Virtual Desktop Managers Market Size, Share, and Trends Analysis Report

CAGR :

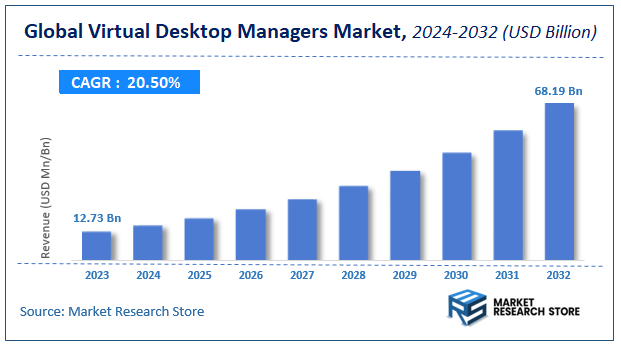

| Market Size 2023 (Base Year) | USD 12.73 Billion |

| Market Size 2032 (Forecast Year) | USD 68.19 Billion |

| CAGR | 20.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Virtual Desktop Managers Market Insights

According to Market Research Store, the global virtual desktop managers market size was valued at around USD 12.73 billion in 2023 and is estimated to reach USD 68.19 billion by 2032, to register a CAGR of approximately 20.5% in terms of revenue during the forecast period 2024-2032.

The virtual desktop managers report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Virtual Desktop Managers Market: Overview

Virtual desktop managers (VDMs) are software solutions designed to manage and control virtual desktop infrastructure (VDI). They allow users to access and manage their desktop environments remotely, providing centralized control, flexibility, and scalability. VDMs can handle the deployment, management, and optimization of virtual desktops on various devices, enhancing user productivity while ensuring security and efficiency. These tools often integrate with cloud computing platforms, supporting features such as desktop provisioning, session management, and load balancing. They enable organizations to streamline IT operations by consolidating resources and simplifying desktop management in a virtualized environment.

Key Highlights

- The virtual desktop managers market is anticipated to grow at a CAGR of 20.5% during the forecast period.

- The global virtual desktop managers market was estimated to be worth approximately USD 12.73 billion in 2023 and is projected to reach a value of USD 68.19 billion by 2032.

- The growth of the virtual desktop managers market is being driven by increasing demand for remote work solutions, scalability, and security in enterprise IT infrastructure.

- Based on the deployment type, the cloud-based segment is growing at a high rate and is projected to dominate the market.

- On the basis of user type, the corporate users segment is projected to swipe the largest market share.

- In terms of functionality features, the security features segment is expected to dominate the market.

- Based on the industry vertical, the IT & Telecommunications segment is expected to dominate the market.

- In terms of end-user, the large enterprises segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Virtual Desktop Managers Market: Dynamics

Key Growth Drivers:

- Growing Demand for Remote Work Solutions: The shift towards remote and hybrid work models has driven the demand for virtual desktop managers, enabling employees to access their work environments securely from anywhere.

- Increased Adoption of Cloud Computing: As organizations migrate to cloud environments, virtual desktop infrastructure (VDI) solutions are becoming essential to manage desktops efficiently and securely across distributed systems.

- Cost Efficiency in IT Infrastructure Management: Virtual desktop managers allow companies to reduce costs related to hardware and software management, as they centralize the management and maintenance of desktop systems.

- Security Concerns and Data Protection Needs: With rising cybersecurity threats, businesses are turning to virtual desktop solutions to ensure secure access, centralized control over data, and enhanced protection against potential breaches.

- Ease of IT Support and Maintenance: Virtual desktop managers simplify the management of large IT environments by allowing centralized administration, making it easier to update and maintain operating systems and software for all users.

Restraints:

- High Initial Setup Costs: The implementation of virtual desktop infrastructure can be costly due to the need for specialized hardware, software, and setup services, which may deter smaller organizations from adopting the technology.

- Performance and Latency Issues: Virtual desktops can sometimes experience performance issues, including slow speeds and latency, especially when running resource-heavy applications, which can affect user experience.

- Complex Integration with Existing IT Systems: Integrating virtual desktop managers with legacy systems or existing IT infrastructure can be complex, requiring significant time, resources, and expertise.

