Software Publishers Market Size, Share, and Trends Analysis Report

CAGR :

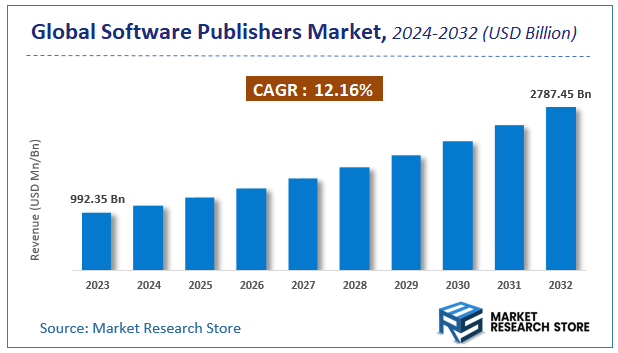

| Market Size 2023 (Base Year) | USD 992.35 Billion |

| Market Size 2032 (Forecast Year) | USD 2787.45 Billion |

| CAGR | 12.16% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Software Publishers Market Insights

According to Market Research Store, the global software publishers market size was valued at around USD 992.35 billion in 2023 and is estimated to reach USD 2787.45 billion by 2032, to register a CAGR of approximately 12.16% in terms of revenue during the forecast period 2024-2032.

The software publishers report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Software Publishers Market: Overview

Software publishers are companies or organizations responsible for developing, distributing, and marketing software products and applications to end users or businesses. They oversee the entire software lifecycle, from initial development and testing to deployment, updates, and customer support. Software publishers operate across various sectors, including operating systems, productivity tools, gaming, security, enterprise solutions, and mobile applications. They may also manage licensing, intellectual property rights, and partnerships with hardware manufacturers or service providers to ensure broad accessibility and integration of their software offerings.

The growth of the software publishers market is driven by the increasing reliance on digital technologies, cloud computing, and mobile devices across both personal and professional domains. As businesses seek to enhance operational efficiency, cybersecurity, and customer engagement, demand for innovative and scalable software solutions continues to rise. Additionally, the expansion of subscription-based and SaaS (Software as a Service) models has transformed the software publishing landscape by providing recurring revenue streams and ongoing customer relationships. Advances in artificial intelligence, machine learning, and automation are enabling software publishers to create smarter, more adaptive applications, further fueling market growth and competition within the industry.

Key Highlights

- The software publishers market is anticipated to grow at a CAGR of 12.16% during the forecast period.

- The global software publishers market was estimated to be worth approximately USD 992.35 billion in 2023 and is projected to reach a value of USD 2787.45 billion by 2032.

- The growth of the software publishers market is being driven by the increasing adoption of cloud computing and the Software-as-a-Service (SaaS) model is a major catalyst.

- Based on the software type, the application software segment is growing at a high rate and is projected to dominate the market.

- On the basis of deployment method, the on-premises software segment is projected to swipe the largest market share.

- In terms of target user, the individual users segment is expected to dominate the market.

- Based on the industry vertical, the healthcare segment is expected to dominate the market.

- Based on the pricing model, the subscription-based segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Software Publishers Market: Dynamics

Key Growth Drivers:

- Accelerated Digital Transformation Across All Industries: Businesses across every sector are actively investing in digital technologies to improve efficiency, customer experience, and competitive advantage. This pervasive digital transformation fuels demand for a wide range of software solutions, from enterprise resource planning (ERP) and customer relationship management (CRM) to specialized industry-specific applications.

- Dominance of Software-as-a-Service (SaaS) Model: The shift from on-premise software to SaaS has fundamentally changed the market. SaaS offers lower upfront costs, easier scalability, automatic updates, and accessibility from anywhere, making it highly attractive to businesses of all sizes, especially SMEs. This subscription-based model provides software publishers with more predictable and recurring revenue streams.

- Explosive Growth of Cloud Computing: The widespread adoption of cloud infrastructure (IaaS, PaaS) provides a flexible and scalable foundation for deploying and delivering software. Cloud computing reduces the need for customers to manage their own hardware, accelerating software adoption and enabling new business models.

- Rise of Artificial Intelligence (AI) and Machine Learning (ML): AI and ML are transforming software across all categories. Software publishers are integrating AI/ML capabilities (e.g., generative AI, predictive analytics, intelligent automation) into their products to enhance functionality, provide deeper insights, automate tasks, and create more personalized user experiences, driving new demand and upgrading cycles.

