Wafer Cases Market Size, Share, and Trends Analysis Report

CAGR :

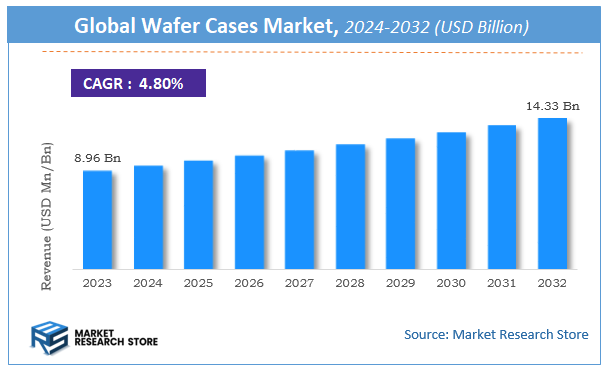

| Market Size 2023 (Base Year) | USD 8.96 Billion |

| Market Size 2032 (Forecast Year) | USD 14.33 Billion |

| CAGR | 4.8% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Wafer Cases Market Insights

According to Market Research Store, the global wafer cases market size was valued at around USD 8.96 billion in 2023 and is estimated to reach USD 14.33 billion by 2032, to register a CAGR of approximately 4.8% in terms of revenue during the forecast period 2024-2032.

The wafer cases report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Wafer Cases Market: Overview

Wafer cases are specialized containers designed to protect semiconductor wafers during transportation, storage, and handling. These cases are essential in preventing contamination, physical damage, and electrostatic discharge, ensuring the integrity of delicate wafers throughout the semiconductor manufacturing process. Common materials used in wafer cases include stainless steel, polycarbonate, and polypropylene, each offering specific advantages such as durability, transparency, and cost-effectiveness.

Key Highlights

- The wafer cases market is anticipated to grow at a CAGR of 4.8% during the forecast period.

- The global wafer cases market was estimated to be worth approximately USD 8.96 billion in 2023 and is projected to reach a value of USD 14.33 billion by 2032.

- The growth of the wafer cases market is being driven by the rapid expansion of the semiconductor industry.

- Based on the material type, the plastic wafer cases segment is growing at a high rate and is projected to dominate the market.

- On the basis of end-user application, the semiconductor manufacturing segment is projected to swipe the largest market share.

- In terms of type of wafer, the silicon wafers segment is expected to dominate the market.

- Based on the loading mechanism, the automatic loading segment is expected to dominate the market.

- In terms of customization options, the standard sizes and configurations segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Wafer Cases Market: Dynamics

Key Growth Drivers:

- Growing Demand for Semiconductor Devices: The increasing use of electronic devices and components in sectors like consumer electronics, automotive, telecommunications, and industrial automation is driving the need for wafer protection and transportation solutions.

- Expansion of the Global Semiconductor Industry: With the rapid growth in semiconductor fabrication and the construction of new fabs worldwide, demand for wafer cases to ensure safe handling and transportation has significantly increased.

- Rising Need for Contamination Control: Wafer cases are crucial in preventing contamination during handling and transport. As chip manufacturers demand cleaner environments, the importance of quality wafer cases grows.

- Technological Advancements in Wafer Packaging: New materials and design innovations are enhancing the durability, weight, and chemical resistance of wafer cases, further driving market adoption.

Restraints:

- High Cost of Advanced Wafer Cases: Cases made with premium materials and sophisticated designs tend to be expensive, which can be a barrier for smaller semiconductor firms or cost-sensitive markets.

- Stringent Industry Standards and Regulations: Meeting rigorous quality and compliance standards in the semiconductor industry adds complexity to wafer case production and limits flexibility in design and materials.

- Limited Reusability and Environmental Concerns: Although many wafer cases are reusable, concerns about plastic waste and environmental impact are leading to scrutiny over the sustainability of traditional materials.

Opportunities:

- Rise in 5G, IoT, and AI Technologies: The proliferation of smart technologies is boosting chip production, thereby creating a higher demand for wafer packaging and protection solutions like wafer cases.

- Growth in Emerging Markets: Semiconductor manufacturing is expanding in regions like Southeast Asia, India, and Eastern Europe, offering new business opportunities for wafer case manufacturers.

