Spine Implant Devices Market Size, Share, and Trends Analysis Report

CAGR :

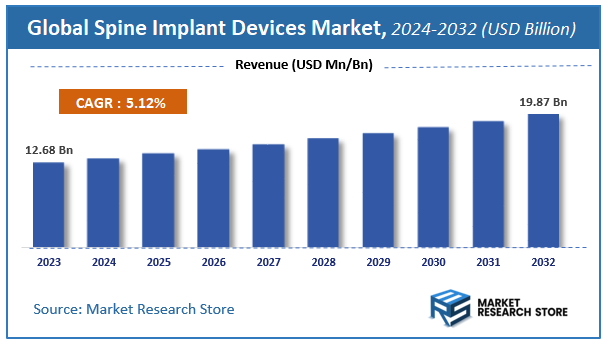

| Market Size 2023 (Base Year) | USD 12.68 Billion |

| Market Size 2032 (Forecast Year) | USD 19.87 Billion |

| CAGR | 5.12% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Spine Implant Devices Market Insights

According to Market Research Store, the global spine implant devices market size was valued at around USD 12.68 billion in 2023 and is estimated to reach USD 19.87 billion by 2032, to register a CAGR of approximately 5.12% in terms of revenue during the forecast period 2024-2032.

The spine implant devices report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Spine Implant Devices Market: Overview

Spine implant devices are medical devices designed to treat and manage various spinal conditions, including degenerative diseases, spinal deformities, fractures, and injuries. These devices are surgically inserted into the spine to stabilize, support, or correct the alignment of the vertebrae. Common types of spine implant devices include spinal fusion devices, artificial disc replacements, interbody cages, rods, screws, plates, and spinal hooks. These implants are made from biocompatible materials such as titanium, stainless steel, and PEEK (polyetheretherketone), which offer strength, durability, and compatibility with human tissue.

The market for spine implant devices is growing due to the increasing prevalence of spinal disorders, the aging global population, and advances in surgical technologies. Minimally invasive surgical techniques, which involve smaller incisions and faster recovery times, are further driving demand for innovative spine implants. Additionally, the development of advanced materials and 3D-printed implants that can be tailored to individual patients' anatomical needs is expanding the scope of treatments available. With continued research into improving the longevity and functionality of spine implants, the market is expected to grow significantly, particularly as the demand for personalized and less invasive spinal treatments increases.

Key Highlights

- The spine implant devices market is anticipated to grow at a CAGR of 5.12% during the forecast period.

- The global spine implant devices market was estimated to be worth approximately USD 12.68 billion in 2023 and is projected to reach a value of USD 19.87 billion by 2032.

- The growth of the spine implant devices market is being driven by the increasing number of individuals affected by spinal disorders, particularly within the aging global population.

- Based on the product, the spinal fusion and fixation segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the hospital segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Spine Implant Devices Market: Dynamics

Key Growth Drivers:

- Aging Global Population: The increasing proportion of elderly individuals worldwide is a significant driver, as age-related degenerative spinal conditions like spinal stenosis, osteoarthritis, and degenerative disc disease become more prevalent.

- Rising Prevalence of Spinal Disorders: Factors such as sedentary lifestyles, obesity, and physically demanding occupations contribute to a growing incidence of spinal disorders, including herniated discs, scoliosis, and spinal injuries.

- Technological Advancements in Implant Design and Materials: Innovations in implant materials (e.g., titanium alloys, PEEK), minimally invasive surgical (MIS) techniques, and implant designs (e.g., motion-preserving devices, expandable cages) are improving patient outcomes and driving market growth.

- Increasing Adoption of Minimally Invasive Surgery (MIS): MIS procedures offer benefits like reduced blood loss, shorter hospital stays, and faster recovery times, leading to greater demand for MIS-compatible spine implants.

- Growing Awareness and Acceptance of Surgical Interventions: As surgical techniques and implant technologies improve, both patients and physicians are becoming more comfortable with surgical interventions for spinal conditions.