- Increasing Cybersecurity Threats: The escalating sophistication of cyberattacks and the growing reliance on digital infrastructure necessitate robust cybersecurity software. Businesses and individuals are investing heavily in solutions for endpoint protection, network security, data privacy, and compliance, creating a continuous demand for security software publishers.

- Proliferation of Connected Devices and IoT: The exponential growth of IoT devices (smart homes, connected cars, industrial sensors) generates massive amounts of data and requires sophisticated software for data collection, analysis, management, and security, driving demand for specialized software platforms and applications.

- Demand for Data Analytics and Business Intelligence (BI): Organizations are increasingly relying on data-driven decision-making. This fuels the demand for software that can collect, process, analyze, and visualize large datasets, providing actionable insights for business strategy, operations, and performance optimization.

Restraints:

- Cybersecurity Risks and Data Privacy Concerns: While a driver for cybersecurity software, the inherent risks of data breaches, privacy violations, and intellectual property theft pose a significant restraint. Publishers must invest heavily in security and compliance (e.g., GDPR, CCPA), and any major security incident can severely damage reputation and customer trust.

- Intense Competition and Market Saturation in Established Segments: Many software segments (e.g., CRM, ERP, productivity suites) are mature and highly competitive, with numerous established players. This leads to price pressure, commoditization, and difficulty for new entrants to gain market share without significant differentiation or niche focus.

- Talent Shortage and High Development Costs: The demand for skilled software developers, AI/ML engineers, and cybersecurity experts far outpaces supply, leading to high labor costs. Furthermore, the continuous need for R&D to keep pace with technological advancements and maintain competitiveness incurs substantial development expenses.

- Integration Complexities with Legacy Systems: Many enterprises operate with legacy IT infrastructure. Integrating new software solutions with existing, often outdated, systems can be complex, time-consuming, and costly, acting as a barrier to new software adoption.

- Rapid Technological Obsolescence and Continuous Innovation Pressure: The software market is characterized by incredibly fast technological change. Publishers face constant pressure to innovate, update their products, and adapt to new platforms and trends (e.g., AI, quantum computing) to avoid becoming obsolete, requiring significant ongoing investment.

- Regulatory Scrutiny and Compliance Burden: Software publishers must navigate a complex and evolving landscape of regulations, including data protection laws, intellectual property rights, accessibility standards, and industry-specific compliance requirements, which can vary significantly by region.

- Customer Resistance to Change and Adoption Challenges: Even with superior software, organizations and individuals can be resistant to changing their established workflows and tools. High training requirements, user interface complexities, or perceived disruption can hinder adoption rates.

Opportunities:

- Generative AI Integration into Software Products: The rapid advancements in generative AI offer immense opportunities for publishers to embed AI capabilities into their existing software (e.g., automated content creation, code generation, personalized recommendations, intelligent customer service) and create entirely new AI-native applications.

- Vertical SaaS and Industry-Specific Solutions: There's a growing demand for highly specialized software tailored to the unique needs of specific industries (e.g., healthcare, logistics, construction, legal tech, FinTech). Vertical SaaS offers deep functionality and compliance features that generic horizontal solutions cannot match, providing a significant growth avenue.

- Low-Code/No-Code (LCNC) Development Platforms: LCNC platforms empower citizen developers and business users to create applications with minimal or no coding, democratizing software development. Publishers can capitalize on this by offering LCNC tools or by building applications on these platforms.

- Expansion into Emerging Markets: Rapid digitalization, increasing internet penetration, and growing economies in regions like Asia-Pacific, Latin America, and Africa present significant untapped opportunities for software publishers to expand their customer base, especially with cloud-based and mobile-first solutions.

- Subscription-Based and Usage-Based Pricing Models: Beyond traditional SaaS subscriptions, opportunities exist in developing more flexible pricing models, such as consumption-based or pay-as-you-go pricing, especially for AI-driven services where resource usage can vary significantly.

- Emphasis on Sustainable SaaS and ESG Integration: As businesses prioritize environmental, social, and governance (ESG) goals, there's an opportunity for software publishers to develop "green" software solutions that optimize energy use, reduce carbon footprints, and enable sustainable business practices for their clients.

- Augmented Reality (AR) and Virtual Reality (VR) Applications: The increasing sophistication of AR/VR hardware and platforms creates opportunities for publishers to develop immersive software for training, design, entertainment, virtual collaboration, and remote assistance.

