Private Hospitals Market Size, Share, and Trends Analysis Report

CAGR :

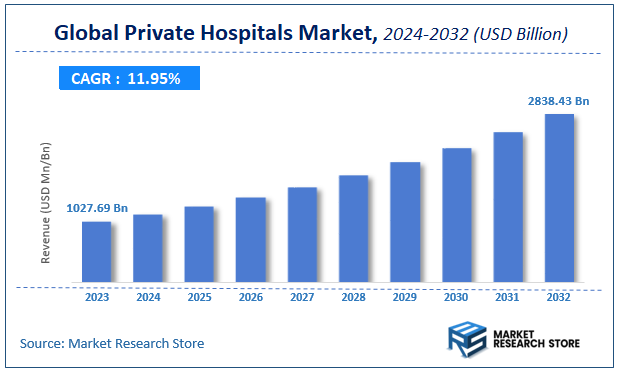

| Market Size 2023 (Base Year) | USD 1027.69 Billion |

| Market Size 2032 (Forecast Year) | USD 2838.43 Billion |

| CAGR | 11.95% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Private Hospitals Market Insights

According to Market Research Store, the global private hospitals market size was valued at around USD 1027.69 billion in 2023 and is estimated to reach USD 2838.43 billion by 2032, to register a CAGR of approximately 11.95% in terms of revenue during the forecast period 2024-2032.

The private hospitals report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Private Hospitals Market: Overview

Private hospitals are healthcare institutions owned and operated by individuals, corporations, or non-profit organizations rather than by government entities. These facilities provide a range of medical services from general care and elective procedures to specialized surgeries and advanced diagnostics often emphasizing personalized attention, reduced wait times, and enhanced amenities. Private hospitals may operate independently or as part of larger healthcare networks and are typically funded through patient fees, private health insurance reimbursements, or direct investment from private entities.

The growth of private hospitals is driven by increasing demand for high-quality, efficient, and accessible healthcare services, particularly in regions where public systems face capacity constraints or quality concerns. Rising income levels, greater health awareness, and expanding medical tourism are also contributing to their expansion. Many private hospitals invest in cutting-edge technology, highly trained staff, and comfortable infrastructure to attract patients seeking superior care experiences. Additionally, the shift toward value-based care and partnerships with digital health platforms is enabling private hospitals to deliver more integrated, outcome-focused services. As healthcare systems worldwide evolve, private hospitals continue to play a vital role in bridging service gaps, fostering innovation, and complementing public sector efforts.

Key Highlights

- The private hospitals market is anticipated to grow at a CAGR of 11.95% during the forecast period.

- The global private hospitals market was estimated to be worth approximately USD 1027.69 billion in 2023 and is projected to reach a value of USD 2838.43 billion by 2032.

- The growth of the private hospitals market is being driven by increasing healthcare expenditure, rising demand for high-quality and personalized medical services, and the expansion of medical tourism.

- Based on the category, the children’s hospital segment is growing at a high rate and is projected to dominate the market.

- On the basis of hospital capacity, the large (>500 beds) segment is projected to swipe the largest market share.

- In terms of location, the rural segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Private Hospitals Market: Dynamics

Key Growth Drivers:

- Growing Middle Class and Rising Disposable Income: As the global middle class expands, particularly in emerging economies, a larger segment of the population can afford private health insurance and out-of-pocket expenses for higher-quality healthcare. This group often prioritizes better facilities, personalized care, and shorter wait times, which are hallmarks of private hospitals.

- Increasing Burden of Chronic and Non-Communicable Diseases (NCDs): The global shift in disease patterns towards lifestyle-related NCDs like diabetes, cardiovascular diseases, and cancer is a major driver. These conditions often require specialized, long-term, and high-tech care, which private hospitals are well-equipped to provide, leading to a sustained demand for their services.

