Surface Additives Market Size, Share, and Trends Analysis Report

CAGR :

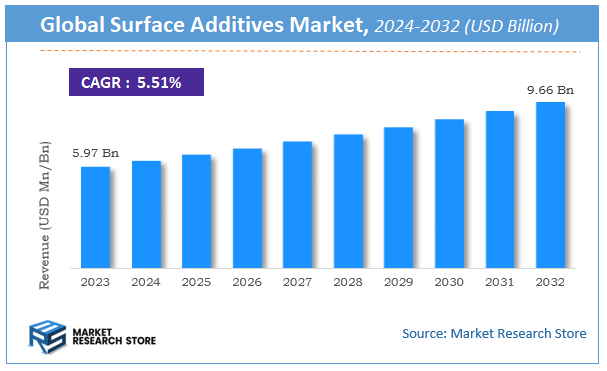

| Market Size 2023 (Base Year) | USD 5.97 Billion |

| Market Size 2032 (Forecast Year) | USD 9.66 Billion |

| CAGR | 5.51% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Surface Additives Market Insights

According to Market Research Store, the global surface additives market size was valued at around USD 5.97 billion in 2023 and is estimated to reach USD 9.66 billion by 2032, to register a CAGR of approximately 5.51% in terms of revenue during the forecast period 2024-2032.

The surface additives report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032

To Get more Insights, Request a Free Sample

Global Surface Additives Market: Overview

Surface additives are chemical compounds incorporated into coatings, paints, plastics, inks, adhesives, and other formulations to enhance or modify surface properties. These additives play a vital role in improving features such as slip, gloss, scratch resistance, anti-blocking, wetting, leveling, and anti-foaming. They help control the flow, spreadability, and appearance of products, ensuring optimal performance and finish. Common types of surface additives include silicones, waxes, acrylates, and fluoropolymers, each tailored to address specific requirements. Industries such as automotive, construction, packaging, and electronics heavily rely on surface additives to meet quality, durability, and aesthetic standards.

Key Highlights

- The surface additives market is anticipated to grow at a CAGR of 5.51% during the forecast period.

- The global surface additives market was estimated to be worth approximately USD 5.97 billion in 2023 and is projected to reach a value of USD 9.66 billion by 2032.

- The growth of the surface additives market is being driven by the rising demand for high-performance coatings and functional surfaces across various industries.

- Based on the type, the wetting agents segment is growing at a high rate and is projected to dominate the market.

- On the basis of functionality, the performance additives segment is projected to swipe the largest market share.

- In terms of application, the coatings and paints segment is expected to dominate the market.

- Based on the end-user industry, the automotive segment is expected to dominate the market.

- In terms of composition, the synthetic additives segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Surface Additives Market: Dynamics

Key Growth Drivers:

- Rising Demand from Automotive and Construction Sectors: Increasing use of surface additives to enhance durability, gloss, scratch resistance, and surface smoothness in automotive coatings and construction materials is fueling market growth.

- Growing Preference for High-Performance Coatings: Industries are demanding coatings with enhanced characteristics like UV resistance, anti-blocking, and improved wetting, all of which rely on surface additives for optimal performance.

- Booming Packaging Industry: Surface additives are widely used in packaging films and inks to improve surface properties like slip, anti-static behavior, and printability, supporting growth in tandem with the packaging industry's expansion.

- Expansion of the Paints & Coatings Industry: Rapid urbanization and infrastructure development, especially in emerging markets, are boosting demand for decorative and protective coatings, which drives surface additive usage.

- Advancements in Additive Technology: Continuous innovation in surface additive formulations, including nanotechnology and eco-friendly variants, is attracting more end users and opening up new application areas.

Restraints:

- Fluctuating Raw Material Prices: Volatility in prices of raw materials like silicones, waxes, and polymers affects production costs and may hinder profitability for manufacturers.

- Stringent Environmental Regulations: Regulatory pressure on VOC emissions and the use of certain chemicals in additives can restrict product formulation options and increase compliance costs.

- Limited Awareness in Developing Regions: In some emerging markets, the adoption of advanced surface additives is limited due to a lack of awareness or preference for lower-cost alternatives.

Opportunities:

- Growing Demand for Eco-Friendly Additives: The increasing emphasis on sustainability and green chemistry is creating demand for bio-based and waterborne surface additives with low environmental impact.

- Rising Applications in 3D Printing and Industrial Coatings: The expanding 3D printing sector and advanced industrial coatings are emerging as new frontiers for surface additive usage, offering lucrative growth potential.