Challenges:

- Ethical Implications and Governance of AI: The rapid integration of AI brings significant ethical challenges, including algorithmic bias, job displacement, privacy concerns, and the potential for misuse. Software publishers must develop robust ethical guidelines, explainable AI, and transparent governance frameworks to build trust and navigate future regulations.

- Data Security and Privacy in a Highly Connected World: Despite advancements, the constant evolution of cyber threats and the increasing volume of sensitive data processed by software make data security and privacy an ongoing, formidable challenge. Publishers must continuously invest in advanced security measures and stay ahead of emerging threats.

- Talent Acquisition and Retention in a Competitive Market: The fierce competition for top-tier software engineering, AI, and cybersecurity talent remains a critical challenge. Companies must offer competitive compensation, foster innovative work environments, and invest in continuous upskilling to attract and retain the best minds.

- Navigating Fragmented Regulatory Landscapes Globally: As software becomes more globalized, publishers face the challenge of complying with a patchwork of diverse and often conflicting data privacy laws, cybersecurity regulations, and intellectual property rules across different countries and regions.

- Maintaining Innovation Amidst Economic Uncertainty: Economic downturns or recessions can lead to reduced IT spending by businesses. Software publishers face the challenge of continuing to invest heavily in innovation and R&D even when economic conditions are uncertain, to ensure long-term competitiveness.

- Open Source Software Adoption: The proliferation of high-quality open-source software can pose a challenge to commercial software publishers, especially for foundational tools and infrastructure components, as businesses may opt for free or lower-cost open-source alternatives.

- Customer Lock-in vs. Interoperability: While customer "stickiness" (high switching costs) can be a benefit, the growing demand for seamless integration and interoperability between different software systems presents a challenge for publishers. They must balance their proprietary offerings with open APIs and partnerships to meet customer ecosystem needs.

Software Publishers Market: Report Scope

This report thoroughly analyzes the Software Publishers Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Software Publishers Market |

| Market Size in 2023 | USD 992.35 Billion |

| Market Forecast in 2032 | USD 2787.45 Billion |

| Growth Rate | CAGR of 12.16% |

| Number of Pages | 173 |

| Key Companies Covered | Microsoft, HP, Oracle, Dell Technologies, IBM |

| Segments Covered | By Software Type, By Deployment Method, By Target User, By Industry Vertical, By Pricing Model, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Software Publishers Market: Segmentation Insights

The global software publishers market is divided by software type, deployment method, target user, industry vertical, pricing model, and region.

Segmentation Insights by Software Type

Based on software type, the global software publishers market is divided into application software, system software, development software, security software, and database management software.

Application Software forms the dominant segment in the Software Publishers Market. This type of software includes programs designed for end-users to perform specific tasks such as productivity tools, multimedia applications, enterprise resource planning (ERP) software, and customer relationship management (CRM) systems. The growing demand for user-friendly, customizable, and industry-specific applications across sectors like healthcare, finance, education, and retail fuels this segment. As businesses and individuals increasingly rely on digital tools to enhance efficiency and customer experience, application software publishers continue to see robust growth.

System Software includes operating systems, utility software, and middleware that manage hardware and create an environment for application software to run effectively. This segment is critical for the overall performance and stability of computing devices. Publishers of system software focus on delivering secure, scalable, and compatible platforms for various hardware configurations. The rise in adoption of new operating systems, cloud platforms, and mobile devices sustains demand in this segment, making it a key pillar of the software publishing market.

Development Software comprises tools and environments used by developers to create, test, and maintain software programs. This includes integrated development environments (IDEs), code editors, debuggers, and version control systems. Growth in software development driven by digital transformation initiatives, startups, and technology innovation fuels this segment. Publishers offering advanced, collaborative, and cloud-based development tools attract a broad user base ranging from individual developers to large enterprises.

Security Software plays a crucial role in protecting systems, networks, and data from cyber threats. This segment includes antivirus software, firewalls, encryption tools, and endpoint protection solutions. With increasing cyberattacks and regulatory compliance demands, organizations prioritize security software to safeguard assets and maintain trust. This leads to a steady rise in security software publishing, making it a high-growth segment in the market.

Database Management Software encompasses solutions that enable data storage, retrieval, and management for enterprises. These include relational database management systems (RDBMS), NoSQL databases, and data warehousing tools. As organizations generate and rely on large volumes of data for analytics and decision-making, database software publishers experience growing demand. The push towards big data, cloud databases, and real-time data processing further expands this segment’s significance.

