Weight Loss App Market Size, Share, and Trends Analysis Report

CAGR :

| Market Size 2023 (Base Year) | USD 856.1 Million |

| Market Size 2032 (Forecast Year) | USD 4271.31 Million |

| CAGR | 17.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Weight Loss App Market Insights

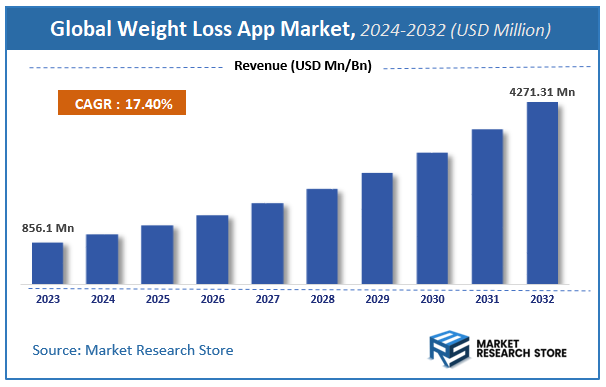

According to Market Research Store, the global weight loss app market size was valued at around USD 856.1 million in 2023 and is estimated to reach USD 4271.31 million by 2032, to register a CAGR of approximately 17.4% in terms of revenue during the forecast period 2024-2032.

The weight loss app report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Weight Loss App Market: Overview

A weight loss app is a mobile application designed to help individuals track, manage, and achieve their weight loss goals. These apps typically offer features like personalized diet plans, exercise tracking, calorie counting, and progress monitoring. Many weight loss apps also provide access to educational content on nutrition, workouts, and mental health, encouraging sustainable and healthy weight loss habits. Some advanced apps integrate with wearable devices, allowing users to track their physical activity and sleep patterns more accurately.

Key Highlights

- The weight loss app market is anticipated to grow at a CAGR of 17.4% during the forecast period.

- The global weight loss app market was estimated to be worth approximately USD 856.1 million in 2023 and is projected to reach a value of USD 4271.31 million by 2032.

- The growth of the weight loss app market is being driven by increasing global awareness of health and fitness.

- Based on the demographic, the age segment is growing at a high rate and is projected to dominate the market.

- On the basis of behavioral, the benefits sought segment is projected to swipe the largest market share.

- In terms of psychographic, the motivation segment is expected to dominate the market.

- Based on the technographic, the device usage segment is expected to dominate the market.

- In terms of motivational, the weight loss goals segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Weight Loss App Market: Dynamics

Key Growth Drivers:

- Increasing Obesity Rates Globally: Rising rates of obesity and associated health risks, such as diabetes, hypertension, and cardiovascular diseases, are driving the demand for weight loss solutions, including apps.

- Growing Health Consciousness: As more individuals adopt healthier lifestyles, there is a growing need for convenient and personalized weight management solutions, which weight loss apps can provide.

- Technological Advancements in Mobile Health (mHealth): Continuous improvements in smartphone technology, sensors, and wearable devices have enhanced the functionality of weight loss apps, making them more effective and user-friendly.

- Integration with Wearable Devices: The growing popularity of wearable health devices (such as fitness trackers and smartwatches) that track physical activity, calories burned, and heart rate has contributed to the growth of weight loss apps that integrate with these devices.

- Personalized Diet and Fitness Plans: Weight loss apps offering personalized and adaptive diet plans, workout routines, and real-time coaching are attracting more users, as they provide tailored solutions to individual health needs.

Restraints:

- Privacy and Data Security Concerns: Weight loss apps often collect sensitive user data, such as personal health information and fitness tracking data, which raises concerns about privacy and the security of this data.

- High Competition in the Market: The weight loss app market is highly saturated, with a large number of similar apps available. This makes it challenging for new entrants to differentiate themselves and capture market share.

- Lack of Standardization in App Quality: Many weight loss apps vary in terms of quality, features, and accuracy. The lack of standardized metrics or certifications may make users skeptical about the effectiveness of some apps.

- User Engagement and Retention Issues: Maintaining user engagement over the long term can be challenging. Users may lose motivation or abandon apps if they do not see immediate results or if the app experience is not engaging enough.

Opportunities:

- Expansion in Emerging Markets: Growing smartphone penetration and increasing awareness of fitness and health in emerging markets present significant growth opportunities for weight loss app providers.

