Rigid and Hollow Prop-shaft Market Size, Share, and Trends Analysis Report

CAGR :

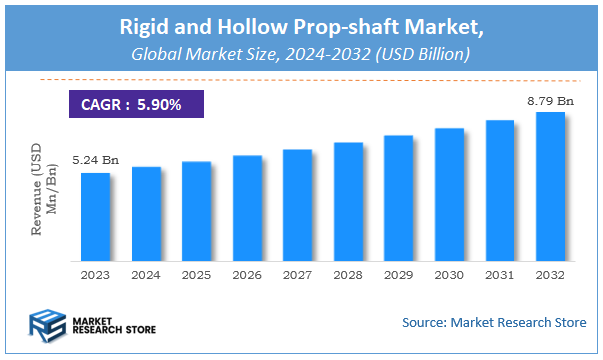

| Market Size 2023 (Base Year) | USD 5.24 Billion |

| Market Size 2032 (Forecast Year) | USD 8.79 Billion |

| CAGR | 5.9% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Rigid and Hollow Prop-shaft Market Insights

According to Market Research Store, the global rigid and hollow prop-shaft market size was valued at around USD 5.24 billion in 2023 and is estimated to reach USD 8.79 billion by 2032, to register a CAGR of approximately 5.9% in terms of revenue during the forecast period 2024-2032.

The rigid and hollow prop-shaft report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Rigid and Hollow Prop-shaft Market: Overview

Rigid and hollow prop-shaft is a critical drivetrain component used primarily in automotive and industrial machinery to transmit torque and rotational power from the engine or transmission to the vehicle’s axle or other driven components. Characterized by its rigid structure and hollow cylindrical design, this type of prop-shaft offers high strength and stiffness while significantly reducing weight compared to solid shafts. The hollow construction enhances the shaft's ability to resist torsional stress and bending forces, contributing to improved performance, fuel efficiency, and reduced vibration in vehicles.

The demand for rigid and hollow prop-shafts is growing due to increasing emphasis on vehicle lightweighting, fuel economy, and enhanced driveline efficiency in the automotive industry. Innovations in materials such as high-strength steel, aluminum alloys, and composite materials have improved the durability and strength-to-weight ratio of these shafts. Additionally, advancements in manufacturing processes like precision machining and friction welding have enabled the production of more reliable and customized prop-shafts tailored to specific vehicle requirements. The trend toward electric and hybrid vehicles is also influencing the design and application of hollow prop-shafts, as manufacturers seek to optimize drivetrain components for new powertrain configurations.

Key Highlights

- The rigid and hollow prop-shaft market is anticipated to grow at a CAGR of 5.9% during the forecast period.

- The global rigid and hollow prop-shaft market was estimated to be worth approximately USD 5.24 billion in 2023 and is projected to reach a value of USD 8.79 billion by 2032.

- The growth of the rigid and hollow prop-shaft market is being driven by the escalating demand for lightweight components in the automotive industry, particularly to meet increasingly stringent fuel efficiency and emissions regulations.

- Based on the type, the rigid prop-shafts segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the automotive segment is projected to swipe the largest market share.

- In terms of material, the metallic materials segment is expected to dominate the market.

- Based on the end-user industry, the transportation segment is expected to dominate the market.

- Based on the component, the universal joints segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Rigid and Hollow Prop-shaft Market: Dynamics

Key Growth Drivers:

- Growing Automotive Production and Sales: The fundamental driver is the consistent global increase in the production and sales of passenger cars, SUVs, and commercial vehicles, especially those with rear-wheel-drive, all-wheel-drive, or four-wheel-drive configurations, which inherently require prop shafts.

- Strict Emission Regulations and Fuel Efficiency Standards: Governments worldwide are imposing increasingly stringent regulations on vehicle emissions and fuel economy. This puts immense pressure on automakers to reduce vehicle weight, making lightweight hollow prop shafts (especially those made from advanced materials) highly attractive to achieve compliance and improve performance.

- Rising Demand for All-Wheel Drive (AWD) and Four-Wheel Drive (4WD) Vehicles: The surging popularity of SUVs and trucks equipped with AWD or 4WD systems, which often utilize multiple prop shafts (e.g., connecting the transfer case to both front and rear differentials), is a significant growth factor for the market.

