Wafer Carrier Market Size, Share, and Trends Analysis Report

CAGR :

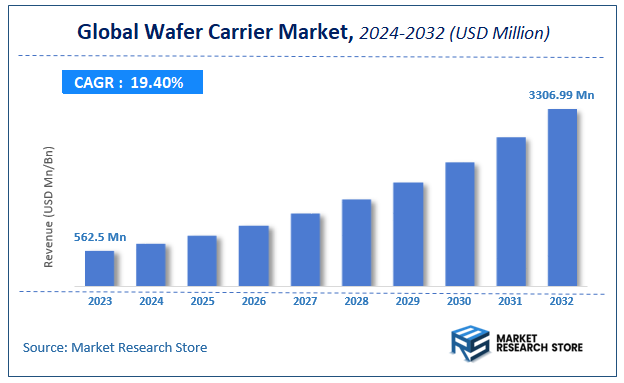

| Market Size 2023 (Base Year) | USD 562.5 Million |

| Market Size 2032 (Forecast Year) | USD 3306.99 Million |

| CAGR | 19.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Wafer Carrier Market Insights

According to Market Research Store, the global wafer carrier market size was valued at around USD 562.5 million in 2023 and is estimated to reach USD 3306.99 million by 2032, to register a CAGR of approximately 19.4% in terms of revenue during the forecast period 2024-2032.

The wafer carrier report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Wafer Carrier Market: Overview

A wafer carrier is a specialized tool used in semiconductor manufacturing to hold and protect semiconductor wafers during various processes such as handling, transport, or testing. These carriers are typically made of materials that ensure stability, prevent contamination, and maintain wafer orientation to avoid damage. They come in different forms, including flat or circular designs, and are designed to accommodate varying wafer sizes such as 5-inch, 6-inch, 8-inch, and even 12-inch wafers. Wafer carriers play a crucial role in preventing physical damage, contamination, and static electricity buildup, which could negatively impact the wafer's integrity and the overall production process.

Key Highlights

- The wafer carrier market is anticipated to grow at a CAGR of 19.4% during the forecast period.

- The global wafer carrier market was estimated to be worth approximately USD 562.5 million in 2023 and is projected to reach a value of USD 3306.99 million by 2032.

- The growth of the wafer carrier market is being driven by increasing demand for semiconductor devices in various industries, including consumer electronics, automotive, telecommunications, and more.

- Based on the material type, the plastic segment is growing at a high rate and is projected to dominate the market.

- On the basis of wafer size, the 300 mm wafers segment is projected to swipe the largest market share.

- In terms of application, the semiconductor manufacturing segment is expected to dominate the market.

- Based on the carrier design, the standard carriers segment is expected to dominate the market.

- In terms of end-user industry, the electrical and electronics segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Wafer Carrier Market: Dynamics

Key Growth Drivers:

- Increasing Demand for Semiconductors: As industries like consumer electronics, automotive, and telecommunications continue to expand, the demand for semiconductors rises, fueling the need for efficient wafer handling and storage solutions such as wafer carriers.

- Advancements in Semiconductor Manufacturing Processes: The ongoing advancements in semiconductor manufacturing technologies, such as the shift to smaller nodes and increased wafer sizes, drive the demand for high-quality wafer carriers capable of maintaining the integrity of delicate wafers during transport and storage.

- Growth of the Electronics and Automotive Industries: The continuous growth of electronics, particularly in mobile devices and electric vehicles (EVs), and the shift towards autonomous systems in automotive applications contribute significantly to the increasing need for wafer carriers in semiconductor production.

- Technological Advancements in Wafer Carrier Materials: The development of more advanced materials, such as ceramic and polymer-based carriers, is driving innovation in the wafer carrier market by enhancing wafer protection, reducing contamination risks, and improving overall reliability.

- Increasing Focus on Automation in Manufacturing: The automation of semiconductor manufacturing processes requires highly efficient and reliable wafer carriers to facilitate robotic handling and ensure the smooth operation of wafer production lines.

Restraints:

- High Production Costs: The manufacturing of wafer carriers, particularly those made of high-quality materials or advanced polymers, can be costly. This can increase the overall production cost for semiconductor manufacturers, making it a restraint for some companies, especially SMEs.

