Food Automation Market Size, Share, and Trends Analysis Report

CAGR :

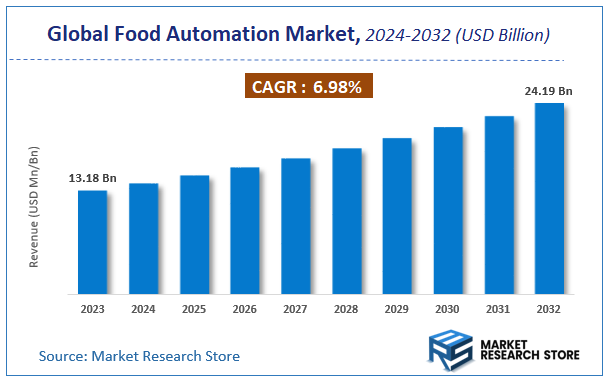

| Market Size 2023 (Base Year) | USD 13.18 Billion |

| Market Size 2032 (Forecast Year) | USD 24.19 Billion |

| CAGR | 6.98% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Food Automation Market Insights

According to Market Research Store, the global food automation market size was valued at around USD 13.18 billion in 2023 and is estimated to reach USD 24.19 billion by 2032, to register a CAGR of approximately 6.98% in terms of revenue during the forecast period 2024-2032.

The food automation report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Food Automation Market: Overview

Food automation refers to the integration of advanced machinery, robotics, and intelligent software systems into the processes of food production, processing, packaging, and distribution to improve efficiency, consistency, and safety. This includes the use of automated equipment for tasks such as sorting, slicing, mixing, cooking, filling, labeling, palletizing, and quality inspection. Automation in the food industry also involves digital technologies like artificial intelligence (AI), machine vision, and the Internet of Things (IoT), which enable real-time monitoring, predictive maintenance, and data-driven decision-making across production lines.

The growth of food automation is driven by several key factors, including the rising demand for higher productivity, improved hygiene standards, and reduced dependency on manual labor. With increasing consumer expectations for consistent quality, customized products, and faster delivery, manufacturers are investing in automated solutions to streamline operations and minimize human error.

Key Highlights

- The food automation market is anticipated to grow at a CAGR of 6.98% during the forecast period.

- The global food automation market was estimated to be worth approximately USD 13.18 billion in 2023 and is projected to reach a value of USD 24.19 billion by 2032.

- The growth of the food automation market is being driven by the rising demand for efficiency, consistency, and safety in food production and processing, alongside increasing labor costs and shortages across the global food industry.

- Based on the automation technology type, the robotic process automation (RPA) segment is growing at a high rate and is projected to dominate the market.

- On the basis of end-user applications, the food processing segment is projected to swipe the largest market share.

- In terms of product type, the packaged foods segment is expected to dominate the market.

- Based on the scale of automation, the fully automated systems segment is expected to dominate the market.

- In terms of deployment mode, the on-premises automation segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Food Automation Market: Dynamics

Key Growth Drivers:

- Growing Emphasis on Food Safety and Quality: Stringent food safety regulations and heightened consumer awareness about foodborne illnesses are a primary driver. Automated systems, equipped with sensors and machine vision, can perform real-time inspections and quality checks with greater accuracy and consistency than human workers, minimizing contamination risks and ensuring compliance.

- Persistent Labor Shortages and Rising Labor Costs: The food industry, particularly in processing and packaging, faces a chronic shortage of manual labor and rising wages. Automation addresses this challenge by taking over repetitive, labor-intensive tasks, thereby increasing productivity, reducing operational costs, and allowing companies to maintain production levels in the face of workforce limitations.

- Increasing Demand for Processed and Ready-to-Eat Foods: Changing consumer lifestyles, urbanization, and a growing middle class are fueling the demand for packaged, processed, and ready-to-eat food products. Automation is essential for meeting this demand by enabling high-speed, high-volume production lines that ensure consistency and efficiency in a mass-market environment.

Restraints:

- High Initial Capital Investment: The high cost of acquiring, installing, and integrating sophisticated automation equipment, such as industrial robots and complex software systems, is a significant barrier to entry, particularly for small and medium-sized enterprises (SMEs). This large upfront investment can make it difficult to justify the move to automation without a guaranteed and quick return on investment.

