Semiconductor And Related Devices Market Size, Share, and Trends Analysis Report

CAGR :

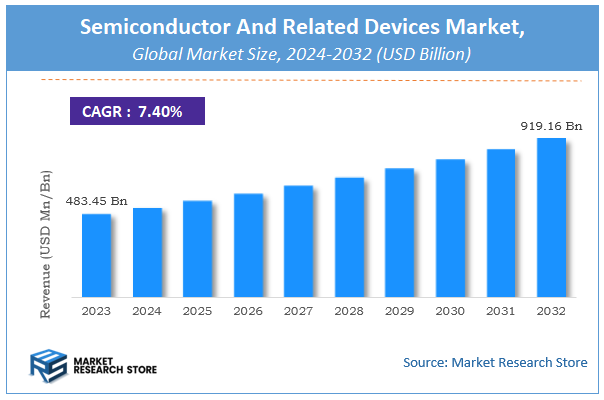

| Market Size 2023 (Base Year) | USD 483.45 Billion |

| Market Size 2032 (Forecast Year) | USD 919.16 Billion |

| CAGR | 7.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Semiconductor And Related Devices Market Insights

According to Market Research Store, the global semiconductor and related devices market size was valued at around USD 483.45 billion in 2023 and is estimated to reach USD 919.16 billion by 2032, to register a CAGR of approximately 7.4% in terms of revenue during the forecast period 2024-2032.

The semiconductor and related devices report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Semiconductor And Related Devices Market: Overview

Semiconductors are materials with electrical conductivity between that of conductors and insulators, making them ideal for controlling electrical current in modern electronic devices. Semiconductor and related devices include a wide range of components such as integrated circuits (ICs), transistors, diodes, sensors, microprocessors, and optoelectronic devices like LEDs and laser diodes. These devices form the backbone of modern electronics, enabling functionality in everything from smartphones, computers, and automobiles to medical equipment and industrial automation systems.

Key Highlights

- The semiconductor and related devices market is anticipated to grow at a CAGR of 7.4% during the forecast period.

- The global semiconductor and related devices market was estimated to be worth approximately USD 483.45 billion in 2023 and is projected to reach a value of USD 919.16 billion by 2032.

- The growth of the semiconductor and related devices market is being driven by increasing demand for advanced electronics, technological innovations, and the widespread adoption of smart devices and Internet of Things (IoT) technologies.

- Based on the type of semiconductor, the digital semiconductors segment is growing at a high rate and is projected to dominate the market.

- On the basis of device type, the integrated circuits (ICs) segment is projected to swipe the largest market share.

- In terms of application, the consumer electronics segment is expected to dominate the market.

- Based on the material type, the silicon segment is expected to dominate the market.

- On the basis of technology, the wafer fabrication segment is projected to swipe the largest market share.

- By region, Asia-Pacific is expected to dominate the global market during the forecast period.

Semiconductor And Related Devices Market: Dynamics

Key Growth Drivers:

- Increasing Demand for Consumer Electronics: The ever-rising consumption of smartphones, laptops, wearables, and other electronic gadgets necessitates a large volume of semiconductors. These devices constantly require more advanced and efficient chips.

- Growth of Artificial Intelligence (AI) and Machine Learning (ML): The widespread adoption of AI and ML across various industries (healthcare, automotive, finance, etc.) drives significant demand for high-performance computing chips, including GPUs and specialized AI processors.

- Rising Adoption of Electric Vehicles (EVs) and Advanced Driver-Assistance Systems (ADAS): EVs require a significantly higher number of semiconductors compared to traditional vehicles for battery management, powertrains, sensors, and ADAS, fueling market growth.

- Expansion of 5G and Internet of Things (IoT): The global rollout of 5G networks and the proliferation of connected IoT devices across homes, industries, and cities are increasing the demand for various types of semiconductors for communication, processing, and sensing.

- Growing Importance of Data Centers and Cloud Computing: The increasing reliance on cloud services and the massive data generation necessitate the development and deployment of powerful semiconductors for data processing, storage, and networking within data centers.

Restraints:

- High Capital Costs and Long Development Cycles: Setting up semiconductor fabrication plants (fabs) and investing in research and development for advanced chip technologies require substantial upfront capital and involve lengthy development and production cycles.

