Sensors and MEMS Market Size, Share, and Trends Analysis Report

CAGR :

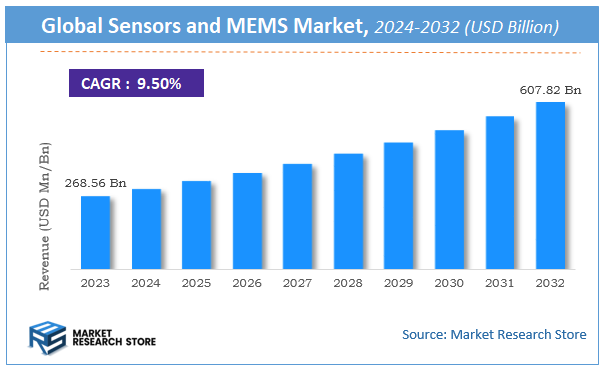

| Market Size 2023 (Base Year) | USD 268.56 Billion |

| Market Size 2032 (Forecast Year) | USD 607.82 Billion |

| CAGR | 9.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Sensors and MEMS Market Insights

According to Market Research Store, the global sensors and MEMS market size was valued at around USD 268.56 billion in 2023 and is estimated to reach USD 607.82 billion by 2032, to register a CAGR of approximately 9.5% in terms of revenue during the forecast period 2024-2032.

The sensors and MEMS report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032

To Get more Insights, Request a Free Sample

Global Sensors and MEMS Market: Overview

Sensors are devices that detect and respond to various physical stimuli such as temperature, pressure, motion, light, or chemical composition and convert them into readable signals for monitoring or control. MEMS (Micro-Electro-Mechanical Systems) are miniature devices that integrate mechanical and electrical components at the microscale. MEMS technology is used to fabricate sensors that are compact, efficient, and capable of high precision. These include accelerometers, gyroscopes, pressure sensors, and microphones. MEMS sensors are integral to various applications, including consumer electronics, automotive systems, healthcare devices, industrial automation, and aerospace systems. Their small size, low power consumption, and high functionality make them ideal for modern, compact, and interconnected technologies.

Key Highlights

- The sensors and MEMS market is anticipated to grow at a CAGR of 9.5% during the forecast period.

- The global sensors and MEMS market was estimated to be worth approximately USD 268.56 billion in 2023 and is projected to reach a value of USD 607.82 billion by 2032.

- The growth of the sensors and MEMS market is being driven by the rising demand for smart devices, IoT integration, and automation across industries. Increasing adoption of consumer electronics like smartphones and wearables.

- Based on the sensor type, the accelerometers segment is growing at a high rate and is projected to dominate the market.

- On the basis of technology, the micro-electro-mechanical systems (MEMS) segment is projected to swipe the largest market share.

- In terms of configuration, the multi-axis sensors segment is expected to dominate the market.

- Based on the application, the consumer electronics segment is expected to dominate the market.

- In terms of end user, the OEMs (Original Equipment Manufacturers) segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Sensors and MEMS Market: Dynamics

Key Growth Drivers:

- Rising Demand for Smart Consumer Electronics: Growing adoption of smartphones, tablets, wearables, and smart home devices is fueling the demand for sensors and MEMS that enable motion sensing, pressure detection, and environmental monitoring.

- Growth in Automotive Applications: Modern vehicles increasingly rely on MEMS-based sensors for applications like tire pressure monitoring, airbag deployment, stability control, and autonomous driving systems.

- Miniaturization and Integration Capabilities: The ability of MEMS to combine mechanical elements, sensors, actuators, and electronics on a single chip supports compact, energy-efficient, and cost-effective solutions.

- Expansion of IoT Ecosystems: Internet of Things (IoT) applications across industries such as healthcare, agriculture, and industrial automation are driving the need for advanced sensing technologies.

- Healthcare and Medical Innovations: Wearable health monitoring devices and diagnostic equipment are leveraging sensors and MEMS for real-time data collection and patient monitoring.