- Incorporation of Artificial Intelligence (AI) and Machine Learning (ML): AI and ML technologies can enhance app functionality by offering more personalized recommendations, tracking, and predictive insights, which can improve user outcomes.

- Collaborations with Healthcare Providers: Partnerships with healthcare professionals, nutritionists, and fitness experts can enhance the credibility of weight loss apps and provide users with access to professional advice, improving the app’s overall value.

- Subscription-Based Revenue Models: A subscription-based model offers weight loss apps the opportunity to generate recurring revenue, providing a more sustainable business model while offering premium features such as personalized coaching or access to exclusive content.

- Integration of Mental Health Support: Weight loss apps that include mental health support, such as stress management techniques or behavioral therapy tools, can create a more holistic approach to weight loss, expanding their appeal.

Challenges:

- Overcoming User Skepticism and Misinformation: Many users may be skeptical about the efficacy of weight loss apps, especially when faced with a flood of conflicting information on diet and exercise, which can lead to uncertainty.

- High Drop-Off Rates: Many users download weight loss apps but fail to use them consistently. The lack of immediate results or difficulties in sticking to weight loss plans may lead to high abandonment rates.

- Unrealistic Expectations: Some apps may promote unrealistic weight loss promises or extreme dieting practices, leading to disappointed users who are not seeing the promised results or experiencing negative health consequences.

- Regulatory and Legal Challenges: With increasing scrutiny on health apps, regulatory bodies may impose stricter guidelines on weight loss apps. Compliance with health and wellness regulations can be complex and costly for app developers.

Weight Loss App Market: Report Scope

This report thoroughly analyzes the Weight Loss App Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Weight Loss App Market |

| Market Size in 2023 | USD 856.1 Million |

| Market Forecast in 2032 | USD 4271.31 Million |

| Growth Rate | CAGR of 17.4% |

| Number of Pages | 172 |

| Key Companies Covered | DailyBu, FatSecret, Fitbit, Fitness Buddy, FitNow, Fooducate, Ideal Weight, iTrackBites, Livestrong, My Diet Coach, MyFitnessPal, Noom Coach, Sworkit, Weight Watchers, YAZIO |

| Segments Covered | By Demographic, By Behavioral, By Psychographic, By Technographic, By Motivational, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Weight Loss App Market: Segmentation Insights

The global weight loss app market is divided by demographic, behavioral, psychographic, technographic, motivational, and region.

Segmentation Insights by Demographic

Based on demographic, the global weight loss app market is divided into age, gender, income level, and occupation.

In the weight loss app market, age is the most dominant demographic segment. Younger adults, especially those in the 18–35 age group, are the most active users of these apps. This age group tends to be more tech-savvy, health-conscious, and driven by aesthetic goals. They are also more likely to engage with digital platforms and social media, making them a prime audience for app-based fitness and diet tracking solutions. Their openness to subscription models and fitness challenges contributes to this segment’s dominance in market engagement and revenue generation.

Following age, gender emerges as the next most significant demographic factor. Women form the majority of users in the weight loss app market. They often seek structured programs, calorie tracking, and community support — features that these apps typically provide. Women are also more likely to engage with personalized wellness content and are often key decision-makers in household health choices, reinforcing their strong presence in the market. While men are also active users, their adoption rates are generally lower compared to women, though this gap has been narrowing in recent years.

Income level ranks next in influence. Individuals with middle to high income levels are more likely to subscribe to premium app features, including personalized coaching, detailed analytics, and ad-free experiences. These users typically have access to smartphones and consistent internet connectivity, allowing for regular use of such digital tools. Conversely, those in lower-income brackets may prefer free versions or seek alternatives due to financial constraints, limiting their overall market impact.

Lastly, occupation is the least dominant demographic segment but still plays a role. Office workers and professionals who are often sedentary are more inclined to use weight loss apps to manage weight and combat inactivity. Meanwhile, individuals in physically demanding jobs might rely less on such tools, as their occupation already contributes to their fitness level. However, the influence of occupation remains limited compared to other demographic factors, making it the least impactful segment in this analysis.

Segmentation Insights by Behavioral

On the basis of behavioral, the global weight loss app market is bifurcated into usage rate, loyalty status, and benefits sought.

