Aircraft Seating Market Size, Share, and Trends Analysis Report

CAGR :

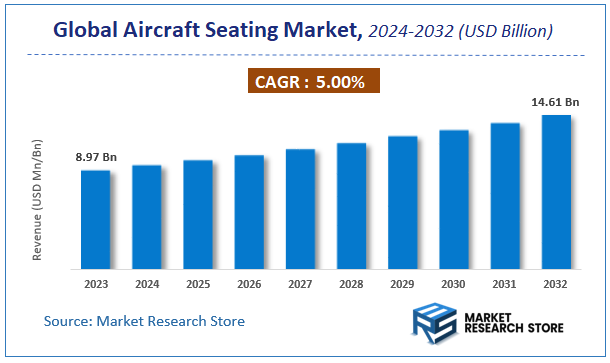

| Market Size 2023 (Base Year) | USD 8.97 Billion |

| Market Size 2032 (Forecast Year) | USD 14.61 Billion |

| CAGR | 5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

According to a recent study by Market Research Store, the global aircraft seating market size was valued at approximately USD 8.97 Billion in 2023. The market is projected to grow significantly, reaching USD 14.61 Billion by 2032, growing at a compound annual growth rate (CAGR) of 5% during the forecast period from 2024 to 2032. The report highlights key growth drivers such as rising demand, technological advancements, and expanding applications. It also outlines potential challenges like regulatory changes and market competition, while emphasizing emerging opportunities for innovation and investment in the aircraft seating industry.

To Get more Insights, Request a Free Sample

Aircraft Seating Market: Overview

The growth of the aircraft seating market is fueled by rising global demand across various industries and applications. The report highlights lucrative opportunities, analyzing cost structures, key segments, emerging trends, regional dynamics, and advancements by leading players to provide comprehensive market insights. The aircraft seating market report offers a detailed industry analysis from 2024 to 2032, combining quantitative and qualitative insights. It examines key factors such as pricing, market penetration, GDP impact, industry dynamics, major players, consumer behavior, and socio-economic conditions. Structured into multiple sections, the report provides a comprehensive perspective on the market from all angles.

Key sections of the aircraft seating market report include market segments, outlook, competitive landscape, and company profiles. Market Segments offer in-depth details based on Component, Class, Aircraft, Standard, End Use, and other relevant classifications to support strategic marketing initiatives. Market Outlook thoroughly analyzes market trends, growth drivers, restraints, opportunities, challenges, Porter’s Five Forces framework, macroeconomic factors, value chain analysis, and pricing trends shaping the market now and in the future. The Competitive Landscape and Company Profiles section highlights major players, their strategies, and market positioning to guide investment and business decisions. The report also identifies innovation trends, new business opportunities, and investment prospects for the forecast period.

Key Highlights:

- As per the analysis shared by our research analyst, the global aircraft seating market is estimated to grow annually at a CAGR of around 5% over the forecast period (2024-2032).

- In terms of revenue, the global aircraft seating market size was valued at around USD 8.97 Billion in 2023 and is projected to reach USD 14.61 Billion by 2032.

- The market is projected to grow at a significant rate due to Rising air passenger traffic and demand for comfort and lightweight seating solutions drive the market.

- Based on the Component, the Structure segment is growing at a high rate and will continue to dominate the global market as per industry projections.

- On the basis of Class, the Business Class segment is anticipated to command the largest market share.

- In terms of Aircraft, the Narrow Body Aircraft segment is projected to lead the global market.

- By Standard, the 9G segment is predicted to dominate the global market.

- Based on the End Use, the OEM segment is expected to swipe the largest market share.

- Based on region, North America is projected to dominate the global market during the forecast period.

Aircraft Seating Market: Report Scope

This report thoroughly analyzes the aircraft seating market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Aircraft Seating Market |

| Market Size in 2023 | USD 8.97 Billion |

| Market Forecast in 2032 | USD 14.61 Billion |

| Growth Rate | CAGR of 5% |

| Number of Pages | 233 |

| Key Companies Covered | Safran Group, RECARO Aircraft Seating GmbH & Co. KG, Jamco Corporation, Thompson Aero Seating, Hong Kong Aircraft Engineering Company Limited, Airbus, RTX Corporation, Expliseat S.A.S., ZIM Aircraft Seating GmbH, Geven SPA, Adient Aerospace LLC, Aviointeriors s.p.a., Mirus Aircraft Seating Ltd, Iacobucci HF Aerospace S.p.A. |

| Segments Covered | By Component, By Class, By Aircraft, By Standard, By End Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Aircraft Seating Market: Dynamics

The Aircraft Seating market is a dynamic and high-value segment within the aviation industry, intricately linked to air travel growth, technological innovation, and evolving passenger expectations.

