Wafer Die Bonding Film Market Size, Share, and Trends Analysis Report

CAGR :

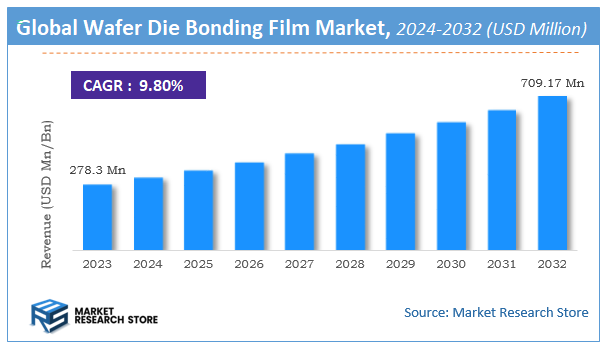

| Market Size 2023 (Base Year) | USD 278.3 Million |

| Market Size 2032 (Forecast Year) | USD 709.17 Million |

| CAGR | 9.8% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Wafer Die Bonding Film Market Insights

According to Market Research Store, the global wafer die bonding film market size was valued at around USD 278.3 million in 2023 and is estimated to reach USD 709.17 million by 2032, to register a CAGR of approximately 9.8% in terms of revenue during the forecast period 2024-2032.

The wafer die bonding film report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Wafer Die Bonding Film Market: Overview

Wafer die bonding film is a specialized adhesive material used in the semiconductor manufacturing process to securely attach individual semiconductor dies (or chips) to substrates, lead frames, or other surfaces. These films serve as an intermediate bonding layer during the die attach process, providing both mechanical support and thermal conductivity. Wafer die bonding films are typically made from thermosetting resins or thermoplastic materials and are engineered to offer precise thickness, excellent adhesion, low outgassing, and compatibility with high-temperature processes commonly used in microelectronics assembly.

The market for wafer die bonding films is growing steadily, driven by the increasing demand for miniaturized and high-performance electronic devices in consumer electronics, automotive electronics, and telecommunications. The rise of advanced packaging technologies, such as flip-chip and wafer-level packaging, is further boosting the adoption of high-performance bonding films. Additionally, as the semiconductor industry continues to shift toward thinner wafers and smaller nodes, manufacturers are developing more advanced bonding film materials that offer improved thermal management, adhesion strength, and reliability. These trends are expected to continue fueling market growth in the years ahead.

Key Highlights

- The wafer die bonding film market is anticipated to grow at a CAGR of 9.8% during the forecast period.

- The global wafer die bonding film market was estimated to be worth approximately USD 278.3 million in 2023 and is projected to reach a value of USD 709.17 million by 2032.

- The growth of the wafer die bonding film market is being driven by the increasing demand for miniaturized and high-performance electronics.

- Based on the product, the non-conductive type segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the die to substrate segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Wafer Die Bonding Film Market: Dynamics

Key Growth Drivers:

- Surging Demand for Semiconductors: The ever-increasing demand for semiconductors across various applications like consumer electronics (smartphones, wearables), automotive (ADAS, EVs), healthcare, industrial automation, and 5G infrastructure necessitates higher production volumes, driving the consumption of die bonding films.

- Trend Towards Miniaturization and High Density: The ongoing drive to create smaller and more powerful electronic devices requires advanced packaging techniques, including the use of thin and high-performance die bonding films for stacking and high-density interconnects.

- Growth in Advanced Packaging Technologies: Advanced packaging methods such as fan-out wafer-level packaging (FOWLP), system-in-package (SiP), and 3D integration rely heavily on die bonding films for reliable die attachment and electrical performance.

- Stringent Performance Requirements: Modern electronic devices demand high reliability, excellent thermal management, and superior electrical performance. Die bonding films are crucial in meeting these requirements by providing strong adhesion, efficient heat dissipation, and stable electrical connections.

- Increasing Automation in Assembly Processes: The need for high throughput and consistent quality in semiconductor manufacturing drives the adoption of automated die bonding equipment, which requires compatible and reliable die bonding films.

- Rise of Electric Vehicles (EVs) and Automotive Electronics: The rapid growth of the EV market and the increasing complexity of automotive electronic systems are driving significant demand for high-performance semiconductors and, consequently, advanced die bonding films.

Restraints:

- High Material Costs: The cost of specialized polymers and conductive fillers used in high-performance die bonding films can be significant, impacting the overall cost of semiconductor packaging.

- Stringent Technical Requirements: Achieving the desired levels of adhesion, thermal conductivity, electrical conductivity (for conductive films), and reliability can be technically challenging and require precise material selection and processing.