- Dependence on Network Connectivity: The effectiveness of virtual desktop managers is highly reliant on network performance. Poor internet connections can lead to interruptions in service or compromised user experience.

Opportunities:

- Growth in SMEs Adoption: As cloud solutions become more affordable and accessible, small and medium-sized enterprises (SMEs) are increasingly adopting virtual desktop solutions to enhance productivity and reduce IT overheads.

- Integration of AI and Automation: The integration of artificial intelligence (AI) and automation in virtual desktop management can optimize performance, enhance security, and reduce manual intervention, presenting significant opportunities for innovation.

- Virtualization in Education and Healthcare: Sectors like education and healthcare are increasingly relying on virtual desktop environments to manage secure access to applications, improve collaboration, and ensure data security, driving further market growth.

- Emerging Markets Adoption: As internet infrastructure improves in emerging markets, there is an opportunity for virtual desktop managers to expand in regions where businesses are looking to modernize their IT infrastructure.

Challenges:

- Scalability Issues: While virtual desktop solutions are beneficial for smaller environments, scaling them for larger organizations with diverse needs can be complex and costly.

- Data Compliance and Legal Concerns: Ensuring data protection and compliance with local regulations (such as GDPR, HIPAA, etc.) across various jurisdictions can be challenging, particularly when managing virtual desktops that span multiple regions.

- User Resistance to Change: Employees and organizations that are used to traditional desktop systems may resist the transition to virtual environments due to concerns about usability, training requirements, or fear of technology disruption.

- Lack of Skilled Workforce: The adoption of virtual desktop managers requires skilled IT professionals for implementation, troubleshooting, and ongoing support, and there is a shortage of qualified talent in some regions.

Virtual Desktop Managers Market: Report Scope

This report thoroughly analyzes the Virtual Desktop Managers Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Virtual Desktop Managers Market |

| Market Size in 2023 | USD 12.73 Billion |

| Market Forecast in 2032 | USD 68.19 Billion |

| Growth Rate | CAGR of 20.5% |

| Number of Pages | 168 |

| Key Companies Covered | Dexpot, MDesktop, NSpaces, OS Templates, Virtual Dimension, Z-Systems |

| Segments Covered | By Deployment Type, By User Type, By Functionality Features, By Industry Vertical, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Virtual Desktop Managers Market: Segmentation Insights

The global virtual desktop managers market is divided by deployment type, user type, functionality features, industry vertical, end-user, and region.

Segmentation Insights by Deployment Type

Based on deployment type, the global virtual desktop managers market is divided into on-premise, cloud-based, and hybrid deployment.

Cloud-Based Deployment stands as the most dominant segment, primarily due to its cost-efficiency, scalability, and flexibility. With the increasing adoption of cloud technologies across industries, businesses prefer cloud-based virtual desktop infrastructure (VDI) as it eliminates the need for heavy infrastructure investments and offers real-time access to desktops from anywhere. This deployment type allows businesses to scale up or down based on needs, reducing operational costs and ensuring that businesses can maintain a competitive edge with a more agile IT infrastructure.

Following cloud-based deployment, Hybrid Deployment comes next in dominance. Hybrid solutions combine both on-premise and cloud infrastructures, allowing organizations to enjoy the benefits of both worlds. For instance, sensitive data and mission-critical applications can be managed on-premise for security reasons, while other less-sensitive workloads are managed in the cloud. This flexible approach appeals to businesses that want to retain control over certain aspects of their operations while embracing the cost-effective, scalable benefits of cloud technologies. The growing need for enhanced flexibility and security is driving the popularity of hybrid deployments in organizations with complex IT requirements.

On-Premise Deployment is the least dominant segment. Although this traditional model offers complete control over the hardware and data, it is increasingly seen as less efficient and cost-effective compared to cloud-based or hybrid options. On-premise solutions require significant upfront investments in infrastructure, maintenance, and IT support. Moreover, the ongoing expenses related to system upgrades, security, and capacity planning often make it a less attractive choice for businesses looking to optimize costs and operational efficiency in the digital age. Despite these drawbacks, certain industries with stringent regulatory requirements or those requiring complete data control still prefer on-premise deployment.

Segmentation Insights by User Type

On the basis of user type, the global virtual desktop managers market is bifurcated into individual users, IT administrators, service providers, managed service providers (MSPs), and corporate users.