- Favorable Reimbursement Policies in Developed Nations: Adequate reimbursement for spine surgeries and implant devices in developed countries supports market growth by making these treatments more accessible.

- Demand for Improved Quality of Life: Patients suffering from chronic back pain and spinal deformities are increasingly seeking surgical solutions to alleviate pain, improve function, and enhance their quality of life.

Restraints:

- High Cost of Spinal Implant Procedures: Spine surgery and the associated implant devices can be expensive, potentially limiting access for patients without adequate insurance coverage or in regions with less developed healthcare systems.

- Stringent Regulatory Approval Processes: The development and commercialization of new spine implant devices require rigorous testing and lengthy approval processes by regulatory bodies like the FDA and EMA, which can increase time-to-market and development costs.

- Clinical Risks and Potential Complications: Spine surgery carries inherent risks, including infection, nerve damage, and implant failure, which can deter some patients and surgeons.

- Lack of Long-Term Clinical Data for Novel Devices: For newer implant technologies, long-term clinical data on their efficacy and safety may be limited, leading to cautious adoption by some surgeons.

- Reimbursement Pressures and Cost Containment Measures: Healthcare payers are increasingly focused on cost containment, which can put pressure on the pricing and reimbursement rates for spine implant devices.

- Availability of Alternative Treatment Options: Non-surgical treatments like physical therapy, pain management, and medication may be preferred as initial options, limiting the immediate need for surgical intervention and implants.

- Concerns Regarding Implant Longevity and Revision Surgeries: The need for revision surgeries due to implant failure or adjacent segment disease can be a concern for both patients and surgeons.

Opportunities:

- Development of Bioresorbable and Biodegradable Implants: The development of implants that gradually degrade and are absorbed by the body could eliminate the need for permanent implants and potential long-term complications.

- Advancements in Spinal Biologics and Tissue Engineering: Innovations in bone grafts, growth factors, and cell-based therapies used in conjunction with implants can enhance fusion rates and improve healing.

- Personalized and Patient-Specific Implants: Utilizing 3D printing and imaging technologies to create customized implants tailored to individual patient anatomy can improve surgical outcomes.

- Expansion in Emerging Markets: The growing healthcare infrastructure and increasing awareness of treatment options in developing countries present significant growth opportunities for spine implant manufacturers.

- Integration of Navigation and Robotics in Spine Surgery: The use of surgical navigation systems and robotics can enhance the precision and safety of implant placement, driving demand for compatible devices.

- Focus on Motion Preservation Technologies: The development and adoption of non-fusion implants like artificial discs aim to maintain spinal motion and potentially reduce the risk of adjacent segment disease.

- Telemedicine and Remote Monitoring for Post-Operative Care: Leveraging digital health technologies for remote patient monitoring and follow-up after spine surgery can improve patient outcomes and reduce healthcare costs.

Challenges:

- Demonstrating Long-Term Clinical Efficacy and Safety: Providing robust evidence of the long-term benefits and safety of spine implant devices is crucial for gaining widespread adoption and favorable reimbursement.

- Managing the High Costs Associated with Research and Development: The development of innovative spine implant technologies requires significant financial investment and carries inherent risks.

- Navigating the Complex and Evolving Regulatory Landscape: Keeping up with and adhering to the varying and often stringent regulatory requirements across different global markets.

- Addressing the Ethical Considerations of Implant Use: Ensuring equitable access to these technologies and addressing potential conflicts of interest in their promotion and utilization.

- Educating Surgeons on New Technologies and Techniques: Providing adequate training and support to surgeons on the proper use of novel spine implant devices and surgical approaches.

- Combating Counterfeit and Substandard Products: Ensuring the authenticity and quality of spine implant devices to protect patient safety.

- Adapting to the Increasing Focus on Value-Based Healthcare: Demonstrating the cost-effectiveness and long-term value of spine implant procedures compared to other treatment options.