- Complexity and Diversity of Food Products: Food products often have irregular shapes, textures, and are highly perishable, making them difficult for traditional robots to handle without damage. The sheer diversity of food items requires highly specialized and adaptable automation solutions, which adds to the complexity and cost of implementation.

- Integration Challenges with Legacy Systems: Many established food processing plants operate with a mix of old and new machinery and legacy control systems. Integrating modern automation technology with these disparate systems can be a complex and time-consuming process, leading to compatibility issues and potential production downtime.

Opportunities:

- Customized and Flexible Solutions for a Diverse Market: There is a significant opportunity to develop more flexible and customizable automation solutions that can adapt to changing consumer preferences and production needs. This includes modular robotics and software that can be easily reprogrammed for new products or different packaging sizes, allowing businesses to be more agile in a dynamic market.

- Expansion in Emerging Markets: As developing economies in regions like Asia-Pacific and Latin America experience urbanization, rising incomes, and a demand for modern food products, there is a vast, untapped market for food automation. These regions can leverage new technologies to build modern food processing infrastructure from the ground up, bypassing the legacy systems of developed nations.

- Focus on AI-Powered Predictive Maintenance and Analytics: Beyond just automation, the market has an opportunity to offer advanced software that uses AI and machine learning for predictive maintenance. By analyzing data from sensors, these systems can forecast equipment failures before they happen, minimizing unplanned downtime and significantly improving overall operational efficiency and profitability.

Challenges:

- Ensuring Data Security and Protecting Intellectual Property: As food automation systems become more connected and data-driven, they also become more vulnerable to cyber threats. Protecting sensitive data, including proprietary recipes, production processes, and operational details, from cyberattacks is a continuous and critical challenge for the industry.

- The "Black Box" of AI-Based Systems: The increasing use of AI in food automation can create a "black box" problem, where the reasoning behind a machine's decision (e.g., rejecting a food item for quality reasons) is not transparent. For companies that need to be accountable for their production processes, this lack of explainability can be a major challenge.

- Standardization and Interoperability: A lack of standardization between different manufacturers' hardware and software can create interoperability issues. For a system to be truly effective, the various components from robots to sensors and control software must be able to communicate seamlessly, which requires a collaborative and open ecosystem.

Food Automation Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Food Automation Market |

| Market Size in 2023 | USD 13.18 Billion |

| Market Forecast in 2032 | USD 24.19 Billion |

| Growth Rate | CAGR of 6.98% |

| Number of Pages | 165 |

| Key Companies Covered | Mitsubishi Electric, Emerson Electric, Kollmorgen, McEnery Automation, GEA Group, Rockwell Automation, Rexnord Corporation, Fortive, Premier Automation, Olympus Automation, Schneider Electric, FANUC CORPORATION, FMI, Matrix Technologies, Benchmark, Siemens, and ABB among others. |

| Segments Covered | By Offering, By Food Industry Type, By Application, By End-User, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Food Automation Market: Segmentation Insights

The global food automation market is divided by automation technology type, end-user applications, product type, scale of automation, deployment mode, and region.

Based on automation technology type, the global food automation market is divided into robotic process automation (RPA), industrial robots, artificial intelligence (AI) systems, machine vision systems, and automated guided vehicles (AGVs). Robotic Process Automation (RPA) dominates the Food Automation Market as it offers streamlined, consistent, and high-speed execution of repetitive tasks such as packaging, labeling, sorting, and palletizing. RPA plays a pivotal role in reducing operational costs and minimizing human error in food processing and handling environments. Its integration with programmable logic controllers (PLCs) and real-time monitoring systems has enabled food manufacturers to scale production while maintaining hygiene and efficiency standards. The increasing adoption of RPA across bakery, dairy, meat, and ready-to-eat food segments is largely driven by its ease of integration, cost-effectiveness, and its role in achieving lean manufacturing objectives.

