Technical Fluid Market Size, Share, and Trends Analysis Report

CAGR :

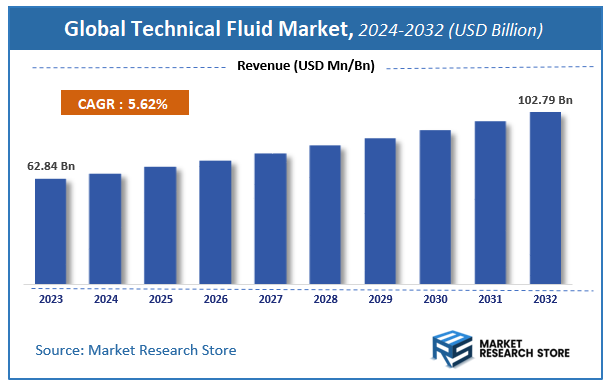

| Market Size 2023 (Base Year) | USD 62.84 Billion |

| Market Size 2032 (Forecast Year) | USD 102.79 Billion |

| CAGR | 5.62% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Technical Fluid Market Insights

According to Market Research Store, the global technical fluid market size was valued at around USD 62.84 billion in 2023 and is estimated to reach USD 102.79 billion by 2032, to register a CAGR of approximately 5.62% in terms of revenue during the forecast period 2024-2032.

The technical fluid report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Technical Fluid Market: Overview

Technical fluid refers to a broad category of specialized liquids used in industrial, automotive, aerospace, and manufacturing sectors to enable, enhance, or protect the function of machinery and equipment. These fluids serve a wide array of purposes such as lubrication, heat transfer, hydraulic power transmission, corrosion resistance, and system cleaning. Common types include lubricants, coolants, transmission fluids, brake fluids, cutting oils, and dielectric fluids. Each formulation is engineered to meet specific performance requirements under varying environmental and operational conditions. The selection of a technical fluid depends on factors like material compatibility, operating temperature range, pressure tolerance, and safety or regulatory compliance.

Key Highlights

- The technical fluid market is anticipated to grow at a CAGR of 5.62% during the forecast period.

- The global technical fluid market was estimated to be worth approximately USD 62.84 billion in 2023 and is projected to reach a value of USD 102.79 billion by 2032.

- The growth of the technical fluid market is being driven by increasing industrialization and technological advancements across key sectors such as automotive, manufacturing, construction, and energy.

- Based on the type of fluid, the lubricants segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the automotive sector segment is projected to swipe the largest market share.

- In terms of base oil type, the mineral oil segment is expected to dominate the market.

- Based on the end-user industry, the manufacturing industry segment is expected to dominate the market.

- In terms of functionality, the anti-wear segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Technical Fluid Market: Dynamics

Key Growth Drivers:

- Rising Demand from Automotive and Manufacturing Industries: Increasing use of technical fluids like lubricants, coolants, and hydraulic fluids in automotive and industrial equipment drives market growth due to expanding vehicle production and industrial activities.

- Technological Advancements in Fluid Formulations: Innovations in synthetic and semi-synthetic fluids that enhance performance, reduce maintenance needs, and improve energy efficiency are encouraging adoption across various sectors.

- Growth in the Electronics and Semiconductor Industry: The need for specialized heat transfer and dielectric fluids is increasing due to the growing complexity and miniaturization of electronic components and devices.

- Stringent Emission and Efficiency Regulations: Environmental and energy-efficiency mandates are prompting industries to shift toward eco-friendly and high-performance technical fluids.

- Expansion of Renewable Energy Projects: Wind turbines and solar systems require specific fluids for cooling and lubrication, contributing to the rising demand for technical fluids in renewable energy applications.

Restraints:

- High Cost of Advanced Technical Fluids: Premium formulations and synthetic fluids can be expensive, which may discourage adoption, particularly in price-sensitive markets and among small manufacturers.

- Volatility in Raw Material Prices: Fluctuations in the cost of base oils, additives, and petrochemical derivatives can impact product pricing and profitability.

- Environmental Concerns and Disposal Regulations: Disposal and spillage of technical fluids pose environmental hazards, leading to stricter regulations and compliance costs for manufacturers and users.

Opportunities:

- Shift Toward Bio-Based and Sustainable Fluids: Growing environmental awareness and regulatory support are creating demand for biodegradable and less toxic alternatives to conventional technical fluids.

- Emerging Markets and Industrialization: Rapid industrial growth and infrastructure development in emerging economies, particularly in Asia-Pacific and Africa, are opening new avenues for technical fluid suppliers.