Key Growth Drivers:

The continuous increase in global air passenger traffic, driven by rising disposable incomes, globalization, and the expansion of tourism, particularly in emerging economies, is the paramount driver. This surge necessitates fleet expansion and new aircraft orders by airlines, directly translating to higher demand for aircraft seats. A significant focus on enhancing passenger comfort and experience, especially on long-haul flights, leads airlines to invest in ergonomic designs, more legroom, adjustable recline, and integrated in-flight entertainment systems. Furthermore, ongoing technological advancements in seat design and materials, such as lightweight composites like carbon fiber, are crucial as they contribute to reduced aircraft weight, improving fuel efficiency for airlines. The growing demand for premium economy and business class seating also drives innovation and higher-value sales.

Restraints:

The market faces significant restraints from the high initial capital investment required for advanced aircraft seats, particularly for premium and first-class cabins, which can be a substantial cost for airlines. The stringent regulatory and certification requirements imposed by aviation authorities (e.g., FAA, EASA) for crashworthiness, fire safety, and overall seat weight, lead to complex and time-consuming testing processes, delaying product introduction and increasing development costs. Disruptions in the global supply chain for specialized materials and components can cause delays in aircraft deliveries and seat manufacturing. Additionally, the fragmented nature of the seat manufacturing sector and the slow recovery from pandemic-related disruptions have contributed to recent seat shortages, further restraining aircraft deliveries.

Opportunities:

Significant opportunities lie in the development of more sustainable and eco-friendly aircraft seating solutions, utilizing recycled, biodegradable, and low-emission materials, aligning with the aviation industry's broader sustainability goals. The integration of smart technologies, such as IoT sensors for real-time seat health monitoring, predictive maintenance, and personalized passenger controls (e.g., via smartphone apps), presents a strong avenue for innovation. The growth of the aftermarket segment, driven by the need for retrofitting older aircraft with newer, more advanced seating to enhance passenger experience and maintain competitiveness, offers a stable revenue stream. Furthermore, the emergence of Urban Air Mobility (UAM) and electric aircraft platforms may open new demands for lightweight, compact, and highly efficient seating designs.

Challenges:

A key challenge is the complexity of aircraft seat manufacturing, which involves thousands of components from numerous global suppliers, making the supply chain highly intricate and susceptible to bottlenecks. Ensuring optimal balance between passenger comfort, seat density for maximizing capacity, and overall aircraft weight to achieve fuel efficiency, remains an ongoing engineering challenge. Manufacturers must continuously innovate to deliver crashworthy and fire-resistant designs that meet stringent safety standards without compromising on aesthetics or cost. Lastly, navigating the cyclical nature of the aviation industry and adapting to fluctuating demand caused by economic downturns or global events (like pandemics) requires robust business strategies.

Aircraft Seating Market: Segmentation Insights

The global aircraft seating market is segmented based on Component, Class, Aircraft, Standard, End Use, and Region. All the segments of the aircraft seating market have been analyzed based on present & future trends and the market is estimated from 2024 to 2032.

Based on Component, the global aircraft seating market is divided into Structure, Foams, Actuators, Electrical Fittings, Others.

On the basis of Class, the global aircraft seating market is bifurcated into Business Class, Economy Class, Premium Economy Class, First Class, Pilot & Crew Seating.

In terms of Aircraft, the global aircraft seating market is categorized into Narrow Body Aircraft, Wide Body Aircraft, Business Jets, Regional Transport Aircraft.

Based on Standard, the global aircraft seating market is split into 9G, 16G, 21G.

By End Use, the global aircraft seating market is divided into OEM, Aftermarket.