- Shift Towards Electric Vehicles (EVs) and Hybrid Vehicles: While EV powertrains differ, they still require specialized prop shafts or axle shafts. For EVs, lightweight prop shafts are crucial for extending battery range and optimizing energy consumption. The specific demands of EV powertrains (higher torque, different NVH characteristics) also drive the development of new, high-performance prop shaft designs.

- Advancements in Material Science and Manufacturing: Continuous innovations in materials (e.g., high-strength steel alloys, aluminum, carbon fiber composites) and manufacturing processes enable the production of lighter, stronger, more durable, and corrosion-resistant prop shafts, expanding their application and enhancing their performance.

- Focus on Enhanced Vehicle Performance and Ride Comfort (NVH Reduction): Automakers and consumers alike prioritize improved vehicle dynamics, reduced noise, vibration, and harshness (NVH). Advanced prop shaft designs contribute to a smoother, quieter, and more comfortable ride by minimizing vibrations and balancing dynamic forces.

- Increasing Applications in Industrial Machinery and Marine: Beyond automotive, prop shafts are vital in various industrial and marine applications, including agricultural equipment, construction machinery, and marine propulsion systems. Growth in these sectors further contributes to market demand for robust and reliable prop shafts.

Restraints:

- High Manufacturing Costs for Advanced Materials: While offering significant benefits, prop shafts made from advanced materials like carbon fiber composites have higher manufacturing complexity and costs compared to traditional steel. This can limit their adoption to premium or high-performance vehicle segments.

- Volatility of Raw Material Prices: The prices of essential raw materials such as steel, aluminum, and resins for composites are subject to global market fluctuations. These volatilities can directly impact production costs and profit margins for prop shaft manufacturers, leading to unstable pricing.

- Supply Chain Disruptions and Geographical Concentration: The global automotive supply chain is susceptible to disruptions (e.g., geopolitical tensions, natural disasters, trade policies). Furthermore, the concentration of certain raw material or component suppliers in specific regions can create vulnerabilities for prop shaft manufacturers.

- Technical Challenges in Vibration and Noise Management: As vehicle cabins become quieter, particularly in EVs, even subtle noises and vibrations from the drivetrain become more noticeable. Designing prop shafts that effectively manage NVH across various operating conditions and temperatures remains a continuous engineering challenge.

- Complexity of Design and Testing for Diverse Applications: Prop shafts must be precisely engineered for specific vehicle models and applications, considering factors like length, angle, torque requirements, and critical speed. The extensive design, prototyping, and rigorous testing processes add to development time and cost.

- Limited Aftermarket Standardization: While there's an aftermarket for replacement parts, a lack of universal standardization for prop shaft designs across different vehicle models can make inventory management and replacement challenging for distributors and repair shops.

Opportunities:

- Specialized Prop Shafts for Electric Vehicle Platforms: The unique architecture of EVs, including electric motors and battery placement, creates a significant opportunity for designing completely new, often shorter, lighter, and high-speed prop shafts that can handle the instantaneous torque delivery of electric powertrains. This includes the development of integrated "e-axle" solutions.

- Increased Adoption of Carbon Fiber and Hybrid Composite Prop Shafts: As manufacturing technologies for composites mature and become more cost-effective, there's a significant opportunity for a wider adoption of carbon fiber and hybrid (e.g., steel ends with a composite tube) prop shafts across a broader range of vehicle segments, beyond just luxury or high-performance vehicles.

- Development of "Smart" Prop Shafts with Integrated Sensors: Integrating sensors into prop shafts to monitor real-time parameters like torque, rotational speed, temperature, and vibration can enable predictive maintenance, optimize performance, and contribute to overall vehicle diagnostics within the framework of connected and smart vehicles.

- Modular and Scalable Prop Shaft Designs: As automakers move towards more modular and flexible vehicle platforms, there's an opportunity for prop shaft manufacturers to develop highly adaptable and scalable designs that can be easily customized and integrated across multiple vehicle models, improving manufacturing efficiency and reducing costs.

- Expansion into Emerging Automotive Markets: Rapid urbanization, increasing disposable incomes, and growing vehicle ownership in emerging economies (e.g., Asia-Pacific, Latin America) present substantial opportunities for prop shaft manufacturers to tap into new markets.

- Optimization for Harsh Environments: Developing prop shafts with enhanced corrosion resistance, better sealing, and robust designs for vehicles operating in extreme conditions (e.g., off-road vehicles, military applications, heavy construction machinery) represents a niche, high-value opportunity.