- Expansion of Health Insurance Coverage: The rise in both public and private health insurance penetration is making private hospital care more accessible. As more people are covered by insurance, the financial barrier to accessing private healthcare is reduced, driving a higher volume of patient admissions and treatments in the private sector.

- Medical Tourism: Private hospitals, particularly in developing countries, are capitalizing on the medical tourism trend. They attract international patients seeking high-quality care, specialized treatments (e.g., robotic surgery, transplants), and cost advantages over their home countries. This not only generates significant revenue but also enhances the global reputation of these institutions.

Restraints:

- High Cost of Care and Affordability Concerns: A major restraint is the high cost of treatment in private hospitals, which can make it unaffordable for a large segment of the population, especially in regions with limited health insurance coverage. This can lead to a public perception of private hospitals as being profit-driven and inaccessible, creating a social and ethical dilemma.

- Shortage of Healthcare Professionals: The private hospital sector faces a persistent challenge in attracting and retaining qualified healthcare professionals, such as doctors and nurses. This shortage can be particularly acute in rural areas, where private hospitals struggle to compete with urban centers on salaries and infrastructure, leading to a concentration of resources in major cities.

- Regulatory and Policy Challenges: Private hospitals must navigate a complex and often evolving regulatory environment. This includes complying with government price controls on certain procedures, dealing with a lack of standardized regulations, and managing the administrative burden of public and private insurance schemes. Ambiguities and inconsistencies in policy can make business planning difficult and lead to financial pressures.

- Intense Competition and Market Fragmentation: The private hospital market is highly competitive and fragmented, with numerous providers vying for patients. This can lead to price wars and a constant pressure to invest in the latest technology and facilities to stay competitive. In this environment, smaller private hospitals may find it difficult to survive against larger hospital chains.

Opportunities:

- Technological Integration and Digital Health: There is a significant opportunity for private hospitals to leverage technology to enhance patient care and operational efficiency. This includes adopting AI-driven diagnostics, robotic surgery, telemedicine for remote consultations, and data analytics to optimize patient flow and resource management.

- Expansion into Tier-2 and Tier-3 Cities: Private hospitals have a strong presence in major metropolitan areas, but there is a vast, underserved market in smaller cities and towns. By expanding into these regions, often through asset-light models or public-private partnerships, hospitals can tap into a new customer base and help alleviate the burden on public healthcare systems.

- Specialization and Niche Services: Private hospitals can differentiate themselves by focusing on specialized and high-margin services, such as cardiology, oncology, transplants, and cosmetic surgery. By investing in these niche areas and building a reputation for excellence, they can attract a specific patient demographic and justify higher prices.

- Focus on Wellness, Preventive Care, and Home Healthcare: The healthcare landscape is shifting from a reactive model to a proactive one. Private hospitals can capitalize on this by expanding their services to include wellness programs, preventive health check-ups, and home healthcare. This not only creates new revenue streams but also positions them as partners in their patients' long-term health, not just during illness.

Challenges:

- Balancing Profitability with Quality of Care: A continuous challenge for private hospitals is to balance their business objectives with their ethical responsibility to provide high-quality, patient-centric care. The pressure to maximize revenue can sometimes lead to perceptions of over-treatment or unnecessary procedures, which can damage a hospital's reputation and erode public trust.

- Maintaining Patient Trust and Combating Negative Perceptions: The private sector often faces public scrutiny and criticism, with allegations of overcharging and a lack of transparency. The challenge is to build and maintain patient trust through transparent billing practices, ethical standards, and a demonstrable commitment to quality.

- Cybersecurity and Data Protection: As private hospitals increasingly digitize their operations and integrate electronic health records (EHRs) and connected medical devices, they become more vulnerable to cyberattacks. Protecting sensitive patient data from breaches is a critical and ongoing challenge that requires significant investment in cybersecurity infrastructure.

