U.S. Pet Food Market Size, Share, and Trends Analysis Report

CAGR :

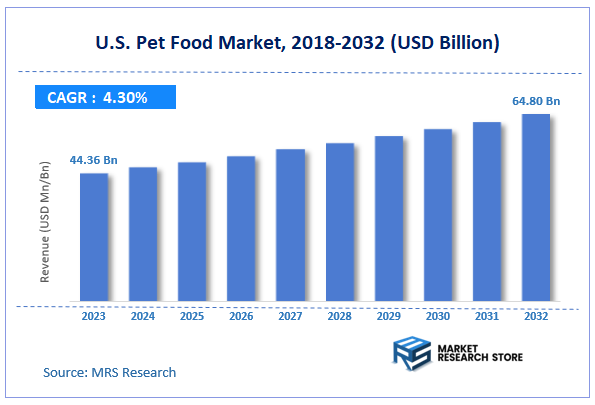

| Market Size 2023 (Base Year) | USD 44.36 Billion |

| Market Size 2032 (Forecast Year) | USD 64.80 Billion |

| CAGR | 4.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

U.S. Pet Food Market Insights

According to Market Research Store, the U.S. Pet Food market size was valued at around USD 44.36 billion in 2023 and is estimated to reach USD 64.80 billion by 2032, to register a CAGR of approximately 4.3% in terms of revenue during the forecast period 2024-2032.

The U.S. Pet Food report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

U.S. Pet Food Market: Overview

U.S. Pet Food refers to commercially manufactured food products formulated to meet the nutritional needs of domesticated animals such as dogs, cats, birds, and small mammals. These products come in various forms including dry kibble, wet or canned food, semi-moist meals, freeze-dried treats, and fresh or raw formulations. U.S. Pet Food is governed by regulations from the Food and Drug Administration (FDA) and the Association of American Feed Control Officials (AAFCO), which establish labeling guidelines, nutritional standards, and safety protocols to ensure product quality and pet health.

The growth of the U.S. Pet Food market is driven by the increasing humanization of pets, rising pet ownership rates, and a heightened focus on animal health and wellness. Consumers are seeking premium, natural, and functional pet food options that mirror human dietary trends, such as grain-free, organic, high-protein, and limited-ingredient diets. The demand for customized nutrition, breed-specific formulations, and life-stage-targeted meals is also contributing to product innovation.

Key Highlights

- The U.S. Pet Food market is anticipated to grow at a CAGR of 4.3% during the forecast period.

- The U.S. Pet Food market was estimated to be worth approximately USD 44.36 billion in 2023 and is projected to reach a value of USD 64.80 billion by 2032.

- The growth of the U.S. Pet Food market is being driven by a powerful combination of evolving consumer attitudes, a heightened focus on pet well-being, and the expanding accessibility of products.

- Based on the product, the wet pet food segment is growing at a high rate and is projected to dominate the market.

- On the basis of pet type, the cats segment is projected to swipe the largest market share.

- In terms of category, the traditional pet food segment is expected to dominate the market.

- Based on the distribution channel, the supermarkets & hypermarkets segment is expected to dominate the market.

U.S. Pet Food Market: Dynamics

Key Growth Drivers:

- Pet Humanization Trend: This is the most significant driver. Pet owners increasingly view their pets as integral family members, leading to a willingness to spend more on premium, nutritious, and often "human-grade" food products that mirror their own dietary preferences. This drives demand for high-quality ingredients, specialized formulations, and gourmet options.

- Growing Pet Ownership: The number of households owning pets in the US continues to rise. This expanding pet population, particularly among millennials and Gen Z, directly translates to a larger consumer base for pet food products.

- Increased Focus on Pet Health and Wellness: Pet owners are becoming highly conscious of their pets' nutritional needs and overall well-being. This fuels demand for functional foods offering specific health benefits (e.g., joint support, weight management, gut health, allergy relief), as well as veterinary-prescribed or therapeutic diets for chronic conditions.

Restraints:

- Rising Cost of Pet Food (Inflation): The increasing cost of ingredients, manufacturing, and supply chain logistics has led to higher pet food prices. This can impact consumer purchasing behavior, especially among budget-conscious owners, potentially leading to a shift towards cheaper alternatives or homemade diets.

- Concerns about Product Safety and Recalls: Despite stringent regulations, past instances of pet food recalls due to contamination or ingredient issues can erode consumer trust and negatively impact sales of affected brands or even the broader market perception of processed pet food.

- Competition from Homemade Diets: Growing awareness and distrust of commercial pet food ingredients have led some pet owners to opt for preparing homemade meals for their pets. While offering perceived control, this can reduce the market for commercially produced foods.

Opportunities:

- Expansion of Fresh, Frozen, and Human-Grade Options: The market for fresh, frozen, and human-grade pet food is experiencing rapid growth. This segment represents a significant opportunity for innovation, new product development, and premium pricing.

- Personalization and Customization: Offering tailored pet food solutions based on factors like breed, age, activity level, specific health conditions, and even DNA analysis presents a lucrative opportunity. Subscription models for customized meals are gaining traction.

- Sustainable and Ethical Sourcing: A strong opportunity exists for brands that emphasize transparency, ethical sourcing of ingredients (e.g., pasture-raised meats, sustainably harvested fish), and eco-friendly packaging, appealing to environmentally conscious consumers.

Challenges:

- Maintaining Quality and Safety at Scale: As production of innovative formats (e.g., fresh, frozen) scales up, ensuring consistent quality, food safety, and extended shelf life while adhering to stringent regulations becomes a significant operational challenge.

- Educating Consumers on Nutritional Science: With the proliferation of different diets and marketing claims, educating pet owners about scientifically sound nutritional principles and debunking misinformation (e.g., myths around grain-free diets) is a continuous challenge.