- Complex and Geopolitically Sensitive Supply Chain: The semiconductor industry relies on a complex global supply chain for raw materials, manufacturing equipment, and specialized processes. Geopolitical tensions and trade disputes can create significant disruptions and uncertainties.

- Shortage of Skilled Labor: The industry faces a growing shortage of specialized talent in areas like chip design, manufacturing, and materials science, which can hinder growth and innovation.

- Cyclical Nature of the Industry: The semiconductor market is historically cyclical, experiencing periods of high demand and supply shortages followed by oversupply and price declines, creating revenue volatility.

- Increasing Complexity and Cost of Advanced Nodes: As chip manufacturing technology advances to smaller nodes (e.g., 3nm, 2nm), the complexity and cost of design and fabrication increase exponentially, posing challenges for profitability and accessibility.

Opportunities:

- Government Incentives and Support: Many governments worldwide are offering substantial incentives, subsidies, and tax breaks to encourage domestic semiconductor manufacturing and research to enhance supply chain resilience and technological leadership.

- Growth in Emerging Markets: The increasing adoption of electronics and digital services in developing economies presents a significant growth opportunity for semiconductor consumption.

- Demand for Specialized Chips: The trend towards domain-specific architectures and the need for optimized performance in applications like AI, automotive, and edge computing create opportunities for specialized chip design and manufacturing.

- Advancements in Packaging Technologies: Innovations in advanced packaging technologies (e.g., chiplets, 3D stacking) offer opportunities to improve performance, reduce power consumption, and enhance integration capabilities of semiconductor devices.

- Increasing Focus on Energy Efficiency and Sustainability: The growing environmental concerns drive demand for power-efficient semiconductors and sustainable manufacturing processes, creating opportunities for innovation in these areas.

Challenges:

- Maintaining Pace with Rapid Technological Advancements: The semiconductor industry is characterized by rapid technological evolution, requiring continuous investment in R&D and infrastructure upgrades to remain competitive.

- Ensuring Supply Chain Resilience and Diversification: Reducing reliance on geographically concentrated suppliers and diversifying the supply chain to mitigate geopolitical risks and natural disasters is a significant challenge.

- Protecting Intellectual Property (IP): The high value of semiconductor designs and manufacturing processes makes IP protection crucial, and the industry faces ongoing challenges related to IP theft and patent disputes.

- Addressing Environmental Concerns: The semiconductor manufacturing process is resource-intensive, with high water and energy consumption and the generation of hazardous waste, necessitating the adoption of more sustainable practices.

- Adapting to Evolving Regulatory Landscapes: Changes in trade policies, export controls, and environmental regulations can significantly impact the semiconductor market, requiring companies to adapt their strategies and operations.

Semiconductor And Related Devices Market: Report Scope

This report thoroughly analyzes the semiconductor and related devices market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Semiconductor And Related Devices Market |

| Market Size in 2023 | USD 483.45 Billion |

| Market Forecast in 2032 | USD 919.16 Billion |

| Growth Rate | CAGR of 7.4% |

| Number of Pages | 150 |

| Key Companies Covered | Broadcom Inc., Samsung Electronics, Intel Corporation, Maxim Integrated Products Inc., Taiwan Semiconductors (Taiwan), Micron Technology, NXP Semiconductors N.V., NVIDIA Corporation, Qualcomm, SK Hynix, Texas Instruments, Toshiba Corporation |

| Segments Covered | By Type of Semiconductor, By Device Type, By Application, By Material Type, By Technology, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Semiconductor And Related Devices Market: Segmentation Insights

The global semiconductor and related devices market is divided by type of semiconductor, device type, application, material type, technology, and region.

Segmentation Insights by Type of Semiconductor

Based on type of semiconductor, the global semiconductor and related devices market is divided into analog semiconductors, digital semiconductors, mixed-signal semiconductors, optoelectronic semiconductors, and power semiconductors.

In the semiconductor and related devices market, the digital semiconductors segment is the most dominant. Digital semiconductors are the backbone of computing systems, including microprocessors, memory chips (such as DRAM and NAND), and digital signal processors (DSPs). Their widespread application in consumer electronics, mobile devices, data centers, and cloud computing infrastructure has led to their significant market dominance. The rise of artificial intelligence, IoT, and 5G has further fueled demand for high-performance digital chips, making this segment the leading contributor to the overall semiconductor market.