Restraints:

- High Initial Development and Production Costs: The design, fabrication, and testing of MEMS devices require significant investment, which may be a barrier for new entrants or small companies.

- Packaging and Integration Challenges: Ensuring mechanical robustness and long-term reliability of MEMS devices during packaging and integration into final products remains a technical challenge.

- Complex Manufacturing Process: The precision and complexity involved in manufacturing MEMS can lead to lower yields and longer development cycles.

Opportunities:

- Emergence of 5G and Advanced Connectivity: The rollout of 5G networks is expected to accelerate demand for high-performance sensors and MEMS in mobile and connected devices.

- Proliferation of Autonomous Systems: Robotics, drones, and autonomous vehicles require advanced sensing capabilities for navigation, object detection, and environmental awareness, presenting growth potential for MEMS.

- Smart Cities and Infrastructure Projects: Government initiatives toward building smart cities are opening new avenues for environmental monitoring, traffic control, and utility management using sensor technologies.

- Industrial Automation and Industry 4.0: Increasing use of sensors and MEMS in smart factories for predictive maintenance, quality control, and process optimization is driving market expansion.

Challenges:

- Standardization and Compatibility Issues: Lack of universal standards for MEMS design and communication protocols may hinder large-scale deployment across different industries.

- Sensor Calibration and Accuracy Concerns: Maintaining accuracy over time and under varying environmental conditions is a major concern in mission-critical applications.

- Data Privacy and Security Risks: As sensors become more embedded in daily life and industrial systems, concerns around data privacy and cyber threats are becoming more prominent.

- Supply Chain Disruptions: Global semiconductor shortages and geopolitical tensions can impact the timely availability and cost of raw materials and components used in MEMS manufacturing.

Sensors and MEMS Market: Report Scope

This report thoroughly analyzes the Sensors and MEMS Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Sensors and MEMS Market |

| Market Size in 2023 | USD 268.56 Billion |

| Market Forecast in 2032 | USD 607.82 Billion |

| Growth Rate | CAGR of 9.5% |

| Number of Pages | 171 |

| Key Companies Covered | Robert Bosch, Honeywell International, HP, STMicroelectronics, Texas Instruments, InvenSense |

| Segments Covered | By Sensor Type, By Technology, By Application, By End User, By Configuration, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Sensors and MEMS Market: Segmentation Insights

The global sensors and MEMS market is divided by sensor type, technology, configuration, application, end user, and region.

Segmentation Insights by Sensor Type

Based on sensor type, the global sensors and MEMS market is divided into temperature sensors, pressure sensors, accelerometers, gyroscopes, magnetic sensors, optical sensors, chemical sensors, proximity sensors, and flow sensors.

In the Sensors and MEMS market, accelerometers stand out as the most dominant segment due to their widespread use in consumer electronics, automotive safety systems (such as airbag deployment), and industrial monitoring. These sensors are critical in detecting motion, tilt, vibration, and shock, making them integral in smartphones, wearable devices, and automotive safety solutions. The miniaturization and low power consumption of MEMS-based accelerometers have fueled their integration into compact and portable electronic products.

Following closely are gyroscopes, which are often paired with accelerometers in Inertial Measurement Units (IMUs) for applications that require precise orientation and angular velocity measurements. Their importance has grown with the advancement of technologies such as virtual reality (VR), augmented reality (AR), drones, and autonomous vehicles, all of which require accurate motion tracking and navigation.

Pressure sensors also occupy a significant share of the market, especially in automotive, medical, and industrial sectors. In vehicles, they monitor tire pressure, engine performance, and HVAC systems. In the medical field, they're used in devices like ventilators and blood pressure monitors, while in industry, they support process automation and environmental monitoring.

Temperature sensors are widely used across various applications—from smartphones and computers to industrial automation and HVAC systems. While they are ubiquitous, their comparatively simpler functionality and lower cost place them slightly behind pressure sensors in terms of market value. However, demand remains strong due to the essential role temperature monitoring plays in ensuring device reliability and user safety.