- Potential for Delamination and Failure: Inadequate adhesion or thermal stress can lead to delamination of the die from the substrate, causing device failure. Ensuring long-term reliability under various operating conditions is crucial.

- Compatibility Issues: The die bonding film must be compatible with the die material, substrate material, and the specific processing conditions used in assembly. Ensuring this compatibility can be complex.

- Limited Shelf Life and Storage Requirements: Some die bonding films may have a limited shelf life and require specific storage conditions (e.g., temperature, humidity) to maintain their properties.

- Environmental Regulations: Increasing environmental regulations regarding the use of certain chemicals in manufacturing processes may pose challenges for the development and use of some die bonding film materials.

Opportunities:

- Development of Next-Generation Materials: Ongoing research into novel polymers, fillers (e.g., silver, copper nanoparticles), and composite materials with enhanced thermal, electrical, and mechanical properties can create opportunities for higher-performance films.

- Creation of Ultra-Thin Films: The demand for smaller and thinner electronic devices drives the need for ultra-thin die bonding films with excellent bonding strength and reliability.

- Development of Anisotropic Conductive Films (ACFs): ACFs, which provide electrical conductivity in the Z-direction only, are increasingly used in fine-pitch interconnections and offer opportunities for specialized die bonding applications.

- Solutions for High-Temperature Applications: The growing use of semiconductors in harsh environments, such as automotive and industrial applications, creates a demand for die bonding films that can withstand high operating temperatures.

- Integration with Advanced Packaging Processes: Developing die bonding films specifically tailored for emerging advanced packaging techniques like hybrid bonding and chiplets offers significant growth potential.

- Environmentally Friendly and Sustainable Materials: Research into and adoption of more sustainable and halogen-free die bonding film materials can cater to the growing demand for eco-friendly electronics.

Challenges:

- Balancing Performance and Cost: Developing high-performance die bonding films that are also cost-effective for mass production is a continuous challenge.

- Ensuring Reliability Under Extreme Conditions: Meeting the stringent reliability requirements of demanding applications, such as automotive and aerospace, which involve wide temperature ranges and harsh environments.

- Achieving Uniform and Void-Free Bonding: Ensuring consistent and void-free bonding across the die-substrate interface is crucial for thermal and electrical performance and remains a technical challenge.

- Adapting to Diverse Substrate Materials: The increasing use of non-traditional substrate materials requires the development of die bonding films with compatible adhesion properties.

- Meeting the Requirements of Miniaturization and Fine Pitch: Developing die bonding films and application processes that can handle the increasingly small feature sizes and fine pitches in advanced semiconductor devices.

- Standardization and Characterization: Establishing industry-wide standards for the characterization and testing of die bonding films is needed to ensure consistency and reliability across different suppliers and applications.

Wafer Die Bonding Film Market: Report Scope

This report thoroughly analyzes the Wafer Die Bonding Film Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Wafer Die Bonding Film Market |

| Market Size in 2023 | USD 278.3 Million |

| Market Forecast in 2032 | USD 709.17 Million |

| Growth Rate | CAGR of 9.8% |

| Number of Pages | 178 |

| Key Companies Covered | Furukawa, Henkel Adhesives, LG, AI Technology, Nitto, LINTEC Corporation, Hitachi Chemical |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Wafer Die Bonding Film Market: Segmentation Insights

The global wafer die bonding film market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global wafer die bonding film market is divided into non-conductive type and conductive type.

Non-Conductive Type wafer die bonding films are the dominant product in this market segment. These films are widely used in advanced packaging technologies where electrical insulation is required between the die and substrate. Non-conductive films offer excellent adhesion, thermal stability, and process compatibility, making them highly suitable for flip chip, CSP (chip-scale packaging), and BGA (ball grid array) applications. Their role in preventing electrical interference while maintaining strong mechanical bonds has made them essential in high-performance semiconductor packaging. Additionally, non-conductive types are favored in large-scale production due to their lower cost and simplified handling during automated processes, further solidifying their dominance in the market.

Conductive Type wafer die bonding films are typically used in applications that require electrical conductivity between the die and the substrate, such as power semiconductors and RF devices. These films incorporate conductive fillers to create a path for electrical signals, making them suitable for niche or performance-critical components. However, their higher cost and the complexity involved in processing limit their widespread adoption compared to non-conductive types. Despite this, the demand for conductive bonding films is expected to grow gradually with the increasing use of high-frequency and high-power electronic devices.