- Adoption of Industry 4.0 and Automation: The integration of automated and precision machinery in manufacturing sectors requires highly specialized fluids, boosting the need for advanced technical fluid solutions.

- Customized Product Offerings for Niche Applications: Providing tailor-made technical fluids for specific applications in aerospace, marine, or medical devices can help companies gain a competitive edge.

Challenges:

- Intense Market Competition and Price Pressure: The presence of numerous players, including local and international brands, creates pricing pressure and limits profit margins.

- Lack of Standardization Across Regions: Varied regulations and standards across different countries make it difficult for manufacturers to ensure compliance and streamline production and distribution.

- Awareness and Adoption Barriers in Developing Regions: Limited awareness about the benefits of high-performance fluids can hinder market penetration in underdeveloped or cost-sensitive regions.

- Counterfeit and Low-Quality Products: The presence of substandard and counterfeit products in the market can affect brand reputation and customer trust, particularly in unregulated regions.

Technical Fluid Market: Report Scope

This report thoroughly analyzes the Technical Fluid Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Technical Fluid Market |

| Market Size in 2023 | USD 62.84 Billion |

| Market Forecast in 2032 | USD 102.79 Billion |

| Growth Rate | CAGR of 5.62% |

| Number of Pages | 177 |

| Key Companies Covered | Arkema Group, VOLTRONIC GmbH, NISOTEC, BIZOL Germany GmbH, Nefteproduct JSC, CIMCOOL Industrial Products, Exxon Mobil Corporation, Multitherm, Dynalene |

| Segments Covered | By Type of Fluid, By Application, By Base Oil Type, By End-user Industry, By Functionality, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Technical Fluid Market: Segmentation Insights

The global technical fluid market is divided by type of fluid, application, base oil type, end-user industry, functionality, and region.

Segmentation Insights by Type of Fluid

Based on type of fluid, the global technical fluid market is divided into hydraulic fluids, lubricants, coolants, heat transfer fluids, and fuel additives.

In the technical fluid market, lubricants represent the most dominant segment among the various fluid types. Lubricants are extensively used across automotive, industrial, marine, and aerospace sectors for reducing friction, preventing wear and tear, and ensuring smooth machinery operation. Their indispensable role in equipment maintenance, combined with continuous demand from automotive and heavy industrial machinery markets, makes lubricants the leading contributor to the market's revenue.

Following lubricants, hydraulic fluids hold a significant share in the technical fluid market. These fluids are vital for transferring power in hydraulic systems, commonly found in construction equipment, manufacturing machinery, aviation systems, and automotive applications. The increased industrialization and mechanization globally, particularly in emerging economies, continue to drive demand for hydraulic fluids.

Next in line are coolants, which play a crucial role in regulating temperature in engines and industrial processes. Coolants are widely used in internal combustion engines to prevent overheating and maintain operational efficiency. With the ongoing growth of the automotive industry and increased emphasis on efficient thermal management in manufacturing environments, this segment continues to expand steadily.

Heat transfer fluids occupy a smaller portion of the market compared to the above segments. These are specialized fluids used in systems requiring precise temperature control, such as chemical processing, pharmaceuticals, solar power plants, and food processing industries. While they serve critical functions, their application is generally limited to niche sectors, which keeps their market share relatively moderate.

The fuel additives segment represents the smallest share among the types of technical fluids. Fuel additives are compounds added to fuel to enhance its performance, efficiency, and cleanliness. While they are important for maintaining engine health and reducing emissions, their market is narrower and highly dependent on fuel quality regulations and regional consumption patterns, particularly as the global focus gradually shifts toward alternative fuels and electric vehicles.

Segmentation Insights by Application

On the basis of application, the global technical fluid market is bifurcated into automotive, aerospace, industrial machinery, marine, and oil & gas.

In terms of application, the automotive sector dominates the technical fluid market. The vast global fleet of passenger and commercial vehicles consistently demands large volumes of lubricants, coolants, hydraulic fluids, and fuel additives to ensure performance, longevity, and emissions compliance. With the rise in vehicle production, maintenance needs, and increasing consumer awareness of high-performance fluids, this segment remains the primary driver of the technical fluid industry.

The industrial machinery segment follows closely behind, leveraging technical fluids such as lubricants, hydraulic fluids, and heat transfer fluids to maintain operational efficiency across manufacturing plants, construction equipment, and heavy machinery. Rapid industrialization in developing countries and automation in manufacturing processes significantly boost demand in this segment, making it a vital pillar of the technical fluid market.

