Secondary Batteries Market Size, Share, and Trends Analysis Report

CAGR :

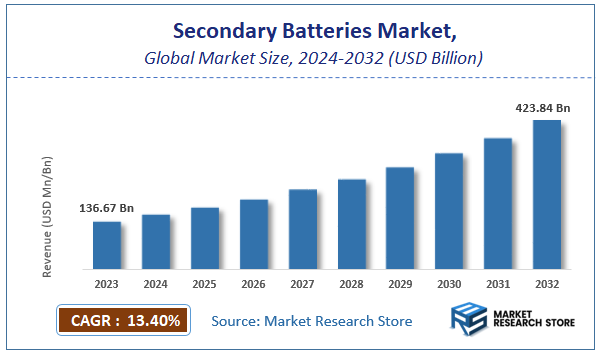

| Market Size 2023 (Base Year) | USD 136.67 Billion |

| Market Size 2032 (Forecast Year) | USD 423.84 Billion |

| CAGR | 13.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Secondary Batteries Market Insights

According to Market Research Store, the global secondary batteries market size was valued at around USD 136.67 billion in 2023 and is estimated to reach USD 423.84 billion by 2032, to register a CAGR of approximately 13.4% in terms of revenue during the forecast period 2024-2032.

The secondary batteries report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Secondary Batteries Market: Overview

Secondary batteries, also known as rechargeable batteries, are energy storage devices that can be discharged and recharged multiple times, unlike primary batteries, which are designed for single-use. These batteries store electrical energy through reversible chemical reactions, allowing them to be reused after being discharged. Common types of secondary batteries include lithium-ion (Li-ion), nickel-metal hydride (NiMH), lead-acid, and sodium-ion batteries, each with its own set of characteristics that make them suitable for specific applications. Lithium-ion batteries are the most widely used type of secondary battery, particularly in portable electronics such as smartphones, laptops, and electric vehicles (EVs), due to their high energy density, long cycle life, and relatively light weight.

The secondary battery market is growing rapidly due to the increasing demand for portable electronics, electric vehicles, renewable energy storage solutions, and power backup systems. Key drivers include the shift towards sustainable energy, the electrification of transportation, and the need for efficient energy storage in applications like solar and wind power generation. Additionally, advancements in battery technology, such as the development of solid-state batteries and improvements in charging speeds, are driving further innovation in the market.

Key Highlights

- The secondary batteries market is anticipated to grow at a CAGR of 13.4% during the forecast period.

- The global secondary batteries market was estimated to be worth approximately USD 136.67 billion in 2023 and is projected to reach a value of USD 423.84 billion by 2032.

- The growth of the secondary batteries market is being driven by the increasing demand for portable power across various applications.

- Based on the product, the lead acid segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the automotive segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Secondary Batteries Market: Dynamics

Key Growth Drivers:

- Surging Demand for Electric Vehicles (EVs): The rapid adoption of EVs, driven by environmental concerns, government incentives, and advancements in battery technology, is the primary growth engine for the secondary battery market. EVs require large, high-capacity rechargeable batteries.

- Growing Adoption of Portable Consumer Electronics: Smartphones, laptops, tablets, and other portable electronic devices rely heavily on rechargeable batteries, sustaining a consistent demand for smaller, high-energy-density batteries.

- Increasing Deployment of Grid-Scale Energy Storage Systems (ESS): The integration of renewable energy sources like solar and wind power necessitates ESS to stabilize the grid and store excess energy. Secondary batteries are a key technology for these applications.

- Rising Demand for Uninterruptible Power Supplies (UPS): UPS systems, used in data centers, hospitals, and industrial facilities to provide backup power, increasingly utilize advanced secondary batteries for reliable and long-duration power.

- Proliferation of Portable Power Tools and Appliances: Cordless power tools, vacuum cleaners, and other portable appliances are increasingly powered by rechargeable batteries, offering convenience and flexibility.

- Advancements in Battery Technology: Continuous innovation in battery chemistries (e.g., lithium-ion and its variants), materials science, and manufacturing processes are leading to higher energy density, longer cycle life, faster charging times, and improved safety, further driving market adoption.

Restraints:

- High Cost of Raw Materials: The prices of key raw materials used in battery manufacturing, such as lithium, cobalt, nickel, and manganese, can be volatile and significantly impact battery production costs.