Segmentation Insights by Application

On the basis of application, the global wafer die bonding film market is bifurcated into die to substrate, die to die, and film on wire.

Die to Substrate is the dominant application in the wafer die bonding film market. This application involves bonding a semiconductor die directly to a substrate, which is a foundational step in creating electronic devices. Die to substrate bonding requires high reliability and strong adhesion, both of which are efficiently provided by wafer die bonding films. These films ensure thermal and mechanical stability, helping to maintain alignment and performance in high-density and miniaturized circuits. As this method is used extensively in consumer electronics, automotive electronics, and industrial devices, it accounts for the largest market share among all application segments.

Die to Die bonding is another significant application, involving the connection of multiple dies to build stacked or 3D integrated circuits (3D ICs). This method is vital for increasing performance and reducing form factors in high-end electronics, such as advanced processors and memory modules. Although still emerging, die to die bonding using wafer die bonding films is growing steadily, fueled by advancements in heterogeneous integration and the need for greater functionality in compact devices.

Film on Wire refers to the use of bonding films in processes involving wire bonding, where the film is applied to stabilize or insulate wire connections. While this is a niche segment compared to die-level bonding, it supports specific use cases where both mechanical strength and thermal management are essential. It is more common in legacy systems or hybrid packaging setups and represents a smaller portion of the overall market.

Wafer Die Bonding Film Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Wafer Die Bonding Film Market due to its advanced semiconductor manufacturing infrastructure, extensive research and development activities, and the presence of key players like Intel, Texas Instruments, and Lam Research. The United States leads the region, driven by strong demand for high-precision semiconductor packaging and increasing investments in chip fabrication facilities. The surge in demand for next-generation electronics, including 5G devices, high-performance computing, and artificial intelligence hardware, further fuels the need for high-performance bonding materials. Government initiatives, such as the CHIPS Act, are also bolstering domestic semiconductor production, thereby boosting the wafer die bonding film market in the region.

Asia-Pacific is the fastest-growing region in the wafer die bonding film market, fueled by its dominant position in global semiconductor manufacturing. Countries like China, Taiwan, South Korea, and Japan house leading foundries and OSAT (Outsourced Semiconductor Assembly and Test) providers. Taiwan’s TSMC and South Korea’s Samsung are key contributors to the demand for wafer bonding films as they expand advanced packaging capacities. China’s push for domestic semiconductor capabilities under its "Made in China 2025" plan and ongoing investment in packaging innovation are also driving regional demand. Additionally, the region benefits from a strong electronics manufacturing base, particularly in consumer electronics and smartphones.

Europe is a significant market for wafer die bonding film, backed by its focus on developing advanced automotive electronics, industrial automation systems, and communication devices. Countries such as Germany, France, and the Netherlands are home to major semiconductor equipment manufacturers and R&D centers. The increasing use of wafer-level packaging in automotive applications—especially with the shift toward electric vehicles and autonomous driving—has accelerated the adoption of high-reliability bonding films. Europe's push for semiconductor self-sufficiency, along with investments in smart factories and microelectronics under initiatives like IPCEI, supports continued market growth.

Latin America presents a growing but modest opportunity in the wafer die bonding film market. Countries like Brazil and Mexico are expanding their roles in electronics manufacturing, largely focused on assembly and lower-end packaging. While the region lacks significant semiconductor fabrication facilities, increasing foreign direct investment and interest in technological advancement are gradually contributing to market development. Growth is expected to be driven by the region’s alignment with global electronics supply chains and the gradual adoption of semiconductor packaging technologies in automotive and industrial sectors.

Middle East and Africa region is an emerging market with limited penetration in the wafer die bonding film sector. However, growing initiatives in smart city infrastructure, digital transformation, and the development of technology parks in countries like the UAE, Israel, and South Africa are fostering interest in semiconductor components and materials. Israel stands out in the region for its strong semiconductor R&D ecosystem and the presence of several fabless design companies, which indirectly supports demand for advanced packaging materials, including bonding films. While still nascent, the region holds long-term growth potential as digitalization spreads.

Wafer Die Bonding Film Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the wafer die bonding film market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global wafer die bonding film market include:

- Furukawa

- Henkel Adhesives

- LG

- AI Technology

- Nitto

- LINTEC Corporation

- Hitachi Chemical

The global wafer die bonding film market is segmented as follows:

By Product

- Non-Conductive Type

- Conductive Type

By Application

- Die to Substrate

- Die to Die

- Film on Wire

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Wafer Die Bonding Film

Request Sample

Wafer Die Bonding Film