On the basis of end-user applications, the global food automation market is bifurcated into food processing, food packaging, food safety and quality control, warehouse and logistics automation, and inventory management. Food Processing represents the dominant segment in the Food Automation Market, driven by the need for consistent quality, scalability, and efficiency in manufacturing food products. Automation technologies in food processing are deployed for cutting, mixing, sorting, washing, cooking, and pasteurizing operations. Automated systems reduce human contact, thus enhancing food safety while maintaining productivity across continuous and batch processing lines. As consumer demand grows for ready-to-eat and processed food items, manufacturers are investing heavily in advanced robotics, programmable logic controllers (PLCs), and AI-driven process monitoring to ensure high throughput and minimal downtime.

In terms of product type, the global food automation market is bifurcated into packaged foods, fresh foods, beverages, frozen foods, and prepared foods. Packaged Foods dominate the Food Automation Market due to their high demand, longer shelf life, and standardized production processes that are ideal for automation. Automation technologies are heavily utilized in tasks such as filling, sealing, labeling, and quality inspection of packaged goods like snacks, ready-to-eat meals, baked items, and canned foods. As consumers increasingly seek convenience and hygiene in food consumption, manufacturers are adopting robotics, machine vision systems, and real-time quality control to improve packaging speed, accuracy, and safety. This segment also benefits from innovations in sustainable packaging, traceability, and regulatory compliance, all of which are enhanced through automation.

On the basis of scale of automation, the global food automation market is bifurcated into fully automated systems, partially automated systems, manual systems with automation support, smart food production lines, and flexible automation solutions. Fully Automated Systems dominate the Food Automation Market owing to their efficiency, consistency, and ability to handle large-scale production with minimal human intervention. These systems encompass integrated robotics, AI-powered process controls, machine vision, and real-time monitoring technologies that execute end-to-end operations from raw material handling to packaging and storage. Fully automated lines are especially prevalent in high-throughput environments like packaged food and beverage production, where speed, precision, and hygiene are critical. The demand for such systems is driven by rising labor costs, stringent food safety regulations, and the growing need for operational scalability and digital traceability across supply chains.

In terms of deployment mode, the global food automation market is bifurcated into on-premises automation, cloud-based automation, hybrid automation solutions, edge computing automation, and IoT-enabled automation systems. On-Premises Automation dominates the Food Automation Market due to its strong suitability for real-time, high-precision operations that require immediate responsiveness and data processing within the facility. These systems are physically housed within the manufacturing plant and offer full control over data security, system customization, and network reliability. On-premises automation is widely preferred in large-scale food production and packaging environments, where latency-sensitive applications such as industrial robotics, vision systems, and safety compliance must be closely managed. Moreover, regulatory constraints and internal IT policies in the food industry further strengthen the adoption of this deployment model.

Food Automation Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the food automation market due to its early adoption of advanced manufacturing technologies and strong presence of automated food processing industries. The United States, in particular, has witnessed widespread integration of robotics, vision systems, and programmable logic controllers (PLCs) across meat processing, dairy, bakery, and packaged food production segments. The increasing demand for processed and convenience foods, along with stringent food safety regulations enforced by agencies such as the FDA and USDA, has compelled manufacturers to invest in automation solutions that enhance traceability, precision, and hygiene. Furthermore, the region's acute labor shortages in food manufacturing and a strong focus on operational efficiency are accelerating the shift toward fully automated facilities, making North America the leading contributor to market revenue.

Asia-Pacific is experiencing the fastest growth in the food automation market, driven by rapid urbanization, rising disposable incomes, and increasing demand for packaged and processed foods in countries such as China, India, Japan, South Korea, and Australia. In China and Japan, food manufacturers are investing heavily in robotics and smart automation to improve food quality, meet export standards, and address workforce aging and shortages. India’s food processing sector, supported by government initiatives like “Make in India” and the establishment of mega food parks, is adopting automation gradually, especially in large-scale dairy and confectionery industries. Moreover, the expanding middle-class population and changing dietary habits in Southeast Asia are creating opportunities for automated systems in food handling, packaging, and sorting.