Corporate Users represent the most dominant segment. The growing trend of digital transformation within large and mid-sized organizations has led to a substantial increase in the adoption of virtual desktop infrastructure (VDI) solutions for enhancing productivity and streamlining IT management. Corporate users require scalable, secure, and flexible VDI solutions to accommodate a growing remote workforce, improve operational efficiency, and ensure smooth access to business applications across multiple devices. The need for centralized management, cost reduction, and remote work capabilities drives their preference for VDM solutions.

Next in dominance are Managed Service Providers (MSPs). MSPs manage IT services and infrastructure for multiple clients, often including virtual desktop environments. Given the growing demand for cloud-based services and remote work solutions, MSPs play a significant role in deploying, managing, and supporting virtual desktop solutions for small to medium-sized businesses (SMBs) and enterprises. They benefit from providing tailored VDI solutions that can be managed remotely, offering flexibility and scalability to clients while ensuring system reliability and security.

IT Administrators come next in the ranking of user types. As the key individuals responsible for managing and maintaining the organization's IT infrastructure, IT administrators are highly involved in the deployment and operation of virtual desktop managers. While they might not be the end-users, their role in selecting, configuring, and managing VDI solutions makes them a crucial part of the market. IT administrators in large enterprises and SMBs alike seek VDI solutions that provide centralized control, efficient resource management, and simplified maintenance, ensuring seamless delivery of desktops to end-users.

Service Providers rank below MSPs, as they often offer more specialized services that are narrower in scope than those provided by MSPs. These service providers may handle specific aspects of virtual desktop management, such as security, cloud storage, or network support. While they contribute to the VDM ecosystem, they serve a more specific niche compared to MSPs, making them less dominant in comparison.

Lastly, Individual Users are the least dominant segment in the VDM market. While individual consumers may adopt virtual desktop solutions for personal use or small-scale needs, the market is primarily driven by enterprise adoption. Individual users tend to use VDI for basic needs like accessing remote work environments or running resource-intensive applications on less capable devices. However, the demand from individual users remains comparatively lower, as the larger, more complex deployments of VDI are typically driven by businesses and organizations with more extensive requirements.

Segmentation Insights by Functionality Features

Based on functionality features, the global virtual desktop managers market is divided into application delivery, storage management, user management, network management, security features, and collaboration tools.

Security Features are the most dominant segment. With increasing cyber threats and the widespread adoption of remote work, organizations prioritize data protection, encryption, and secure access controls to safeguard sensitive information. VDI solutions that provide robust security features, such as multi-factor authentication, data encryption, secure tunneling, and endpoint protection, are highly sought after by businesses. Ensuring secure access to desktops and applications across various devices is a top concern, driving the demand for VDI solutions with strong security capabilities.

Following security features, Application Delivery ranks as the next most important functionality. The ability to deliver applications seamlessly to end-users, regardless of their device or location, is a critical component of any VDI solution. Application delivery enables businesses to run resource-intensive applications on remote servers while providing users with a responsive and native experience on their devices. The growing need for remote work solutions and cloud-based applications boosts the adoption of VDI solutions with strong application delivery features, making it a central feature in many enterprise deployments.

User Management comes next in the ranking of functionality features. As organizations grow and employee mobility increases, managing user access, profiles, and preferences becomes more complex. VDI solutions that offer comprehensive user management functionalities, such as centralized user provisioning, access control, and role-based authentication, are in high demand. Efficient user management helps streamline IT operations, reduce security risks, and ensure that users have a seamless experience when accessing their virtual desktops, making it an essential feature for most organizations.

Network Management follows as another significant feature, especially in environments where VDI solutions rely on high-performance networks for optimal user experience. Network management ensures that the virtual desktop environment runs smoothly across different network conditions by optimizing bandwidth, minimizing latency, and prioritizing traffic for VDI workloads. In large-scale deployments, where many users access virtual desktops concurrently, robust network management is crucial to ensure performance, reliability, and user satisfaction.