In the weight loss app market, benefits sought is the most dominant behavioral segmentation factor. Users typically look for specific outcomes such as calorie tracking, weight monitoring, personalized diet plans, or fitness coaching. These desired benefits drive the design, functionality, and marketing of weight loss apps. Apps that provide multiple, customizable benefits—such as integration with wearables, AI-based recommendations, or mental health tracking—tend to capture a broader user base. The specific benefits users seek often correlate with their fitness goals (e.g., fat loss, muscle gain, or overall health), making this the most influential behavioral driver in the market.

Usage rate comes next in importance. High-usage users, often daily users, represent the most valuable customer group as they engage consistently with app features, contribute to community forums, track progress rigorously, and are more likely to subscribe to premium plans. These users also offer app developers valuable data for improvements. Moderate and light users, while still relevant, have a lower impact on app revenue and retention metrics. Therefore, usage frequency plays a critical role in determining user value and shaping app design and engagement strategies.

Loyalty status is the least dominant behavioral segment, though still meaningful. While brand loyalty exists—especially for well-established apps like MyFitnessPal, Noom, or Lose It!—many users are willing to switch platforms if they find better features or pricing. The prevalence of freemium models and promotional offers often leads to app-hopping behavior. Although some users remain loyal due to community features, historical data, or habit, the market’s competitive nature and ease of switching reduce the overall influence of loyalty in driving long-term user retention.

Segmentation Insights by Psychographic

Based on psychographic, the global weight loss app market is divided into lifestyle, motivation and personality traits.

In the weight loss app market, motivation is the most dominant psychographic segmentation factor. Users are primarily driven by goals such as improving physical appearance, achieving better health, managing chronic conditions, or enhancing athletic performance. These motivations significantly influence how users interact with apps—for instance, someone aiming to manage diabetes may prefer apps with blood sugar tracking, while a user seeking body transformation might prioritize workout routines and calorie counters. Understanding user motivation allows developers to tailor app features, notifications, and content to maintain engagement and achieve better outcomes.

Lifestyle follows as the next key psychographic factor. Individuals with health-conscious or fitness-oriented lifestyles are more likely to adopt and consistently use weight loss apps. Busy professionals may seek quick, efficient tools like meal planning or 10-minute workout modules, while wellness-focused users may prefer holistic platforms that include mindfulness, sleep tracking, and mental health features. Lifestyle patterns also dictate the time of day and context in which users engage with the app, shaping UX/UI design and feature integration.

Personality traits are the least dominant psychographic factor, though they still influence user preferences. Traits like conscientiousness, discipline, and goal orientation can affect app adherence. For example, highly organized individuals might regularly log meals and track progress, while spontaneous users may prefer apps with flexible or gamified experiences. However, personality traits are harder to measure and act upon compared to lifestyle and motivation, which makes them less directly impactful in market targeting and product development.

Segmentation Insights by Technographic

On the basis of technographic, the global weight loss app market is bifurcated into device usage, app usage frequency, and technology adoption.

In the weight loss app market, device usage is the most dominant technographic segmentation factor. Most users access these apps via smartphones, with iOS and Android devices being the primary platforms. The device type and its capabilities—such as screen size, storage, processing speed, and compatibility with wearables—significantly influence user experience. Many premium users also connect their weight loss apps to smartwatches or fitness bands (like Apple Watch, Fitbit, or Garmin), enabling advanced tracking features such as real-time activity monitoring and heart rate data integration. Therefore, understanding device preferences and capabilities is critical for app optimization and user retention.

App usage frequency ranks next in technographic importance. Users who access the app daily or multiple times per day are the most valuable for developers, as they are more likely to engage with advanced features, participate in in-app challenges, and invest in premium subscriptions. These users typically form the core base that drives app revenue and feedback loops. Moderate and occasional users, while still contributing to user volume, offer lower lifetime value and often require re-engagement strategies such as notifications, reminders, and gamified incentives.

Technology adoption is the least dominant technographic factor in this context, though it still plays a role. Early adopters of new fitness technologies, including AI-driven coaching or virtual nutritionists, are often enthusiastic and engaged, but they represent a niche segment. The broader user base generally comprises the early majority or mainstream users who prefer proven and user-friendly features. The weight loss app market thrives more on intuitive UX and reliable functionality than on cutting-edge technology, which limits the impact of technology adoption rates compared to other technographic factors.

Segmentation Insights by Motivational

On the basis of motivational, the global weight loss app market is bifurcated into weight loss goals, support preferences, and dietary preferences.

