Single Codec Market Size, Share, and Trends Analysis Report

CAGR :

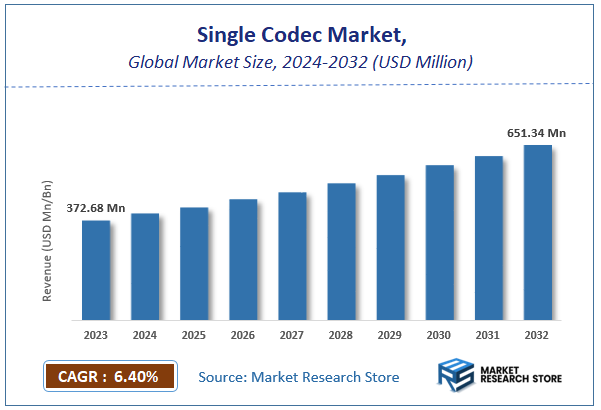

| Market Size 2023 (Base Year) | USD 372.68 Million |

| Market Size 2032 (Forecast Year) | USD 651.34 Million |

| CAGR | 6.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Single Codec Market Insights

According to Market Research Store, the global single codec market size was valued at around USD 372.68 million in 2023 and is estimated to reach USD 651.34 million by 2032, to register a CAGR of approximately 6.4% in terms of revenue during the forecast period 2024-2032.The single codec report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Single Codec Market: Overview

Single codec refers to a standalone audio or video compression and decompression algorithm or device that encodes and decodes digital media using a specific standardized format. Unlike multi-codec systems that support a range of encoding standards, a single codec is designed to handle one particular format, such as H.264 for video or AAC for audio. These codecs are implemented either in software (as part of applications or operating systems) or in hardware (as embedded chips within devices like cameras, smartphones, or streaming equipment) to reduce file sizes and bandwidth requirements while preserving quality.

The adoption of single codecs is common in applications where consistent format handling, low latency, or hardware optimization is critical. For instance, video surveillance systems, digital broadcasting platforms, or dedicated communication devices often rely on single codecs to ensure compatibility, reliability, and efficiency. The growth of the single codec market is driven by rising demand for streamlined media delivery, reduced processing complexity, and integration in cost-sensitive or low-power devices. As media consumption expands across fixed and mobile platforms, single codecs continue to play a vital role in enabling real-time communication, content streaming, and efficient digital storage.

Key Highlights

- The single codec market is anticipated to grow at a CAGR of 6.4% during the forecast period.

- The global single codec market was estimated to be worth approximately USD 372.68 million in 2023 and is projected to reach a value of USD 651.34 million by 2032.

- The growth of the single codec market is being driven by the ever-increasing global consumption of digital content and the widespread proliferation of smart devices.

- Based on the end-user, the smart TVS segment is growing at a high rate and is projected to dominate the market.

- On the basis of technology type, the AAC (advanced audio codec) segment is projected to swipe the largest market share.

- In terms of deployment mode, the enterprise solutions segment is expected to dominate the market.

- Based on the feature set, the lossy compression segment is expected to dominate the market.

- Based on the user base, the film and video producers segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Single Codec Market: Dynamics

Key Growth Drivers:

- Simplification of Development and Deployment: Using a single, standardized codec simplifies the development process for content creators, hardware manufacturers, and software developers. It reduces complexity in encoding, decoding, and playback, leading to faster time-to-market for new products and services.

- Optimized Performance and Efficiency for Specific Use Cases: A single codec can be highly optimized for a particular application (e.g., specific streaming service, communication protocol, device type). This allows for maximum compression efficiency, lower latency, and better quality output for that specific environment, leading to significant bandwidth and storage savings.

- Enhanced Interoperability within an Ecosystem: When a single codec becomes a de facto standard within a specific ecosystem (e.g., a particular gaming console, a closed communication platform, or a specific broadcasting standard like DVB), it ensures seamless interoperability and compatibility across all devices and content within that ecosystem.