Aircraft Seating Market: Regional Insights

The North American region dominates the global aircraft seating market, accounting for the largest market share due to high demand from commercial airlines, strong presence of major aircraft manufacturers (Boeing, Airbus), and increasing fleet modernization programs. According to recent industry reports (2023-2024), North America holds over 35% of the market share, driven by the U.S., which has the highest number of aircraft in service and a robust aftermarket demand for premium and lightweight seating solutions.

The region's growth is further supported by rising air passenger traffic, stringent FAA regulations promoting advanced seating safety, and investments in next-generation aircraft like the Boeing 787 and Airbus A350. Meanwhile, Asia-Pacific is the fastest-growing market, fueled by expanding low-cost carriers and increasing aircraft deliveries in China and India. Europe remains a key player with a focus on luxury and ergonomic seating innovations. However, North America's well-established aerospace ecosystem and high procurement rates solidify its leading position.

Aircraft Seating Market: Competitive Landscape

The aircraft seating market Report offers a thorough analysis of both established and emerging players within the market. It includes a detailed list of key companies, categorized based on the types of products they offer and other relevant factors. The report also highlights the market entry year for each player, providing further context for the research analysis.

The "Global Aircraft Seating Market" study offers valuable insights, focusing on the global market landscape, with an emphasis on major industry players such as;

- Safran Group

- RECARO Aircraft Seating GmbH & Co. KG

- Jamco Corporation

- Thompson Aero Seating

- Hong Kong Aircraft Engineering Company Limited

- Airbus

- RTX Corporation

- Expliseat S.A.S.

- ZIM Aircraft Seating GmbH

- Geven SPA

- Adient Aerospace LLC

- Aviointeriors s.p.a.

- Mirus Aircraft Seating Ltd

- Iacobucci HF Aerospace S.p.A.

The Global Aircraft Seating Market is Segmented as Follows:

By Component

- Structure

- Foams

- Actuators

- Electrical Fittings

- Others

By Class

- Business Class

- Economy Class

- Premium Economy Class

- First Class

- Pilot & Crew Seating

By Aircraft

- Narrow Body Aircraft

- Wide Body Aircraft

- Business Jets

- Regional Transport Aircraft

By Standard

- 9G

- 16G

- 21G

By End Use

- OEM

- Aftermarket

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Market Evolution

This section evaluates the market position of the product or service by examining its development pathway and competitive dynamics. It provides a detailed overview of the product's growth stages, including the early (historical) phase, the mid-stage, and anticipated future advancements influenced by innovation and emerging technologies.

Porter’s Analysis

Porter’s Five Forces framework offers a strategic lens for assessing competitor behavior and the positioning of key players in the aircraft seating industry. This section explores the external factors shaping competitive dynamics and influencing market strategies in the years ahead. The analysis focuses on five critical forces:

- Competitive Rivalry

- Threat of New Entrants

- Threat of Substitutes

- Supplier Bargaining Power

- Buyer Bargaining Power

Value Chain & Market Attractiveness Analysis

The value chain analysis helps businesses optimize operations by mapping the product flow from suppliers to end consumers, identifying opportunities to streamline processes and gain a competitive edge. Segment-wise market attractiveness analysis evaluates key dimensions like product categories, demographics, and regions, assessing growth potential, market size, and profitability. This enables businesses to focus resources on high-potential segments for better ROI and long-term value.

PESTEL Analysis

PESTEL analysis is a powerful tool in market research reports that enhances market understanding by systematically examining the external macro-environmental factors influencing a business or industry. The acronym stands for Political, Economic, Social, Technological, Environmental, and Legal factors. By evaluating these dimensions, PESTEL analysis provides a comprehensive overview of the broader context within which a market operates, helping businesses identify potential opportunities and threats.

- Political factors assess government policies, stability, trade regulations, and political risks that could impact market operations.

- Economic factors examine variables like inflation, exchange rates, economic growth, and consumer spending power to determine market viability.

- Social factors explore cultural trends, demographics, and lifestyle changes that shape consumer behavior and preferences.

- Technological factors evaluate innovation, R&D, and technological advancements affecting product development and operational efficiencies.

- Environmental factors focus on sustainability, climate change impacts, and eco-friendly practices shaping market trends.

- Legal factors address compliance requirements, industry regulations, and intellectual property laws impacting market entry and operations.