In the weight loss app market, weight loss goals are the most dominant motivational segmentation factor. Users often begin using these apps with a clear objective in mind—whether it’s losing a specific number of pounds, reducing body fat percentage, preparing for an event (like a wedding or competition), or improving overall health. These goals shape nearly every aspect of app interaction, from initial onboarding to personalized recommendations and progress tracking. Apps that allow users to set and adjust goals, monitor milestones, and receive tailored feedback tend to see higher engagement and retention rates. Because weight loss goals directly drive the core purpose of these apps, this segment carries the most weight in user motivation.

Next in importance are dietary preferences, which significantly affect user engagement but are more specific in nature. Users often look for apps that align with particular diets—such as keto, intermittent fasting, vegan, low-carb, or paleo. Apps that offer customized meal plans, macro tracking, grocery lists, and recipe suggestions based on these preferences tend to attract niche but loyal user bases. As dietary habits are often deeply personal or medically driven, aligning app features with user food preferences adds substantial value and boosts satisfaction.

Support preferences rank as the least dominant motivational factor but still contribute to user experience. Some users prefer self-guided approaches with minimal interaction, while others seek external motivation through in-app communities, coaching, or accountability partners. While not every user requires support systems, offering options like chatbots, social groups, or real-time coaching can improve engagement and retention among those who do. However, the need for support is secondary to having clear goals and compatible dietary options, making this the least influential segment in terms of initial user attraction.

Weight Loss App Market: Regional Insights

- North America is expected to dominates the global market

The North American market for weight loss apps is the most dominant globally. It is driven by a strong culture of fitness, high smartphone penetration, and significant disposable incomes. The United States and Canada lead in the adoption of health and wellness apps, supported by government health initiatives and the presence of major tech and fitness brands, further driving market growth.

Europe follows closely behind, with countries such as Germany, the UK, and France showing robust demand for weight loss apps. Growing health awareness, government support for fitness initiatives, and the widespread adoption of digital health solutions contribute to the region's growth. The established healthcare infrastructure and focus on preventive health also play significant roles in expanding the market.

The Asia Pacific region is rapidly emerging as a key market for weight loss apps. Rising disposable incomes, increasing smartphone users, and the growing prevalence of obesity are fueling market demand. Countries like China, India, and Japan are witnessing a surge in popularity, supported by the localization of app content and language options. The shift towards more sedentary lifestyles in urban areas further drives the need for digital health solutions.

Latin America is still in the early stages of adopting weight loss apps but shows considerable growth potential. Increasing urbanization, a rising focus on health, and the growing smartphone user base are key factors driving market interest. Countries such as Brazil and Mexico are gradually adopting these digital health solutions, although cultural relevance and affordability remain important considerations for market expansion.

The Middle East and Africa (MEA) region represents a smaller share of the global weight loss app market, but growth is happening due to urbanization and increasing health awareness. In the Gulf Cooperation Council (GCC) countries, like Saudi Arabia and the UAE, there is rising interest in fitness apps, driven by disposable incomes and a younger demographic. However, challenges such as limited internet access in certain areas and cultural factors may hinder widespread adoption in other parts of the region.

Recent Developments:

- In February 2024, Samsung Electronics partnered with FlexIt to bring trainer-led fitness content to Samsung Smart TV users. Through the Samsung Daily+ lifestyle hub on the Tizen OS, users can now access interactive, personalized workouts designed to make exercise more accessible and convenient at home.

- In August 2023, IT company Amo launched HARNA, a fitness app designed to transform how women approach exercise. HARNA syncs workouts with the menstrual cycle, using a phase-based approach to tailor routines for each stage. This helps women integrate effective, personalized workouts into their daily lives, enhancing performance and overall well-being.

Weight Loss App Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the weight loss app market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global weight loss app market include:

- DailyBu

- FatSecret

- Fitbit

- Fitness Buddy

- FitNow

- Fooducate

- Ideal Weight

- iTrackBites

- Livestrong

- My Diet Coach

- MyFitnessPal

- Noom Coach

- Sworkit

- Weight Watchers

- YAZIO

The global weight loss app market is segmented as follows:

By Demographic

- Age

- Gender

- Income Level

- Occupation

By Behavioral

- Usage Rate

- Loyalty Status

- Benefits Sought

By Psychographic

- Lifestyle

- Motivation

- Personality Traits

By Technographic

- Device Usage

- App Usage Frequency

- Technology Adoption

By Motivational

- Weight Loss Goals

- Support Preferences

- Dietary Preferences

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Weight Loss App

Request Sample

Weight Loss App