Europe holds a significant share of the global food automation market, supported by a highly industrialized food and beverage sector and a growing emphasis on sustainable, high-quality food production. Countries like Germany, France, Italy, and the Netherlands are leading adopters of smart automation in food packaging, sorting, cutting, and quality control. European regulations related to food safety, energy consumption, and waste management are pushing food processors to modernize their operations using robotics, automated inspection systems, and IoT-enabled production lines. The rise of Industry 4.0 across the continent, along with government support for automation in manufacturing, has further fueled investments in food automation technologies, particularly among large-scale food and beverage manufacturers.

Latin America presents moderate growth in the food automation market, with Brazil, Mexico, and Argentina leading the adoption of automated food processing and packaging solutions. Rising demand for hygienically processed foods, improvements in cold chain logistics, and the growth of export-oriented food production are encouraging automation across large food and beverage companies. While small and medium-sized enterprises face challenges due to high initial costs of automation equipment, larger players are implementing robotics and PLCs to improve productivity and reduce labor dependency. The increasing penetration of international food brands and technology providers is also fostering regional market development.

Middle East & Africa region is gradually embracing food automation technologies, especially in the Gulf Cooperation Council (GCC) countries such as the UAE and Saudi Arabia. The region’s food sector is expanding rapidly due to rising demand for convenience foods and growing investments in food security and local food production. Food automation is being adopted in bakery, dairy, and ready-to-eat meal processing to ensure consistent quality and compliance with halal and food safety standards. In Africa, growth remains limited by infrastructure and capital constraints, though countries like South Africa and Egypt are witnessing slow but steady modernization of their food industries. Increasing foreign direct investment (FDI) and public-private partnerships are expected to support future growth in this region.

Food Automation Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the food automation market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global food automation market include:

- Mitsubishi Electric Corporation

- ABB Ltd

- Rockwell Automation Inc

- Siemens AG

- Yokogawa Electric Corporation

- Schneider Electric SE

- GEA Group

- Fortive Corporation

- Yaskawa Electric Corporation

- Rexnord Corporation

- Emerson Electric Co.

- Nord Drivesystems

The global food automation market is segmented as follows:

By Automation Technology Type

- Robotic Process Automation (RPA)

- Industrial Robots

- Artificial Intelligence (AI) Systems

- Machine Vision Systems

- Automated Guided Vehicles (AGVs)