Following digital semiconductors, analog semiconductors form the next most significant segment. Analog chips are essential for interpreting real-world signals like sound, light, temperature, and motion into digital data. They are commonly used in power management systems, automotive electronics, industrial machinery, and communication devices. As more devices require sensing and power control features, analog semiconductors remain crucial for enabling efficient system performance across various industries.

Mixed-signal semiconductors, which combine both analog and digital components on a single chip, hold a strong but smaller share of the market. These semiconductors are vital in applications that need real-time signal processing, such as wireless communication, automotive infotainment systems, and consumer electronics. Their versatility and ability to reduce system complexity and size make them increasingly popular, though their market size is still more niche compared to pure analog or digital chips.

Power semiconductors come next, primarily used in energy conversion and management systems. These are crucial for electric vehicles, industrial motors, renewable energy systems, and power supply units. With the global push for energy efficiency and the transition to electric transportation, power semiconductors are gaining traction but still trail behind digital and analog segments in overall market share.

Finally, optoelectronic semiconductors represent the smallest segment. These devices involve the interaction of light with semiconductors and include components such as LEDs, image sensors, and laser diodes. They are widely used in consumer electronics (like smartphone cameras), optical communication systems, and lighting. Despite their specialized applications and growing demand in sectors like healthcare and automotive (e.g., LiDAR for autonomous vehicles), their market size remains more limited compared to other semiconductor types.

Segmentation Insights by Device Type

On the basis of device type, the global semiconductor and related devices market is bifurcated into integrated circuits (ICs), discrete semiconductors, optoelectronic devices, microelectromechanical systems (MEMS), and sensors.

In the semiconductor and related devices market, Integrated Circuits (ICs) are the most dominant device type. ICs combine numerous transistors, resistors, and capacitors onto a single chip, enabling complex computing and processing functions. They are essential in virtually all modern electronic devices, including computers, smartphones, automotive systems, industrial machines, and communication infrastructure. The wide-ranging application of ICs—such as microcontrollers, microprocessors, memory chips, and logic ICs—drives their dominance, especially with growing demand for AI, 5G, cloud computing, and consumer electronics.

Next in line are sensors, which play a crucial role in detecting and converting physical inputs like temperature, motion, light, and pressure into electrical signals. Sensors are increasingly embedded in a wide range of products across sectors such as automotive (for ADAS and safety systems), consumer electronics (like smart wearables and home automation), healthcare devices, and industrial IoT solutions. Their ability to enable smart and connected technologies keeps them in high demand and steadily growing in market share.

Discrete semiconductors come next, comprising individual components like diodes, transistors, and thyristors. These are essential for basic functions such as signal amplification, switching, and voltage regulation. While less complex than ICs, discrete semiconductors are foundational in power electronics, automotive systems, telecommunications, and industrial control applications. Their utility in high-power and high-frequency applications keeps them relevant, although their market size is smaller compared to ICs.

Optoelectronic devices follow, leveraging the interaction between light and electricity. These include components such as photodiodes, laser diodes, LEDs, and optical sensors. Optoelectronics are crucial for applications in optical communication, display technologies, medical imaging, and lighting. Despite their technological importance and niche growth areas (like LiDAR and fiber-optics), their share is relatively limited due to narrower application scope compared to ICs and sensors.

Finally, Microelectromechanical Systems (MEMS) make up the smallest segment. MEMS are miniaturized mechanical and electro-mechanical devices integrated into semiconductor chips, often used for accelerometers, gyroscopes, pressure sensors, and microphones. MEMS are vital for smartphones, automotive electronics, and wearable devices. However, their market size remains comparatively smaller due to their specialized usage and integration challenges, although their importance is growing with the expansion of smart and compact technologies.

Segmentation Insights by Application

Based on application, the global semiconductor and related devices market is divided into consumer electronics, automotive, telecommunications, healthcare, and industrial automation.

In the semiconductor and related devices market, consumer electronics is the most dominant application segment. This sector encompasses devices like smartphones, laptops, tablets, gaming consoles, smart TVs, and wearable tech—all of which heavily rely on a wide range of semiconductors, including processors, memory chips, sensors, and power management ICs. The constant demand for more powerful, energy-efficient, and compact devices fuels innovation and high-volume production in this segment. The consumer electronics market’s rapid refresh cycles and global penetration contribute significantly to the dominant position of semiconductors in this space.

