Silicon Carbide (Sic) in Semiconductor Market Size, Share, and Trends Analysis Report

CAGR :

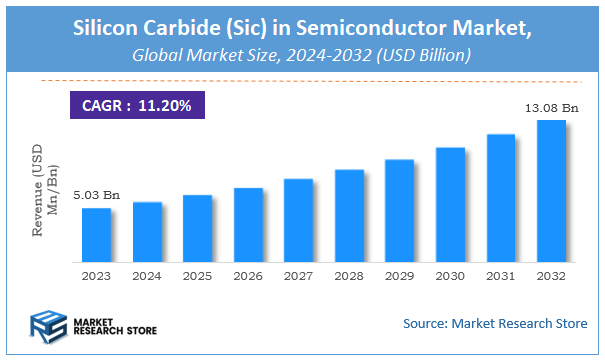

| Market Size 2023 (Base Year) | USD 5.03 Billion |

| Market Size 2032 (Forecast Year) | USD 13.08 Billion |

| CAGR | 11.2% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Silicon Carbide (Sic) in Semiconductor Market Insights

According to Market Research Store, the global silicon carbide (sic) in semiconductor market size was valued at around USD 5.03 billion in 2023 and is estimated to reach USD 13.08 billion by 2032, to register a CAGR of approximately 11.2% in terms of revenue during the forecast period 2024-2032.

The silicon carbide (sic) in semiconductor report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Silicon Carbide (Sic) in Semiconductor Market: Overview

Silicon carbide (SiC) is a wide-bandgap semiconductor material known for its superior electrical and thermal properties compared to traditional silicon. It exhibits high breakdown voltage, excellent thermal conductivity, and low power losses, making it ideal for high-performance applications. SiC is widely used in power electronics, particularly in electric vehicles (EVs), industrial power supplies, renewable energy systems, and telecommunications due to its ability to handle higher voltages, operate at elevated temperatures, and improve energy efficiency.

Key Highlights

- The silicon carbide (sic) in semiconductor market is anticipated to grow at a CAGR of 11.2% during the forecast period.

- The global silicon carbide (sic) in semiconductor market was estimated to be worth approximately USD 5.03 billion in 2023 and is projected to reach a value of USD 13.08 billion by 2032.

- The growth of the silicon carbide (sic) in semiconductor market is being driven by the increasing demand for energy-efficient electronic devices and the widespread adoption of electric vehicles.

- Based on the product type, the wafers segment is growing at a high rate and is projected to dominate the market.

- On the basis of technology, the SiC MOSFETs segment is projected to swipe the largest market share.

- In terms of voltage rating, the high voltage (above 1kV) segment is expected to dominate the market.

- Based on the application, the power devices segment is expected to dominate the market.

- On the basis of end-user, the automotive sector segment is projected to swipe the largest market share.

- By region, Asia-Pacific is expected to dominate the global market during the forecast period.

Silicon Carbide (Sic) in Semiconductor Market: Dynamics

Key Growth Drivers:

- High Demand for Power Electronics – SiC semiconductors enable higher efficiency and lower power loss, making them essential for electric vehicles (EVs), renewable energy systems, and industrial applications.

- Growing Adoption in Electric Vehicles (EVs) – Automakers are shifting towards SiC-based power electronics for improved battery efficiency and extended driving range.

- Expansion of 5G and Telecommunications – SiC chips provide enhanced performance in high-frequency and high-power applications, supporting the rollout of 5G infrastructure.

- Advancements in SiC Wafer Technology – Ongoing R&D efforts are leading to improved wafer quality, larger wafer sizes (e.g., 200mm), and cost reductions, boosting market adoption.

Restraints:

- High Manufacturing Costs – The complex fabrication process and expensive raw materials make SiC semiconductors costly compared to traditional silicon-based alternatives.

- Limited Supply Chain and Production Capacity – The SiC industry faces supply constraints due to limited foundries and material availability, affecting large-scale adoption.

Opportunities:

- Rising Demand for Renewable Energy – SiC-based inverters improve efficiency in solar and wind power systems, creating strong market growth potential.

- Expansion in Aerospace & Defense – The durability and high-temperature tolerance of SiC semiconductors make them suitable for military and space applications.

- Government Initiatives for Energy Efficiency – Policies promoting energy-efficient technologies encourage the adoption of SiC-based solutions across industries.

Challenges:

- Complex Fabrication Process – The production of high-quality SiC wafers involves advanced techniques that require significant expertise and investment.

- Competition from Alternative Materials – GaN (Gallium Nitride) is emerging as a strong competitor, particularly in high-frequency applications, posing a challenge to SiC adoption.