Import-Export Analysis & Pricing Analysis

An import-export analysis is vital for market research, revealing global trade dynamics, trends, and opportunities. It examines trade volumes, product categories, and regional competitiveness, offering insights into supply chains and market demand. This section also analyzes past and future pricing trends, helping businesses optimize strategies and enabling consumers to assess product value effectively.

Aircraft Seating Market: Company Profiles

The report identifies key players in the aircraft seating market through a competitive landscape and company profiles, evaluating their offerings, financial performance, strategies, and market positioning. It includes a SWOT analysis of the top 3-5 companies, assessing strengths, weaknesses, opportunities, and threats. The competitive landscape highlights rankings, recent activities (mergers, acquisitions, partnerships, product launches), and regional footprints using the Ace matrix. Customization is available to meet client-specific needs.

Regional & Industry Footprint

This section details the geographic reach, sales networks, and market penetration of companies profiled in the aircraft seating report, showcasing their operations and distribution across regions. It analyzes the alignment of companies with specific industry verticals, highlighting the industries they serve and the scope of their products and services within those sectors.

Ace Matrix

This section categorizes companies into four distinct groups—Active, Cutting Edge, Innovator, and Emerging—based on their product and business strategies. The evaluation of product strategy focuses on aspects such as the range and depth of offerings, commitment to innovation, product functionalities, and scalability. Key elements like global reach, sector coverage, strategic acquisitions, and long-term growth plans are considered for business strategy. This analysis provides a detailed view of companies' position within the market and highlights their potential for future growth and development.

Research Methodology

The qualitative and quantitative insights for the aircraft seating market are derived through a multi-faceted research approach, combining input from subject matter experts, primary research, and secondary data sources. Primary research includes gathering critical information via face-to-face or telephonic interviews, surveys, questionnaires, and feedback from industry professionals, key opinion leaders (KOLs), and customers. Regular interviews with industry experts are conducted to deepen the analysis and reinforce the existing data, ensuring a robust and well-rounded market understanding.

Secondary research for this report was carried out by the Market Research Store team, drawing on a variety of authoritative sources, such as:

- Official company websites, annual reports, financial statements, investor presentations, and SEC filings

- Internal and external proprietary databases, as well as relevant patent and regulatory databases

- Government publications, national statistical databases, and industry-specific market reports

- Media coverage, including news articles, press releases, and webcasts about market participants

- Paid industry databases for detailed market insights

Market Research Store conducted in-depth consultations with various key opinion leaders in the industry, including senior executives from top companies and regional leaders from end-user organizations. This effort aimed to gather critical insights on factors such as the market share of dominant brands in specific countries and regions, along with pricing strategies for products and services.

To determine total sales data, the research team conducted primary interviews across multiple countries with influential stakeholders, including:

- Distributors

- Marketing, Brand, and Product Managers

- Procurement and Production Managers

- Sales and Regional Sales Managers, Country Managers

- Technical Specialists

- C-Level Executives

These subject matter experts, with their extensive industry experience, helped validate and refine the findings. For secondary research, data were sourced from a wide range of materials, including online resources, company annual reports, industry publications, research papers, association reports, and government websites. These various sources provide a comprehensive and well-rounded perspective on the market.