- Reduced Licensing Complexities (if open-source or royalty-free): If the single chosen codec is open-source (like AV1) or royalty-free, it eliminates the burden of complex and potentially expensive licensing fees associated with patented codecs. This can significantly reduce costs for manufacturers and service providers, accelerating adoption.

- Lower Hardware and Software Requirements: A single, optimized codec often requires less computational power for encoding and decoding compared to supporting multiple codecs, which can translate to lower hardware costs, less energy consumption, and better battery life for devices.

- Consistent User Experience: By standardizing on one codec, service providers can deliver a more consistent and predictable user experience in terms of video/audio quality, latency, and playback reliability across all supported devices.

- Large-Scale Infrastructure Optimization: For major streaming platforms or broadcasters, standardizing on a single highly efficient codec allows for massive optimization of their infrastructure, including content delivery networks (CDNs) and storage, leading to significant operational cost reductions.

Restraints:

- Limited Compatibility and Interoperability Beyond the Ecosystem: The primary restraint is the inherent limitation of a single codec outside its designated ecosystem. Content encoded with one codec may not be playable on devices or platforms that do not support it, leading to fragmentation and reduced reach in a diverse market.

- Risk of Technological Obsolescence: If the chosen single codec becomes outdated or new, more efficient codecs emerge, the entire ecosystem relying on that single codec faces the challenge of a costly and complex migration to new technologies. This can lock entities into less efficient solutions.

- Dependence on a Single Technology Provider (for proprietary codecs): For proprietary single codecs, reliance on one technology provider can lead to vendor lock-in, limited innovation, and potential issues with licensing terms, support, or future development.

- Lack of Flexibility for Diverse Content and Network Conditions: A single codec might not be optimal for all types of content (e.g., live vs. on-demand, high-motion vs. static scenes) or varying network conditions (e.g., high-bandwidth 5G vs. limited mobile data). A "one-size-fits-all" approach can compromise quality or efficiency in certain scenarios.

- High Barrier to Entry for New Codecs (if an incumbent dominates): When a single codec is deeply embedded and widely adopted, it creates a high barrier to entry for new, potentially more efficient, codecs to gain market share due to the immense effort and cost required for widespread adoption and hardware integration.

- Patent and Licensing Complexities (if not open-source): Even a single dominant codec can be subject to complex patent licensing frameworks and royalty stacking, which can lead to legal disputes and increased costs for implementers, especially if it's a proprietary standard.

- Resistance to Change from Established Infrastructure: Industries with significant legacy infrastructure built around an older, established single codec (e.g., some broadcasting standards) face immense resistance to changing to a new codec due to the prohibitive costs and disruptions of updating hardware and software.

Opportunities:

- Emergence of Highly Efficient Open-Source Codecs (e.g., AV1, VVC): The rise of powerful, royalty-free, open-source codecs like AV1 (AOMedia Video 1) and the anticipated VVC (Versatile Video Coding) presents a significant opportunity. If one of these gains widespread adoption, it could effectively become a dominant single codec across many platforms, driving efficiency and innovation without licensing burdens.

- AI-Powered Codec Optimization: Leveraging AI and machine learning to dynamically optimize a single codec's parameters in real-time based on content characteristics, network conditions, and user device capabilities can further enhance its efficiency and quality, pushing the boundaries of what a single codec can achieve.

- Specialized Codecs for Niche High-Growth Areas: Opportunities exist for developing highly specialized single codecs optimized for emerging high-growth areas such as immersive VR/AR content, real-time gaming streams, or specific industrial IoT applications, where a tailored solution can offer superior performance.

- Integration with 5G and Edge Computing: The rollout of 5G networks and the increasing adoption of edge computing provide opportunities for single codecs that can be optimized for low-latency, high-bandwidth applications, facilitating seamless streaming and communication directly at the network edge.

- Simplification for Content Creation Tools: As content creation becomes more democratized, providing simple, high-quality, and standardized single-codec encoding options within user-friendly tools (e.g., for social media, live streaming from mobile devices) can significantly boost content generation.