- Long Design and Certification Cycles – Industries such as automotive and aerospace require extensive testing and validation for SiC components, delaying mass adoption.

Silicon Carbide (Sic) in Semiconductor Market: Report Scope

This report thoroughly analyzes the Silicon Carbide (Sic) in Semiconductor Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Silicon Carbide (Sic) in Semiconductor Market |

| Market Size in 2023 | USD 5.03 Billion |

| Market Forecast in 2032 | USD 13.08 Billion |

| Growth Rate | CAGR of 11.2% |

| Number of Pages | 179 |

| Key Companies Covered | Norstel, Cree, Rohm, INFINEON, STMicroelectronics, TOSHIBA, Genesic Semiconductor, Fairchild Semiconductor, Microsemi, Renesas Electronics |

| Segments Covered | By Product Type, By Technology, By Voltage Rating, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Silicon Carbide (Sic) in Semiconductor Market: Segmentation Insights

The global silicon carbide (sic) in semiconductor market is divided by product type, technology, voltage rating, application, end-user, and region.

Segmentation Insights by Product Type

Based on product type, the global silicon carbide (sic) in semiconductor market is divided into wafer, substrate, power modules, diodes, and transistors.

In the silicon carbide (SiC) semiconductor market, wafers hold the dominant position among product types. SiC wafers serve as the foundational material for advanced semiconductor devices, enabling high-power and high-temperature performance. The increasing demand for SiC wafers is driven by the rapid adoption of electric vehicles (EVs), renewable energy systems, and industrial power applications, where their superior efficiency and thermal conductivity make them a preferred choice over traditional silicon wafers. As manufacturers ramp up production to meet the rising demand, wafers continue to lead the market in terms of revenue and volume.

Substrates follow as the second most significant segment, closely linked to wafer production. SiC substrates provide the necessary foundation for fabricating high-performance semiconductor components, supporting applications in power electronics and RF devices. The demand for larger-diameter SiC substrates is increasing as they improve yield and cost-effectiveness in device fabrication. Companies are investing in expanding SiC substrate manufacturing to cater to industries such as automotive, telecommunications, and aerospace.

Power modules rank next in the SiC semiconductor market. These integrated components combine multiple semiconductor devices, such as MOSFETs and diodes, into a single package to optimize power efficiency and thermal performance. Their use in fast-charging stations, industrial motor drives, and renewable energy systems has fueled their market growth. The rising electrification of transportation and grid infrastructure supports further adoption.

Diodes hold a significant market share, particularly in power conversion applications. SiC-based Schottky diodes are widely used in power supplies, solar inverters, and automotive charging systems due to their low switching losses and high efficiency. Their ability to handle high voltages and operate at elevated temperatures makes them a superior alternative to silicon-based diodes in demanding applications.

Finally, transistors represent a smaller but steadily growing segment. SiC-based transistors, including MOSFETs and BJTs, are gaining traction in power electronics, enabling higher energy efficiency in high-frequency applications. While the market for SiC transistors is expanding, they are still in the early stages of widespread adoption compared to other SiC semiconductor products. Ongoing technological advancements and cost reductions are expected to boost their usage in the coming years.

Segmentation Insights by Technology

On the basis of technology, the global silicon carbide (sic) in semiconductor market is bifurcated into pure SiC, SiC-based heterojunctions, SiC MOSFETs, and junction field effect transistors (JFETs).

In the silicon carbide (SiC) semiconductor market, SiC MOSFETs hold the dominant position among technologies. SiC MOSFETs have revolutionized power electronics by offering higher efficiency, faster switching speeds, and superior thermal performance compared to traditional silicon-based MOSFETs. These characteristics make them ideal for electric vehicles (EVs), renewable energy applications, and industrial power systems. As demand for high-power and high-frequency applications rises, SiC MOSFETs continue to see widespread adoption, driving their market dominance.

Following MOSFETs, SiC-based heterojunctions represent the second most significant segment. These structures, which combine SiC with other semiconductor materials, enable improved performance in optoelectronic and high-power applications. SiC heterojunction technology is being explored for next-generation high-frequency communication devices and power electronics, particularly in industries requiring robust and efficient semiconductor solutions.

Pure SiC technology holds a strong position in the market, as it is the basis for all SiC semiconductor devices. Pure SiC is widely used in substrates, wafers, and basic semiconductor components that power SiC-based devices. Its superior properties, such as high thermal conductivity and wide bandgap, provide the foundation for advanced power and RF applications. While not a standalone commercial product in most cases, pure SiC technology underpins the growth of the overall market.