- Development of Eco-Friendly Wafer Cases: Increasing focus on sustainability is pushing manufacturers to develop biodegradable or recyclable wafer cases, opening up new market segments.

- Customization and Smart Packaging: The demand for application-specific and traceable packaging is rising. Integration of tracking features and custom-fit cases presents new avenues for innovation.

Challenges:

- Supply Chain Disruptions: Global events like pandemics or geopolitical tensions can disrupt the supply of raw materials and impact the wafer case production and delivery timeline.

- Intense Market Competition: A large number of manufacturers competing on pricing and innovation make it difficult to maintain strong profit margins and market differentiation.

- Dependence on Semiconductor Market Cycles: The wafer case market is closely tied to the cyclical nature of the semiconductor industry, making it vulnerable to periods of slowdown or reduced chip production.

- Limited Awareness in Smaller Markets: In some developing markets, the importance of using high-quality wafer cases is not fully recognized, which affects demand growth in those regions.

Wafer Cases Market: Report Scope

This report thoroughly analyzes the Wafer Cases Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Wafer Cases Market |

| Market Size in 2023 | USD 8.96 Billion |

| Market Forecast in 2032 | USD 14.33 Billion |

| Growth Rate | CAGR of 4.8% |

| Number of Pages | 169 |

| Key Companies Covered | Entegris, Shin-Etsu Polymer, Miraial Co. Ltd., 3S Korea, Chuang King Enterprise, Gudeng Precision |

| Segments Covered | By Material Type, By End-user Application, By Type of Wafer, By Loading Mechanism, By Customization Options, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Wafer Cases Market: Segmentation Insights

The global wafer cases market is divided by material type, end-user application, type of wafer, loading mechanism, customization options, and region.

Segmentation Insights by Material Type

Based on material type, the global wafer cases market is divided into plastic wafer cases, metal wafer cases, composite wafer cases, and silicon wafer cases.

In the wafer cases market, plastic wafer cases are the most dominant segment by material type. Their widespread adoption is attributed to their lightweight nature, cost-effectiveness, and excellent resistance to chemicals and moisture. These characteristics make plastic wafer cases ideal for storing and transporting delicate semiconductor wafers without contamination or damage. Moreover, their compatibility with automation systems and customization options have further solidified their place as the leading choice among manufacturers.

Composite wafer cases follow plastic in terms of market share. These are engineered using a combination of materials—often plastic reinforced with fiberglass or carbon fiber—to enhance mechanical strength and thermal stability. Composite cases are favored in environments that demand both durability and protection against thermal and electrostatic risks. Though they are more expensive than pure plastic cases, their superior performance justifies the investment, particularly in high-end semiconductor manufacturing.

Metal wafer cases come next and are primarily used in highly specialized applications where robustness and long-term durability are critical. Made commonly from stainless steel or aluminum, these cases offer excellent structural integrity and shielding against electromagnetic interference (EMI). However, due to their higher weight and cost, their use is generally restricted to niche sectors or research facilities requiring maximum protection.

Silicon wafer cases represent the least dominant segment. These are typically used for very specific use cases involving ultra-clean environments, where their soft and flexible nature helps in preventing any physical stress or scratches on the wafers. Although they offer excellent sealing and vibration absorption, their limited structural strength and relatively high cost have kept their adoption rate low compared to other materials.

Segmentation Insights by End-user Application

On the basis of end-user application, the global wafer cases market is bifurcated into semiconductor manufacturing, photovoltaics, microelectronics, and optoelectronics.

In the wafer cases market by application, semiconductor manufacturing stands as the most dominant segment. This dominance is driven by the ever-growing demand for integrated circuits and chips used in a wide range of electronics, from consumer devices to industrial machinery. Wafer cases in this sector are essential for safely transporting and storing wafers throughout various stages of the manufacturing process, including lithography, etching, and packaging. The need for contamination-free handling and precise environmental protection further amplifies the demand for high-quality wafer cases in this application.

Photovoltaics is the second most significant application segment. With the global push toward renewable energy, the production of solar cells has seen tremendous growth. Wafer cases play a crucial role in ensuring the safe handling and transportation of silicon wafers used in photovoltaic panels. While the cleanliness standards are slightly less stringent than those in semiconductor fabrication, the increasing volume of solar wafer production keeps this segment highly active.