- Innovation in Multifunctional Additives: Development of surface additives that combine multiple properties—such as anti-foaming, leveling, and dispersing—can attract industries looking for cost-effective and efficient solutions.

- Expansion into Emerging Economies: Rapid industrialization and growth in end-user industries across Asia-Pacific, Latin America, and the Middle East provide untapped potential for market players.

Challenges:

- Intense Market Competition: A large number of players, including multinational corporations and local suppliers, leads to price competition and margin pressure.

- Technical Complexity in Formulation: Achieving the right balance of performance characteristics while maintaining compatibility with various formulations can be complex and requires significant R&D investment.

- Supply Chain Disruptions: Global events such as pandemics, trade restrictions, and geopolitical tensions can disrupt the raw material supply chain, affecting production and delivery timelines.

- Customer Demand for Customization: End-users increasingly demand tailored additive solutions, which can complicate manufacturing processes and increase development time and cost.

Surface Additives Market: Report Scope

This report thoroughly analyzes the Surface Additives Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Surface Additives Market |

| Market Size in 2023 | USD 5.97 Billion |

| Market Forecast in 2032 | USD 9.66 Billion |

| Growth Rate | CAGR of 5.51% |

| Number of Pages | 174 |

| Key Companies Covered | BYK, Concentrol, KANSAI ALTAN, Deuteron, ADD-Additives, HSH Chemie, Balaji Chem Solutions |

| Segments Covered | By Type, By Functionality, By Application, By End-User Industry, By Composition, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Surface Additives Market: Segmentation Insights

The global surface additives market is divided by type, functionality, application, end-user industry, composition, and region.

Segmentation Insights by Type

Based on type, the global surface additives market is divided into wetting agents, dispersing agents, surfactants, emulsifiers, and leveling agents.

In the surface additives market, wetting agents emerge as the most dominant segment. These additives play a crucial role in improving the spreadability and adhesion of coatings or formulations on various substrates. By reducing the surface tension between the liquid and the surface, wetting agents enhance the uniformity of the application, making them indispensable in industries like paints, coatings, inks, and adhesives. Their widespread use across multiple end-use sectors due to their effectiveness in surface preparation and coverage makes them the leading segment in this market.

Dispersing agents follow closely, holding a significant share in the market. These additives help to evenly distribute solid particles within a liquid medium, preventing clumping or sedimentation. Dispersing agents are vital in maintaining the stability and consistency of formulations, especially in paints, pigments, and other chemical mixtures. Their importance in ensuring product quality and shelf life makes them widely adopted in industrial and commercial applications.

Surfactants come next in the ranking and are known for their versatility across several industries. They work by reducing surface and interfacial tension, thereby enhancing the interaction between different phases (like oil and water). Surfactants are commonly used not only in surface modification but also in cleaning agents, coatings, and emulsions. While essential, their generalized application across both industrial and consumer markets positions them slightly behind wetting and dispersing agents in terms of dominance in the surface additives segment.

Emulsifiers occupy a more niche yet essential role, particularly in maintaining the stability of emulsions—mixtures of immiscible liquids such as oil and water. In surface coatings and specialty chemicals, emulsifiers help in forming and maintaining uniform mixtures, which are crucial for consistent performance. Though not as widely used as wetting or dispersing agents, their necessity in specific formulations keeps them relevant in the market.

Leveling agents, while vital for ensuring smooth and defect-free surfaces in coatings and paints, represent the least dominant segment. These additives help eliminate surface irregularities and improve the final appearance of a product. Their application is somewhat specialized and often limited to high-end or precision-required finishes, which narrows their overall demand compared to other more broadly applicable additives.

Segmentation Insights by Functionality

On the basis of functionality, the global surface additives market is bifurcated into performance additives, processing aids, durability enhancers, stabilizers, and compatibility agents.

In the surface additives market, performance additives represent the most dominant segment by functionality. These additives are designed to enhance specific attributes of the final product, such as gloss, smoothness, anti-blocking, or anti-static properties. Their ability to directly improve product performance and aesthetics across a wide array of industries—including paints and coatings, plastics, and automotive—makes them highly valued and widely adopted. The versatility and targeted benefits they provide drive their strong demand and dominant market position.

Processing aids follow as the next most significant segment. These additives facilitate the manufacturing process by improving the flow, dispersion, or mixing characteristics of formulations during production. They are crucial in ensuring consistent processing, especially in high-volume manufacturing sectors such as plastic molding, extrusion, and coatings. While they do not typically alter the final product's end-use properties, their role in optimizing efficiency and production quality makes them integral to the supply chain.