- Automotive and In-Vehicle Infotainment Systems: The automotive industry's increasing shift towards connected vehicles and advanced infotainment systems offers an opportunity for a standardized single codec to manage diverse audio and video streams within the vehicle ecosystem, ensuring compatibility and high quality.

- Strategic Consolidation and Partnerships: Companies can pursue strategic partnerships or acquisitions to consolidate codec technologies, potentially leading to a more unified ecosystem around a single, superior codec, thereby reducing market fragmentation.

Challenges:

- Achieving Widespread Hardware and Software Support: Even a technically superior single codec faces the immense challenge of gaining widespread adoption across a fragmented landscape of devices, operating systems, browsers, and applications. This requires significant industry collaboration and investment in hardware acceleration.

- Overcoming the "Chicken and Egg" Problem of Adoption: For a new single codec to succeed, content creators need to encode in it, and device manufacturers need to support it. This creates a "chicken and egg" problem where neither fully commits without the other, slowing down adoption.

- Complex Intellectual Property and Patent Pools: Even if a new codec is designed to be royalty-free, the landscape of multimedia patents is complex. Challenges can arise from "patent trolls" or existing patents that may inadvertently cover aspects of the new codec, leading to legal disputes and potential licensing costs.

- Balancing Compression Efficiency with Encoding/Decoding Complexity: Developing a single codec that offers significantly better compression ratios while maintaining reasonable encoding/decoding complexity (i.e., not requiring excessive processing power) is a continuous technical challenge. More efficient codecs often require more computational resources.

- Maintaining Backward Compatibility (if an incumbent): For an established single codec, the challenge is to introduce improvements or new features without breaking backward compatibility with older devices and content, which is crucial for maintaining its market position and preventing user frustration.

- Global Standardization and Fragmentation of Regional Markets: While some codecs achieve global dominance (e.g., H.264), regional preferences, regulatory requirements, or local industry alliances can lead to market fragmentation, making it difficult for a truly "single" codec to achieve universal adoption.

- Evolving User Expectations for Quality and Latency: As internet speeds increase and user expectations for higher resolution (4K, 8K), immersive experiences, and real-time interaction grow, a single codec must continuously evolve to meet these demands without compromising on efficiency or introducing unacceptable latency.

Single Codec Market: Report Scope

This report thoroughly analyzes the Single Codec Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Single Codec Market |

| Market Size in 2023 | USD 372.68 Million |

| Market Forecast in 2032 | USD 651.34 Million |

| Growth Rate | CAGR of 6.4% |

| Number of Pages | 178 |

| Key Companies Covered | Analog Devices, Beamr, Cisco, DivX, Intel, Netposa, RealNetworks, Renesas Electronics, Sumavision, Tieline Technology |

| Segments Covered | By End-User, By Technology Type, By Deployment Mode, By Feature Set, By User Base, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Single Codec Market: Segmentation Insights

The global single codec market is divided by end-user, technology type, deployment mode, feature set, user base, and region.

Segmentation Insights by End-User

Based on end-user, the global single codec market is divided into smart TVS, set-top boxes, and mobile devices.

Smart TVs dominate the Single Codec Market due to their high demand for efficient audio and video compression in delivering seamless multimedia experiences. Single codec chips are vital in enabling Smart TVs to decode and play high-definition and ultra-high-definition content in real time while maintaining low power consumption and system cost. These codecs support various formats like H.264, H.265, and AV1, ensuring compatibility with major streaming services and broadcasting standards. With consumer expectations for 4K and 8K content, as well as features like HDR, surround sound, and interactive apps, Smart TVs rely heavily on robust codec performance. This makes them the primary end-use application, driving the largest share in the market.

Set-top Boxes form a significant segment, as they use single codec units to decode live television broadcasts, satellite feeds, and on-demand content. These devices require real-time processing and error-free decoding to maintain video quality, especially in subscription-based platforms and cable services. Single codecs in set-top boxes help in compressing large video data, reducing bandwidth usage, and optimizing signal integrity across different resolutions and bitrates. With increasing shifts toward IPTV and hybrid set-top box systems, the need for flexible, multi-format codec support is crucial, making this segment a stable contributor to the market.