Optical sensors are gaining momentum, particularly with the rising demand for advanced driver-assistance systems (ADAS), biometric systems, and industrial automation. These sensors detect light and translate it into an electronic signal, proving useful in proximity detection, ambient light sensing, and optical character recognition.

Magnetic sensors, used in position sensing, speed detection, and current sensing, play a key role in automotive and industrial applications. Hall effect sensors and magnetometers are typical examples, with usage in everything from anti-lock braking systems to electronic compasses in smartphones.

Proximity sensors are essential in automation and mobile devices, providing object detection capabilities without physical contact. They are vital in industrial robotics, touchless interfaces, and smartphones (e.g., turning off the screen when the phone is near the ear). Despite their usefulness, their market size is slightly smaller compared to motion and environmental sensors.

Chemical sensors are more niche and primarily used in environmental monitoring, industrial safety systems, and healthcare applications such as gas detection and glucose monitoring. Their market presence is growing but remains smaller due to more specialized use cases and complex integration needs.

At the bottom in terms of market share are flow sensors, which measure the rate of fluid or gas movement. While they are critical in industries like water management, pharmaceuticals, and automotive, their adoption is more application-specific, leading to a relatively lower market dominance compared to the more versatile sensor types.

Segmentation Insights by Technology

On the basis of technology, the global sensors and MEMS market is bifurcated into micro-electro-mechanical systems (MEMS), bulk acoustic wave (BAW), surface acoustic wave (SAW), and optical sensors technology.

In the Sensors and MEMS market, Micro-Electro-Mechanical Systems (MEMS) technology is the most dominant segment, largely due to its versatility, compactness, and low power consumption. MEMS sensors are widely used across various industries, including consumer electronics, automotive, industrial automation, and healthcare. Their ability to integrate mechanical elements, sensors, actuators, and electronics on a single silicon chip allows for miniaturized, cost-effective, and high-performance devices. MEMS technology powers a wide range of sensor types—such as accelerometers, gyroscopes, pressure sensors, and microphones—making it the backbone of modern sensing applications in smartphones, wearables, and advanced driver-assistance systems (ADAS).

Following MEMS is Bulk Acoustic Wave (BAW) technology, which is increasingly adopted in high-frequency filtering applications, particularly in telecommunications. BAW sensors are favored for their high performance in harsh environments and ability to operate at higher frequencies than traditional MEMS sensors. This makes them ideal for RF filters in smartphones and IoT devices, where reliable and fast wireless communication is essential.

Surface Acoustic Wave (SAW) technology comes next, with applications in touchscreens, wireless sensors, and radio frequency filters. SAW sensors are especially valued in industrial and medical fields due to their ability to function wirelessly and passively, without the need for external power sources. Though not as pervasive as MEMS or BAW technologies, SAW sensors are gaining attention for niche applications where ruggedness and wireless operation are critical.

Lastly, Optical Sensors Technology holds a smaller share in comparison but is rapidly growing due to increasing demand in areas such as biometric authentication, environmental monitoring, and industrial automation. Optical sensors offer high sensitivity and fast response times, making them suitable for precise measurements of light, distance, and chemical properties. However, the higher cost and complexity of integration relative to MEMS have limited their dominance in mass-market applications.

Segmentation Insights by Configuration

Based on configuration, the global sensors and MEMS market is divided into single axis sensors, multi-axis sensors, and combined sensors.

In the Sensors and MEMS market by configuration, Multi-Axis Sensors hold the most dominant position. These sensors are capable of detecting movement or orientation along two or more axes (commonly 3-axis or 6-axis), making them ideal for complex motion sensing applications. They are widely used in smartphones, drones, gaming controllers, virtual reality systems, and automotive applications such as electronic stability control and navigation. Their ability to provide comprehensive data from a single unit has led to their widespread adoption, especially as devices become smarter and more compact. The increasing integration of multi-axis sensors into Internet of Things (IoT) devices further boosts their market leadership.