By End-User Applications

- Food Processing

- Food Packaging

- Food Safety and Quality Control

- Warehouse and Logistics Automation

- Inventory Management

By Product Type

- Packaged Foods

- Fresh Foods

- Beverages

- Frozen Foods

- Prepared Foods

By Scale of Automation

- Fully Automated Systems

- Partially Automated Systems

- Manual Systems with Automation Support

- Smart Food Production Lines

- Flexible Automation Solutions

By Deployment Mode

- On-Premises Automation

- Cloud-Based Automation

- Hybrid Automation Solutions

- Edge Computing Automation

- IoT-Enabled Automation Systems

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

CHAPTER 1. Executive Summary 25 CHAPTER 2. Food Automation market – Food Industry Type Analysis 27 2.1. Global Food Automation Market – Food Industry Type Overview 27 2.2. Global Food Automation Market Share, by Food Industry Type, 2018 & 2025 (USD Million) 27 2.3. Dairy 29 2.3.1. Global Dairy Food Automation Market, 2015-2025 (USD Million) 29 2.4. Bakery and Confectionary 30 2.4.1. Global Bakery and Confectionary Food Automation Market, 2015-2025 (USD Million) 30 2.5. Grains and Oils 31 2.5.1. Global Grains and Oils Food Automation Market, 2015-2025 (USD Million) 31 2.6. Meat and Poultry 32 2.6.1. Global Meat and Poultry Food Automation Market, 2015-2025 (USD Million) 32 2.7. Beverages 33 2.7.1. Global Beverages Food Automation Market, 2015-2025 (USD Million) 33 2.8. Meat Substitutes 34 2.8.1. Global Meat Substitutes Food Automation Market, 2015-2025 (USD Million) 34 2.9. Pet Food 35 2.9.1. Global Pet Food Food Automation Market, 2015-2025 (USD Million) 35 2.10. Dairy Alternatives 36 2.10.1. Global Dairy Alternatives Food Automation Market, 2015-2025 (USD Million) 36 CHAPTER 3. Food Automation market – Offerings Analysis 36 3.1. Global Food Automation Market – Offerings Overview 36 3.2. Global Food Automation Market Share, by Offerings, 2018 & 2025 (USD Million) 37 3.3. Solutions 38 3.3.1. Global Solutions Food Automation Market, 2015-2025 (USD Million) 38 3.4. Services 39 3.4.1. Global Services Food Automation Market, 2015-2025 (USD Million) 39 CHAPTER 4. Food Automation market – Application Analysis 39 4.1. Global Food Automation Market – Application Overview 39 4.2. Global Food Automation Market Share, by Application, 2018 & 2025 (USD Million) 40 4.3. Processing 41 4.3.1. Global Processing Food Automation Market, 2015-2025 (USD Million) 41 4.4. Packaging 42 4.4.1. Global Packaging Food Automation Market, 2015-2025 (USD Million) 42 4.5. Palletizing 43 4.5.1. Global Palletizing Food Automation Market, 2015-2025 (USD Million) 43 4.6. Picking 44 4.6.1. Global Picking Food Automation Market, 2015-2025 (USD Million) 44 4.7. Sorting 45 4.7.1. Global Sorting Food Automation Market, 2015-2025 (USD Million) 45 4.8. Biopackaging 46 4.8.1. Global Biopackaging Food Automation Market, 2015-2025 (USD Million) 46 4.9. Others 47 4.9.1. Global Others Food Automation Market, 2015-2025 (USD Million) 47 CHAPTER 5. Food Automation market – End Users Analysis 47 5.1. Global Food Automation Market – End Users Overview 47 5.2. Global Food Automation Market Share, by End Users, 2018 & 2025 (USD Million) 48 5.3. Food Manufacturers 49 5.3.1. Global Food Manufacturers Food Automation Market, 2015-2025 (USD Million) 49 5.4. Logistics Providers 50 5.4.1. Global Logistics Providers Food Automation Market, 2015-2025 (USD Million) 50 5.5. Others 51 5.5.1. Global Others Food Automation Market, 2015-2025 (USD Million) 51 CHAPTER 6. Food Automation market – Regional Analysis 52 6.1. Global Food Automation Market Regional Overview 52 6.2. Global Food Automation Market Share, by Region, 2018 & 2025 (Value) 52 6.3. North America 54 6.3.1. North America Food Automation Market size and forecast, 2015-2025 