Segmentation Insights by Deployment Method

On the basis of deployment method, the global software publishers market is bifurcated into on-premises software, cloud-based software, and hybrid deployment.

On-Premises Software dominates the Software Publishers Market due to its strong appeal among organizations that require complete control over their data and IT infrastructure. Many enterprises, especially those in highly regulated industries such as finance, healthcare, and government sectors, prefer on-premises deployment to ensure compliance with strict security and privacy standards. This deployment model allows companies to customize their software extensively and maintain critical applications within their own secure environments, reducing reliance on external networks. Despite the growing popularity of cloud-based solutions, on-premises software remains the preferred choice for businesses prioritizing data sovereignty, system reliability, and tailored IT management, thereby holding a significant share of the market.

Cloud-Based Software is the fastest-growing segment due to the increasing demand for flexibility, scalability, and cost efficiency. Cloud deployment allows users to access software via the internet on a subscription or pay-as-you-go basis without the need for local installations. This model supports remote work, rapid updates, and easy integration with other cloud services, making it popular among startups, SMEs, and even large enterprises undergoing digital transformation. The rise of Software-as-a-Service (SaaS) platforms and cloud-native applications fuels strong growth in this segment.

Hybrid Deployment combines elements of both on-premises and cloud-based software, offering a balanced approach that meets diverse organizational needs. Hybrid deployment enables companies to keep sensitive data and critical workloads on-premises while leveraging the cloud for scalability, collaboration, and backup. This flexible model is increasingly adopted by businesses seeking to optimize costs, enhance security, and maintain operational continuity. The hybrid approach addresses concerns around data sovereignty, compliance, and gradual cloud migration, positioning it as a strategic choice in the evolving software deployment landscape.

Segmentation Insights by Target User

On the basis of target user, the global software publishers market is bifurcated into individual users, small and medium enterprises (SMEs), large enterprises, government entities, and educational institutions.

Individual Users dominate the Software Publishers Market due to the widespread adoption of personal computing devices such as smartphones, tablets, and laptops across the globe. This segment is fueled by increasing digitalization in everyday life, where software applications for productivity, entertainment, communication, and personal finance have become essential. The rise of remote work, online education, gaming, and social media further amplifies the demand from individual users for diverse and user-friendly software solutions. Affordability, frequent updates, and seamless user experiences are critical factors driving software purchases in this group. Additionally, the growing penetration of internet access and mobile technology in emerging economies expands the user base significantly, making Individual Users the largest and most rapidly growing segment in the market.

Small and Medium Enterprises (SMEs) are rapidly expanding their footprint in the software market as digital transformation becomes imperative for business agility and competitiveness. SMEs seek scalable and flexible software solutions that can accommodate their growth without requiring substantial upfront investment. They often opt for subscription-based models and hybrid deployment options, which provide the benefits of cloud computing while maintaining control over critical operations. Key software categories include customer relationship management (CRM), enterprise resource planning (ERP), and cybersecurity solutions, which help SMEs optimize operations and secure their data assets.

Large Enterprises dominate the Software Publishers Market in terms of revenue and complexity of software needs. These organizations manage vast amounts of data, complex workflows, and stringent compliance requirements, necessitating highly customized and integrated software solutions. On-premises software is frequently preferred for mission-critical applications to ensure enhanced security, control, and compliance adherence. Large enterprises also invest heavily in development and security software to protect their infrastructure from cyber threats and enable continuous innovation. The scale and complexity of these organizations ensure they remain the largest spending segment in the market.

Government Entities represent a critical segment with specialized software requirements focused on transparency, data security, and public service efficiency. Governments prioritize software that supports large-scale administration, citizen services, and regulatory compliance. On-premises deployment is often mandated for sensitive applications to maintain national security and data sovereignty. Furthermore, governments are increasingly adopting cloud and hybrid solutions to improve scalability and cost efficiency, while ensuring robust cybersecurity measures.

Educational Institutions are an important and growing segment, leveraging software to facilitate digital learning, administration, and research. The rise of e-learning platforms, virtual classrooms, and collaborative tools has driven demand for software that supports both students and faculty. Educational software often emphasizes ease of use, accessibility, and cost-effectiveness. Cloud-based and hybrid deployment models are popular here, as they allow institutions to scale resources dynamically and provide remote access to educational content, especially in response to the increasing adoption of remote learning methodologies.

Segmentation Insights by Industry Vertical

On the basis of industry vertical, the global software publishers market is bifurcated into healthcare, finance and banking, retail, manufacturing, and information technology.

