Vehicle Plastic Fuel Tank Systems Market Size, Share, and Trends Analysis Report

CAGR :

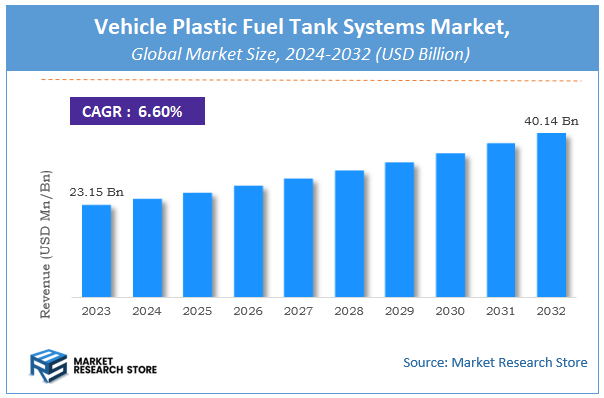

| Market Size 2023 (Base Year) | USD 23.15 Billion |

| Market Size 2032 (Forecast Year) | USD 40.14 Billion |

| CAGR | 6.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Vehicle Plastic Fuel Tank Systems Market Insights

According to Market Research Store, the global vehicle plastic fuel tank systems market size was valued at around USD 23.15 billion in 2023 and is estimated to reach USD 40.14 billion by 2032, to register a CAGR of approximately 6.6% in terms of revenue during the forecast period 2024-2032.

The vehicle plastic fuel tank systems report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Vehicle Plastic Fuel Tank Systems Market: Overview

Vehicle plastic fuel tank systems are lightweight containers used to store fuel in automobiles, typically made from high-density polyethylene (HDPE) or other durable plastics. These systems are designed to meet stringent safety, environmental, and performance standards, offering advantages such as resistance to corrosion, improved fuel efficiency due to reduced weight, and enhanced design flexibility. Unlike traditional metal tanks, plastic fuel tanks can be molded into complex shapes, allowing for better space optimization within the vehicle chassis. They also contribute to lower emissions through advanced multilayer structures that limit fuel vapor permeation, aligning with global regulatory trends.

Key Highlights

- The vehicle plastic fuel tank systems market is anticipated to grow at a CAGR of 6.6% during the forecast period.

- The global vehicle plastic fuel tank systems market was estimated to be worth approximately USD 23.15 billion in 2023 and is projected to reach a value of USD 40.14 billion by 2032.

- The growth of the vehicle plastic fuel tank systems market is being driven by the automotive industry's shift towards lightweight and fuel-efficient vehicles.

- Based on the material type, the high-density polyethylene (HDPE)segment is growing at a high rate and is projected to dominate the market.

- On the basis of vehicle type, the passenger cars segment is projected to swipe the largest market share.

- In terms of sales channel, the OEM segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Vehicle Plastic Fuel Tank Systems Market: Dynamics

Key Growth Drivers:

- Lightweight and Fuel-Efficient Design: Plastic fuel tanks are significantly lighter than their metal counterparts, contributing to improved fuel efficiency and reduced vehicle emissions, aligning with global sustainability goals.

- Corrosion Resistance and Durability: Plastic tanks are resistant to rust and corrosion, enhancing the lifespan of the fuel system and reducing maintenance costs for vehicle owners.

- Growing Automotive Production: The increasing demand for passenger and commercial vehicles worldwide is directly boosting the demand for plastic fuel tank systems.

- Stringent Emission Norms: Regulatory pressure to reduce vehicle emissions is encouraging automakers to adopt lightweight materials like plastic in fuel tank systems to meet fuel economy standards.

- Design Flexibility and Integration Capabilities: Plastic fuel tanks offer better design flexibility, allowing for complex shapes and integration with components such as sensors, valves, and pumps.

Restraints:

- High Initial Tooling and Production Costs: The setup and tooling costs for manufacturing plastic fuel tanks, especially in smaller production volumes, can be high, limiting entry for smaller players.

- Limited Temperature Resistance: Plastic fuel tanks may not perform as well as metal ones under extremely high-temperature conditions, which can limit their use in certain vehicle types or regions.

- Concerns Over Permeability: Despite advancements, plastic fuel tanks may still have higher fuel permeability compared to metal tanks, which can be a concern in meeting environmental and safety regulations.

Opportunities:

- Rising Adoption in Hybrid and Plug-in Hybrid Vehicles: As hybrid vehicle adoption increases, demand for lightweight components like plastic fuel tanks is expected to grow significantly.

