory standards involved.

Segmentation Insights by Distribution Channel

On the basis of distribution channel, the global SCM ultrafine mill market is bifurcated into direct sales, distributors & dealers, and online retailers.

In the SCM ultrafine mill market, Direct Sales is the most dominant distribution channel. This is largely due to the specialized nature of the product, which requires detailed consultations and customized solutions for different industries like mining, chemicals, and pharmaceuticals. Manufacturers often sell directly to large industrial clients to ensure that the equipment meets specific requirements, such as milling capacity, particle size, and operational conditions. Direct sales also allow for more personalized customer support, technical assistance, and after-sales services, which are critical in the industrial equipment market. Additionally, the high cost and complexity of SCM ultrafine mills make direct sales more common, as manufacturers often prefer to engage in one-on-one negotiations and offer tailored solutions.

The Distributors & Dealers segment follows as the second most important distribution channel. Distributors and dealers play a significant role in expanding the reach of SCM ultrafine mills, particularly in regions where direct sales may be logistically challenging or too costly for the manufacturer. These intermediaries help bridge the gap between the manufacturers and end-users by facilitating sales, offering technical support, and managing stock and delivery. They are particularly vital in markets where multiple sectors, such as chemicals, energy, and construction, require a local presence for easy access to the equipment. Distributors also help maintain a steady flow of products in the market and cater to a wider customer base.

The Online Retailers segment, while growing, is the least dominant distribution channel. Online sales are more common in smaller or less complex milling systems, rather than large-scale industrial equipment like SCM ultrafine mills, which typically require on-site evaluations, installations, and specialized services. However, as the industrial sector increasingly moves toward e-commerce and digital platforms for purchasing industrial equipment, online retailers have started to play a larger role. This channel can be particularly beneficial for small businesses or companies that are looking to purchase smaller or standardized equipment online. Nevertheless, the complexity, cost, and service requirements of ultrafine mills limit their widespread sale through online platforms.

Segmentation Insights by Operational Mode

On the basis of operational mode, the global SCM ultrafine mill market is bifurcated into manual operation and automated operation.

In the SCM ultrafine mill market, Automated Operation is the most dominant operational mode. This is driven by the increasing demand for efficiency, precision, and reduced human intervention in industrial milling processes. Automated ultrafine mills provide significant advantages, such as consistent product quality, higher throughput, and the ability to operate continuously without the need for frequent manual adjustments. These mills are equipped with advanced control systems and sensors, allowing for optimized operation and minimal downtime, which is especially important in large-scale production environments like mining, chemicals, and pharmaceuticals. The push for automation is also in line with broader industrial trends towards smart manufacturing and Industry 4.0, where increased automation leads to better overall operational efficiency.

Manual Operation comes next in terms of market share. While manual mills are generally simpler and less expensive than their automated counterparts, they are more labor-intensive and less efficient for large-scale industrial applications. Manual mills are often used in smaller operations or in industries that require less precision in particle size. These mills rely on the operator to adjust and control the grinding process, which can lead to variations in product quality and throughput. However, for small-scale applications or industries with less frequent milling needs, manual operation can be a cost-effective solution. Additionally, manual mills are often used in research and development settings where flexibility and operator control are prioritized.

SCM Ultrafine Mill Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region dominates the SCM ultrafine mill market, driven by rapid industrialization, urbanization, and significant infrastructure development in countries like China, India, and Japan. The growing demand for high-quality materials in sectors such as construction, chemicals, and mining, coupled with government investments, strengthens the region’s market position.

North America holds a strong position in the SCM ultrafine mill market, with the United States and Canada leading the demand due to advanced manufacturing industries and a focus on energy-efficient technologies. Industries such as mining, chemicals, and construction play a key role, supported by research and development aimed at improving grinding technologies.

Europe follows closely behind with a substantial share in the market. The region's advanced industrial capabilities, particularly in countries like Germany, France, and the United Kingdom, contribute significantly to the demand for high-precision grinding solutions. The region’s focus on sustainability and energy efficiency further boosts the adoption of SCM ultrafine mills.

Latin America experiences moderate growth in the SCM ultrafine mill market, with key players like Brazil, Mexico, and Argentina driving demand in the mining, construction, and chemicals sectors. While the market is not as large as in Asia Pacific, North America, and Europe, growth potential remains as industries continue to expand.

The Middle East and Africa region exhibits the least market share, with slow but steady growth. Countries like Saudi Arabia, the United Arab Emirates, and South Africa are investing in infrastructure and industrial development, although the adoption of ultrafine grinding mills remains limited. However, with increasing industrial activities, the region holds future potential for market growth.

SCM Ultrafine Mill Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the SCM ultrafine mill market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global SCM ultrafine mill market include:

- Shanghai SBM Company

- GBM

- Thaim Trading Company

- YCM MINING MACHINERY

- Shanghai SYM Company

- ZAQ Industry & Technology Group

- TQMC Company

- Shanghai Hmard Company

- Shanghai MCG Company

- CCM Industry and Technology Group

The global SCM ultrafine mill market is segmented as follows:

By Application

- Mining Industry

- Chemical Industry

- Construction Industry

- Pharmaceutical Industry

- Other Applications

By Product Type

- Dry Type SCM Ultrafine Mill

- Wet Type SCM Ultrafine Mill

By End-User Industry

- Mining and Metallurgical Industry

- Chemicals and Fertilizers Industry

- Energy and Power Industry

- Building and Construction Industry

- Pharmaceutical and Healthcare Industry

By Distribution Channel

- Direct Sales

- Distributors and Dealers

- Online Retailers

By Operational Mode

- Manual Operation

- Automated Operation

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

SCM Ultrafine Mill

Request Sample

SCM Ultrafine Mill