Durability enhancers rank next in the hierarchy. These additives extend the lifespan of materials by improving resistance to environmental factors such as UV radiation, moisture, abrasion, and chemical exposure. Commonly used in construction materials, outdoor paints, and automotive coatings, durability enhancers ensure long-term performance. Though essential for certain applications, their demand is more concentrated in sectors where extended product life is critical.

Stabilizers are slightly less dominant, serving a specialized yet important function by maintaining the chemical and physical integrity of formulations over time. They help prevent degradation, discoloration, or phase separation during storage and use. While their role is vital in preserving product consistency, their narrower scope of application compared to performance or processing additives places them further down the list.

Compatibility agents, while important, constitute the least dominant segment. These additives are used to improve the miscibility and integration of different materials within a formulation—especially in blends of polymers or multi-component systems. Their specialized use in ensuring homogeneity and avoiding material incompatibilities makes them crucial for certain niche applications, but their overall demand remains limited relative to more broadly applied functionalities.

Segmentation Insights by Application

On the basis of application, the global surface additives market is bifurcated into coatings & paints, plastics, adhesives & sealants, cosmetics, and food & beverage.

In the surface additives market, coatings and paints represent the most dominant application segment. Surface additives are extensively used in this sector to improve properties such as spreadability, leveling, gloss, scratch resistance, and durability. These enhancements are critical in architectural, industrial, automotive, and decorative coatings, where performance and aesthetics are equally important. The vast scale of the coatings and paints industry, combined with its need for continual performance improvements, positions it as the largest consumer of surface additives.

Following closely is the plastics segment, which relies heavily on surface additives to improve processing efficiency and final product quality. Additives in this application help with anti-static behavior, surface smoothness, and compatibility among different polymers. Given the widespread use of plastics across packaging, automotive, electronics, and consumer goods, the demand for additives in this sector remains robust and diverse.

The adhesives and sealants segment also plays a significant role, with surface additives being used to enhance spreadability, adhesion, flexibility, and curing properties. These applications are essential in construction, electronics, and industrial bonding. Although not as large as the coatings or plastics industries, adhesives and sealants require high-performance customization, which drives consistent demand for advanced surface additives.

Cosmetics represent a more specialized yet important application area. Surface additives in cosmetics are used to enhance product texture, spreadability, and stability. They also contribute to the visual appeal and sensory properties of skincare and makeup products. While the volume demand is lower compared to industrial sectors, the value per unit and innovation rate in cosmetic formulations maintain steady interest in high-quality additives.

Lastly, the food and beverage segment is the least dominant in the surface additives market. Here, additives are used in very specific applications, such as improving surface gloss or preventing sticking in packaging. Due to strict regulatory constraints and the limited scope of use, this segment generates lower demand compared to the others, though it still represents a niche opportunity, particularly in food-grade and biodegradable additive formulations.

Segmentation Insights by End-User Industry

Based on end-user industry, the global surface additives market is divided into aerospace, automotive, construction, consumer goods, and electronics.

In the surface additives market, the automotive industry stands as the most dominant end-user segment. Surface additives are widely utilized in automotive coatings, interior plastics, adhesives, and sealants to enhance durability, appearance, chemical resistance, and UV stability. As the industry continuously evolves to meet stricter performance and aesthetic standards—especially with the growth of electric vehicles and lightweight materials—surface additives play a crucial role in improving product longevity and performance, making this sector the largest consumer.

The construction industry follows closely, driven by its extensive use of paints, sealants, adhesives, and coatings. Surface additives in this sector are essential for improving weather resistance, adhesion, leveling, and durability of construction materials. Whether in infrastructure, residential, or commercial projects, the need for protective and high-performance surface treatments makes construction a major contributor to the market.

Consumer goods form the next significant segment, encompassing a wide range of products including household items, packaging, and personal care goods. Surface additives enhance product aesthetics, texture, shelf life, and user experience in these applications. With rising consumer expectations for quality and performance in everyday products, this segment continues to see steady demand for functional surface additives.

The electronics industry uses surface additives in specialized applications such as coatings for circuit boards, casings, and protective films. These additives enhance properties like antistatic behavior, smoothness, and resistance to heat or chemicals. While smaller in volume compared to automotive or construction, the electronics sector demands high-precision and high-performance materials, maintaining a consistent if smaller share of the market.

Lastly, the aerospace industry represents the least dominant end-user segment. Despite its relatively low volume demand, the sector requires highly specialized and regulatory-compliant surface additives to improve thermal stability, corrosion resistance, and aerodynamic surface quality. The niche nature and high cost of aerospace applications limit its overall market share, though the value of additives used per unit is typically higher than in other industries.