Healthcare is a dominant vertical in the software publishers market due to the sector’s growing reliance on digital technologies for patient management, diagnostics, and treatment. The adoption of electronic health records (EHR), telemedicine platforms, and healthcare analytics software has surged in recent years, driven by the need to improve patient outcomes and operational efficiency. Software solutions in this vertical also include medical imaging software, hospital management systems, and regulatory compliance tools. The increasing focus on personalized medicine and data-driven care further accelerates demand. Additionally, the global pandemic has expedited digital transformation in healthcare, boosting investment in software that supports remote patient monitoring, virtual consultations, and automated workflows.

Finance and Banking sector remains one of the largest consumers of software solutions, owing to the stringent regulatory environment and the critical need for data security, fraud detection, and risk management. Software publishers provide a range of products including core banking software, payment processing systems, customer relationship management (CRM) tools, and advanced analytics platforms for financial forecasting. With the rise of fintech innovations such as blockchain, digital wallets, and AI-powered advisory services, software demand in this vertical is rapidly evolving. The push towards automation, real-time transaction monitoring, and compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations also supports continuous growth.

Retail is another key vertical driving demand in the software publishers market, fueled by the shift toward e-commerce, omnichannel sales strategies, and enhanced customer engagement technologies. Retailers require software for inventory management, point of sale (POS) systems, supply chain optimization, and customer analytics. The integration of AI and machine learning in retail software helps in personalized marketing, demand forecasting, and fraud prevention. The rise of mobile shopping and digital payment systems has led to increased adoption of cloud-based retail software platforms. Additionally, the retail sector’s need for seamless customer experiences across physical and digital storefronts propels investment in software solutions that support agility and scalability.

Manufacturing vertical is increasingly dependent on software to drive automation, improve production efficiency, and ensure quality control. Manufacturing execution systems (MES), enterprise resource planning (ERP) software, and computer-aided design (CAD) tools are widely used to optimize operations. With Industry 4.0 initiatives gaining momentum, manufacturers are adopting IoT-enabled software, predictive maintenance tools, and robotics programming platforms. Software that facilitates supply chain management, product lifecycle management (PLM), and compliance with environmental and safety standards is also critical. The need to reduce downtime and improve responsiveness to market demands makes software an essential investment in manufacturing.

Information Technology sector is both a major consumer and creator of software, continually pushing innovation across various software categories. This vertical requires robust development environments, system management tools, cybersecurity solutions, and cloud computing platforms. IT companies invest heavily in software for application lifecycle management, DevOps automation, and artificial intelligence to enhance productivity and security. The rapid growth of cloud services, virtualization, and containerization technologies further drives software demand. Additionally, the IT industry’s need for scalable, flexible, and interoperable software solutions fosters a competitive environment for software publishers, fueling continuous advancement and market expansion.

Segmentation Insights by Pricing Model

On the basis of pricing model, the global software publishers market is bifurcated into subscription-based, one-time purchase, freemium, pay-per-use, and volume licensing.

Subscription-Based pricing dominates the Software Publishers Market due to its flexibility, scalability, and predictable revenue model. This approach allows users to access software through recurring payments, typically monthly or annually, which often include continuous updates, maintenance, and customer support. The subscription model lowers the upfront cost barrier, making it highly attractive for small and medium enterprises as well as individual users who seek access to the latest software features without large capital expenditure. Furthermore, the rise of cloud computing and SaaS (Software-as-a-Service) platforms has accelerated the adoption of subscription pricing, enabling seamless remote access and collaboration.

One-Time Purchase pricing model, also known as perpetual licensing, involves a single upfront payment that grants indefinite access to the software. This traditional pricing model is still prevalent for certain types of software, particularly desktop applications such as design tools, productivity suites, and specialized software that do not require continuous updates or cloud connectivity. One-time purchase appeals to users who prefer to avoid recurring fees and maintain full control over their software. However, this model may include optional paid upgrades or support contracts. While less dominant than subscription pricing, it remains relevant in markets where customers value ownership over subscription-based access.

Freemium pricing model offers a basic version of the software free of charge, while charging for premium features, advanced capabilities, or enhanced support. This model is widely used for consumer-focused applications, mobile apps, and SaaS platforms looking to build a large user base quickly. Freemium models help publishers gain market penetration and user engagement by providing essential functionality for free and incentivizing users to upgrade. Monetization usually comes from upselling premium tiers or add-ons. This approach is particularly effective for software products that benefit from network effects, such as communication tools or collaboration platforms.