54 6.3.2. North America Food Automation Market, by Country, 2018 & 2025 (USD Million) 54 6.3.3. North America Food Automation Market, by Food Industry Type, 2015-2025 56 6.3.3.1. North America Food Automation Market, by Food Industry Type, 2015-2025 (USD Million) 56 6.3.4. North America Food Automation Market, by Offerings, 2015-2025 57 6.3.4.1. North America Food Automation Market, by Offerings, 2015-2025 (USD Million) 57 6.3.5. North America Food Automation Market, by Application, 2015-2025 58 6.3.5.1. North America Food Automation Market, by Application, 2015-2025 (USD Million) 58 6.3.6. North America Food Automation Market, by End Users, 2015-2025 59 6.3.6.1. North America Food Automation Market, by End Users, 2015-2025 (USD Million) 59 6.3.7. U.S. 60 6.3.7.1. U.S. Market size and forecast, 2015-2025 (USD Million) 60 6.3.8. Canada 61 6.3.8.1. Canada Market size and forecast, 2015-2025 (USD Million) 61 6.3.9. Mexico 62 6.3.9.1. Mexico Market size and forecast, 2015-2025 (USD Million) 62 6.4. Europe 63 6.4.1. Europe Food Automation Market size and forecast, 2015-2025 63 6.4.2. Europe Food Automation Market, by Country, 2018 & 2025 (USD Million) 63 6.4.3. Europe Food Automation Market, by Food Industry Type, 2015-2025 65 6.4.3.1. Europe Food Automation Market, by Food Industry Type, 2015-2025 (USD Million) 65 6.4.4. Europe Food Automation Market, by Offerings, 2015-2025 66 6.4.4.1. Europe Food Automation Market, by Offerings, 2015-2025 (USD Million) 66 6.4.5. Europe Food Automation Market, by Application, 2015-2025 67 6.4.5.1. Europe Food Automation Market, by Application, 2015-2025 (USD Million) 67 6.4.6. Europe Food Automation Market, by End Users, 2015-2025 68 6.4.6.1. Europe Food Automation Market, by End Users, 2015-2025 (USD Million) 68 6.4.7. Germany 69 6.4.7.1. Germany Market size and forecast, 2015-2025 (USD Million) 69 6.4.8. France 70 6.4.8.1. France Market size and forecast, 2015-2025 (USD Million) 70 6.4.9. U.K. 71 6.4.9.1. U.K. Market size and forecast, 2015-2025 (USD Million) 71 6.4.10. Italy 72 6.4.10.1. Italy Market size and forecast, 2015-2025 (USD Million) 72 6.4.11. Spain 73 6.4.11.1. Spain Market size and forecast, 2015-2025 (USD Million) 73 6.4.12. Nordic Countries 74 6.4.12.1. Nordic Countries Market size and forecast, 2015-2025 (USD Million) 74 6.4.13. Benelux Union 75 6.4.13.1. Benelux Union Market size and forecast, 2015-2025 (USD Million) 75 6.4.14. Rest of Europe 76 6.4.14.1. Rest of Europe Market size and forecast, 2015-2025 (USD Million) 76 6.5. Asia Pacific 77 6.5.1. Asia Pacific Food Automation Market size and forecast, 2015-2025 77 6.5.2. Asia Pacific Food Automation Market, by Country, 2018 & 2025 (USD Million) 77 6.5.3. Asia Pacific Food Automation Market, by Food Industry Type, 2015-2025 79 6.5.3.1. Asia Pacific Food Automation Market, by Food Industry Type, 2015-2025 (USD Million) 79 6.5.4. Asia Pacific Food Automation Market, by Offerings, 2015-2025 80 6.5.4.1. Asia Pacific Food Automation Market, by Offerings, 2015-2025 (USD Million) 80 6.5.5. Asia Pacific Food Automation Market, by Application, 2015-2025 81 6.5.5.1. Asia Pacific Food Automation Market, by Application, 2015-2025 (USD Million) 81 6.5.6. Asia Pacific Food Automation Market, by End Users, 2015-2025 82 6.5.6.1. Asia Pacific Food Automation Market, by End Users, 2015-2025 (USD Million) 82 6.5.7. China 83 6.5.7.1. China Market size and forecast, 2015-2025 (USD Million) 83 6.5.8. Japan 84 6.5.8.1. Japan Market size and forecast, 2015-2025 (USD Million) 84 6.5.9. India 85 6.5.9.1. India Market size and forecast, 2015-2025 (USD Million) 85 6.5.10. New Zealand 86 6.5.10.1. New Zealand Market size and forecast, 2015-2025 (USD Million) 86 6.5.11. Australia 87 6.5.11.1. Australia Market size and forecast, 2015-2025 (USD