Next is the oil & gas sector, which utilizes a wide range of technical fluids in exploration, drilling, refining, and transportation processes. These fluids ensure the safe and efficient operation of high-pressure, high-temperature systems, particularly in offshore and harsh environment applications. While the sector's dependency on volatile crude prices affects fluid demand, its scale and complexity secure a stable market share.

The aerospace segment requires highly specialized technical fluids, including advanced lubricants and hydraulic fluids, designed to withstand extreme conditions and meet stringent regulatory standards. Though it contributes a smaller volume relative to automotive and industrial sectors, its demand is value-intensive due to the high quality and performance requirements of aerospace systems.

Lastly, the marine sector holds the least share in the market. Technical fluids are essential here for vessel engines, hydraulic systems, and other onboard equipment. However, this segment is constrained by relatively slower fleet growth and stricter environmental regulations, which limit consumption and require a shift toward more environmentally friendly fluid alternatives.

Segmentation Insights by Base Oil Type

Based on base oil type, the global technical fluid market is divided into mineral oil, synthetic oil, bio-based oil, and water-based fluids.

In the technical fluid market, mineral oil-based fluids are the most dominant by base oil type. Derived from refined crude oil, mineral oils are cost-effective and widely used in automotive, industrial, and marine applications. Their broad availability, established infrastructure, and compatibility with a variety of equipment make them the go-to choice for many end users, especially in price-sensitive markets. Despite growing environmental concerns, their dominance persists due to affordability and long-standing industry familiarity.

Synthetic oils follow as the second most dominant base oil type. These fluids offer superior thermal stability, oxidation resistance, and performance in extreme conditions, making them ideal for high-end automotive engines, aerospace, and precision industrial machinery. Though more expensive than mineral oils, their longer service life and performance benefits justify their use in applications demanding high reliability and efficiency. The growing preference for premium-grade fluids in developed markets is gradually expanding the share of synthetic oils.

Bio-based oils are gaining traction but currently occupy a smaller market share. Made from renewable sources like vegetable oils, they offer environmentally friendly alternatives to petroleum-based fluids. Their biodegradability and low toxicity make them attractive in ecologically sensitive industries and for regulatory compliance. However, issues such as limited oxidative stability, higher production costs, and compatibility concerns with existing equipment have kept their adoption relatively modest.

Water-based fluids hold the smallest share among all base oil types. These fluids, often used in specialized cooling and fire-resistant applications, have niche utility in industries like metalworking and fire-prone environments. While they offer advantages like non-flammability and environmental safety, their limited lubricating properties and susceptibility to microbial growth restrict their use to specific, controlled applications.

Segmentation Insights by End-user Industry

On the basis of end-user industry, the global technical fluid market is bifurcated into manufacturing, construction, energy and utilities, transportation, and agriculture.

In the technical fluid market, the manufacturing industry stands as the most dominant end-user segment. This sector consumes large volumes of lubricants, hydraulic fluids, coolants, and heat transfer fluids to support continuous operation of machinery and equipment across diverse sub-industries like automotive, electronics, metal fabrication, and chemicals. The need for operational efficiency, reduced downtime, and extended equipment life drives steady and large-scale demand for technical fluids in manufacturing environments worldwide.

The transportation sector is the second-largest consumer, encompassing road vehicles, aviation, marine, and rail systems. Technical fluids such as lubricants, coolants, and fuel additives are critical for ensuring optimal performance, safety, and compliance with emissions standards. The continued growth in global mobility, logistics, and public transit infrastructure further fuels fluid consumption in this segment, particularly in rapidly urbanizing regions.

Construction comes next, driven by the use of heavy machinery and equipment that rely on hydraulic systems, lubricants, and coolants. With expanding infrastructure projects in developing regions and ongoing urban development in mature markets, construction activities demand reliable technical fluids to maintain uptime and efficiency in harsh working environments.

The energy and utilities sector follows, including oil & gas, power generation, and renewable energy systems. These industries require specialized technical fluids for turbines, compressors, drilling rigs, transformers, and other critical equipment. While the demand is high in terms of value due to the need for high-performance and long-life fluids, the sector’s share remains moderate due to its relatively lower consumption volume compared to manufacturing or transportation.

Finally, the agriculture industry holds the smallest share among end-user industries. Tractors, harvesters, irrigation systems, and other machinery utilize lubricants, hydraulic fluids, and coolants, but the scale and frequency of use are limited compared to other sectors. Additionally, many agricultural applications are seasonal, leading to fluctuating demand patterns.