Automotive comes next, rapidly emerging as a key growth driver for semiconductors. Modern vehicles are increasingly becoming electronic systems on wheels, with semiconductors playing a central role in everything from engine control units (ECUs) and infotainment systems to advanced driver-assistance systems (ADAS) and electric powertrains. The push toward electric vehicles (EVs) and autonomous driving technology has intensified the demand for specialized automotive-grade semiconductors, making this one of the fastest-growing applications in the market.

Telecommunications is another major application area, particularly with the global rollout of 5G infrastructure. Semiconductors are crucial for the functioning of base stations, network equipment, modems, and mobile devices. They enable high-speed data transfer, signal processing, and connectivity. The surge in mobile data consumption, cloud computing, and edge computing continues to drive demand for advanced chips in this sector, although it trails slightly behind consumer electronics and automotive in market share.

Healthcare follows, with increasing reliance on semiconductors for medical devices such as imaging systems (like MRI and CT scanners), diagnostic tools, wearable health monitors, and implantable devices. The integration of AI, telemedicine, and remote patient monitoring is expanding semiconductor use in this field. Although smaller in comparison to the previously mentioned sectors, healthcare is a high-value market where reliability, precision, and innovation are critical.

Industrial automation represents the smallest application segment, but it is steadily growing due to the advancement of smart manufacturing and Industry 4.0. Semiconductors in this space are used in robotics, process control systems, sensors, and industrial IoT devices. While its overall volume is lower than consumer or automotive electronics, the long product lifecycles and demand for durability and precision drive steady growth.

Segmentation Insights by Material Type

On the basis of material type, the global semiconductor and related devices market is bifurcated into silicon, gallium arsenide, silicon carbide, gallium nitride, and other compound semiconductors.

In the semiconductor and related devices market, silicon is by far the most dominant material type. Silicon has been the cornerstone of the semiconductor industry for decades due to its abundance, cost-effectiveness, and well-established manufacturing infrastructure. It is the primary material used in the production of integrated circuits, memory chips, processors, and power devices. Silicon’s versatility and mature fabrication ecosystem make it ideal for mass production across a wide range of applications, from consumer electronics and automotive systems to industrial controls and telecommunications.

Next in the hierarchy is gallium arsenide (GaAs), which holds a significant but smaller share compared to silicon. GaAs is prized for its superior electron mobility and ability to operate at high frequencies, making it ideal for RF (radio frequency) and microwave applications. It is widely used in mobile phones, satellite communications, and radar systems. While more expensive and less abundant than silicon, GaAs continues to serve critical roles where high-speed and high-frequency performance is necessary.

Silicon carbide (SiC) is gaining traction, particularly in power electronics. SiC semiconductors offer high thermal conductivity, wide bandgap energy, and the ability to operate at high voltages and temperatures. These properties make SiC highly suitable for electric vehicles (especially in inverters and onboard chargers), renewable energy systems, and industrial motor drives. While still relatively niche, SiC is growing quickly due to the push for energy efficiency and electrification.

Following closely is gallium nitride (GaN), another wide bandgap material that is rapidly emerging in high-power, high-efficiency applications. GaN is favored for its high breakdown voltage and fast switching capabilities, which make it ideal for RF amplifiers, power converters, and 5G base stations. GaN devices are increasingly used in data centers, EVs, and consumer fast chargers, though they are still in an earlier phase of market adoption compared to SiC.

Segmentation Insights by Technology

On the basis of technology, the global semiconductor and related devices market is bifurcated into wafer fabrication, die packaging, testing and inspection technologies, assembly technologies, design software and tools.

In the semiconductor and related devices market, wafer fabrication is the most dominant technology segment. This stage involves the intricate process of creating semiconductor devices on silicon wafers through photolithography, doping, etching, and deposition. As the foundation of chip manufacturing, wafer fabrication is capital- and technology-intensive, requiring cutting-edge cleanroom environments and advanced equipment. Given its central role in defining chip performance, power efficiency, and miniaturization, wafer fabrication accounts for the largest share of investment and technological innovation in the semiconductor ecosystem.

Die packaging follows as the next significant segment. Once the semiconductor dies are fabricated, they need to be packaged to protect them from environmental damage and to facilitate electrical connections. Advanced packaging techniques—such as system-in-package (SiP), 3D packaging, and chiplet integration—are gaining traction to meet the growing demand for smaller, more efficient, and higher-performing devices. The evolution of packaging has become a critical factor in enhancing device performance and thermal management, making this a vital, growing area of the market.