Microelectronics follows next, covering applications like sensors, microcontrollers, and miniature electronic components used in medical devices, automotive systems, and industrial equipment. The compact and intricate nature of these devices requires wafer cases that offer precise protection during fabrication and assembly. Though this segment is smaller in scale than semiconductor manufacturing, it still contributes significantly to the overall market due to the diversity of products it supports.

Optoelectronics is the least dominant application segment in the wafer cases market. This area includes devices like LEDs, laser diodes, and photodetectors. While these components are crucial in fields like telecommunications, display technology, and imaging, the volume of wafers used is comparatively lower. However, because of the sensitivity of these devices to contamination and physical damage, specialized wafer cases are still essential, albeit on a smaller scale relative to other application areas.

Segmentation Insights by Type of Wafer

Based on type of wafer, the global wafer cases market is divided into silicon wafers, gallium arsenide wafers, silicon carbide wafers, and other specialty wafers.

In the wafer cases market by type of wafer, silicon wafers are by far the most dominant segment. Silicon is the foundational material for the majority of semiconductor devices due to its ideal electronic properties, abundant availability, and mature processing ecosystem. Wafer cases designed for silicon wafers are produced at high volumes and are optimized for cost-effective protection, cleanliness, and compatibility with automated manufacturing systems. The massive demand from sectors such as consumer electronics, automotive, telecommunications, and computing fuels the continued dominance of this segment.

Silicon carbide (SiC) wafers are the next most significant type. SiC wafers are increasingly used in high-power and high-temperature applications, particularly in electric vehicles (EVs), power electronics, and industrial systems. Although still smaller in volume compared to silicon wafers, the rapid growth of EV and renewable energy markets has accelerated the demand for durable wafer cases that can handle the unique properties and higher costs of SiC wafers, which are more brittle and expensive than their silicon counterparts.

Gallium arsenide (GaAs) wafers follow, primarily used in high-frequency and optoelectronic applications, such as RF amplifiers, satellite communications, and LEDs. GaAs wafers are highly sensitive and require robust protection against contamination and mechanical stress. While they represent a smaller portion of the total wafer production, their use in niche but critical technologies support a steady demand for specialized wafer cases tailored to their specific handling requirements.

Segmentation Insights by Loading Mechanism

On the basis of loading mechanism, the global wafer cases market is bifurcated into manual loading, automatic loading, and hybrid loading mechanisms.

In the wafer cases market by loading mechanism, automatic loading mechanisms represent the most dominant segment. The drive toward automation in semiconductor and electronics manufacturing has significantly increased the demand for wafer cases compatible with automated handling systems. These cases are designed to work seamlessly with robotic arms, conveyors, and wafer transfer systems in cleanroom environments, ensuring minimal human contact, reduced contamination risk, and improved operational efficiency. As fabrication facilities scale up production and adopt Industry 4.0 practices, the preference for automation-compatible wafer cases continues to grow.

Hybrid loading mechanisms come next, offering a flexible combination of both manual and automatic features. These are especially valuable in facilities where certain stages of wafer handling are automated, while others still rely on human intervention. Hybrid systems are favored in mid-sized fabs, R&D labs, and facilities transitioning from manual to fully automated workflows. They provide a balance between cost, control, and adaptability, making them a practical solution in semi-automated environments.

Manual loading mechanisms are the least dominant segment, largely due to the increasing need for cleanliness, consistency, and speed in wafer handling. However, they are still commonly used in smaller fabrication units, academic institutions, and specialized processes where automation is either not feasible or cost-justifiable. Manual loading wafer cases are typically simpler in design and lower in cost but require stringent handling protocols to avoid wafer damage and contamination. As automation continues to permeate the industry, the usage of manual systems is expected to decline, though it will likely remain relevant in low-volume or specialized settings.

Segmentation Insights by Customization Options

On the basis of customization options, the global wafer cases market is bifurcated into standard sizes & configurations, custom designed wafer cases, branded wafer cases, and environmentally friendly options.

In the wafer cases market by customization options, standard sizes and configurations dominate the segment. These wafer cases are manufactured in compliance with industry norms and specifications (such as SEMI standards), making them highly compatible with existing equipment and automated systems. Their widespread use across semiconductor fabs, photovoltaics, and microelectronics is driven by their cost-efficiency, mass availability, and reliability for general-purpose wafer handling. They offer sufficient protection and are readily available in bulk, which is ideal for high-volume production environments.