Storage Management ranks next in importance. Virtual desktops often require substantial storage resources to store user profiles, operating system images, applications, and data. Effective storage management helps optimize storage usage, ensure quick access to files, and prevent performance bottlenecks. This feature is particularly important in environments with large-scale VDI deployments, where managing the storage of multiple virtual desktops and applications across different users is crucial for maintaining performance and reducing operational costs.

Finally, Collaboration Tools are the least dominant feature in this market. While collaboration tools such as messaging, video conferencing, and shared workspaces are important, they are often secondary features in virtual desktop environments. However, with the growing trend of remote work and team collaboration, integration of collaboration tools within VDI solutions is gaining importance. Businesses are looking for seamless integration between virtual desktops and collaboration platforms like Microsoft Teams, Slack, or Zoom, which enhances productivity and fosters communication in virtual environments. Despite being less dominant than other features, collaboration tools are becoming increasingly relevant in modern VDI deployments, especially in remote-first organizations.

Segmentation Insights by Industry Vertical

On the basis of industry vertical, the global virtual desktop managers market is bifurcated into IT & telecommunications, banking, financial services, & insurance (BFSI), retail, healthcare, manufacturing, energy & utilities, and education.

IT & Telecommunications sector is the most dominant. This industry is at the forefront of digital transformation and relies heavily on flexible, secure, and scalable IT infrastructures. Virtual desktop solutions are ideal for IT and telecom companies as they enable centralized management of desktops, facilitate remote work, ensure data security, and streamline software updates across global teams. The constant need for rapid provisioning, infrastructure optimization, and high availability makes this sector a major adopter of VDM technologies.

Following IT & Telecommunications, the BFSI (Banking, Financial Services, and Insurance) sector is another major contributor to VDM adoption. Security and regulatory compliance are critical in this industry, and VDM provides the necessary centralized control, data protection, and secure access mechanisms to meet those needs. With the increasing push toward digitization and remote banking services, VDI solutions help financial institutions maintain operational continuity, support customer service operations remotely, and protect sensitive customer data across devices and geographies.

Healthcare is the next significant vertical, benefiting from VDM's ability to provide secure, real-time access to patient data and medical applications. With the growing use of electronic health records (EHRs), telemedicine, and remote diagnostics, virtual desktops ensure that healthcare professionals can access critical systems securely and efficiently, regardless of location. The need for HIPAA compliance and data security further drives the sector’s reliance on VDI solutions.

Education follows, driven by the rapid digitalization of learning environments and the rise in remote and hybrid learning models. Virtual desktops provide students and educators with access to learning resources and applications on any device, simplifying IT management for schools and universities. Centralized updates and support reduce administrative overhead and enhance the consistency of the learning experience across various platforms.

Retail is gaining traction in the VDM market, particularly as retail chains expand digital operations and remote customer service capabilities. VDI enables centralized control over POS systems, inventory applications, and employee portals across distributed retail locations. It helps ensure uniformity in user experience while reducing IT overhead. However, adoption is more pronounced among larger retail chains than smaller stores due to cost and scale considerations.

Manufacturing comes next, where VDM is used to manage design, production, and operational systems from centralized locations. It supports remote monitoring, CAD application access, and secure collaboration across departments and suppliers. However, adoption is slower compared to other verticals due to concerns over latency, network dependencies, and integration with legacy systems on factory floors.

Lastly, Energy & Utilities represents the least dominant segment. While there is growing interest in centralized management and secure access to control systems and enterprise applications, adoption remains limited. This is mainly due to the critical nature of energy infrastructure, reliance on legacy systems, and the conservative pace of digital transformation in this sector. However, as energy providers embrace smart grid technologies and distributed workforces, the potential for VDM growth in this vertical is expected to increase over time.

Segmentation Insights by End-User

On the basis of end-user, the global virtual desktop managers market is bifurcated into small & medium enterprises (SMEs), large enterprises, government & public sector, education institutions, and healthcare organizations.

Large Enterprises are the most dominant end-user segment. These organizations typically have complex IT infrastructures and a large, distributed workforce, making virtual desktop solutions highly attractive for centralized management, scalability, and enhanced data security. Large enterprises prioritize efficient resource utilization, secure remote access, and compliance, all of which are addressed effectively by VDM platforms. Their greater financial resources also enable them to adopt and integrate advanced VDI solutions across multiple departments and locations.