Combined Sensors, which integrate multiple types of sensing elements—such as accelerometers with gyroscopes or magnetometers—into a single package, follow closely behind. These configurations offer enhanced functionality and data fusion capabilities, making them essential for advanced applications like inertial navigation systems, autonomous vehicles, and industrial automation. The demand for higher precision and multifunctional sensing in compact forms is fueling the growth of combined sensors, especially in wearables and robotics.

Single Axis Sensors are the least dominant segment, primarily because their functionality is limited to one direction or dimension. While they are still important in applications where only basic motion or measurement is needed—such as vibration monitoring, simple positioning systems, or low-cost consumer devices—they are increasingly being replaced by multi-axis alternatives that offer more value and data in a smaller footprint. However, due to their simplicity, low cost, and ease of integration, single axis sensors continue to be used in cost-sensitive or legacy systems.

Segmentation Insights by Application

On the basis of application, the global sensors and MEMS market is bifurcated into automotive, consumer electronics, industrial automation, healthcare, and aerospace.

In the Sensors and MEMS market by application, Consumer Electronics represents the most dominant segment. The explosive growth in smartphones, tablets, wearable devices, and smart home technologies has significantly driven demand for sensors such as accelerometers, gyroscopes, pressure sensors, proximity sensors, and temperature sensors. MEMS sensors are integral to enabling features like screen rotation, gesture recognition, step counting, biometric authentication, and environmental monitoring. As consumers increasingly adopt IoT-enabled and multifunctional devices, the need for compact, low-power, and cost-effective sensors in this sector continues to rise.

Automotive follows closely, driven by advancements in vehicle safety, efficiency, and automation. Sensors play a pivotal role in systems such as airbag deployment, tire pressure monitoring, engine management, and advanced driver-assistance systems (ADAS). The trend toward electric vehicles (EVs) and autonomous driving has further increased the complexity and number of sensors required per vehicle. MEMS and other sensor technologies support key automotive innovations like in-cabin monitoring, adaptive cruise control, and lane-keeping systems.

Industrial Automation is another significant application area, where sensors are critical for monitoring, control, and predictive maintenance across manufacturing processes. Pressure, temperature, proximity, flow, and vibration sensors are commonly used in smart factories and industrial IoT applications. The push toward Industry 4.0 has accelerated the adoption of advanced sensor systems that ensure real-time monitoring and operational efficiency in harsh or complex environments.

Healthcare applications are expanding rapidly, although they hold a smaller market share compared to consumer electronics and automotive. Sensors in this domain are essential for patient monitoring, diagnostic devices, wearable health trackers, and surgical tools. MEMS-based pressure sensors, accelerometers, and optical sensors enable innovations like remote health monitoring, smart inhalers, and minimally invasive diagnostics. The pandemic and growing emphasis on preventive healthcare have boosted demand in this sector.

Aerospace represents the least dominant but highly specialized segment. In this field, sensors are used in avionics, navigation, engine performance monitoring, and structural health diagnostics. The extreme environmental conditions and strict regulatory requirements mean that sensors used here must offer exceptional reliability, precision, and durability. While the market size is relatively small due to limited production volumes, the value and sophistication of aerospace sensor systems remain high.

Segmentation Insights by End User

On the basis of end user, the global sensors and MEMS market is bifurcated into OEMs (original equipment manufacturers), aftermarket, research institutions, and government agencies.

In the Sensors and MEMS market by end user, OEMs (Original Equipment Manufacturers) dominate as the primary segment. OEMs integrate sensors directly into their products during the manufacturing process, whether it's smartphones, vehicles, industrial machinery, medical devices, or consumer electronics. Their consistent and large-volume demand for compact, efficient, and cost-effective sensing solutions fuels the majority of sensor shipments worldwide. OEMs are the main drivers of innovation and volume adoption, pushing the need for miniaturized and multifunctional sensors across a wide array of industries.