- Advanced Manufacturing Techniques: Opportunities exist in leveraging advanced manufacturing processes like precision forging, hydroforming, and potentially additive manufacturing (for prototypes or specific components) to improve efficiency, reduce waste, and create more complex geometries.

Challenges:

- Navigating the Rapid Evolution of Vehicle Powertrains: The automotive industry is undergoing an unprecedented transformation towards electrification and alternative propulsion. Prop shaft manufacturers face the critical challenge of adapting their product portfolios and investing heavily in R&D to meet the rapidly evolving demands of diverse and new drivetrain architectures (e.g., BEVs, PHEVs, FCEVs).

- Balancing Cost, Weight, and Performance: The continuous pressure from OEMs to deliver lightweight prop shafts while maintaining or improving strength, durability, and NVH characteristics, all within tight cost constraints, is a persistent and complex challenge.

- Global Competitive Landscape and Intellectual Property: The market is characterized by intense competition from established global players and regional manufacturers. Protecting intellectual property rights related to advanced designs and manufacturing processes is crucial to maintain a competitive edge.

- Ensuring Supply Chain Resilience and Regionalization: The industry needs to build more resilient and diversified supply chains to mitigate risks from geopolitical events, trade tensions, and localized disruptions, potentially involving more regionalized manufacturing to reduce reliance on single-source suppliers.

- Attracting and Retaining Specialized Talent: The design, engineering, and manufacturing of advanced prop shafts require highly specialized skills in mechanical engineering, materials science, and production technology. Recruiting and retaining this expert talent remains a significant challenge.

- Integration with Advanced Vehicle Systems: As vehicles become more integrated with complex electronic control units and software, prop shafts (especially "smart" ones) need to seamlessly communicate with other vehicle systems, presenting challenges in software integration, data protocols, and cybersecurity.

- Addressing End-of-Life and Recycling for Composite Prop Shafts: While composites offer weight benefits, their recycling at the end of a vehicle's life can be more challenging and costly than traditional metal shafts, posing an environmental and logistical challenge that the industry needs to address.

Rigid and Hollow Prop-shaft Market: Report Scope

This report thoroughly analyzes the Rigid and Hollow Prop-shaft Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Rigid and Hollow Prop-shaft Market |

| Market Size in 2023 | USD 5.24 Billion |

| Market Forecast in 2032 | USD 8.79 Billion |

| Growth Rate | CAGR of 5.9% |

| Number of Pages | 150 |

| Key Companies Covered | GKN, NTN, SDS, Dana, Nexteer, Hyundai-Wia, IFA Rotorion, Meritor, AAM, Neapco, JTEKT, Yuandong, Wanxiang |

| Segments Covered | By Type, By Application, By Material, By End-User Industry, By Component, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Rigid and Hollow Prop-shaft Market: Segmentation Insights

The global rigid and hollow prop-shaft market is divided by type, application, material, end-user industry, component, and region.

Segmentation Insights by Type

Based on type, the global rigid and hollow prop-shaft market is divided into rigid prop-shafts and hollow prop-shafts.

Rigid Prop-shafts dominate applications rigid and hollow prop-shaft market, particularly in heavy-duty and industrial sectors. Known for their robust construction and ability to handle high torque loads, rigid prop-shafts are commonly employed in heavy-duty vehicles, trucks, and industrial machinery where durability and strength are paramount. These shafts provide reliable power transmission with minimal maintenance requirements, making them ideal for environments involving heavy stress and continuous operation. However, rigid prop-shafts tend to be heavier, which can impact overall vehicle efficiency and fuel consumption.

Hollow Prop-shafts represent a more advanced and increasingly preferred option, especially in sectors emphasizing weight reduction and improved performance. By having a hollow structure, these shafts significantly reduce weight while maintaining comparable strength and torsional rigidity to their rigid counterparts. This weight advantage leads to improved fuel efficiency, reduced rotational inertia, and enhanced vehicle handling characteristics, which are crucial in passenger cars, electric vehicles, and performance-oriented applications. The adoption of hollow prop-shafts is growing rapidly due to advances in materials such as high-strength steel and composites that enhance durability without compromising strength.

Segmentation Insights by Application

On the basis of application, the global rigid and hollow prop-shaft market is bifurcated into automotive and industries.

