Wireless Telecommunication Carriers Market Size, Share, and Trends Analysis Report

CAGR :

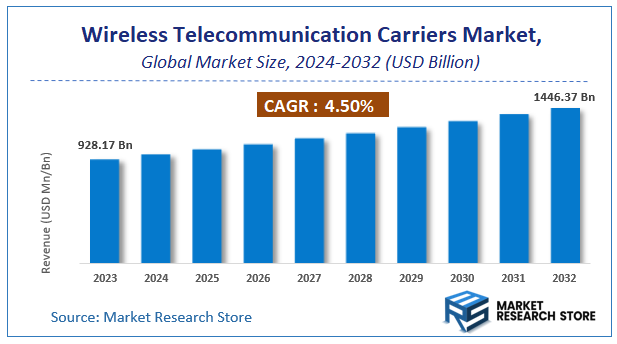

| Market Size 2023 (Base Year) | USD 928.17 Billion |

| Market Size 2032 (Forecast Year) | USD 1446.37 Billion |

| CAGR | 4.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Wireless Telecommunication Carriers Market Insights

According to Market Research Store, the global wireless telecommunication carriers market size was valued at around USD 928.17 billion in 2023 and is estimated to reach USD 1446.37 billion by 2032, to register a CAGR of approximately 4.5% in terms of revenue during the forecast period 2024-2032.

The wireless telecommunication carriers report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Wireless Telecommunication Carriers Market: Overview

Wireless telecommunication carriers are companies that provide wireless communication services to consumers and businesses using radio frequency signals rather than wired infrastructure. These services primarily include voice calling, text messaging (SMS), and data transmission via cellular networks such as 3G, 4G LTE, and increasingly 5G. Wireless carriers operate and maintain network infrastructure such as cell towers, antennas, and base stations, and they often offer mobile plans, devices, and value-added services. Major global players in this sector include Verizon, AT&T, T-Mobile, Vodafone, and China Mobile, among others. These carriers also engage in partnerships with device manufacturers and content providers to expand their service offerings and customer base.

Key Highlights

- The wireless telecommunication carriers market is anticipated to grow at a CAGR of 4.5% during the forecast period.

- The global wireless telecommunication carriers market was estimated to be worth approximately USD 928.17 billion in 2023 and is projected to reach a value of USD 1446.37 billion by 2032.

- The growth of the wireless telecommunication carriers market is being driven by the rapid rise in mobile device usage, increased internet penetration, and the global shift toward digital communication.

- Based on the service type, the data services segment is growing at a high rate and is projected to dominate the market.

- In terms of technology, the 4G segment is expected to dominate the market.

- Based on the end-user, the residential segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Wireless Telecommunication Carriers Market: Dynamics

Key Growth Drivers:

- Rising Mobile Data Consumption: The exponential growth in mobile data usage driven by video streaming, social media, and mobile applications is significantly boosting demand for wireless telecom services.

- Expansion of 5G Networks: The global rollout of 5G technology is enhancing network capabilities, increasing speed, and reducing latency, which is attracting more users and driving carrier revenue.

- Proliferation of IoT Devices: The growing adoption of Internet of Things (IoT) devices across industries is increasing the need for robust wireless connectivity, further expanding the market for wireless carriers.

- Increasing Smartphone Penetration: The rapid rise in smartphone adoption, especially in emerging economies, is fueling the demand for mobile voice and data services.

- Remote Work and Digital Transformation: Shifts in work culture and the digitalization of services post-pandemic have heightened the importance of reliable wireless communication, accelerating market growth.

Restraints:

- High Infrastructure and Spectrum Costs: The need for continuous investment in network infrastructure and spectrum licenses creates financial burdens, particularly for smaller or regional players.

- Stringent Regulatory Environment: Regulatory challenges including spectrum allocation, pricing controls, and data privacy laws can hinder operational flexibility and profitability.

- Market Saturation in Developed Economies: In regions like North America and Western Europe, the market is nearing saturation, making customer acquisition increasingly difficult.

Opportunities:

- Emerging Markets Expansion: Developing countries offer huge potential due to growing populations, rising smartphone usage, and improving telecom infrastructure.

- Network Virtualization and Cloud Integration: The adoption of software-defined networking (SDN) and network function virtualization (NFV) enables more efficient operations and service innovation.

- Private 5G Networks and Enterprise Solutions: Carriers can tap into new revenue streams by providing private 5G solutions for enterprises seeking secure, high-performance networks.