Frequently Asked Questions

Table Of Content

Global Aircraft Seating Industry Market Research Report 1 Aircraft Seating Introduction and Market Overview 1.1 Objectives of the Study 1.2 Definition of Aircraft Seating 1.3 Aircraft Seating Market Scope and Market Size Estimation 1.3.1 Market Concentration Ratio and Market Maturity Analysis 1.3.2 Global Aircraft Seating Value ($) and Growth Rate from 2013-2023 1.4 Market Segmentation 1.4.1 Types of Aircraft Seating 1.4.2 Applications of Aircraft Seating 1.4.3 Research Regions 1.4.3.1 North America Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.4.3.2 Europe Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.4.3.3 China Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.4.3.4 Japan Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.4.3.5 Middle East & Africa Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.4.3.6 India Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.4.3.7 South America Aircraft Seating Production Value ($) and Growth Rate (2013-2018) 1.5 Market Dynamics 1.5.1 Drivers 1.5.1.1 Emerging Countries of Aircraft Seating 1.5.1.2 Growing Market of Aircraft Seating 1.5.2 Limitations 1.5.3 Opportunities 1.6 Industry News and Policies by Regions 1.6.1 Industry News 1.6.2 Industry Policies 2 Industry Chain Analysis 2.1 Upstream Raw Material Suppliers of Aircraft Seating Analysis 2.2 Major Players of Aircraft Seating 2.2.1 Major Players Manufacturing Base and Market Share of Aircraft Seating in 2017 2.2.2 Major Players Product Types in 2017 2.3 Aircraft Seating Manufacturing Cost Structure Analysis 2.3.1 Production Process Analysis 2.3.2 Manufacturing Cost Structure of Aircraft Seating 2.3.3 Raw Material Cost of Aircraft Seating 2.3.4 Labor Cost of Aircraft Seating 2.4 Market Channel Analysis of Aircraft Seating 2.5 Major Downstream Buyers of Aircraft Seating Analysis 3 Global Aircraft Seating Market, by Type 3.1 Global Aircraft Seating Value ($) and Market Share by Type (2013-2018) 3.2 Global Aircraft Seating Production and Market Share by Type (2013-2018) 3.3 Global Aircraft Seating Value ($) and Growth Rate by Type (2013-2018) 3.4 Global Aircraft Seating Price Analysis by Type (2013-2018) 4 Aircraft Seating Market, by Application 4.1 Global Aircraft Seating Consumption and Market Share by Application (2013-2018) 4.2 Downstream Buyers by Application 4.3 Global Aircraft Seating Consumption and Growth Rate by Application (2013-2018) 5 Global Aircraft Seating Production, Value ($) by Region (2013-2018) 5.1 Global Aircraft Seating Value ($) and Market Share by Region (2013-2018) 5.2 Global Aircraft Seating Production and Market Share by Region (2013-2018) 5.3 Global Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.4 North America Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.5 Europe Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.6 China Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.7 Japan Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.8 Middle East & Africa Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.9 India Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 5.10 South America Aircraft Seating Production, Value ($), Price and Gross Margin (2013-2018) 6 Global Aircraft Seating Production, Consumption, Export, Import by Regions (2013-2018) 6.1 Global Aircraft Seating Consumption by Regions (2013-2018) 6.2 North America Aircraft Seating Production, Consumption, Export, Import (2013-2018) 6.3 Europe Aircraft Seating Production, Consumption, Export, Import (2013-2018) 6.4 China Aircraft Seating Production, Consumption, Export, Import (2013-2018) 6.5 Japan Aircraft Seating Production, Consumption, Export, Import (2013-2018) 6.6 Middle East & Africa Aircraft Seating Production, Consumption, Export, Import (2013-2018) 6.7 India Aircraft Seating Production, Consumption, Export, Import (2013-2018) 6.8 South America Aircraft Seating Production, Consumption, Export, Import (2013-2018) 7 Global Aircraft Seating Market Status and SWOT Analysis by Regions 7.1 North America Aircraft Seating Market Status and SWOT Analysis 7.2 Europe Aircraft Seating Market Status and SWOT Analysis 7.3 China Aircraft Seating Market Status and SWOT Analysis 7.4 Japan Aircraft Seating Market Status and SWOT Analysis 7.5 Middle East & Africa Aircraft Seating Market Status and SWOT Analysis 7.6 India Aircraft Seating Market