Segmentation Insights by Composition

On the basis of composition, the global surface additives market is bifurcated into organic additives, inorganic additives, polymeric additives, natural & bio-based additives, and synthetic additives.

In the surface additives market, synthetic additives represent the most dominant segment by composition. These are chemically engineered compounds designed to deliver precise performance characteristics such as enhanced durability, leveling, wetting, and gloss. Their consistency, adaptability, and compatibility with a wide range of formulations—especially in coatings, plastics, and industrial applications—make synthetic additives highly preferred across numerous industries. Their dominance is largely attributed to their cost-effectiveness, availability, and well-established performance profiles.

Polymeric additives follow closely, offering superior performance in terms of film formation, flow control, and surface modification. These additives are particularly valued in high-performance coatings and plastic formulations due to their molecular structure, which allows for better integration and functionality in complex formulations. They are widely used in automotive, construction, and industrial applications where specific surface behaviors like scratch resistance and chemical resilience are crucial.

Organic additives also hold a significant share, especially in applications requiring compatibility with organic compounds or formulations. These include surfactants, dispersants, and emulsifiers derived from carbon-based molecules. They are widely used in industries like paints, adhesives, and cosmetics, providing effective surface interaction properties. Their popularity stems from their versatility, although they sometimes lag behind polymeric and synthetic additives in terms of durability under harsh environmental conditions.

Inorganic additives, while essential in certain technical applications, occupy a smaller portion of the market. These include compounds such as silica, metal oxides, and clays used to provide texture, thermal stability, or matte finishes. Their primary strength lies in enhancing mechanical and thermal properties, making them suitable for specific industrial applications. However, their relatively rigid chemical nature limits their flexibility in a broader range of formulations.

Natural and bio-based additives represent the least dominant segment, though they are gaining traction due to increasing environmental regulations and consumer demand for sustainable products. Derived from renewable sources like plant oils, starches, and biopolymers, these additives are primarily used in eco-friendly coatings, packaging, and cosmetics. Despite their ecological benefits, limitations in performance consistency, higher costs, and formulation challenges have kept their market share comparatively low—for now.

Surface Additives Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific is the most dominant region in the global surface additives market, driven by rapid industrial expansion, urban growth, and rising demand across key industries such as coatings, plastics, printing inks, and packaging. Countries like China and India play pivotal roles due to their vast manufacturing bases and growing construction sectors. The region also benefits from increasing consumer awareness and demand for high-performance materials in automotive and electronics, further pushing the market forward.

North America holds a significant share in the surface additives market, fueled by technological advancements and a strong industrial base. The United States leads with well-established construction, automotive, and packaging sectors that rely heavily on high-quality coatings and plastic modifiers. Continued investment in R&D and innovation ensures sustained demand for advanced surface additive formulations, particularly in environmentally regulated applications.

Europe follows closely, with its surface additives market shaped by stringent environmental standards and a high focus on sustainable solutions. Countries such as Germany, France, and the UK are frontrunners in developing eco-friendly additives for use in paints, coatings, and packaging materials. The region’s emphasis on reducing VOC emissions and enhancing product durability contributes to steady market demand.

Latin America is experiencing moderate growth, supported by increasing construction activities and the expansion of the automotive and consumer goods sectors. Brazil and Mexico are the primary contributors, with infrastructure development and rising urban populations driving the need for surface-enhancing materials. The region’s emerging economies are gradually adopting newer technologies, pushing the market upward.

Middle East and Africa represent the least dominant but steadily growing region in the surface additives market. Economic diversification, particularly in the Gulf countries, is encouraging industrial development. The demand for advanced coatings and surface treatment products in construction and transportation is rising, especially in the UAE and Saudi Arabia, contributing to a gradual market expansion.

Surface Additives Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the surface additives market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global surface additives market include:

- BYK

- Concentrol

- KANSAI ALTAN

- Deuteron

- ADD-Additives

- HSH Chemie

- Balaji Chem Solutions

The global surface additives market is segmented as follows:

By Type

- Wetting Agents

- Dispersing Agents

- Surfactants

- Emulsifiers

- Leveling Agents

By Functionality

- Performance Additives

- Processing Aids

- Durability Enhancers

- Stabilizers

- Compatibility Agents

By Application

- Coatings and Paints

- Plastics

- Adhesives and Sealants

- Cosmetics

- Food and Beverage

By End-User Industry

- Aerospace

- Automotive

- Construction

- Consumer Goods

- Electronics

By Composition

- Organic Additives

- Inorganic Additives

- Polymeric Additives

- Natural and Bio-Based Additives

- Synthetic Additives

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Surface Additives

Request Sample

Surface Additives