- Risk of Contamination: Wafer carriers are susceptible to contamination from external particles, chemicals, or physical damage, which could compromise wafer quality during transport and storage. This risk of contamination can create concerns for manufacturers and end-users.

- Complexity in Customization: Different semiconductor manufacturers may require wafer carriers with specific dimensions and properties, making the customization of carriers complex and time-consuming. The need for tailored solutions increases the complexity and cost of wafer carrier production.

- Supply Chain Disruptions: The wafer carrier market relies on specialized materials and technologies, and disruptions in the global supply chain—such as material shortages or logistical issues—can hinder the timely availability of wafer carriers.

Opportunities:

- Expansion in Emerging Markets: The growing adoption of advanced semiconductor technologies in emerging markets like China, India, and Southeast Asia presents a significant opportunity for wafer carrier manufacturers to expand their reach and capitalize on the increasing demand for semiconductor products.

- Development of Eco-Friendly Wafer Carriers: As sustainability becomes a key focus for many industries, the development of environmentally friendly wafer carriers made from recyclable materials presents a significant growth opportunity. Companies that prioritize sustainability could gain a competitive advantage.

- R&D in Smart Wafer Carriers: The integration of sensor technologies in wafer carriers could lead to the development of "smart" carriers that can monitor wafer conditions, track handling, and improve overall process efficiency, creating new opportunities for growth and innovation in the market.

- Increasing Demand for Advanced Packaging Technologies: As semiconductor packaging techniques evolve, especially in 3D and fan-out wafer-level packaging, the demand for advanced wafer carriers that can support these technologies is expected to grow, offering new market opportunities.

Challenges:

- Technological Complexity in Manufacturing: The production of wafer carriers requires precise engineering, especially when dealing with specialized materials and custom designs. The increasing technological complexity of semiconductor production systems poses challenges for manufacturers of wafer carriers.

- Intense Competition and Price Pressure: The wafer carrier market is highly competitive, with several players offering similar products. This intense competition can lead to price pressure, making it difficult for manufacturers to maintain profit margins.

- Material and Product Development Challenges: Developing new materials that balance cost, performance, and environmental sustainability can be challenging. Innovations in wafer carriers must strike a delicate balance between maintaining the integrity of the wafer and offering cost-effective solutions.

- Fluctuating Demand Based on Semiconductor Cycles: The wafer carrier market is closely tied to semiconductor production cycles, and fluctuations in demand for semiconductors can result in unpredictable demand for wafer carriers, making it challenging for manufacturers to forecast and plan production effectively.

Wafer Carrier Market: Report Scope

This report thoroughly analyzes the Wafer Carrier Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Wafer Carrier Market |

| Market Size in 2023 | USD 562.5 Million |

| Market Forecast in 2032 | USD 3306.99 Million |

| Growth Rate | CAGR of 19.4% |

| Number of Pages | 166 |

| Key Companies Covered | Entegris, Shin-Etsu Polymer, H-Square Corporation, Miraial, Palbam Class, E-SUN, 3S Korea, Gudeng Precision, Pozzetta, Chung King Enterprise, Dou Yee, YJ Stainless, DISCO, Long-Tech Precision Machinery |

| Segments Covered | By Material Type, By Wafer Size, By Application, By Carrier Design, By End-User Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Wafer Carrier Market: Segmentation Insights

The global wafer carrier market is divided by material type, wafer size, application, carrier design, end-user industry, and region.

Segmentation Insights by Material Type

Based on material type, the global wafer carrier market is divided into plastic, metal, ceramic, and composite materials.

In the wafer carrier market, plastic is the most dominant material type, primarily due to its cost-effectiveness, ease of manufacturing, and versatility. Plastic carriers, particularly those made from high-performance polymers, offer excellent mechanical properties and are widely used in the semiconductor industry for wafer handling. They provide the necessary protection for delicate wafers during transportation and storage, ensuring minimal risk of damage. The availability of different grades of plastics for specific requirements, such as anti-static or high-temperature resistance, further enhances their adoption.

Following plastic, metal is the second most dominant material type in the wafer carrier market. Metal carriers, often made of aluminum or stainless steel, offer high strength and durability, making them suitable for applications requiring a robust material to withstand harsh environments. While they are heavier than plastic carriers, metals are preferred in scenarios where additional stability and structural integrity are essential, such as for larger or more sensitive wafers. Their conductive properties can also be an advantage in specific applications where electrostatic discharge (ESD) control is critical.