Pay-Per-Use pricing charges customers based on the actual consumption of software resources or services, rather than a fixed fee. This model is common in cloud computing services, data analytics platforms, and APIs, where usage varies significantly between users. It allows businesses to align costs directly with usage, providing cost efficiency and flexibility. Pay-per-use models are favored in environments with fluctuating workloads or seasonal demands, such as big data processing, streaming services, or high-performance computing. This pricing structure encourages optimization of resource use but can lead to unpredictable monthly expenses if not monitored carefully.

Volume Licensing targets large organizations or enterprises that require multiple copies of software for extensive deployment across many users or devices. This pricing model offers discounted rates based on the quantity of licenses purchased, providing cost savings and simplified license management. Volume licensing agreements often come with added benefits such as dedicated support, customizations, and centralized billing. This model is prevalent in sectors such as government, education, and large enterprises where widespread software adoption is necessary. Volume licensing supports scalability and long-term partnerships between software publishers and large clients.

Software Publishers Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the software publishers market, led by the United States which is home to many of the world’s largest and most influential software companies. The region benefits from a mature technology infrastructure, high digital adoption rates, and strong demand across sectors such as finance, healthcare, education, and government. Key software segments—such as enterprise applications, cloud platforms, cybersecurity solutions, and development tools—see continuous innovation supported by robust venture capital and R&D investment. The presence of major tech hubs like Silicon Valley, Seattle, and Austin fosters a thriving ecosystem for startups and large-scale enterprises alike. Additionally, favorable regulatory conditions for digital businesses and strong IP protections further reinforce the region's leadership.

Europe holds a significant share of the global software publishing market, driven by the digital transformation initiatives across various industries, particularly in Western Europe. Countries like Germany, the UK, and France have well-developed IT sectors and a growing demand for cloud-based software, enterprise solutions, and AI-driven applications. Government-led digital initiatives such as the EU’s Digital Strategy and GDPR compliance requirements also push organizations to invest in advanced software products. While the region faces challenges related to market fragmentation and stringent data protection regulations, it continues to invest heavily in AI, edge computing, and cybersecurity solutions to stay competitive.

Asia-Pacific is the fastest-growing region in the software publishers market, with countries such as China, India, Japan, and South Korea leading adoption. Rapid digitalization, increased smartphone penetration, and a surge in internet users are driving demand for software across education, finance, retail, and government sectors. India, in particular, is emerging as a global software development hub, with a thriving ecosystem of software service providers, startups, and exporters. Meanwhile, Japan and South Korea are pushing advancements in industrial software and automation. Despite high growth, the region faces challenges such as uneven infrastructure development and regulatory discrepancies across countries.

Latin America is experiencing growing demand for software publishing, especially in business management, customer relationship, and enterprise mobility solutions. Countries such as Brazil, Mexico, and Argentina are at the forefront, with expanding IT industries and increasing demand for cloud and SaaS applications among SMEs. Economic fluctuations and limited access to high-speed internet in some areas pose hurdles, but digital transformation efforts and increased government initiatives in e-governance and education are helping expand the market.

Middle East and Africa present emerging opportunities in the software publishers market, fueled by digital transformation in government services, education, and financial sectors. The Gulf Cooperation Council (GCC) countries, including the UAE and Saudi Arabia, are heavily investing in smart cities, cybersecurity infrastructure, and AI applications, creating demand for software publishing. In Africa, countries like South Africa, Kenya, and Nigeria are adopting mobile-based and cloud-driven software solutions to improve access to services. However, challenges such as low digital literacy, underdeveloped infrastructure, and limited funding for startups restrict the pace of market expansion.

Software Publishers Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the software publishers market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global software publishers market include:

- Microsoft

- HP

- Oracle

- Dell Technologies

- IBM

The global software publishers market is segmented as follows:

By Software Type

- Application Software

- System Software

- Development Software

- Security Software

- Database Management Software

By Deployment Method

- On-Premises Software

- Cloud-Based Software

- Hybrid Deployment

By Target User

- Individual Users

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- Government Entities

- Educational Institutions

By Industry Vertical

- Healthcare

- Finance and Banking

- Retail

- Manufacturing

- Information Technology

By Pricing Model

- Subscription-Based

- One-Time Purchase

- Freemium

- Pay-Per-Use

- Volume Licensing

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Software Publishers

Request Sample

Software Publishers