Spine Implant Devices Market: Report Scope

This report thoroughly analyzes the Spine Implant Devices Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Spine Implant Devices Market |

| Market Size in 2023 | USD 12.68 Billion |

| Market Forecast in 2032 | USD 19.87 Billion |

| Growth Rate | CAGR of 5.12% |

| Number of Pages | 162 |

| Key Companies Covered | Stryker, Ulrich Medicals, Zimmer Biomet Corporation, Globus medical, Aesculap Implant Systems, Orthofix International, Titan Spine, Medtronic, DePuy Synthes |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Spine Implant Devices Market: Segmentation Insights

The global spine implant devices market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global spine implant devices market is divided into spinal fusion and fixation, vertebral compression fracture treatment, non-fusion, and motion preservation.

Spinal Fusion and Fixation this product category dominates the spine implant devices market due to the high demand for spinal fusion surgeries, which are commonly performed to treat conditions such as degenerative disc disease, scoliosis, and spinal fractures. Spinal fusion and fixation devices, including screws, rods, plates, and cages, help stabilize the spine by fusing two or more vertebrae. The increasing prevalence of spinal disorders, coupled with advancements in surgical techniques, has driven the adoption of these devices in both elective and emergency surgeries.

Vertebral Compression Fracture Treatment this segment is focused on the treatment of vertebral compression fractures (VCFs), which are commonly caused by osteoporosis. Devices used for vertebral compression fracture treatment, such as kyphoplasty and vertebroplasty tools, help restore vertebral height and alleviate pain. The growing elderly population and the rising incidence of osteoporosis-related fractures have contributed to the market growth in this category. These treatments are minimally invasive, offering quicker recovery times and fewer complications compared to traditional surgeries, making them highly popular.

Non-Fusion spine implants, such as dynamic stabilization devices, are used for treating degenerative disc disease, lumbar instability, and certain conditions where fusion is not appropriate. This segment is growing due to the shift toward preserving motion in the spine, rather than restricting it through fusion. Non-fusion implants allow for better mobility and are becoming increasingly preferred in certain cases, particularly among younger, more active patients. The market for non-fusion devices is expected to expand as surgeons and patients seek alternatives to traditional fusion procedures.

Motion Preservation devices are designed to maintain the natural motion of the spine, particularly in cases of degenerative disc disease or spinal deformities. These devices, such as artificial disc replacements and interspinous spacers, are used to replace damaged discs while preserving spinal movement. The increasing focus on minimizing the long-term consequences of spinal fusion, such as adjacent segment disease, has led to the growing adoption of motion preservation devices. This segment is expected to see significant growth, particularly with advancements in technology that improve device performance and safety.

Segmentation Insights by Application

On the basis of application, the global spine implant devices market is bifurcated into hospital, clinic, and other.

Hospital are the dominant application segment in the spine implant devices market, primarily due to their ability to provide a wide range of advanced medical services, including surgical procedures for complex spine conditions. Hospitals, especially those with specialized orthopedic and neurosurgery departments, perform the majority of spine surgeries, such as spinal fusion, vertebral compression fracture treatments, and motion preservation surgeries. These medical institutions typically have access to the latest technology and equipment, allowing them to handle a diverse patient base, including those with severe spinal disorders. The demand for spine implants in hospitals is expected to continue growing due to increasing incidences of spine-related conditions, the aging population, and advancements in surgical techniques.

Clinic, particularly specialized orthopedic and spine clinics, play an important role in the spine implant devices market. While they typically handle less complex cases than hospitals, they are still a significant source of demand for spine implants, especially for non-invasive or minimally invasive procedures. Clinics offer a more personalized and less resource-intensive approach to spine care, often providing consultations, diagnostic imaging, and follow-up care for patients undergoing spinal treatments. With the rise in outpatient spine surgeries and treatments, clinics are expected to see an increase in the demand for spine implants. The growing trend towards minimally invasive surgeries, which can be performed in clinic settings, is expected to further drive this segment’s growth.