Ceramic is the third most dominant material in the wafer carrier market. Ceramic carriers offer superior thermal stability, making them ideal for high-temperature processes in semiconductor manufacturing. They also exhibit excellent wear resistance, which is crucial when handling delicate wafers. However, ceramics are more expensive and fragile compared to plastic and metal carriers, limiting their usage to high-end applications where these specific properties are required.

Finally, composite materials are the least dominant in the wafer carrier market. Composite carriers combine materials like carbon fiber, glass fiber, and resins to create lightweight yet durable carriers. While they can offer enhanced performance in terms of strength-to-weight ratio and resistance to corrosion, their high cost and more complex manufacturing processes mean they are less commonly used. Composite materials are typically chosen for specialized applications where a balance of lightweight properties and strength is necessary, but they have not yet achieved the widespread adoption of plastics or metals.

Segmentation Insights by Wafer Size

On the basis of wafer size, the global wafer carrier market is bifurcated into 150 mm, 200 mm, 300 mm, and 450 mm.

In the wafer carrier market, 300 mm wafers are the most dominant segment. This size has become the industry standard for advanced semiconductor manufacturing due to its ability to accommodate a larger number of chips per wafer, improving production efficiency and reducing costs. As semiconductor devices become more complex, the demand for 300 mm wafers has grown significantly, especially in the production of integrated circuits (ICs) for high-performance applications like mobile devices, consumer electronics, and data centers. The increased adoption of 300 mm wafers is largely driven by advancements in manufacturing technologies, enabling better yield and higher throughput.

The second most dominant wafer size is 200 mm. While 200 mm wafers were once the standard, they are now primarily used for older technologies or in markets where smaller scale production is needed. Many semiconductor manufacturers continue to use 200 mm wafers for producing devices that do not require the scale or processing power of more advanced chips. Despite this, the demand for 200 mm wafers is expected to remain steady, particularly in niche applications such as analog ICs and power devices.

150 mm wafers are less common but still relevant, particularly for specialized or legacy semiconductor manufacturing processes. These wafers are typically used for older technologies or for applications where cost considerations are more important than processing power. As semiconductor manufacturers transition to larger wafer sizes for mainstream production, 150 mm wafers are becoming increasingly rare, but there is still some demand for them in certain markets and regions with less advanced manufacturing capabilities.

Finally, 450 mm wafers represent the smallest and least dominant segment in the wafer carrier market. Although there has been significant interest in 450 mm wafers due to their potential for even higher production efficiency and chip yield, the adoption of this wafer size has been slow. The technological challenges associated with manufacturing, handling, and processing larger wafers have delayed the widespread use of 450 mm wafers. However, ongoing research and development in wafer handling technologies and semiconductor equipment may eventually drive the adoption of 450 mm wafers in the future, especially as the demand for increasingly powerful and efficient semiconductor devices grows.

Segmentation Insights by Application

Based on application, the global wafer carrier market is divided into semi-conductor manufacturing, solar cell production, microelectronics, and LEDs & displays.

In the wafer carrier market, semiconductor manufacturing is the most dominant application. This sector accounts for the largest share of the market due to the critical role wafers play in the production of integrated circuits (ICs) and other semiconductor devices. Wafer carriers are essential for transporting and protecting delicate wafers throughout the semiconductor fabrication process, which includes various steps like photolithography, etching, and doping. As the demand for advanced semiconductors grows across industries such as consumer electronics, automotive, and telecommunications, the semiconductor manufacturing application remains the key driver of wafer carrier demand.

Solar cell production is the second most dominant application. As the demand for renewable energy increases, the use of wafers in photovoltaic (PV) solar cell production has also expanded. Wafers, typically made from silicon, serve as the foundation for solar cells, and wafer carriers are crucial for handling these wafers during the manufacturing process. While the wafer size and material used in solar cell production differ from semiconductor manufacturing, the fundamental role of wafer carriers in ensuring efficient production and preventing damage remains the same. Solar energy production is a growing market, especially in regions focusing on sustainable energy solutions, making this application highly significant.