- Integration with Public Health Systems: In many countries, the private sector operates in parallel to the public health system, with limited collaboration. The challenge is to find ways for private hospitals to work effectively with public systems, for instance, by participating in publicly funded insurance schemes, to improve overall healthcare access and quality without compromising their financial viability.

Private Hospitals Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Private Hospitals Market |

| Market Size in 2023 | USD 1027.69 Billion |

| Market Forecast in 2032 | USD 2838.43 Billion |

| Growth Rate | CAGR of 11.95% |

| Number of Pages | 240 |

| Key Companies Covered | St Francis Foundation, Ramsay Health Care UK,ToulonHyères Private Hospital,Helios,Spire Healthcare Group plc, Cambie Surgery Centre,Hospital Group London Bridge Hospital,Highgate Private Hospital,Deaconesses Croix Saint, HCA Healthcare UK, MEOCLINIC GmbH, Nuffield Health, Shouldice, Premier Healthcare Germany, and Bupa |

| Segments Covered | By Hospital Type, By Size, By Location, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Private Hospitals Market: Segmentation Insights

The global private hospitals market is divided by category, hospital capacity, location, and region.

Based on category, the global private hospitals market is divided into children’s hospital, multispecialty hospitals, acute care hospitals, and specialty hospitals. Children’s Hospitals dominate the Private Hospital Market, driven by the increasing demand for specialized pediatric care and dedicated infrastructure for neonatal and adolescent healthcare. These hospitals focus on treating a wide range of childhood illnesses, genetic disorders, and developmental conditions, often offering services such as pediatric surgery, pediatric oncology, and pediatric intensive care units (PICUs). With rising awareness of child-specific health needs, improvements in pediatric diagnostics, and growing investments in child health programs, children’s hospitals are becoming a crucial component of private healthcare systems, especially in urban and semi-urban regions.

On the basis of hospital capacity, the global private hospitals market is bifurcated into large (>500 beds), medium (100 beds-500 beds), and small (100 beds). Large (>500 Beds) private hospitals dominate the market due to their extensive infrastructure, multidisciplinary care capabilities, and ability to handle a high patient volume. These hospitals typically function as tertiary or quaternary care centers, offering specialized treatments, advanced surgeries, organ transplants, and comprehensive diagnostic services. Large private hospitals also tend to be affiliated with medical colleges or research centers, providing a combination of clinical care, teaching, and innovation. Their presence is especially strong in metropolitan areas and medical tourism hubs, where they attract both domestic and international patients seeking world-class facilities and personalized treatment.

In terms of location, the global private hospitals market is bifurcated into rural and urban. Rural private hospitals dominate the market, owing to the increasing demand for accessible and affordable healthcare services in remote and underserved regions. With limited availability of government medical infrastructure in rural areas, private hospitals play a critical role in addressing the healthcare needs of vast rural populations. These hospitals typically offer essential medical services such as maternal care, emergency treatments, infectious disease management, and general consultations. The dominance of rural hospitals is further driven by government incentives for rural healthcare investment, rising rural incomes, and efforts by private healthcare chains to expand their footprint beyond urban centers. The expansion of telemedicine and mobile health services also supports the efficiency and reach of rural private hospitals, making them a crucial component in national healthcare delivery.

Private Hospitals Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Private Hospitals Market, driven by a high concentration of privately operated healthcare facilities, strong insurance penetration, and an increasing preference for personalized care and shorter wait times. In the United States, major healthcare groups and investor-owned hospital chains control a significant portion of private inpatient and outpatient care, supported by advanced medical technologies and specialist availability. The region also benefits from a favorable reimbursement landscape, competitive consolidation, and a growing elderly population with chronic illnesses, all contributing to increasing demand for private healthcare services. In Canada, although public healthcare is dominant, private facilities are expanding in niche areas like diagnostics, elective procedures, and rehabilitation, marking a gradual but notable rise in the private segment.