- Limited Availability and Geopolitical Risks Associated with Raw Materials: The geographical concentration of raw material reserves and geopolitical factors can create supply chain vulnerabilities and price instability.

- Safety Concerns Associated with Certain Battery Chemistries: Thermal runaway and the potential for fire or explosion, particularly with some lithium-ion battery chemistries, remain a concern and necessitate robust safety measures.

- Long Charging Times Compared to Traditional Fueling: While charging infrastructure is improving, the time required to fully charge an EV battery is still significantly longer than refueling a gasoline car, which can be a deterrent for some consumers.

- Limited Lifespan and Degradation Over Time: Secondary batteries have a finite lifespan and their capacity degrades over charge-discharge cycles, eventually requiring replacement, which adds to the overall cost of ownership.

- Lack of Standardized Recycling Infrastructure: The infrastructure for recycling end-of-life secondary batteries, especially EV batteries, is still developing and needs significant expansion to handle the growing volumes.

Opportunities:

- Development of Next-Generation Battery Technologies: Extensive research and development efforts are underway to develop batteries with higher energy density, faster charging times, improved safety, longer lifespan, and lower cost, such as solid-state batteries, lithium-sulfur batteries, and metal-air batteries.

- Expansion of Battery Recycling and Second-Life Applications: Developing efficient and cost-effective battery recycling processes and exploring second-life applications for used EV batteries (e.g., in stationary storage) can create a more circular economy and reduce waste.

- Standardization of Battery Formats and Charging Infrastructure: Establishing standardized battery formats and widespread, convenient charging infrastructure for EVs will accelerate their adoption and drive battery demand.

- Integration of Batteries with Smart Grids: Advanced battery management systems and their integration with smart grids can optimize energy storage and distribution, enhancing grid stability and efficiency.

- Growth in Microbattery and Flexible Battery Applications: The demand for miniaturized and flexible batteries for wearable electronics, medical devices, and IoT applications presents a growing opportunity.

- Development of Sustainable and Environmentally Friendly Battery Materials: Research into and adoption of battery materials with lower environmental impact and ethical sourcing practices are gaining importance and creating opportunities.

Challenges:

- Reducing Battery Costs to Achieve Price Parity with Internal Combustion Engines: Lowering the cost of EV batteries is crucial for achieving price parity with gasoline cars and accelerating mass adoption.

- Improving Battery Safety and Addressing Thermal Runaway Risks: Enhancing the inherent safety of batteries and developing robust thermal management systems are critical for consumer confidence and wider adoption.

- Developing Fast and Convenient Charging Solutions: Overcoming the long charging times of EVs through the development of ultra-fast charging technologies and expanding charging infrastructure is essential.

- Establishing a Sustainable and Scalable Battery Recycling Ecosystem: Creating a comprehensive and economically viable system for collecting, dismantling, and recycling end-of-life batteries is a significant logistical and environmental challenge.

- Ensuring Ethical and Sustainable Sourcing of Raw Materials: Addressing the environmental and social impacts associated with the mining and processing of battery raw materials is a growing ethical and supply chain challenge.

- Standardization and Interoperability Across Different Battery Technologies and Manufacturers: Lack of standardization can hinder the development of charging infrastructure and battery swapping technologies.

Secondary Batteries Market: Report Scope

This report thoroughly analyzes the Secondary Batteries Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Secondary Batteries Market |

| Market Size in 2023 | USD 136.67 Billion |

| Market Forecast in 2032 | USD 423.84 Billion |

| Growth Rate | CAGR of 13.4% |

| Number of Pages | 167 |

| Key Companies Covered | Amperex Technologies, BYD, LG, Samsung, Johnson Controls, Tosoh, Prince |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Secondary Batteries Market: Segmentation Insights

The global secondary batteries market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global secondary batteries market is divided into lead acid, lithium-ion (Li-Ion), nickel-cadmium (Ni-Cd), nickel metal hydride, and others

Lead Acid batteries dominate the secondary batteries market due to their long-established use in a variety of applications, including automotive, backup power systems, and uninterruptible power supplies (UPS). Despite the growing popularity of more advanced battery technologies, lead-acid batteries remain highly prevalent because of their cost-effectiveness, reliability, and well-understood manufacturing processes. They are especially dominant in the automotive sector for starting, lighting, and ignition (SLI) applications in vehicles. Their ability to deliver a large amount of current in a short period makes them suitable for these applications. However, environmental concerns regarding lead content are pushing the industry towards more eco-friendly alternatives.