Microelectronics comes in third place, closely related to semiconductor manufacturing but more specific to smaller-scale devices such as sensors, actuators, and other microelectromechanical systems (MEMS). These components are critical in a wide range of applications, from medical devices to automotive systems. Wafer carriers in microelectronics manufacturing are used to transport smaller wafers with more specialized properties, requiring precise handling during production. While the demand for microelectronics is growing, it remains a niche segment compared to broader semiconductor production.

LEDs and displays are the least dominant application segment in the wafer carrier market, although it is still significant. The production of light-emitting diodes (LEDs) and displays, particularly in consumer electronics like smartphones, televisions, and other display technologies, requires high-quality wafers for the fabrication of LED chips. Wafer carriers in this application help handle wafers during processes like epitaxial growth, photolithography, and packaging. While the LED and display market is growing due to the increasing demand for advanced display technologies (e.g., OLED, MicroLED), it still represents a smaller share of the wafer carrier market compared to semiconductor manufacturing and solar cell production.

Segmentation Insights by Carrier Design

On the basis of carrier design, the global wafer carrier market is bifurcated into standard carriers, custom carriers, pallet carriers, and stackable carriers.

In the wafer carrier market, standard carriers are the most dominant design type. These carriers are widely used due to their cost-effectiveness, versatility, and ease of manufacturing. Standard carriers are designed to hold wafers of specific sizes and are used in various applications, particularly in semiconductor manufacturing, where uniformity and efficiency are essential. Their broad applicability across different industries, including microelectronics, solar cell production, and LED manufacturing, makes them the go-to option for most wafer handling needs. Standard carriers typically come in predefined shapes and sizes, which suit a variety of production environments.

Custom carriers follow as the second most dominant design. Custom carriers are tailored to meet the specific needs of particular processes, wafer sizes, or sensitive handling requirements. These carriers are often used in high-precision manufacturing environments, such as in the semiconductor and microelectronics industries, where wafers may have unique shapes, sizes, or surface treatments that demand specialized handling. Custom carriers are also favored when handling wafers with high value or those that require advanced protection against contamination, static, or mechanical damage. While custom carriers are more expensive and take longer to produce than standard carriers, their specialized design ensures optimal performance and wafer protection.

Pallet carriers come next in the wafer carrier market. These carriers are typically used for transporting large quantities of wafers simultaneously, making them suitable for high-volume production environments. Pallet carriers are designed to handle multiple wafers stacked in a tray-like configuration and are commonly used in industries like solar cell production, where bulk handling is essential. While they are not as widely used as standard carriers, pallet carriers offer a practical solution for larger-scale manufacturing operations, enabling efficient and safe handling of wafers during transportation and storage.

Stackable carriers are the least dominant design in the wafer carrier market. Stackable carriers are designed to be vertically stacked, offering space-saving benefits and facilitating organized storage and transport of multiple wafers. These carriers are particularly useful in applications where space is limited, or where a high density of wafers needs to be stored or transported without compromising safety. While stackable carriers are beneficial for certain logistical needs, their adoption is limited compared to the more straightforward designs of standard and custom carriers. The primary challenge with stackable carriers lies in ensuring that the wafers remain properly aligned and protected when stacked, as any misalignment can cause damage during handling.

Segmentation Insights by End-User Industry

On the basis of end-user industry, the global wafer carrier market is bifurcated into electrical & electronics, automotive, telecommunication, and consumer goods.

In the wafer carrier market, the electrical and electronics industry is the most dominant end-user sector. This is primarily due to the widespread use of semiconductor wafers in the production of integrated circuits (ICs) and other electronic components. The electrical and electronics industry drives the majority of wafer carrier demand, as wafers are integral to the manufacturing of devices such as computers, smartphones, and consumer electronics. Semiconductor fabrication is a highly sensitive process, requiring precise handling and transport of wafers, which makes wafer carriers critical in ensuring the efficiency and safety of production processes. As the demand for electronic devices continues to grow globally, particularly with advancements in IoT and smart technologies, the electrical and electronics sector remains the key driver of the wafer carrier market.

The automotive industry ranks second in terms of wafer carrier demand. With the increasing integration of electronic systems in vehicles, especially with the rise of electric vehicles (EVs), autonomous driving technologies, and advanced driver-assistance systems (ADAS), the automotive sector is becoming a significant consumer of semiconductor components. Wafer carriers are used to handle wafers that are later processed into chips for automotive applications, including sensors, microcontrollers, and power management ICs. The automotive sector's growing reliance on high-tech semiconductor components for its next-generation vehicles contributes to the expanding demand for wafer carriers in this industry.