Million) 87 6.5.12. South Korea 88 6.5.12.1. South Korea Market size and forecast, 2015-2025 (USD Million) 88 6.5.13. South-East Asia 89 6.5.13.1. South-East Asia Market size and forecast, 2015-2025 (USD Million) 89 6.5.14. Rest of Asia Pacific 90 6.5.14.1. Rest of Asia Pacific Market size and forecast, 2015-2025 (USD Million) 90 6.6. Latin America 91 6.6.1. Latin America Food Automation Market size and forecast, 2015-2025 91 6.6.2. Latin America Food Automation Market, by Country, 2018 & 2025 (USD Million) 91 6.6.3. Latin America Food Automation Market, by Food Industry Type, 2015-2025 93 6.6.3.1. Latin America Food Automation Market, by Food Industry Type, 2015-2025 (USD Million) 93 6.6.4. Latin America Food Automation Market, by Offerings, 2015-2025 94 6.6.4.1. Latin America Food Automation Market, by Offerings, 2015-2025 (USD Million) 94 6.6.5. Latin America Food Automation Market, by Application, 2015-2025 95 6.6.5.1. Latin America Food Automation Market, by Application, 2015-2025 (USD Million) 95 6.6.6. Latin America Food Automation Market, by End Users, 2015-2025 96 6.6.6.1. Latin America Food Automation Market, by End Users, 2015-2025 (USD Million) 96 6.6.7. Brazil 97 6.6.7.1. Brazil Market size and forecast, 2015-2025 (USD Million) 97 6.6.8. Argentina 98 6.6.8.1. Argentina Market size and forecast, 2015-2025 (USD Million) 98 6.6.9. Rest of Latin America 99 6.6.9.1. Rest of Latin America Market size and forecast, 2015-2025 (USD Million) 99 6.7. The Middle-East and Africa 100 6.7.1. The Middle-East and Africa Food Automation Market size and forecast, 2015-2025 100 6.7.2. The Middle-East and Africa Food Automation Market, by Country, 2018 & 2025 (USD Million) 100 6.7.3. The Middle-East and Africa Food Automation Market, by Food Industry Type, 2015-2025 102 6.7.3.1. The Middle-East and Africa Food Automation Market, by Food Industry Type, 2015-2025 (USD Million) 102 6.7.4. The Middle-East and Africa Food Automation Market, by Offerings, 2015-2025 103 6.7.4.1. The Middle-East and Africa Food Automation Market, by Offerings, 2015-2025 (USD Million) 103 6.7.5. The Middle-East and Africa Food Automation Market, by Application, 2015-2025 104 6.7.5.1. The Middle-East and Africa Food Automation Market, by Application, 2015-2025 (USD Million) 104 6.7.6. The Middle-East and Africa Food Automation Market, by End Users, 2015-2025 105 6.7.6.1. The Middle-East and Africa Food Automation Market, by End Users, 2015-2025 (USD Million) 105 6.7.7. Saudi Arabia 106 6.7.7.1. Saudi Arabia Market size and forecast, 2015-2025 (USD Million) 106 6.7.8. UAE 107 6.7.8.1. UAE Market size and forecast, 2015-2025 (USD Million) 107 6.7.9. Egypt 108 6.7.9.1. Egypt Market size and forecast, 2015-2025 (USD Million) 108 6.7.10. Kuwait 109 6.7.10.1. Kuwait Market size and forecast, 2015-2025 (USD Million) 109 6.7.11. South Africa 110 6.7.11.1. South Africa Market size and forecast, 2015-2025 (USD Million) 110 6.7.12. Rest of Middle-East Africa 111 6.7.12.1. Rest of Middle-East Africa Market size and forecast, 2015-2025 (USD Million) 111 CHAPTER 7. Food Automation market – Competitive Landscape 112 7.1. Competitor Market Share – Revenue 112 7.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players 114 7.3. Strategic Development 115 7.3.1. Acquisitions and Mergers 115 7.3.2. New Products 115 7.3.3. Research & Development Activities 115 CHAPTER 8. Company Profiles 116 8.1. ABB 116 8.1.1. Company Overview 116 8.1.2. ABB Revenue and Gross Margin 116 8.1.3. Product portfolio 117 8.1.4. Recent initiatives 118 8.2. Benchmark 118 8.2.1. Company Overview 118 8.2.2. Benchmark Revenue and Gross Margin 118 8.2.3. Product portfolio 119 8.2.4. Recent initiatives 120 8.3. Emerson Electric Co. 120 8.3.1. Company Overview 120 8.3.2. Emerson Electric Co. Revenue and