Mobile Devices represent a growing segment in the Single Codec Market, driven by the demand for efficient multimedia playback, video calling, and content creation on smartphones and tablets. These devices require compact and power-efficient codecs capable of handling both video compression and decompression with minimal latency. Mobile devices benefit from single codecs that support newer formats like HEVC and VP9, enhancing video streaming quality over limited mobile bandwidth. As smartphones continue to integrate high-resolution cameras and AI-driven video features, the need for advanced codec solutions becomes increasingly critical, boosting the growth of this segment.

Segmentation Insights by Technology Type

On the basis of technology type, the global single codec market is bifurcated into AAC (advanced audio codec), MP3, and opus.

AAC (Advanced Audio Codec) is the dominant technology type in the Single Codec Market due to its superior audio compression efficiency, broad device compatibility, and adoption across a wide range of applications. AAC offers better sound quality than MP3 at similar bitrates, making it the default codec for major platforms like YouTube, iTunes, and various mobile operating systems. Its support for multichannel audio, low-latency streaming, and scalability across different bitrates makes it ideal for Smart TVs, mobile devices, and Bluetooth audio systems. As streaming services and multimedia platforms prioritize both audio quality and bandwidth efficiency, AAC continues to lead in codec deployments across consumer electronics.

MP3 remains a widely used codec technology, especially in legacy systems and low-resource applications. Despite being one of the earliest standardized digital audio compression formats, MP3 retains a strong foothold due to its simplicity, broad hardware support, and acceptable quality at modest bitrates. It is commonly integrated in portable music players, car infotainment systems, and low-cost mobile devices. Although it lacks the efficiency and advanced features of newer codecs, its entrenched user base and backward compatibility ensure continued relevance in the Single Codec Market, particularly for budget-conscious or compatibility-driven deployments.

Opus is an emerging technology in the Single Codec Market, designed for interactive real-time audio applications such as VoIP, video conferencing, and online gaming. As an open, royalty-free codec developed by the IETF, Opus supports both narrowband speech and fullband stereo music, dynamically adapting to changing network conditions. Its low latency and high resilience to packet loss make it ideal for communication platforms and live media streaming. Though still growing in adoption compared to AAC and MP3, Opus is gaining traction in browsers, mobile communication apps, and WebRTC-based services, representing a forward-looking segment with strong potential in real-time audio delivery markets.

Segmentation Insights by Deployment Mode

On the basis of deployment mode, the global single codec market is bifurcated into enterprise solutions, media servers, and private cloud solutions.

Enterprise Solutions dominate the Single Codec Market as businesses across media, telecommunications, and technology sectors rely on robust and scalable codec implementations to manage large volumes of audio and video data. These solutions are typically integrated within complex digital infrastructure, powering everything from corporate video conferencing systems and digital content delivery platforms to unified communication suites. Enterprise-grade single codecs prioritize high reliability, security, real-time performance, and compliance with industry standards. They are optimized for multi-format support, low latency, and high throughput, making them essential for broadcasting, streaming, education platforms, and digital media production environments.

Media Servers represent a vital segment in the Single Codec Market as they act as the backbone for video-on-demand services, live streaming, and content delivery networks (CDNs). Single codec components integrated within media servers enable efficient encoding and decoding of digital content in real time, ensuring quality delivery across multiple devices and bandwidth profiles. These codecs support adaptive bitrate streaming and facilitate content transcoding for seamless playback on different platforms. Media servers are crucial in ensuring optimized storage and delivery, especially as demand for high-resolution content and low-latency streaming increases.

Private Cloud Solutions are an emerging deployment mode for single codec systems, particularly among enterprises and media firms that require enhanced control, data security, and scalability. Private cloud environments allow organizations to deploy codec engines with custom configurations for encoding, decoding, and transcoding tasks without relying on public cloud infrastructure. These solutions are favored in industries where content sensitivity and compliance with strict data governance policies are paramount. Private cloud-based codec deployments are also increasingly used for edge computing applications, remote production workflows, and internal media archives where performance and privacy are key.