Spine Implant Devices Market: Regional Insights

- North America is expected to dominate the global market.

North America dominates the Spine Implant Devices Market, driven by the region's advanced healthcare infrastructure, high prevalence of spinal disorders, and well-established medical device industry. The United States holds a significant market share, with a large number of hospitals, specialized clinics, and spine surgeons contributing to the demand for spine implants. Key factors such as an aging population, increasing incidences of spinal injuries, and technological advancements in minimally invasive spine surgery are major drivers. Additionally, the region’s regulatory environment, especially the approval of new and innovative spine implant devices by the U.S. Food and Drug Administration (FDA), has further fueled the market growth. North America's focus on high-quality healthcare and cutting-edge innovations in spinal surgery technologies ensures that it remains the dominant region in this market.

Europe holds a substantial share in the Spine Implant Devices Market, with countries such as Germany, France, Italy, and the United Kingdom leading the demand. The European market benefits from a large elderly population, rising healthcare expenditure, and growing awareness of advanced spinal surgeries. The presence of key players in the spine implant industry, particularly in countries like Germany and Switzerland, contributes to the development and availability of innovative spine implant devices. The increasing number of spine surgeries, such as spinal fusion and disc replacement, further drives demand in the region. Additionally, Europe's robust healthcare systems, along with government-backed medical reimbursements, continue to support market growth, despite challenges such as regulatory complexities in some countries.

Asia-Pacific region is the fastest-growing market for Spine Implant Devices, driven by increasing healthcare spending, rising incidences of spinal deformities, and a rapidly aging population in countries like China, India, Japan, and Australia. The growing adoption of advanced healthcare technologies, along with increasing awareness of spinal health, has led to a rise in the number of spine surgeries and a corresponding demand for spine implants. In particular, India and China are seeing a rapid increase in medical tourism for spinal treatments, further driving the market. Moreover, countries like Japan and South Korea have well-established healthcare systems that are increasingly adopting minimally invasive spine surgeries, thus accelerating the growth of the spine implant market.

Latin America region is experiencing steady growth in the Spine Implant Devices Market, driven by increasing healthcare awareness, a growing elderly population, and a rise in spinal injuries due to lifestyle changes and accidents. Countries like Brazil, Mexico, and Argentina are leading the adoption of spine implants, although the market remains constrained by challenges such as high import costs, limited access to advanced healthcare technologies in rural areas, and economic instability. However, with healthcare infrastructure improvements, along with growing demand for minimally invasive spinal surgery and an increasing number of surgical procedures, Latin America presents significant growth opportunities for spine implant manufacturers.

Middle East and Africa region is an emerging market for Spine Implant Devices, with demand growing in countries like Saudi Arabia, United Arab Emirates, and South Africa. The market is driven by increasing investments in healthcare infrastructure, higher awareness about spinal health, and rising incidences of spinal disorders due to lifestyle factors, traffic accidents, and an aging population. Governments in the region are focusing on improving healthcare facilities and encouraging the adoption of advanced medical technologies, which drives the demand for high-quality spine implant devices. However, the market's growth is somewhat restrained by economic and political challenges, as well as limited access to healthcare in certain regions, especially in sub-Saharan Africa.

Spine Implant Devices Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the spine implant devices market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global spine implant devices market include:

- Stryker

- Ulrich Medicals

- Zimmer Biomet Corporation

- Globus medical

- Aesculap Implant Systems

- Orthofix International

- Titan Spine

- Medtronic

- DePuy Synthes

The global spine implant devices market is segmented as follows:

By Product

- Spinal Fusion and Fixation

- Vertebral Compression Fracture Treatment

- Non-Fusion

- Motion Preservation

By Application

- Hospital

- Clinic

- Other

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Spine Implant Devices

Request Sample

Spine Implant Devices