Gross Margin 120 8.3.3. Product portfolio 121 8.3.4. Recent initiatives 122 8.4. FANUC CORPORATION 122 8.4.1. Company Overview 122 8.4.2. FANUC CORPORATION Revenue and Gross Margin 122 8.4.3. Product portfolio 123 8.4.4. Recent initiatives 124 8.5. FMI 124 8.5.1. Company Overview 124 8.5.2. FMI Revenue and Gross Margin 124 8.5.3. Product portfolio 125 8.5.4. Recent initiatives 126 8.6. Fortive 126 8.6.1. Company Overview 126 8.6.2. Fortive Revenue and Gross Margin 126 8.6.3. Product portfolio 127 8.6.4. Recent initiatives 128 8.7. GEA Group Aktiengesellschaft 128 8.7.1. Company Overview 128 8.7.2. GEA Group Aktiengesellschaft Revenue and Gross Margin 128 8.7.3. Product portfolio 129 8.7.4. Recent initiatives 130 8.8. Kollmorgen 130 8.8.1. Company Overview 130 8.8.2. Kollmorgen Revenue and Gross Margin 130 8.8.3. Product portfolio 131 8.8.4. Recent initiatives 132 8.9. Matrix Technologies , Inc 132 8.9.1. Company Overview 132 8.9.2. Matrix Technologies , Inc Revenue and Gross Margin 132 8.9.3. Product portfolio 133 8.9.4. Recent initiatives 134 8.10. McEnery Automation 134 8.10.1. Company Overview 134 8.10.2. McEnery Automation Revenue and Gross Margin 134 8.10.3. Product portfolio 135 8.10.4. Recent initiatives 136 8.11. Mitsubishi Electric Corporation 136 8.11.1. Company Overview 136 8.11.2. Mitsubishi Electric Corporation Revenue and Gross Margin 136 8.11.3. Product portfolio 137 8.11.4. Recent initiatives 138 8.12. NORD Drivesystems 138 8.12.1. Company Overview 138 8.12.2. NORD Drivesystems Revenue and Gross Margin 138 8.12.3. Product portfolio 139 8.12.4. Recent initiatives 140 8.13. Olympus Automation Ltd. (OAL) 140 8.13.1. Company Overview 140 8.13.2. Olympus Automation Ltd. (OAL) Revenue and Gross Margin 140 8.13.3. Product portfolio 141 8.13.4. Recent initiatives 142 8.14. Premier Automation 142 8.14.1. Company Overview 142 8.14.2. Premier Automation Revenue and Gross Margin 142 8.14.3. Product portfolio 143 8.14.4. Recent initiatives 144 8.15. Rexnord Corporation 144 8.15.1. Company Overview 144 8.15.2. Rexnord Corporation Revenue and Gross Margin 144 8.15.3. Product portfolio 145 8.15.4. Recent initiatives 146 8.16. Rockwell Automation, Inc 146 8.16.1. Company Overview 146 8.16.2. Rockwell Automation, Inc Revenue and Gross Margin 146 8.16.3. Product portfolio 147 8.16.4. Recent initiatives 148 8.17. Schneider Electric 148 8.17.1. Company Overview 148 8.17.2. Schneider Electric Revenue and Gross Margin 148 8.17.3. Product portfolio 149 8.17.4. Recent initiatives 150 8.18. Siemens AG 150 8.18.1. Company Overview 150 8.18.2. Siemens AG Revenue and Gross Margin 150 8.18.3. Product portfolio 151 8.18.4. Recent initiatives 152 CHAPTER 9. Food Automation — Industry Analysis 153 9.1. Food Automation Market – Key Trends 153 9.1.1. Market Drivers 154 9.1.2. Market Restraints 154 9.1.3. Market Opportunities 155 9.2. Value Chain Analysis 156 9.3. Technology Roadmap and Timeline 157 9.4. Food Automation Market – Attractiveness Analysis 158 9.4.1. By Food Industry Type 158 9.4.2. By Offerings 158 9.4.3. By Application 159 9.4.4. By End Users 160 9.4.5. By Region 161 CHAPTER 10. Marketing Strategy Analysis, Distributors 162 10.1. Marketing Channel 162 10.2. Direct Marketing 163 10.3. Indirect Marketing 163 10.4. Marketing Channel Development Trend 163 10.5. Economic/Political Environmental Change 164 CHAPTER 11. Report Conclusion 165 CHAPTER 12. Research Approach & Methodology 166 12.1. Report Description 166 12.2. Research Scope 167 12.3. Research Methodology 167 12.3.1. Secondary Research 168 12.3.2. Primary Research 169 12.3.3. Models 170 12.3.3.1. Company Share Analysis Model 170 12.3.3.2. Revenue Based Modeling 171 12.3.3.3. Research Limitations 171

Inquiry For Buying

Food Automation

Request Sample

Food Automation