Next in line is the Aftermarket, which caters to replacement, upgrade, and customization needs once products are sold. This segment is particularly strong in the automotive sector, where consumers and repair shops require replacement sensors for tire pressure, engine control, or vehicle diagnostics. In industrial and consumer electronics, aftermarket sales include sensors used in retrofitting, repairs, or performance upgrades. Though not as large in volume as OEMs, the aftermarket segment is vital for long-term product support and customization.

Research Institutions form a smaller but impactful segment of the market. These institutions play a critical role in developing new sensor technologies, materials, and applications. They often partner with manufacturers or governments to prototype cutting-edge systems, test performance under novel conditions, or explore niche scientific use cases. While not high in volume, their influence on innovation and market direction is significant.

Government Agencies represent the least dominant segment in terms of volume but are key in strategic and high-value applications. These include defense, aerospace, environmental monitoring, and public infrastructure. Sensors used in government applications often require high precision, security, and reliability. Procurement in this segment is typically project-based, focusing on specialized needs such as surveillance, national defense, disaster response, or smart city infrastructure.

Sensors and MEMS Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region is the most dominant in the global sensors and MEMS market, primarily due to its strong manufacturing base and high-volume production of consumer electronics, automotive components, and industrial systems. Countries like China, Japan, South Korea, and Taiwan play a vital role in this dominance through their extensive semiconductor infrastructure and investment in emerging technologies such as electric vehicles, IoT, and smart appliances. The rising adoption of automation in industries and increasing consumer demand for smart devices continue to strengthen the region's leading position.

North America follows closely behind, driven by its advanced technological landscape and the presence of key players in the MEMS and sensor ecosystem. The region benefits from high adoption rates of innovative applications in healthcare, automotive safety, aerospace, and smart homes. Demand for wearable technologies and autonomous vehicles has significantly increased the integration of MEMS sensors across various industries, supported by robust R&D activities and a favorable investment climate.

Europe maintains a substantial share of the sensors and MEMS market, supported by its strong automotive sector, industrial automation, and focus on energy efficiency. Countries such as Germany, France, and the United Kingdom are at the forefront of integrating MEMS technologies into advanced manufacturing and healthcare equipment. The region’s commitment to sustainability, smart infrastructure, and Industry 4.0 initiatives further propels demand for precision sensors and microelectromechanical components.

Latin America is an emerging market for MEMS and sensors, showing gradual adoption in automotive, telecommunications, and consumer electronics. Nations like Brazil and Mexico are making strides in integrating smart technologies, although the pace is slower due to economic and infrastructural limitations. Increasing smartphone penetration and digital transformation initiatives are beginning to open new growth avenues in the region.

Middle East and Africa represents the least dominant region in the global sensors and MEMS market. Growth in this region is primarily driven by adoption in oil and gas, healthcare, and infrastructure sectors. Urbanization and smart city projects are creating demand for sensor-based technologies, but overall market development is hindered by challenges such as limited technical expertise, lower investment in R&D, and relatively slower industrial modernization compared to other regions.

Sensors and MEMS Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the sensors and MEMS market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global sensors and MEMS market include:

- Robert Bosch

- Honeywell International

- HP

- STMicroelectronics

- Texas Instruments

- InvenSense

The global sensors and MEMS market is segmented as follows:

By Sensor Type

- Temperature Sensors

- Pressure Sensors

- Accelerometers

- Gyroscopes

- Magnetic Sensors

- Optical Sensors

- Chemical Sensors

- Proximity Sensors

- Flow Sensors

By Technology

- Micro-Electro-Mechanical Systems (MEMS)

- Bulk Acoustic Wave (BAW)

- Surface Acoustic Wave (SAW)

- Optical Sensors Technology

By Application

- Automotive

- Consumer Electronics

- Industrial Automation

- Healthcare

- Aerospace

By End User

- OEMs (Original Equipment Manufacturers)

- Aftermarket

- Research Institutions

- Government Agencies

By Configuration

- Single Axis Sensors

- Multi-Axis Sensors

- Combined Sensors

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Sensors and MEMS

Request Sample

Sensors and MEMS