Status and SWOT Analysis 7.7 South America Aircraft Seating Market Status and SWOT Analysis 8 Competitive Landscape 8.1 Competitive Profile 8.2 Stelia Aerospace 8.2.1 Company Profiles 8.2.2 Aircraft Seating Product Introduction 8.2.3 Stelia Aerospace Production, Value ($), Price, Gross Margin 2013-2018E 8.2.4 Stelia Aerospace Market Share of Aircraft Seating Segmented by Region in 2017 8.3 Thompson Aero 8.3.1 Company Profiles 8.3.2 Aircraft Seating Product Introduction 8.3.3 Thompson Aero Production, Value ($), Price, Gross Margin 2013-2018E 8.3.4 Thompson Aero Market Share of Aircraft Seating Segmented by Region in 2017 8.4 Aviointeriors 8.4.1 Company Profiles 8.4.2 Aircraft Seating Product Introduction 8.4.3 Aviointeriors Production, Value ($), Price, Gross Margin 2013-2018E 8.4.4 Aviointeriors Market Share of Aircraft Seating Segmented by Region in 2017 8.5 B/E Aerospace 8.5.1 Company Profiles 8.5.2 Aircraft Seating Product Introduction 8.5.3 B/E Aerospace Production, Value ($), Price, Gross Margin 2013-2018E 8.5.4 B/E Aerospace Market Share of Aircraft Seating Segmented by Region in 2017 8.6 Haeco 8.6.1 Company Profiles 8.6.2 Aircraft Seating Product Introduction 8.6.3 Haeco Production, Value ($), Price, Gross Margin 2013-2018E 8.6.4 Haeco Market Share of Aircraft Seating Segmented by Region in 2017 8.7 Acro Aircraft Seating 8.7.1 Company Profiles 8.7.2 Aircraft Seating Product Introduction 8.7.3 Acro Aircraft Seating Production, Value ($), Price, Gross Margin 2013-2018E 8.7.4 Acro Aircraft Seating Market Share of Aircraft Seating Segmented by Region in 2017 8.8 Geven 8.8.1 Company Profiles 8.8.2 Aircraft Seating Product Introduction 8.8.3 Geven Production, Value ($), Price, Gross Margin 2013-2018E 8.8.4 Geven Market Share of Aircraft Seating Segmented by Region in 2017 8.9 Recaro 8.9.1 Company Profiles 8.9.2 Aircraft Seating Product Introduction 8.9.3 Recaro Production, Value ($), Price, Gross Margin 2013-2018E 8.9.4 Recaro Market Share of Aircraft Seating Segmented by Region in 2017 8.10 PAC 8.10.1 Company Profiles 8.10.2 Aircraft Seating Product Introduction 8.10.3 PAC Production, Value ($), Price, Gross Margin 2013-2018E 8.10.4 PAC Market Share of Aircraft Seating Segmented by Region in 2017 8.11 ZIM Flugsitz 8.11.1 Company Profiles 8.11.2 Aircraft Seating Product Introduction 8.11.3 ZIM Flugsitz Production, Value ($), Price, Gross Margin 2013-2018E 8.11.4 ZIM Flugsitz Market Share of Aircraft Seating Segmented by Region in 2017 8.12 Zodiac Aerospace 8.12.1 Company Profiles 8.12.2 Aircraft Seating Product Introduction 8.12.3 Zodiac Aerospace Production, Value ($), Price, Gross Margin 2013-2018E 8.12.4 Zodiac Aerospace Market Share of Aircraft Seating Segmented by Region in 2017 9 Global Aircraft Seating Market Analysis and Forecast by Type and Application 9.1 Global Aircraft Seating Market Value ($) & Volume Forecast, by Type (2018-2023) 9.1.1 Economy Class Seat Market Value ($) and Volume Forecast (2018-2023) 9.1.2 Business Class Seat Market Value ($) and Volume Forecast (2018-2023) 9.1.3 First Class Seat Market Value ($) and Volume Forecast (2018-2023) 9.2 Global Aircraft Seating Market Value ($) & Volume Forecast, by Application (2018-2023) 9.2.1 Private aircraft Market Value ($) and Volume Forecast (2018-2023) 9.2.2 Military aircraft Market Value ($) and Volume Forecast (2018-2023) 9.2.3 Commercial Aircraft Market Value ($) and Volume Forecast (2018-2023) 10 Aircraft Seating Market Analysis and Forecast by Region 10.1 North America Market Value ($) and Consumption Forecast (2018-2023) 10.2 Europe Market Value ($) and Consumption Forecast (2018-2023) 10.3 China Market Value ($) and Consumption Forecast (2018-2023) 10.4 Japan Market Value ($) and Consumption Forecast (2018-2023) 10.5 Middle East & Africa Market Value ($) and Consumption Forecast (2018-2023) 10.6 India Market Value ($) and Consumption Forecast (2018-2023) 10.7 South America Market Value ($) and Consumption Forecast (2018-2023) 11 New Project Feasibility Analysis 11.1 Industry Barriers and New Entrants SWOT Analysis 11.2 Analysis and Suggestions on New Project Investment 12 Research Finding and Conclusion 13 Appendix 13.1 Discussion Guide 13.2 Knowledge Store: Maia Subscription Portal 13.3 Research Data Source 13.4 Research Assumptions and Acronyms Used

Inquiry For Buying

Aircraft Seating

Request Sample

Aircraft Seating