Lithium-Ion (Li-Ion) batteries have become the dominant choice in portable electronics and are rapidly gaining ground in automotive applications, particularly with the rise of electric vehicles (EVs). Li-Ion batteries offer high energy density, lightweight construction, and a longer lifespan compared to other secondary battery types. Their ability to be recharged many times over without significant capacity degradation has made them the preferred option in smartphones, laptops, and EVs. As governments and industries continue to push for cleaner energy solutions, the demand for lithium-ion batteries in electric vehicles and energy storage systems is expected to grow significantly in the coming years. The scalability and advanced performance of Li-Ion batteries contribute to their increasing dominance in various market segments.

Nickel-Cadmium (Ni-Cd) batteries, while once widely used, have seen a decline in popularity due to environmental concerns over cadmium content and the availability of more efficient alternatives. However, they are still used in some niche applications such as in power tools, medical devices, and emergency lighting systems. Ni-Cd batteries have a good performance in extreme temperatures and can tolerate deep discharge cycles. Despite their advantages, their toxicity and the fact that newer technologies offer better performance have caused Ni-Cd to lose ground to more sustainable options, particularly lithium-ion batteries.

Nickel Metal Hydride (NiMH) batteries are widely used in hybrid vehicles, power tools, and consumer electronics. Although not as energy-dense as lithium-ion, NiMH batteries offer a safer alternative to nickel-cadmium batteries and are more environmentally friendly. They are less toxic and can deliver a more consistent voltage throughout their discharge cycle. While lithium-ion batteries have overtaken NiMH in many applications, NiMH is still a key player in hybrid vehicles and other sectors requiring moderate power output. Their relatively lower cost and good performance in mid-power applications continue to drive their use in specific markets.

Segmentation Insights by Application

On the basis of application, the global secondary batteries market is bifurcated into automotive, household, and industrial.

Automotive sector, secondary batteries dominate due to the growing shift towards electric vehicles (EVs). Lead-acid batteries have long been used in vehicles for starting, lighting, and ignition (SLI) purposes, while lithium-ion batteries are becoming more common in electric vehicles (EVs). The demand for EVs, which rely heavily on lithium-ion batteries due to their energy density and lightweight properties, is expected to continue growing with the rise of sustainable energy initiatives and government regulations. The automotive sector's shift towards electric mobility is driving innovation in battery technologies, with both lead-acid and lithium-ion batteries competing for dominance based on cost, efficiency, and performance.

Household applications primarily use lead-acid batteries for backup power systems, uninterruptible power supplies (UPS), and emergency lighting, although lithium-ion batteries are increasingly being adopted for home energy storage systems, such as solar energy storage. Lithium-ion batteries, with their longer lifespan, higher energy density, and safer properties, have found a growing role in domestic applications, including the storage of solar energy and power backup. The convenience and reliability offered by lithium-ion batteries are helping them dominate in households for these uses, especially as the price of these batteries continues to decrease. However, lead-acid batteries are still prevalent in less expensive systems due to their lower upfront cost.

Industrial applications utilize a wide range of secondary batteries, including lead-acid, lithium-ion, nickel-cadmium, and nickel-metal hydride (NiMH) batteries. Lead-acid batteries are still widely used in industrial sectors for backup power, forklifts, and other heavy machinery. Lithium-ion batteries are increasingly being used for their efficiency in power tools, material handling equipment, and renewable energy storage solutions. In industrial applications, battery technologies are often chosen based on their durability, cost-effectiveness, and ability to withstand harsh working conditions. Nickel-cadmium and nickel-metal hydride batteries are sometimes used for specialized industrial applications due to their robust performance in high-temperature environments and their capacity to handle deep discharge cycles. The growth of energy storage systems and automation in industries is further fueling the demand for advanced battery technologies, particularly lithium-ion.

Secondary Batteries Market: Regional Insights

- North America is expected to dominate the global market

North America is the dominant region in the Secondary Batteries Market, particularly driven by the United States, which leads the market in terms of both demand and technological advancements. The United States is the primary contributor, with the increasing adoption of secondary batteries in sectors such as electric vehicles (EVs), consumer electronics, and renewable energy storage systems. The rise of electric mobility, led by companies like Tesla and Rivian, has notably driven the demand for high-capacity lithium-ion and solid-state batteries. Additionally, advancements in battery technology, such as longer-lasting batteries, fast-charging capabilities, and improvements in energy density, are driving growth in the region. Canada is also contributing to the market growth with initiatives aimed at improving energy storage solutions for electric grid systems and developing cleaner energy technologies. North America's market is further supported by substantial investments in battery manufacturing facilities, with major players like Tesla, LG Chem, and Panasonic expanding their operations in the region.