Automotive applications represent a dominant segment in the rigid and hollow prop-shaft market. Prop-shafts in automotive vehicles are crucial components for transmitting torque from the engine or transmission to the drive wheels, enabling vehicle movement. Both rigid and hollow prop-shafts are utilized in passenger cars, commercial vehicles, and electric vehicles, with hollow prop-shafts increasingly preferred due to their lightweight nature that enhances fuel efficiency and vehicle performance. The growing demand for lightweight vehicles, electric mobility, and stricter emission regulations are driving innovation and adoption of advanced prop-shaft designs in the automotive sector. This sector’s continuous growth, fueled by rising vehicle production and technological advancements, strongly supports the market demand for prop-shafts.

Industries encompass a wide range of applications where rigid and hollow prop-shafts are used in machinery, heavy equipment, and industrial vehicles. These shafts are essential for power transmission in construction equipment, agricultural machinery, mining vehicles, and manufacturing machinery. The focus in industrial applications is often on durability and high torque handling capacity, favoring rigid prop-shafts for their robustness. However, with the industrial sector’s gradual move towards efficiency and weight reduction, hollow prop-shafts are increasingly adopted for their balance of strength and lightweight design. Growth in infrastructure development, industrial automation, and mechanization of agriculture further contributes to the rising demand in this application segment.

Segmentation Insights by Material

On the basis of material, the global rigid and hollow prop-shaft market is bifurcated into metallic materials and non-metallic materials.

Metallic Materials dominate the rigid and hollow prop-shaft market due to their excellent mechanical properties, including high strength, durability, and resistance to fatigue. Common metals used include steel and aluminum alloys, with steel being the most widely used because of its superior load-bearing capacity and cost-effectiveness. Metallic prop-shafts provide reliable performance in demanding automotive and industrial applications, capable of withstanding high torque and harsh operating conditions. Advances in metallurgy have also led to lighter yet stronger metal alloys, which support the growing demand for hollow prop-shafts that offer weight reduction without compromising strength.

Non-metallic Materials in the prop-shaft market are emerging as innovative alternatives aimed at reducing weight and enhancing corrosion resistance. These materials typically include composites such as carbon fiber reinforced polymers (CFRP) and fiberglass. Non-metallic prop-shafts offer significant advantages in terms of lightweight construction, improved fuel efficiency, and resistance to environmental degradation. Although currently representing a smaller share of the market due to higher costs and limited large-scale adoption, non-metallic materials are gaining traction, especially in high-performance automotive sectors and electric vehicles where weight savings translate directly to performance and range benefits.

Segmentation Insights by End-User Industry

On the basis of end-user industry, the global rigid and hollow prop-shaft market is bifurcated into transportation and manufacturing.

Transportation is the dominant end-user industry for rigid and hollow prop-shafts. This sector includes automotive manufacturers producing passenger cars, commercial vehicles, trucks, buses, and electric vehicles. Prop-shafts are critical components for power transmission in these vehicles, enabling efficient transfer of engine torque to the wheels. The transportation industry’s focus on improving fuel efficiency, reducing emissions, and enhancing vehicle performance drives demand for both rigid and hollow prop-shafts. Hollow shafts, in particular, are favored for their lightweight characteristics, which help improve overall vehicle efficiency and meet stringent regulatory standards. Growth in vehicle production globally, especially in emerging economies, continues to propel this segment’s demand.

Manufacturing is another important end-user industry for rigid and hollow prop-shafts, mainly utilizing these components in heavy machinery, industrial equipment, and automation systems. Manufacturing plants employ prop-shafts in conveyors, robotic arms, and power transmission systems where durability and reliability are crucial. This industry often demands robust, high-strength shafts capable of withstanding continuous operation under high loads. While rigid prop-shafts remain prevalent due to their structural integrity, hollow variants are gaining interest to enhance operational efficiency and reduce equipment weight. Expansion in manufacturing sectors worldwide, including automation and industrial modernization, is supporting steady demand from this segment.

Segmentation Insights by Component

On the basis of component, the global rigid and hollow prop-shaft market is bifurcated into universal joints and flange yokes.