Segmentation Insights by Feature Set

On the basis of feature set, the global single codec market is bifurcated into lossy compression, lossless compression, and real-time compression.

Lossy Compression dominates the Single Codec Market due to its efficiency in reducing file sizes while maintaining acceptable quality, making it ideal for streaming, broadcasting, and mobile content delivery. This feature set is foundational in codecs such as AAC, MP3, and H.264, which are widely used across Smart TVs, mobile devices, and web-based platforms. Lossy compression allows for the transmission and storage of high volumes of audio and video content over limited bandwidth and storage environments. Its ability to prioritize perceptual quality by removing less critical data makes it the standard choice in consumer and commercial multimedia applications where performance and bandwidth optimization are critical.

Lossless Compression forms a specialized but growing segment, especially in professional media production, archival systems, and audiophile-grade audio solutions. This feature set preserves all original data without degradation, making it ideal for use cases where content fidelity and precision are paramount. Lossless codecs like FLAC and ALAC are commonly employed in high-resolution music players, digital mastering studios, and scientific or medical imaging systems. While the file sizes are larger than those of lossy formats, the assurance of unaltered content quality drives adoption in sectors where accuracy cannot be compromised.

Real-Time Compression is a critical feature in applications requiring immediate encoding or decoding of media content with minimal delay, such as video conferencing, live broadcasting, gaming, and remote control interfaces. Single codecs with real-time compression capabilities are engineered to balance speed and quality, often using adaptive bitrates and latency-optimized protocols. Technologies like Opus for audio and H.265/VP9 for video ensure real-time delivery while adapting to fluctuating network conditions. This segment is increasingly important in enterprise collaboration tools, virtual classrooms, and low-latency streaming platforms that depend on uninterrupted, high-quality media delivery.

Segmentation Insights by User Base

On the basis of user base, the global single codec market is bifurcated into film and video producers, audio engineers, and broadcasting professionals.

Film and Video Producers dominate the Single Codec Market as they require high-performance codecs capable of compressing and decompressing large volumes of high-definition and ultra-high-definition video content without compromising visual fidelity. These users often work with 4K, 6K, or even 8K footage that needs to be efficiently stored, edited, and transmitted across production pipelines. Single codecs used in this domain must support high bitrates, wide format compatibility, and post-production workflows. Whether during shooting, editing, or color grading, these professionals rely on lossless and lossy codec technologies to balance between quality preservation and workflow speed, making them the largest and most technologically demanding segment in the market.

Audio Engineers represent a crucial user base in the Single Codec Market, utilizing audio-specific codecs to ensure clean, accurate sound capture, manipulation, and distribution. They work across various industries, including music production, sound design, game audio, and post-production. Codecs like AAC, FLAC, and Opus are frequently used for their ability to deliver high audio clarity at various compression levels. Audio engineers require real-time monitoring capabilities, bit-depth control, and format interoperability, especially when working in studio environments or with streaming services. Their codec needs emphasize tonal precision, minimal latency, and fidelity, making them essential contributors to market demand.

Broadcasting Professionals constitute a key user group, heavily dependent on single codec solutions that enable the real-time transmission of video and audio content over various networks and platforms. From live news feeds to sports events and satellite transmissions, broadcasters rely on codec technologies for encoding content in formats suitable for over-the-air, cable, and digital streaming. These professionals prioritize reliability, speed, and compatibility with standard transmission protocols. The ability to maintain quality across resolutions, bitrates, and devices under live conditions drives the need for robust and scalable codec integrations within broadcasting infrastructure.