Custom-designed wafer cases are the second most prominent segment. These cases are tailored to meet specific client requirements regarding wafer size, shape, material handling preferences, or environmental protection needs. Industries working with specialty wafers or conducting R&D often opt for custom designs to accommodate non-standard dimensions or enhanced protection features. Although more expensive than standard cases, they are crucial for applications where generic options cannot provide adequate safety or performance.

Branded wafer cases come next. These are cases that not only offer functional benefits but also carry customized brand logos, colors, or design elements. They are typically used by companies that want to reinforce brand identity within cleanroom operations or differentiate their handling equipment. While branding does not affect the core functionality of the wafer case, it plays a role in corporate image and internal consistency, especially among large OEMs or fabless semiconductor companies.

Environmentally friendly options are currently the least dominant but rapidly emerging segment. These include wafer cases made from recyclable, biodegradable, or reusable materials, aimed at reducing the environmental footprint of semiconductor manufacturing. With growing sustainability mandates and ESG commitments across the tech industry, there's increasing interest in eco-conscious solutions. However, due to concerns over contamination control, durability, and cost, these cases are still in early adoption phases and have yet to match the scale of traditional solutions.

Wafer Cases Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific is the most dominant region in the wafer cases market, primarily due to its advanced semiconductor manufacturing ecosystem and strong demand for electronic devices. Countries such as China, Japan, South Korea, and Taiwan play a pivotal role in driving regional growth, with China holding the largest market share owing to its expansive production capabilities and government-backed initiatives in the semiconductor sector. The increasing adoption of miniaturized electronics, along with rising investments in wafer-level packaging technologies, continues to strengthen the region’s leadership. Additionally, India is emerging as a fast-growing market, fueled by rising consumer demand and strategic developments in chip fabrication.

North America follows as a key region in the wafer cases market, supported by its technological innovation, strong research and development infrastructure, and the presence of major semiconductor companies. The region sees significant demand from sectors such as high-performance computing, automotive electronics, and telecommunications. Continued advancements in wafer-level integration and packaging techniques contribute to the steady growth of the market. Government support for reshoring semiconductor manufacturing and investment in domestic chip production also bolster the regional outlook.

Europe holds a solid position in the global market, driven by its well-established automotive and industrial electronics sectors. Countries like Germany, France, and the United Kingdom contribute significantly, with increasing deployment of IoT and smart technologies requiring advanced semiconductor solutions. Supportive policies, regional innovation hubs, and collaborative research initiatives across the EU further enhance the market environment, although the region’s reliance on imports for certain critical materials can pose challenges to faster growth.

Latin America is witnessing moderate growth in the wafer cases market, with Brazil acting as a key contributor. The gradual expansion of the electronics manufacturing industry and increasing investments in digital transformation are helping the region develop its semiconductor infrastructure. However, limited local production capabilities and high dependence on imports restrict market acceleration compared to other regions.

Middle East and Africa (MEA) is the least dominant region but is gradually gaining traction due to increasing government initiatives aimed at diversifying economies and investing in high-tech industries. The UAE and Saudi Arabia are focusing on building smart city infrastructure, which in turn supports demand for electronic components, including wafer cases. However, the market in this region remains nascent and faces challenges related to technological readiness and limited local manufacturing capacity.

Wafer Cases Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the wafer cases market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global wafer cases market include:

- Entegris

- Shin-Etsu Polymer

- Miraial Co. Ltd.

- 3S Korea

- Chuang King Enterprise

- Gudeng Precision

The global wafer cases market is segmented as follows:

By Material Type

- Plastic Wafer Cases

- Metal Wafer Cases

- Composite Wafer Cases

- Silicone Wafer Cases

By End-user Application

- Semiconductor Manufacturing

- Photovoltaics

- Microelectronics

- Optoelectronics

By Type of Wafer

- Silicon Wafers

- Gallium Arsenide Wafers

- Silicon Carbide Wafers

- Other Specialty Wafers

By Loading Mechanism

- Manual Loading

- Automatic Loading

- Hybrid Loading Mechanisms

By Customization Options

- Standard Sizes and Configurations

- Custom Designed Wafer Cases

- Branded Wafer Cases

- Environmentally Friendly Options

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Wafer Cases

Request Sample

Wafer Cases