- Volatile Raw Material Prices and Supply Chain Stability: Managing the fluctuating costs of ingredients and ensuring a stable, reliable supply chain in the face of economic and environmental uncertainties remains a persistent challenge for manufacturers.

U.S. Pet Food Market: Report Scope

This report thoroughly analyzes the U.S. Pet Food Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | U.S. Pet Food Market |

| Market Size in 2023 | USD 44.36 Billion |

| Market Forecast in 2032 | USD 64.80 Billion |

| Growth Rate | CAGR of 4.3% |

| Number of Pages | 140 |

| Key Companies Covered | The J.M. Smucker Company, Nestlé Purina, Mars Petcare Inc., The J.M. Smucker Company, Hill’s Pet Nutrition, Inc., General Mills Inc., Wellness Pet Company, The Hartz Mountain Corporation, Diamond Pet Foods, P&G PetCare, Big Heart Pet Brands, Midwestern Pet Foods, Heristo AG, and others. |

| Segments Covered | By Product, By Pet Type, By Distribution Channel, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

U.S. Pet Food Market: Segmentation Insights

The U.S. Pet Food market is divided by product, pet type, category, distribution channel, and region.

Based on product, the U.S. Pet Food market is divided into wet pet food, dry pet food, and snacks/treats. Dry pet food dominates the U.S. pet food market due to its convenience, long shelf life, and cost-effectiveness. Pet owners widely prefer dry food for both dogs and cats because it is easy to store, measure, and serve. It also promotes dental health by reducing plaque buildup through chewing. The segment benefits from continuous innovation in terms of fortified blends with added vitamins, proteins, and functional ingredients like probiotics or omega fatty acids. Major brands are investing heavily in grain-free, high-protein, and breed-specific formulations, further driving consumer adoption. Its affordability and availability across all retail formats—from grocery stores to pet specialty shops—secure its lead in the market.

On the basis of pet type, the U.S. Pet Food market is bifurcated into cats, dogs, and others. Cats dominate the U.S. pet food market segment in this analysis due to increasing cat ownership in urban households, particularly among single professionals and apartment dwellers. Cats require less space and care compared to dogs, making them ideal companions in cities. This has driven demand for a wide range of specialized cat food options, including wet foods, high-protein dry foods, and functional treats designed for urinary health, hairball control, and indoor nutrition. Manufacturers are capitalizing on this trend by launching gourmet, organic, and grain-free cat food products in both dry and wet formats.

By Category, the U.S. pet food market is bifurcated into traditional pet food and specialist veterinary nutrition. Traditional pet food dominates the U.S. Pet Food market in this segmentation due to its widespread accessibility, cost-effectiveness, and alignment with the general dietary needs of the average pet. This category includes both wet and dry food formats designed for routine feeding without the need for veterinary prescriptions. Traditional pet food products are available across various retail channels such as supermarkets, pet stores, online platforms, and convenience stores, making them highly accessible to a broad consumer base. Major manufacturers focus on flavor variety, shelf life, brand loyalty, and attractive packaging, which collectively enhance market appeal.

In terms of distribution channel, the U.S. pet food market is bifurcated into supermarkets & hypermarkets, convenience stores, e-commerce, pet specialty stores, and others. Supermarkets & hypermarkets dominate the distribution landscape of the U.S. Pet Food market, owing to their broad consumer reach, convenience, and competitive pricing. These large retail outlets serve as a one-stop destination for consumers purchasing both household essentials and pet care products, offering a diverse range of pet food brands across various price points. Their extensive shelf space allows for the display of multiple product formats, including dry food, wet food, and treats, thereby catering to different pet dietary needs. Promotional offers, loyalty programs, and seasonal discounts frequently drive bulk purchases, while private-label brands further expand affordability. The dominance of this segment is also supported by the strong presence of national chains such as Walmart, Target, and Kroger, whose expansive distribution networks ensure consistent product availability across both urban and suburban markets.

U.S. Pet Food Market: Regional Insights

Regionally, the United States stands as the dominant force within the pet food industry, contributing the largest share of overall market revenues. Among all pet categories, cat food leads in popularity, while dog food, treats, and niche segments such as freeze-dried or raw food are gaining momentum. Online retail channels are expanding rapidly, supported by subscription models and convenience-driven consumer preferences, though brick-and-mortar pet specialty stores and supermarkets still account for a significant portion of sales.

The market is also influenced by a high rate of pet ownership and increasing adoption of companion animals, particularly in urban and suburban households. Regional leaders include states with large pet populations such as California, Texas, and Florida, where spending on pet nutrition tends to be higher due to a combination of disposable income, lifestyle trends, and access to premium retail channels. Overall, the U.S. pet food market continues to grow at a moderate pace, with strong consumer demand fueling both innovation and competition across the country.

U.S. Pet Food Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the U.S. Pet Food market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the U.S. Pet Food market include:

- The J.M. Smucker Company

- Nestlé Purina

- Mars Petcare Inc.

- The J.M. Smucker Company

- Hill’s Pet Nutrition, Inc.

- General Mills Inc.

- Wellness Pet Company

- The Hartz Mountain Corporation

- Diamond Pet Foods

- P&G PetCare

- Big Heart Pet Brands

- Midwestern Pet Foods

- Heristo AG

The U.S. Pet Food market is segmented as follows:

By Product

- Wet Pet Food

- Dry Pet Food

- Snacks/Treats

By Pet Type

- Cats

- Dogs

- Others

By Category

- Traditional Pet Food

- Specialist Veterinary Nutrition

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- E-commerce

- Pet Specialty Stores

- Others

By Region

- U.S.

Frequently Asked Questions

Table Of Content

Inquiry For Buying

U.S. Pet Food

Request Sample

U.S. Pet Food