- Expansion in Emerging Automotive Markets: Rapid vehicle production and growing middle-class populations in regions like Asia-Pacific and Latin America provide a strong growth avenue for plastic fuel tank manufacturers.

- Technological Innovations in Materials: Advancements in high-performance polymers and multi-layer plastic tank technologies are enhancing strength, safety, and environmental compatibility, opening new market opportunities.

- Aftermarket Growth Potential: Replacement and retrofitting of fuel tank systems in aging vehicle fleets present additional business opportunities for aftermarket players.

Challenges:

- Volatility in Raw Material Prices: The cost of plastic resins, primarily derived from petrochemicals, is subject to market fluctuations, impacting the profitability of manufacturers.

- Environmental Regulations on Plastic Use: Increasing scrutiny and regulation on plastic usage and disposal could affect the market perception and growth of plastic-based fuel tank systems.

- Competition from Alternative Fuel Systems: The growing shift toward electric vehicles (EVs), which do not require conventional fuel tanks, poses a long-term challenge to the market.

- Quality and Safety Compliance Across Regions: Ensuring uniform quality standards and meeting varying regional regulatory requirements for plastic fuel tanks can be complex and resource-intensive.

Vehicle Plastic Fuel Tank Systems Market: Report Scope

This report thoroughly analyzes the Vehicle Plastic Fuel Tank Systems Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Vehicle Plastic Fuel Tank Systems Market |

| Market Size in 2023 | USD 23.15 Billion |

| Market Forecast in 2032 | USD 40.14 Billion |

| Growth Rate | CAGR of 6.6% |

| Number of Pages | 196 |

| Key Companies Covered | Kautex Textron GmbH & Co. KG, Plastic Omnium, Magna International Inc., YAPP Automotive Systems Co. Ltd., TI Fluid Systems, Yachiyo Industry Co. Ltd., Inergy Automotive Systems, FTS Co. Ltd., Sakamoto Industry Co. Ltd., Martinrea International Inc., Unipr |

| Segments Covered | By Material Type, By Vehicle Type, By Sales Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Vehicle Plastic Fuel Tank Systems Market: Segmentation Insights

The global vehicle plastic fuel tank systems market is divided by material type, vehicle type, sales channel, and region.

Segmentation Insights by Material Type

Based on material type, the global vehicle plastic fuel tank systems market is divided into high-density polyethylene (HDPE), polypropylene (PP), and others.

In the vehicle plastic fuel tank systems market, High-Density Polyethylene (HDPE) is the most dominant material type. HDPE is widely preferred due to its excellent chemical resistance, lightweight nature, and high durability under varying environmental conditions. It also offers superior impact resistance and can be easily molded into complex shapes, making it ideal for modern fuel tank designs. Additionally, HDPE supports multi-layer structures that help in reducing hydrocarbon emissions, which aligns with increasingly strict environmental regulations.

Polypropylene (PP) follows HDPE in terms of market share. PP offers good resistance to chemicals and moderate mechanical properties, but it is generally considered slightly inferior to HDPE when it comes to strength and impact resistance. However, PP is lightweight and cost-effective, making it a viable option for certain vehicle applications, especially where cost optimization is a major concern. PP may be more common in smaller or less demanding fuel system components rather than full tank constructions.

Segmentation Insights by Vehicle Type

On the basis of vehicle type, the global vehicle plastic fuel tank systems market is bifurcated into passenger cars, light commercial vehicles, heavy commercial vehicles, and others.

In the vehicle plastic fuel tank systems market, Passenger Cars represent the most dominant segment by vehicle type. This dominance is driven by the sheer volume of passenger car production globally, particularly in regions like Asia-Pacific and Europe. Plastic fuel tanks in passenger cars are favored for their lightweight properties, which contribute to improved fuel efficiency and reduced emissions. Moreover, the flexibility of plastic materials like HDPE allows for better utilization of space in compact car designs, further enhancing their popularity in this segment.

Light Commercial Vehicles (LCVs) follow passenger cars in market share. These vehicles, including vans and small trucks, benefit from plastic fuel tanks due to their need for fuel efficiency and moderate payload capacity. The use of plastic tanks in LCVs helps reduce overall vehicle weight, contributing to operational cost savings and compliance with emission standards. Additionally, manufacturers in this segment are increasingly adopting plastic fuel tank systems to meet regulatory demands and consumer expectations for performance and durability.