- Value-Added Services and Bundled Offerings: Offering integrated services like cloud storage, media streaming, and IoT-based solutions can increase customer retention and average revenue per user (ARPU).

Challenges:

- Intense Competitive Pressure: The market is highly competitive, with carriers constantly vying for market share through aggressive pricing and service packages, which can erode profit margins.

- Rapid Technological Changes: Keeping up with fast-evolving technologies and customer expectations requires continual investment and innovation.

- Cybersecurity Threats: Increasing dependence on digital networks raises vulnerability to cyberattacks, requiring robust security infrastructure and protocols.

- Environmental and Health Concerns: Public concerns regarding the environmental impact of network expansion and potential health risks from electromagnetic fields (EMFs) can lead to opposition and regulatory delays.

Wireless Telecommunication Carriers Market: Report Scope

This report thoroughly analyzes the Wireless Telecommunication Carriers Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Wireless Telecommunication Carriers Market |

| Market Size in 2023 | USD 928.17 Billion |

| Market Forecast in 2032 | USD 1446.37 Billion |

| Growth Rate | CAGR of 4.5% |

| Number of Pages | 193 |

| Key Companies Covered | AT&T Inc. (U.S.), China Mobile Communications Corporation (China), Verizon Communications Inc. (U.S.), Vodafone Group PLC (U.K.), The Nippon Telegraph and Telephone Corporation (Japan), Telefónica S.A.(Spain), América Móvil (Mexico), Deutsche Telekom AG ( |

| Segments Covered | By Service Type, By Technology, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Wireless Telecommunication Carriers Market: Segmentation Insights

The global wireless telecommunication carriers market is divided by service type, technology, end-user, and region.

Segmentation Insights by Service Type

Based on service type, the global wireless telecommunication carriers market is divided into voice services, data services, and messaging services.

In the wireless telecommunication carriers market, data services have emerged as the most dominant segment among service types. The widespread adoption of smartphones, increasing demand for mobile internet, and the rapid expansion of 4G and 5G networks have significantly fueled the growth of data services. Consumers and businesses increasingly rely on mobile data for video streaming, social media, cloud-based applications, and remote work solutions. As a result, data services have become the primary revenue driver for wireless telecom providers, overshadowing traditional voice and messaging services.

Voice services rank second in the market. Although their usage has declined compared to the peak of mobile communication in the early 2000s, voice services still hold relevance for personal and business communications. Innovations such as VoLTE (Voice over LTE) and VoWiFi (Voice over Wi-Fi) have kept voice communication efficient and cost-effective. However, their share in the overall revenue mix has reduced due to the growing consumer preference for internet-based communication platforms.

Messaging services represent the least dominant segment in this market. The traditional SMS and MMS services have experienced a sharp decline in demand due to the rise of over-the-top (OTT) messaging platforms like WhatsApp, Telegram, and Facebook Messenger. These apps offer richer features, such as media sharing, voice notes, and end-to-end encryption, which have drawn users away from conventional carrier-based messaging services. As a result, messaging services now contribute minimally to the revenue and growth of wireless telecom carriers.

Segmentation Insights by Technology

On the basis of technology, the global wireless telecommunication carriers market is bifurcated into 3G, 4G, and 5G.

In the wireless telecommunication carriers market, 4G technology currently stands as the most dominant segment by technology. Its widespread global deployment, strong network stability, and ability to support high-speed internet access have made it the backbone of mobile communications for the past decade. 4G networks offer efficient bandwidth use, support for high-definition video streaming, seamless mobile browsing, and a wide range of app-based services. The maturity of 4G infrastructure and its extensive availability in both urban and rural areas contribute significantly to its continued dominance, even as newer technologies emerge.

5G technology is the second most prominent and rapidly growing segment. Although still in its early to mid-stages of global deployment, 5G promises ultra-fast internet speeds, low latency, and enhanced connectivity for emerging technologies such as the Internet of Things (IoT), autonomous vehicles, and smart cities. Telecommunications carriers are heavily investing in 5G rollouts, and adoption is accelerating in major markets like the U.S., China, South Korea, and parts of Europe. As the ecosystem matures and compatible devices become more affordable, 5G is expected to gradually overtake 4G in the long term.

3G technology is the least dominant segment and is gradually being phased out in many regions. Once a revolutionary leap in mobile data and voice transmission, 3G has now become outdated in the face of more advanced and efficient technologies. Many telecom operators are shutting down their 3G networks to repurpose the spectrum for 4G and 5G services. While 3G may still be active in some developing regions with limited infrastructure, its relevance in the market continues to decline rapidly.