Single Codec Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the global single codec market due to its advanced electronics and semiconductor industries, along with strong demand from sectors like telecommunications, automotive, consumer electronics, and defense. The United States leads this region with extensive R&D capabilities, particularly in audio and video signal processing, where single codecs are used to compress and decompress digital data efficiently. These devices are widely implemented in smartphones, headsets, voice assistants, set-top boxes, automotive infotainment systems, and industrial equipment. Major companies such as Texas Instruments, Analog Devices, Cirrus Logic, and Qualcomm operate significant manufacturing and design operations in the region, providing cutting-edge single codec solutions with low power consumption, high fidelity, and multi-format compatibility. Additionally, the presence of tech giants and OEMs that emphasize integration, space optimization, and energy efficiency supports strong adoption of single codec ICs. North America also benefits from a robust regulatory framework and high-speed network infrastructure that push the adoption of efficient digital encoding systems in both commercial and consumer domains.

Asia-Pacific is a major contributor to the single codec market, driven by high-volume manufacturing and rapidly growing electronics demand. Countries like China, South Korea, Japan, and Taiwan dominate in consumer electronics production, with single codecs embedded in mobile phones, wearables, laptops, and multimedia devices. South Korea and Japan, home to leading consumer electronics brands such as Samsung, Sony, and LG, emphasize the use of advanced audio and video compression hardware, driving innovation in single codec design. China, as a hub for electronics assembly and smartphone production, is a large consumer of codec ICs, though it still imports much of its high-end silicon. Taiwan contributes through its strong IC fabrication and packaging capabilities. While Asia-Pacific leads in production volume, many firms rely on North American companies for design IP, and the region trails in system-level innovation and end-to-end control over codec performance optimization.

Europe maintains a steady position in the single codec market, largely due to its strength in the automotive and industrial sectors. Countries such as Germany, France, and the UK utilize single codecs in in-vehicle infotainment systems, driver-assistance modules, and industrial automation equipment. European manufacturers focus heavily on compliance, energy efficiency, and system robustness, often integrating codecs in high-reliability and safety-critical applications. Moreover, companies in this region prioritize high-quality acoustic and video performance, especially for premium automotive brands and professional-grade electronics. While Europe contributes significantly to application-specific demand, particularly in embedded systems, the design and production of high-performance single codecs are still largely centered in North America and Asia-Pacific.

Latin America has a limited but growing presence in the single codec market, with primary demand stemming from the consumer electronics and automotive industries in Brazil, Mexico, and Argentina. Most of the region relies on imported codec ICs integrated into devices assembled locally. Brazil’s electronics sector uses codecs in televisions, media players, and communication devices, while Mexico’s role in automotive electronics assembly contributes to demand in vehicle audio and communication systems. However, lack of local design expertise and fabrication facilities limits the region’s role to end-use integration, with minimal contribution to global codec innovation or production. North America retains clear dominance through its vertically integrated supply chains and advanced product development ecosystem.

Middle East & Africa region is in an early stage of market development for single codecs, with limited adoption primarily in telecommunications infrastructure, consumer electronics distribution, and security systems. Gulf countries such as the UAE and Saudi Arabia are increasingly deploying digital communication and smart surveillance systems where codecs play a crucial role in signal compression. South Africa shows some adoption in public safety communications and broadcasting equipment. However, the absence of a strong semiconductor industry means most codecs are imported as part of finished products or sub-assemblies. Compared to North America, the region remains highly dependent on external suppliers with minimal domestic R&D or customization capabilities.

Single Codec Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the single codec market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global single codec market include:

- Analog Devices

- Beamr

- Cisco

- DivX

- Intel

- Netposa

- RealNetworks

- Renesas Electronics

- Sumavision

- Tieline Technology

The global single codec market is segmented as follows:

By End-User

- Smart TVs

- Set-top Boxes

- Mobile Devices

By Technology Type

- AAC (Advanced Audio Codec)

- MP3

- Opus

By Deployment Mode

- Enterprise Solutions

- Media Servers

- Private Cloud Solutions

By Feature Set

- Lossy Compression

- Lossless Compression

- Real-Time Compression

By User Base

- Film and Video Producers

- Audio Engineers

- Broadcasting Professionals

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Single Codec

Request Sample

Single Codec