Asia-Pacific is the fastest-growing region in the private hospitals market due to rising healthcare expenditure, urbanization, and a growing middle-class population. Countries such as India, China, Japan, South Korea, and Thailand are experiencing a boom in private hospital networks. In India and China, private hospitals dominate tertiary care services and are rapidly expanding through multi-specialty and super-specialty chains, catering to domestic and international patients. Medical tourism is a major growth driver, particularly in Southeast Asian countries like Thailand, Malaysia, and Singapore, where private hospitals offer high-quality, cost-effective treatments. Additionally, increased government encouragement of public-private partnerships in healthcare infrastructure is further fueling private sector expansion.

Europe holds a substantial share of the private hospitals market, with the United Kingdom, Germany, France, and Spain being key contributors. In many European countries, private hospitals operate alongside public systems under dual healthcare models. The private sector thrives especially in elective surgeries, cosmetic procedures, and specialized care. Increasing patient demand for faster access to services, more comfortable settings, and choice of specialists drives the market forward. In countries like Germany and Switzerland, the private hospital segment benefits from supplemental private insurance and high-income populations. Additionally, private healthcare providers in Europe often maintain partnerships with national health services to reduce the burden on public facilities.

Latin America represents a developing region for the private hospitals market, with Brazil, Mexico, Argentina, and Chile leading the sector. In many urban areas, private hospitals offer higher standards of care and reduced wait times compared to public facilities, which face resource limitations. Increasing health insurance coverage, along with growing demand for elective and specialty care, supports the rise of private hospital services. While public hospitals dominate rural healthcare, private institutions in metropolitan regions are expanding in response to rising middle-class expectations and the need for technologically advanced care environments.

Middle East & Africa is experiencing gradual growth in the private hospitals market, driven by increasing investment in healthcare infrastructure and efforts to attract medical tourism. In the Middle East, particularly in the UAE, Saudi Arabia, and Qatar, private hospitals are well-equipped and offer high-end services in areas such as oncology, cardiology, and cosmetic surgery. The presence of international hospital chains and collaborations with global healthcare groups contributes to quality improvement and expansion. In Africa, the private hospital market remains fragmented but is expanding in urban centers where affordability and access are improving. Governments in several countries are promoting private sector participation through reforms and investment incentives.

Private Hospitals Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the private hospitals market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global private hospitals market include:

- Toulon Hyères Private Hospital

- St Francis Foundation

- Deaconesses Croix Saint

- Apollo Hospitals Enterprise Ltd.

- Healthe Care

- Ramsay Health Care

- HCA Healthcare

- Fresenius SE & Co. KGaA

- Nuffield Health

- Fortis Healthcare Limited

- London Bridge Healthcare

- Life Healthcare

- Spire Healthcare Group Plc.

- MEOCLINIC Gmbh

- IASIS Healthcare

- Care UK

- ToulonHyères Private Hospital

- Helios

- Cambie Surgery Centre

- Hospital Group London Bridge Hospital

- Highgate Private Hospital

- Shouldice

- Premier Healthcare Germany

- Bupa

The global private hospitals market is segmented as follows:

By Category

- Children’s Hospital

- Multispecialty Hospitals

- Acute care Hospitals

- Specialty Hospitals

By Hospital Capacity

- Large (>500 beds)

- Medium (100 beds-500 beds)

- Small (100 beds)