Heavy Commercial Vehicles (HCVs) come next, though their adoption of plastic fuel tanks is less widespread. Traditionally, metal tanks have been preferred in this segment due to their strength and capacity to withstand harsh operational environments. However, with advancements in plastic technologies and the push for weight reduction even in heavy-duty applications, the use of plastic tanks is gradually increasing. That said, the transition is slower compared to passenger cars and LCVs.

Segmentation Insights by Sales Channel

On the basis of sales channel, the global vehicle plastic fuel tank systems market is bifurcated into OEM and aftermarket.

In the vehicle plastic fuel tank systems market, the OEM (Original Equipment Manufacturer) segment is the most dominant sales channel. OEMs integrate plastic fuel tanks directly into new vehicle models during the manufacturing process, ensuring that the tanks meet stringent design, safety, and emission standards. The rise in global vehicle production, coupled with growing preferences for lightweight and fuel-efficient components, drives the demand for plastic fuel tanks through OEMs. Additionally, OEMs often collaborate with material suppliers and component manufacturers to develop advanced, multi-layered fuel tank systems tailored to the specifications of modern vehicles, further cementing their dominance in the market.

The Aftermarket segment holds a smaller share in comparison, but it still plays a significant role, especially in regions with older vehicle fleets or high vehicle replacement rates. Aftermarket sales typically involve the replacement of damaged or worn-out fuel tanks, and the demand here is driven by vehicle maintenance trends, repair needs, and the cost-effectiveness of plastic replacements. However, due to the longer lifespan and durability of plastic fuel tanks, the frequency of aftermarket replacements is relatively low, which limits the growth of this segment compared to OEM installations.

Vehicle Plastic Fuel Tank Systems Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the vehicle plastic fuel tank systems market. This dominance is driven by the strong presence of established automobile manufacturers and high demand for lightweight components that enhance fuel efficiency and meet environmental standards. The United States leads the region in terms of adoption, supported by advanced manufacturing technologies, a mature automotive supply chain, and regulatory policies that encourage the use of plastic over metal fuel tanks to reduce vehicle weight and emissions.

Europe ranks second in the market, driven by stringent environmental regulations and a long-standing emphasis on automotive innovation. Countries such as Germany, France, and the United Kingdom are at the forefront, with manufacturers focusing on sustainable and fuel-efficient vehicle technologies. The region’s commitment to reducing carbon emissions, along with a strong export-oriented automotive industry, supports the continuous integration of plastic fuel tank systems in both passenger and commercial vehicles.

Asia-Pacific shows the fastest-growing demand, primarily due to expanding vehicle production in China, India, and Japan. China, in particular, acts as a major contributor with its vast automotive manufacturing base and government initiatives supporting the use of lightweight and efficient components. The region benefits from cost-effective raw materials and labor, making it a strategic hub for global production and export of plastic fuel tanks.

Latin America demonstrates steady growth, supported by increasing automotive production in countries like Brazil and Mexico. The region is gradually transitioning from traditional metal tanks to plastic systems, encouraged by the rising demand for durable and corrosion-resistant fuel tanks. Market expansion is further assisted by foreign investments and the growth of local vehicle assembly operations.

Middle East and Africa remains the least dominant region in the market, though it shows emerging potential in specific areas such as the Gulf countries. While overall vehicle production is limited, rising urbanization and increasing consumer interest in private vehicle ownership are contributing to gradual market development. The uptake of plastic fuel tank systems is still in early stages due to limited local manufacturing and slower adoption of advanced automotive technologies.

Vehicle Plastic Fuel Tank Systems Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the vehicle plastic fuel tank systems market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global vehicle plastic fuel tank systems market include:

- Kautex Textron GmbH & Co. KG

- Plastic Omnium

- Magna International Inc.

- YAPP Automotive Systems Co. Ltd.

- TI Fluid Systems

- Yachiyo Industry Co. Ltd.

- Inergy Automotive Systems

- FTS Co. Ltd.

- Sakamoto Industry Co. Ltd.

- Martinrea International Inc.

- Unipres Corporation

- Donghee Industrial Co. Ltd.

- Futaba Industrial Co. Ltd.

- SABIC

- Kongsberg Automotive

- ABC Group Inc.

- Vibracoustic SE

- Mitsubishi Chemical Corporation

- Calsonic Kansei Corporation

The global vehicle plastic fuel tank systems market is segmented as follows:

By Material Type

- High-Density Polyethylene (HDPE)

- Polypropylene (PP)

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Others

By Sales Channel

- OEM

- Aftermarket

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Vehicle Plastic Fuel Tank Systems

Request Sample

Vehicle Plastic Fuel Tank Systems