Finally, Junction Field Effect Transistors (JFETs) hold a smaller but steadily growing market share. SiC JFETs offer high-speed switching and low conduction losses, making them suitable for applications in power conversion and amplification. However, their adoption is somewhat limited due to the widespread preference for MOSFETs, which offer easier gate control and compatibility with existing power electronic systems. As research continues, SiC JFETs may find increased adoption in niche high-voltage and high-frequency applications.

Segmentation Insights by Voltage Rating

On the basis of voltage rating, the global silicon carbide (sic) in semiconductor market is bifurcated into low voltage (up to 600v), medium voltage (600v to 1kv), and high voltage (above 1kv).

In the silicon carbide (SiC) semiconductor market, the high voltage (above 1kV) segment dominates due to the increasing demand for high-efficiency power electronics in electric vehicles (EVs), industrial power systems, and renewable energy applications. SiC’s ability to handle high voltages while minimizing power losses makes it ideal for high-power inverters, grid infrastructure, and high-voltage DC transmission. The shift toward electrification in transportation and energy sectors continues to drive the growth of this segment, as SiC semiconductors significantly outperform traditional silicon in high-voltage environments.

The medium voltage (600V to 1kV) segment follows closely, driven by applications in fast-charging stations, uninterruptible power supplies (UPS), and industrial motor drives. Medium-voltage SiC devices, such as MOSFETs and diodes, offer superior energy efficiency and switching speed, making them increasingly popular in power conversion and distribution systems. As demand for faster and more efficient power electronics grows, this segment continues to expand, especially in the EV charging infrastructure and smart grid applications.

The low voltage (up to 600V) segment holds a smaller share of the market but remains essential for power supplies, consumer electronics, and low-power industrial applications. While SiC provides advantages over silicon even at lower voltages, the cost-benefit trade-off has limited its adoption in this range, as traditional silicon-based semiconductors remain dominant in low-voltage applications. However, ongoing cost reductions and technological advancements may drive further growth in this segment, particularly for high-efficiency power management systems.

Segmentation Insights by Application

On the basis of application, the global silicon carbide (sic) in semiconductor market is bifurcated into power devices, RF devices, LEDs and laser diodes.

In the silicon carbide (SiC) semiconductor market, power devices dominate the application segments due to their critical role in high-power, high-efficiency electronics. SiC-based power devices, including MOSFETs, diodes, and power modules, are widely used in electric vehicles (EVs), renewable energy systems, industrial power supplies, and data centers. Their superior thermal conductivity, high voltage tolerance, and reduced switching losses make them the preferred choice over traditional silicon-based power electronics. The increasing global push for electrification and energy efficiency continues to drive strong demand for SiC power devices.

RF devices hold the second-largest market share, benefiting from SiC’s ability to operate at high frequencies with minimal signal loss. SiC-based RF components are essential for radar systems, satellite communications, and 5G infrastructure, where high power and efficiency are required. The telecommunications sector, in particular, is driving the demand for SiC RF devices as the need for high-speed data transmission and improved network performance continues to grow.

LEDs and laser diodes represent a smaller but significant segment of the SiC semiconductor market. SiC serves as a substrate material for gallium nitride (GaN)-based LEDs, enabling higher efficiency and brightness in lighting and display applications. Laser diodes using SiC substrates find applications in optical communication, medical devices, and industrial cutting tools. While this segment does not generate as much revenue as power and RF devices, advancements in optoelectronics and high-performance lighting solutions continue to support its growth.

Segmentation Insights by End-User

On the basis of end-user, the global silicon carbide (sic) in semiconductor market is bifurcated into aerospace & defense, automotive, telecommunications, consumer electronics, and industrial sector.

In the silicon carbide (SiC) semiconductor market, the automotive sector holds the dominant position among end-users. The increasing adoption of SiC-based power electronics in electric vehicles (EVs) and hybrid electric vehicles (HEVs) has significantly boosted demand. SiC MOSFETs and diodes are widely used in EV inverters, onboard chargers, and fast-charging infrastructure, offering superior efficiency, reduced heat dissipation, and extended driving range. As automakers push for higher performance and energy efficiency, SiC continues to be a crucial component in the EV industry’s growth.

The industrial sector follows as the second-largest end-user. SiC power devices are essential in renewable energy systems, industrial motor drives, power supplies, and high-voltage applications. Industries focusing on energy efficiency and sustainability are shifting towards SiC-based power modules to improve operational performance and reduce energy losses. The expansion of smart grids, data centers, and power distribution systems further accelerates SiC adoption in industrial applications.