By Location

- Rural

- Urban

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

CHAPTER 1. Executive Summary 21 CHAPTER 2. Private Hospitals market – Hospital Type Analysis 23 2.1. Global Private Hospitals Market – Hospital Type Overview 23 2.2. Global Private Hospitals Market Share, by Hospital Type, 2018 & 2025 (USD Billion) 23 2.3. Acute care hospitals 25 2.3.1. Global Acute care hospitals Private Hospitals Market, 2015-2027 (USD Billion) 25 2.4. Children’s hospitals 26 2.4.1. Global Children’s hospitals Private Hospitals Market, 2015-2027 (USD Billion) 26 2.5. Specialty hospitals 27 2.5.1. Global Specialty hospitals Private Hospitals Market, 2015-2027 (USD Billion) 27 2.6. Multispecialty hospitals 28 2.6.1. Global Multispecialty hospitals Private Hospitals Market, 2015-2027 (USD Billion) 28 CHAPTER 3. Private Hospitals market – Size Analysis 28 3.1. Global Private Hospitals Market – Size Overview 28 3.2. Global Private Hospitals Market Share, by Size, 2018 & 2025 (USD Billion) 29 3.3. Small (less 100 beds) 30 3.3.1. Global Small (less 100 beds) Private Hospitals Market, 2015-2027 (USD Billion) 30 3.4. Medium (100 to 500 beds) 31 3.4.1. Global Medium (100 to 500 beds) Private Hospitals Market, 2015-2027 (USD Billion) 31 3.5. Large (more than 500 beds) 32 3.5.1. Global Large (more than 500 beds) Private Hospitals Market, 2015-2027 (USD Billion) 32 CHAPTER 4. Private Hospitals market – Location Analysis 32 4.1. Global Private Hospitals Market – Location Overview 32 4.2. Global Private Hospitals Market Share, by Location, 2018 & 2025 (USD Billion) 33 4.3. Rural 34 4.3.1. Global Rural Private Hospitals Market, 2015-2027 (USD Billion) 34 4.4. Urban 35 4.4.1. Global Urban Private Hospitals Market, 2015-2027 (USD Billion) 35 CHAPTER 5. Private Hospitals market – Regional Analysis 36 5.1. Global Private Hospitals Market Regional Overview 36 5.2. Global Private Hospitals Market Share, by Region, 2018 & 2025 (Value) 36 5.3. North America 38 5.3.1. North America Private Hospitals Market size and forecast, 2015-2027 38 5.3.2. North America Private Hospitals Market, by Country, 2018 & 2025 (USD Billion) 38 5.3.3. North America Private Hospitals Market, by Hospital Type, 2015-2027 40 5.3.3.1. North America Private Hospitals Market, by Hospital Type, 2015-2027 (USD Billion) 40 5.3.4. North America Private Hospitals Market, by Size, 2015-2027 41 5.3.4.1. North America Private Hospitals Market, by Size, 2015-2027 (USD Billion) 41 5.3.5. North America Private Hospitals Market, by Location, 2015-2027 42 5.3.5.1. North America Private Hospitals Market, by Location, 2015-2027 (USD Billion) 42 5.3.6. U.S. 43 5.3.6.1. U.S. Market size and forecast, 2015-2027 (USD Billion) 43 5.3.7. Canada 44 5.3.7.1. Canada Market size and forecast, 2015-2027 (USD Billion) 44 5.3.8. Mexico 45 5.3.8.1. Mexico Market size and forecast, 2015-2027 (USD Billion) 45 5.4. Europe 46 5.4.1. Europe Private Hospitals Market size and forecast, 2015-2027 46 5.4.2. Europe Private Hospitals Market, by Country, 2018 & 2025 (USD Billion) 46 5.4.3. Europe Private Hospitals Market, by Hospital Type, 2015-2027 48 5.4.3.1. Europe Private Hospitals Market, by Hospital Type, 2015-2027 (USD Billion) 48 5.4.4. Europe Private Hospitals Market, by Size, 2015-2027 49 5.4.4.1. Europe Private Hospitals Market, by Size, 