Segmentation Insights by Functionality

On the basis of functionality, the global technical fluid market is bifurcated into anti-wear, corrosion inhibitors, foam control, thermal stability, and viscosity index improvers.

In the technical fluid market, anti-wear additives represent the most dominant functionality segment. These components are essential in reducing friction and protecting metal surfaces from wear under high pressure and heavy load conditions, making them indispensable in automotive engines, industrial gearboxes, and hydraulic systems. Their widespread usage across multiple industries ensures a consistently high demand, positioning them at the forefront of the functionality-based segmentation.

Corrosion inhibitors follow closely behind, playing a vital role in protecting metal components from degradation due to moisture, oxygen, and other corrosive agents. They are particularly important in marine, oil & gas, and industrial applications where equipment is exposed to harsh environments. The increasing focus on equipment longevity and system reliability drives strong demand for fluids enhanced with corrosion protection.

Foam control agents come next in terms of market share. These additives are crucial for maintaining system performance by preventing foam formation, which can reduce the efficiency of hydraulic and lubrication systems. Although essential, foam control additives are typically used in smaller quantities and have a more specific application focus, which places them slightly lower in the hierarchy.

Thermal stability additives, while essential, occupy a moderate share of the market. These additives help fluids maintain their chemical properties under extreme temperatures, ensuring consistent performance in high-heat environments such as engines, turbines, and industrial furnaces. While highly valuable in performance-focused applications, their use is somewhat niche, which limits overall volume demand.

At the lower end of the spectrum are viscosity index improvers, which help technical fluids maintain stable viscosity across a broad temperature range. They are primarily used in lubricants and hydraulic fluids to ensure proper flow and film strength under varying conditions. Although they provide critical benefits, the volume used is relatively small, and their application scope is narrower than other functional additives, placing them as the least dominant segment by functionality.

Technical Fluid Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region is the most dominant in the global technical fluid market. This dominance is driven by rapid industrialization, large-scale infrastructure development, and the growing automotive and electronics sectors in countries such as China, India, and Japan. The widespread adoption of advanced manufacturing processes and an expanding base of hydraulic system applications across industries further fuel demand. Additionally, the presence of major production hubs and cost-efficient labor contribute to the region’s sustained leadership in the market.

North America holds a substantial share in the technical fluid market, largely due to its mature industrial infrastructure and the presence of technologically advanced automotive and aerospace sectors. Stringent environmental regulations promote the use of high-performance, environmentally friendly fluids. Continuous R&D investments and a strong presence of leading manufacturers ensure consistent innovation and demand, particularly in the United States and Canada.

Europe remains a key region with strong emphasis on sustainability and efficient production systems. The region’s advanced automotive industry, particularly in Germany, France, and the UK, supports high demand for specialty fluids. Strict regulatory compliance and a shift toward energy-efficient technologies further strengthen the use of technical fluids in various sectors such as manufacturing, power generation, and transportation.

Middle East and Africa show growing potential, primarily supported by extensive oil and gas exploration and production activities. Countries such as Saudi Arabia, the UAE, and South Africa are investing in large-scale industrial projects that require specialized fluids for lubrication, drilling, and hydraulic systems. While the region lags behind in manufacturing diversification, its reliance on energy and petrochemical sectors continues to drive steady demand.

Latin America represents the smallest market share among the regions but still offers emerging opportunities, especially in Brazil and Mexico. Growth is supported by expanding industrial activities and adoption of hydraulic and cooling systems in manufacturing and energy sectors. However, the market faces challenges such as political and economic instability, as well as inadequate infrastructure, which can slow broader adoption and investment.

Technical Fluid Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the technical fluid market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global technical fluid market include:

- Arkema Group

- VOLTRONIC GmbH

- NISOTEC

- BIZOL Germany GmbH

- Nefteproduct JSC

- CIMCOOL Industrial Products

- Exxon Mobil Corporation

- Multitherm

- Dynalene

The global technical fluid market is segmented as follows:

By Type of Fluid

- Hydraulic Fluids

- Lubricants

- Coolants

- Heat Transfer Fluids

- Fuel Additives

By Application

- Automotive

- Aerospace

- Industrial Machinery

- Marine

- Oil and Gas

By Base Oil Type

- Mineral Oil

- Synthetic Oil

- Bio-based Oil

- Water-based Fluids

By End-user Industry

- Manufacturing

- Construction

- Energy and Utilities

- Transportation

- Agriculture

By Functionality

- Anti-wear

- Corrosion Inhibitors

- Foam Control

- Thermal Stability

- Viscosity Index Improvers

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Technical Fluid

Request Sample

Technical Fluid