The telecommunication industry follows closely in third place. Wafer carriers are essential for the production of semiconductor components used in telecommunication devices and infrastructure, such as mobile phones, routers, and network equipment. As 5G technology and high-speed communication networks continue to expand globally, the demand for chips capable of supporting these advanced systems increases, which in turn drives the need for wafer carriers. Telecommunication companies rely on high-quality, reliable semiconductor components, and wafer carriers play a vital role in ensuring the integrity and quality of the wafers during the manufacturing process.

Finally, the consumer goods industry is the least dominant but still a notable end-user of wafer carriers. In this sector, wafers are primarily used for the production of semiconductor components found in consumer products like home appliances, entertainment systems, wearables, and gaming devices. While the consumer goods market does not generate as much demand for semiconductor components as the electrical and electronics, automotive, or telecommunication industries, it still represents an important sector for wafer carrier usage. The increasing adoption of smart home devices and connected products continues to support the demand for semiconductor-based components, contributing to wafer carrier requirements in this industry.

Wafer Carrier Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region is the most dominant in the wafer carrier market, driven by its leadership in semiconductor manufacturing. Countries such as China, Japan, South Korea, and Taiwan house major semiconductor companies like TSMC, Samsung, and SK Hynix, all of which heavily influence the demand for wafer carriers. The region’s advanced electronics industry, ongoing investments in semiconductor infrastructure, and favorable government policies further bolster its position. Additionally, the growth in renewable energy and electric vehicle sectors across Asia Pacific is expected to continue driving the need for wafer carriers in the coming years.

North America holds a significant share of the wafer carrier market, largely due to the presence of leading semiconductor manufacturers and research facilities in the United States. Companies such as Intel, AMD, and Texas Instruments rely on wafer carriers to support their sophisticated manufacturing processes. The U.S. government’s efforts, including the CHIPS Act, aim to increase domestic semiconductor production, further boosting demand for wafer carriers in the region.

Europe plays a crucial role in the wafer carrier market, with key contributors like Germany, France, and the United Kingdom. The region’s strong focus on technological innovation, research and development, and the growing adoption of renewable energy sources support the demand for wafer carriers. Germany’s emphasis on Industry 4.0 and the automotive sector’s adoption of advanced electronics are also key drivers of market growth, making Europe an important player in this sector.

Latin America is an emerging market for wafer carriers, with growing demand from countries like Brazil and Mexico. The region's expanding electronics manufacturing industry and investment in renewable energy projects contribute to the need for wafer handling solutions. Although Latin America's market share is smaller compared to other regions, the development of semiconductor production capabilities and the adoption of advanced technologies is expected to boost market growth in the coming years.

The Middle East and Africa (MEA) region shows steady growth in the wafer carrier market, largely driven by investments in renewable energy and electric vehicle infrastructure. Countries like Saudi Arabia and the United Arab Emirates are diversifying their economies and developing advanced manufacturing capabilities, including semiconductor production. These initiatives offer opportunities for wafer carrier manufacturers to expand their presence in the MEA region.

Wafer Carrier Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the wafer carrier market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global wafer carrier market include:

- Entegris

- Shin-Etsu Polymer

- H-Square Corporation

- Miraial

- Palbam Class

- E-SUN

- 3S Korea

- Gudeng Precision

- Pozzetta

- Chung King Enterprise

- Dou Yee

- YJ Stainless

- DISCO

- Long-Tech Precision Machinery

The global wafer carrier market is segmented as follows:

By Material Type

- Plastic

- Metal

- Ceramic

- Composite Materials

By Wafer Size

- 150 mm

- 200 mm

- 300 mm

- 450 mm

By Application

- Semi-conductor Manufacturing

- Solar Cell Production

- Microelectronics

- LEDs and Displays

By Carrier Design

- Standard Carriers

- Custom Carriers

- Pallet Carriers

- Stackable Carriers

By End-User Industry

- Electrical and Electronics

- Automotive

- Telecommunication

- Consumer Goods

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Wafer Carrier

Request Sample

Wafer Carrier