Europe is another key region for the Secondary Batteries Market, with a strong focus on the transition to electric mobility and renewable energy systems. Germany, France, and the United Kingdom are at the forefront of this transition. Germany, home to automakers like Volkswagen, BMW, and Mercedes-Benz, has been actively investing in battery technology to meet the rising demand for electric vehicles (EVs). The European Union's commitment to sustainability and decarbonization is fueling the demand for secondary batteries, particularly lithium-ion batteries, in electric vehicle manufacturing, grid energy storage, and consumer electronics. The growth of battery production facilities in Europe, such as the Northvolt gigafactory in Sweden, is also contributing to regional expansion. The region is also focused on reducing reliance on imports for critical raw materials like lithium and cobalt, which is driving local production and technological innovation in secondary battery systems. Furthermore, Europe’s stringent regulations on emissions and its goal to achieve carbon neutrality by 2050 are key factors pushing the adoption of energy storage systems and electric vehicles, thus supporting market growth.

Asia-Pacific is the largest and fastest-growing region for the Secondary Batteries Market, led by the dominance of countries like China, Japan, and South Korea. China is the global leader in battery manufacturing, with a substantial market share driven by its large-scale production of lithium-ion batteries for electric vehicles, consumer electronics, and renewable energy systems. The country’s ambitious electric vehicle adoption goals and investment in battery technologies are driving demand for secondary batteries. Japan has a strong presence in battery manufacturing, with major companies like Panasonic, Sony, and LG Energy Solution at the forefront of innovation. South Korea, home to battery giants like Samsung SDI and LG Chem, is another key player, particularly in the electric vehicle sector, where demand for high-performance, long-lasting batteries is increasing. Additionally, India is emerging as a significant market for secondary batteries, with rising adoption of electric vehicles, renewable energy storage systems, and consumer electronics. As the region continues to advance in electric mobility and energy storage technologies, the demand for secondary batteries, particularly lithium-ion and next-generation technologies, is expected to grow significantly.

Latin America, the Secondary Batteries Market is showing steady growth, driven by increasing demand for electric vehicles and energy storage solutions in countries like Brazil, Mexico, and Argentina. Brazil, as the largest economy in the region, is investing heavily in renewable energy and electric mobility. The country’s growing interest in electric buses and commercial electric vehicles is contributing to the rise in demand for secondary batteries. Mexico is also experiencing growth due to its proximity to the U.S. and its role in the global supply chain for automotive manufacturing, especially in electric vehicle production. The adoption of solar energy systems in Latin America is further pushing the demand for stationary energy storage solutions, where secondary batteries play a critical role. Additionally, increasing government incentives and policies that support green technologies, including electric vehicles and renewable energy, are likely to drive the growth of the market in the region. However, the market faces challenges due to high import taxes and limited local manufacturing capabilities in some countries.

Middle East and Africa region represents an emerging market for Secondary Batteries, with growth primarily driven by the demand for electric vehicles and energy storage systems in countries like the United Arab Emirates (UAE), Saudi Arabia, and South Africa. The UAE, particularly Dubai, is heavily investing in electric mobility and sustainability, leading to an increasing demand for secondary batteries. Saudi Arabia is also focused on diversifying its economy and has plans to invest in electric vehicles and renewable energy, pushing for growth in the energy storage market. South Africa, as the largest economy in Africa, is showing increased interest in secondary batteries due to the adoption of renewable energy and off-grid solar systems. However, the market in MEA is still developing, with growth dependent on infrastructure investments, government policies, and increasing consumer awareness regarding electric vehicles and renewable energy solutions.

Secondary Batteries Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the secondary batteries market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global secondary batteries market include:

- Amperex Technologies

- BYD

- LG

- Samsung

- Johnson Controls

- Tosoh

- Prince

The global secondary batteries market is segmented as follows:

By Product

- Lead Acid

- Lithium-Ion (Li-Ion)

- Nickel-Cadmium (Ni-Cd)

- Nickel Metal Hydride

- Others

By Application

- Automotive

- Household

- Industrial

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Secondary Batteries

Request Sample

Secondary Batteries