The telecommunications sector ranks third, benefiting from SiC’s high-frequency capabilities. SiC-based RF devices play a crucial role in 5G infrastructure, satellite communications, and radar systems. As the demand for high-speed data transmission and network efficiency increases, SiC power amplifiers and RF transistors are becoming more widely adopted. The rollout of 5G networks and advancements in broadband technology continue to drive SiC growth in telecommunications.

The aerospace & defense sector holds a significant but smaller market share. SiC semiconductors are used in high-frequency radar systems, electronic warfare equipment, and satellite power management due to their ability to operate in extreme environments. Their radiation resistance and high thermal conductivity make them ideal for space and defense applications. While the sector’s overall volume is lower compared to automotive and industrial applications, SiC’s reliability and performance advantages make it indispensable in mission-critical systems.

Finally, the consumer electronics sector represents a growing but relatively smaller market segment for SiC semiconductors. While traditional silicon-based semiconductors dominate consumer devices, SiC is increasingly finding applications in high-power adapters, fast-charging circuits, and energy-efficient home appliances. As cost reductions and technology improvements continue, SiC adoption in premium consumer electronics may expand further in the coming years.

Silicon Carbide (Sic) in Semiconductor Market: Regional Insights

- Asia-Pacific is expected to dominates the global market

Asia-Pacific leads the silicon carbide (SiC) semiconductor market, driven by rapid industrialization and the expansion of the electric vehicle (EV) sector. Countries like China, Japan, and South Korea are at the forefront, with China accounting for a significant portion of the market. The region's focus on renewable energy projects and advancements in consumer electronics further bolster SiC adoption. Government initiatives promoting energy efficiency and substantial investments in semiconductor manufacturing contribute to this dominance. For instance, China's emphasis on 5G infrastructure and efficient satellite communications has increased the use of SiC-based power amplifiers and transistors.

North America is experiencing significant growth in the SiC semiconductor market, propelled by the increasing adoption of electric vehicles and renewable energy solutions. The presence of key industry players and a strong focus on technological innovation drive this expansion. Government incentives supporting EV infrastructure and renewable energy projects further enhance market growth. Additionally, the aerospace and defense sectors in the U.S. are integrating SiC technology for high-performance applications, contributing to the region's growing market share.

Europe is witnessing steady growth in the SiC semiconductor market, underpinned by stringent emission regulations and a commitment to renewable energy adoption. Countries such as Germany, France, and the U.K. are investing in SiC technology to enhance automotive and industrial applications. The European Union's support for electric vehicles and efforts to reduce carbon emissions drive demand for efficient power electronics. Companies are investing in SiC technology to meet the demand for more efficient power electronics in the automotive sector.

Latin America presents emerging opportunities in the SiC semiconductor market, fueled by the growing adoption of renewable energy and advancements in the automotive industry. Countries like Brazil and Mexico are exploring SiC applications in power electronics to support sustainable technologies. The increasing demand for electric vehicles and renewable energy projects in Brazil, for instance, is boosting the market, with SiC-enabled solar power systems and EV infrastructure playing a crucial role in the country's clean energy transition.

Middle East and Africa are gradually embracing SiC semiconductor technology, driven by investments in power projects and renewable energy initiatives. Nations such as the UAE, Saudi Arabia, and South Africa are focusing on enhancing their energy infrastructure, creating opportunities for SiC applications in power conversion systems. These developments align with the global shift towards energy efficiency and sustainable practices, positioning the region as a potential growth area for the SiC semiconductor market.

Silicon Carbide (Sic) in Semiconductor Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the silicon carbide (sic) in semiconductor market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global silicon carbide (sic) in semiconductor market include:

- Norstel

- Cree

- Rohm

- INFINEON

- STMicroelectronics

- TOSHIBA

- Genesic Semiconductor

- Fairchild Semiconductor

- Microsemi

- Renesas Electronics

The global silicon carbide (sic) in semiconductor market is segmented as follows:

By Product Type

- Wafer

- Substrate

- Power Modules

- Diodes

- Transistors

By Technology

- Pure SiC

- SiC-based Heterojunctions

- SiC MOSFETs

- Junction Field Effect Transistors (JFETs)

By Voltage Rating

- Low Voltage (up to 600V)

- Medium Voltage (600V to 1kV)

- High Voltage (above 1kV)

By Application

- Power Devices

- RF Devices

- LEDs and Laser Diodes

By End-User

- Aerospace and Defense

- Automotive

- Telecommunications

- Consumer Electronics

- Industrial Sector

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Silicon Carbide (Sic) in Semiconductor

Request Sample

Silicon Carbide (Sic) in Semiconductor