Universal Joints segment dominates due to its essential role in allowing angular flexibility and smooth power transmission in rigid and hollow prop-shaft. They provide flexibility to accommodate angular misalignment and movement between connected components, which is essential in automotive and industrial applications where shafts must operate smoothly despite suspension movements or shaft angle variations. Universal joints dominate this segment due to their widespread use across various vehicle types and machinery. Their ability to maintain constant velocity and torque transfer under varying angles makes them indispensable in ensuring reliable power transmission and reducing wear on the drivetrain.

Flange Yokes serve as the connecting interface between the prop-shaft and other drivetrain components, such as the transmission or differential. They provide a secure, rigid mounting point that maintains shaft alignment and supports torque transfer. Flange yokes are typically made from high-strength materials to withstand substantial mechanical stresses. This component segment is crucial in both rigid and hollow prop-shaft systems, offering ease of installation and maintenance. Flange yokes complement universal joints by providing structural integrity and connection stability, ensuring efficient drivetrain operation in automotive and industrial equipment.

Rigid and Hollow Prop-shaft Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the rigid and hollow prop-shaft market due to its mature automotive and aerospace sectors focusing on performance, efficiency, and emission reduction. The rapid growth of electric and hybrid vehicles in the U.S. and Canada is a key driver for hollow prop-shafts, which provide significant weight reduction without compromising strength. The aerospace industry's demand for lightweight and high-strength propulsion components further supports market expansion. Continuous advancements in materials such as carbon fiber composites and aluminum alloys enhance the performance and durability of prop-shafts. Additionally, stringent regulatory standards for vehicle safety and emissions in North America drive manufacturers to adopt innovative prop-shaft designs, making this region the global leader.

Europe is a significant market for rigid and hollow prop-shafts, largely driven by the automotive industry's shift toward electrification and lightweight components. Countries such as Germany, France, and Italy, with their strong automotive manufacturing bases, emphasize the integration of hollow prop-shafts to meet rigorous CO2 emission targets. Aerospace applications, particularly in commercial and defense sectors, also contribute significantly to demand. Europe’s focus on research and development in advanced materials and manufacturing processes supports ongoing innovation. However, challenges such as high production costs and supply chain complexities may temper growth.

Asia-Pacific represents the fastest-growing market segment for rigid and hollow prop-shafts, fueled by expanding automotive production in China, India, Japan, and South Korea. The region's increasing demand for passenger vehicles, commercial trucks, and electric vehicles propels the adoption of lightweight hollow prop-shafts. Rapid industrialization and infrastructural development, especially in emerging economies, further stimulate demand for durable propulsion systems in heavy machinery and commercial vehicles. Despite growth opportunities, fluctuating raw material prices and inconsistent regulations across countries pose challenges. Nevertheless, increasing exports to Western markets and growing local demand support strong market growth.

Latin America experiences steady growth in the prop-shaft market, with Brazil and Mexico as the key contributors. The region's automotive sector is evolving with growing production of commercial vehicles and gradual adoption of hybrid technologies, driving demand for reliable and lightweight prop-shafts. Infrastructure projects in mining, agriculture, and construction sectors also create demand for robust propulsion components. Economic volatility and slower technology adoption remain challenges. Import dependency for advanced components impacts costs, but partnerships and local manufacturing initiatives are helping market development.

Middle East and Africa are emerging markets for rigid and hollow prop-shafts, driven by expanding automotive production and industrial activities. GCC countries invest heavily in infrastructure and transportation, increasing demand for durable propulsion components. South Africa serves as a regional hub for automotive manufacturing, supporting market growth. The mining, construction, and oil & gas sectors further contribute to demand. However, political instability, supply chain issues, and limited advanced manufacturing infrastructure challenge rapid market expansion. Increased foreign investments and focus on electric vehicles are expected to foster growth.

Rigid and Hollow Prop-shaft Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the rigid and hollow prop-shaft market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global rigid and hollow prop-shaft market include:

- GKN

- NTN

- SDS

- Dana

- Nexteer

- Hyundai-Wia

- IFA Rotorion

- Meritor

- AAM

- Neapco

- JTEKT

- Yuandong

- Wanxiang

The global rigid and hollow prop-shaft market is segmented as follows:

By Type

- Rigid Prop-shafts

- Hollow Prop-shafts

By Application

- Automotive and Industries

By Material

- Metallic Materials

- Non-metallic Materials

By End-User Industry

- Transportation

- Manufacturing

By Component

- Universal Joints

- Flange Yokes

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Rigid and Hollow Prop-shaft

Request Sample

Rigid and Hollow Prop-shaft