Segmentation Insights by End-User

On the basis of end-user, the global wireless telecommunication carriers market is bifurcated into residential, commercial, and industrial.

In the wireless telecommunication carriers market, the residential segment is the most dominant end-user category. This dominance is driven by the mass adoption of smartphones and mobile devices for personal communication, entertainment, social media, and remote learning. Residential users heavily rely on wireless services for both voice and data, making them the primary revenue contributors to telecom carriers. The growing consumption of streaming services, mobile gaming, and everyday digital connectivity needs has further cemented the residential segment's leading position in the market.

The commercial segment follows as the second most significant end-user. Businesses of all sizes depend on wireless telecom services for operations, including mobile workforce management, cloud-based solutions, video conferencing, and enterprise communication tools. The adoption of advanced technologies such as 5G in the commercial sector is rapidly increasing to support real-time data transfer, automation, and remote collaboration. While not as large in user volume as the residential segment, the commercial sector generates substantial revenue due to higher data usage and premium service requirements.

The industrial segment is currently the least dominant but holds strong growth potential. Industrial users include sectors such as manufacturing, logistics, mining, and energy, which are beginning to integrate wireless telecom services into their operations through technologies like machine-to-machine (M2M) communication and industrial IoT (IIoT). While adoption is still emerging, especially in less connected regions, the rollout of private 5G networks and the push for smart factories and automation are expected to increase the relevance of this segment in the coming years.

Wireless Telecommunication Carriers Market: Regional Insights

- North America is expected to dominates the global market

The North America region is the most dominant in the global wireless telecommunication carriers market. Its leadership is primarily driven by the United States, which has seen rapid and widespread deployment of advanced wireless infrastructure, particularly 5G. The region boasts high smartphone penetration, strong demand for data services, and substantial investments by major telecom providers in expanding and upgrading networks. Additionally, early adoption of emerging technologies such as IoT, edge computing, and AI-driven network optimization reinforces North America's leading position in the global market.

The Asia-Pacific region follows as a strong contender, with significant contributions from China, India, Japan, and South Korea. China’s aggressive 5G rollout and integration of wireless technology in smart cities and industrial automation have greatly influenced the regional growth. Meanwhile, India is rapidly expanding its telecom infrastructure to accommodate its vast population and rising internet users. The combination of government digital initiatives, expanding mobile user base, and technological innovation makes Asia-Pacific a high-growth region with long-term potential.

The Europe region holds a notable position in the market, supported by established telecom infrastructure and regulatory support for next-generation wireless services. Countries such as Germany, France, and the UK lead in terms of network quality and service offerings. Despite market maturity and slower growth rates compared to Asia-Pacific, European operators are investing in 5G development and exploring opportunities in adjacent regions like the Middle East and Africa to drive future expansion.

The Latin America region is experiencing moderate growth, fueled by increasing mobile device adoption and demand for improved internet access. Countries such as Brazil and Mexico are prioritizing network modernization and expanding coverage to underserved populations. While the region faces infrastructure and affordability challenges, ongoing investments in 4G and gradual 5G introduction are enhancing the competitive landscape and digital inclusion.

The Middle East and Africa region represents an emerging opportunity within the wireless telecommunication carriers market. This region is characterized by a young and digitally aware population, especially in urban centers. While connectivity gaps remain in rural areas, telecom companies are actively working to expand coverage and deploy affordable mobile solutions. Investments in digital transformation and cross-border telecom partnerships are beginning to unlock the region’s long-term potential.

Wireless Telecommunication Carriers Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the wireless telecommunication carriers market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global wireless telecommunication carriers market include:

- AT&T Inc. (U.S.)

- China Mobile Communications Corporation (China)

- Verizon Communications Inc. (U.S.)

- Vodafone Group PLC (U.K.)

- The Nippon Telegraph and Telephone Corporation (Japan)

- Telefónica S.A.(Spain)

- América Móvil (Mexico)

- Deutsche Telekom AG (Germany)

- China Telecommunications Corporation (China)

- SoftBank Group Corp (Japan)

The global wireless telecommunication carriers market is segmented as follows:

By Service Type

- Voice Services

- Data Services

- Messaging Services

By Technology

- 3G

- 4G

- 5G

By End-User

- Residential

- Commercial

- Industrial

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Wireless Telecommunication Carriers

Request Sample

Wireless Telecommunication Carriers