Testing and inspection technologies come next. These technologies are essential throughout the manufacturing process to ensure the reliability, quality, and functionality of semiconductor devices. As chips become smaller and more complex, the need for precise and comprehensive testing—from wafer-level to final product—has become more important than ever. Advanced inspection systems using AI, machine learning, and optical/e-beam techniques help detect defects early, reducing waste and ensuring product integrity.

Assembly technologies follow, focusing on physically assembling the packaged dies into their final form—whether as part of a device, module, or printed circuit board (PCB). Assembly involves processes such as wire bonding, die attachment, and soldering. While essential, this segment typically involves more mature and standardized processes, giving it a relatively smaller market share compared to fabrication and packaging.

Design software and tools make up the smallest yet highly strategic segment. These electronic design automation (EDA) tools are used to design and simulate semiconductor devices before fabrication. They are critical for ensuring chip functionality, optimizing layout, and reducing time-to-market. Although this segment represents a smaller portion of total market revenue, it plays a pivotal role in innovation and productivity, especially as chip architectures grow more complex.

Semiconductor And Related Devices Market: Regional Insights

- Asia-Pacific is expected to dominates the global market

Asia-Pacific is the most dominant region in the global semiconductor and related devices market. Its leadership is driven by strong manufacturing hubs in countries like China, South Korea, Taiwan, and Japan. These nations host major fabrication facilities and are home to leading chipmakers that supply components for smartphones, computers, industrial machinery, and automotive electronics. The rapid adoption of technologies such as AI, 5G, IoT, and electric vehicles has significantly increased the demand for semiconductors in this region. Additionally, government initiatives and strategic investments in semiconductor infrastructure further strengthen its global position.

North America follows closely behind, driven primarily by the United States, which is home to several of the world’s largest semiconductor design and manufacturing companies. The region benefits from a highly advanced R&D ecosystem and strong integration of semiconductors in high-tech industries such as aerospace, defense, and cloud computing. Increased demand for high-performance computing, data centers, and automotive technologies continues to fuel growth in this market. Strategic onshoring efforts and investment in domestic chip production have also been key trends in recent years.

Europe holds a significant position in the semiconductor market, largely supported by demand from the automotive and industrial automation sectors. Countries like Germany, France, and the Netherlands are leading contributors, with a focus on developing advanced automotive electronics, energy-efficient chips, and telecom infrastructure. Government backing through subsidies and partnerships has encouraged semiconductor innovation and domestic production. Europe is also investing in developing sovereign capabilities to reduce dependency on external supply chains.

Rest of the World, including Latin America, the Middle East, and Africa, is showing gradual but steady growth in the semiconductor market. Although not yet as dominant as other regions, the increasing penetration of smart technologies, industrial digitization, and investments in infrastructure are driving demand. In Latin America, the rise of digital devices and gaming has elevated the need for processing components. Meanwhile, Middle Eastern nations are adopting smart manufacturing technologies as part of broader economic diversification plans, gradually creating opportunities in semiconductor-related sectors.

Semiconductor And Related Devices Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the semiconductor and related devices market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global semiconductor and related devices market include:

- Broadcom Inc.

- Samsung Electronics

- Intel Corporation

- Maxim Integrated Products Inc.

- Taiwan Semiconductors (Taiwan)

- Micron Technology

- NXP Semiconductors N.V.

- NVIDIA Corporation

- Qualcomm

- SK Hynix

- Texas Instruments

- Toshiba Corporation

The global semiconductor and related devices market is segmented as follows:

By Type of Semiconductor

- Analog Semiconductors

- Digital Semiconductors

- Mixed-Signal Semiconductors

- Optoelectronic Semiconductors

- Power Semiconductors

By Device Type

- Integrated Circuits (ICs)

- Discrete Semiconductors

- Optoelectronic Devices

- Microelectromechanical Systems (MEMS)

- Sensors

By Application

- Consumer Electronics

- Automotive

- Telecommunications

- Healthcare

- Industrial Automation

By Material Type

- Silicon

- Gallium Arsenide

- Silicon Carbide

- Gallium Nitride

- Other Compound Semiconductors

By Technology

- Wafer Fabrication

- Die Packaging

- Testing and Inspection Technologies

- Assembly Technologies

- Design Software and Tools

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Semiconductor And Related Devices

Request Sample

Semiconductor And Related Devices