Next in line are Healthcare Organizations, which heavily rely on virtual desktop infrastructure to ensure secure, real-time access to patient records, imaging systems, and clinical applications. With strict data protection regulations such as HIPAA, healthcare providers prefer VDM solutions for their strong security features and centralized access control. VDI also supports remote consultations and mobile healthcare delivery, which have become increasingly important in modern medical services.

Government & Public Sector entities follow closely, especially as they seek to modernize infrastructure while ensuring national security and regulatory compliance. Virtual desktop solutions enable public agencies to provide employees and contractors with secure access to internal systems while maintaining centralized control and monitoring. The ability to rapidly deploy secure desktops to a geographically dispersed workforce, particularly during emergencies or crisis situations, makes VDM an appealing solution for this sector.

Educational Institutions are next in dominance. Schools, colleges, and universities use VDM to deliver consistent desktop experiences to students and staff across devices and campuses. It simplifies IT management, reduces hardware dependency, and supports hybrid and remote learning environments. Virtual desktops also allow institutions to centrally manage software licenses and updates, which is especially beneficial in budget-constrained education settings.

Finally, Small & Medium Enterprises (SMEs) represent the least dominant end-user segment. While SMEs are increasingly recognizing the benefits of VDM—such as cost savings, flexibility, and improved security—their adoption is relatively slower due to budget constraints and limited IT resources. However, with the growing availability of cloud-based and subscription-based VDI models, SMEs are gradually entering the market, particularly those in tech-driven or compliance-sensitive industries looking for affordable, scalable solutions.

Virtual Desktop Managers Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the virtual desktop infrastructure (VDI) market, with its early adoption of VDI technologies and a well-established IT infrastructure. The United States, in particular, stands out due to the high demand across various industries, including healthcare, banking, and government sectors. The presence of major technology providers like VMware, Microsoft, and Citrix further strengthens the region’s leadership in the market.

Europe holds a strong second position, driven by mature IT markets and stringent data protection laws such as GDPR. Countries like Germany, the United Kingdom, and France are key adopters of VDI solutions, particularly in industries that require high levels of security and compliance, such as finance, healthcare, and public services. The regulatory environment has played a significant role in the rapid adoption of virtual desktop technologies in the region.

Asia Pacific (APAC) is experiencing significant growth, supported by digital transformation initiatives and a growing shift toward cloud computing. Countries such as China, India, Japan, and South Korea are key players, with a rising demand for VDI solutions among small and medium-sized enterprises (SMEs). The growing trend of Bring Your Own Device (BYOD) and the shift to remote work are driving market expansion in this region.

Latin America is gradually gaining momentum in the VDI market, with Brazil and Mexico leading the way. While the market is still developing, there is growing interest in VDI solutions as businesses seek to modernize their IT infrastructure and support remote work models. Large enterprises are the main adopters, but there is a noticeable rise in SMEs exploring cost-effective VDI options.

Middle East and Africa (MEA) are emerging markets for VDI, with steady adoption fueled by the region’s focus on digital transformation and IT security. Countries like the United Arab Emirates and Saudi Arabia are leading the charge, with both large enterprises and SMEs increasingly embracing VDI solutions to support remote work and business continuity. The region’s emphasis on cybersecurity and IT infrastructure development is contributing to the growing adoption of VDI technologies.

Virtual Desktop Managers Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the virtual desktop managers market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global virtual desktop managers market include:

- Dexpot

- MDesktop

- NSpaces

- OS Templates

- Virtual Dimension

- Z-Systems

The global virtual desktop managers market is segmented as follows:

By Deployment Type

- On-Premise

- Cloud-Based

- Hybrid Deployment

By User Type

- Individual Users

- IT Administrators

- Service Providers

- Managed Service Providers (MSPs)

- Corporate Users

By Functionality Features

- Application Delivery

- Storage Management

- User Management

- Network Management

- Security Features

- Collaboration Tools

By Industry Vertical

- IT and Telecommunications

- Banking

- Financial Services

- and Insurance (BFSI)

- Retail

- Healthcare

- Manufacturing

- Energy and Utilities

- Education

By End-User

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- Government and Public Sector

- Education Institutions

- Healthcare Organizations

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Virtual Desktop Managers

Request Sample

Virtual Desktop Managers