2015-2027 (USD Billion) 49 5.4.5. Europe Private Hospitals Market, by Location, 2015-2027 50 5.4.5.1. Europe Private Hospitals Market, by Location, 2015-2027 (USD Billion) 50 5.4.6. Germany 51 5.4.6.1. Germany Market size and forecast, 2015-2027 (USD Billion) 51 5.4.7. France 52 5.4.7.1. France Market size and forecast, 2015-2027 (USD Billion) 52 5.4.8. U.K. 53 5.4.8.1. U.K. Market size and forecast, 2015-2027 (USD Billion) 53 5.4.9. Italy 54 5.4.9.1. Italy Market size and forecast, 2015-2027 (USD Billion) 54 5.4.10. Spain 55 5.4.10.1. Spain Market size and forecast, 2015-2027 (USD Billion) 55 5.4.11. Nordic Countries 56 5.4.11.1. Nordic Countries Market size and forecast, 2015-2027 (USD Billion) 56 5.4.12. Benelux Union 57 5.4.12.1. Benelux Union Market size and forecast, 2015-2027 (USD Billion) 57 5.4.13. Rest of Europe 58 5.4.13.1. Rest of Europe Market size and forecast, 2015-2027 (USD Billion) 58 5.5. Asia Pacific 59 5.5.1. Asia Pacific Private Hospitals Market size and forecast, 2015-2027 59 5.5.2. Asia Pacific Private Hospitals Market, by Country, 2018 & 2025 (USD Billion) 59 5.5.3. Asia Pacific Private Hospitals Market, by Hospital Type, 2015-2027 61 5.5.3.1. Asia Pacific Private Hospitals Market, by Hospital Type, 2015-2027 (USD Billion) 61 5.5.4. Asia Pacific Private Hospitals Market, by Size, 2015-2027 62 5.5.4.1. Asia Pacific Private Hospitals Market, by Size, 2015-2027 (USD Billion) 62 5.5.5. Asia Pacific Private Hospitals Market, by Location, 2015-2027 63 5.5.5.1. Asia Pacific Private Hospitals Market, by Location, 2015-2027 (USD Billion) 63 5.5.6. China 64 5.5.6.1. China Market size and forecast, 2015-2027 (USD Billion) 64 5.5.7. Japan 65 5.5.7.1. Japan Market size and forecast, 2015-2027 (USD Billion) 65 5.5.8. India 66 5.5.8.1. India Market size and forecast, 2015-2027 (USD Billion) 66 5.5.9. New Zealand 67 5.5.9.1. New Zealand Market size and forecast, 2015-2027 (USD Billion) 67 5.5.10. Australia 68 5.5.10.1. Australia Market size and forecast, 2015-2027 (USD Billion) 68 5.5.11. South Korea 69 5.5.11.1. South Korea Market size and forecast, 2015-2027 (USD Billion) 69 5.5.12. South-East Asia 70 5.5.12.1. South-East Asia Market size and forecast, 2015-2027 (USD Billion) 70 5.5.13. Rest of Asia Pacific 71 5.5.13.1. Rest of Asia Pacific Market size and forecast, 2015-2027 (USD Billion) 71 5.6. Latin America 72 5.6.1. Latin America Private Hospitals Market size and forecast, 2015-2027 72 5.6.2. Latin America Private Hospitals Market, by Country, 2018 & 2025 (USD Billion) 72 5.6.3. Latin America Private Hospitals Market, by Hospital Type, 2015-2027 74 5.6.3.1. Latin America Private Hospitals Market, by Hospital Type, 2015-2027 (USD Billion) 74 5.6.4. Latin America Private Hospitals Market, by Size, 2015-2027 75 5.6.4.1. Latin America Private Hospitals Market, by Size, 2015-2027 (USD Billion) 75 5.6.5. Latin America Private Hospitals Market, by Location, 2015-2027 76 5.6.5.1. Latin America Private Hospitals Market, by Location, 2015-2027 (USD Billion) 76 5.6.6. Brazil 77 5.6.6.1. Brazil Market size and forecast, 2015-2027 (USD Billion) 77 5.6.7. Argentina 78 5.6.7.1. Argentina Market size and forecast, 2015-2027 (USD Billion) 78 5.6.8. Rest of Latin America 79 5.6.8.1. Rest of Latin America Market size and forecast, 2015-2027 (USD Billion) 79 5.7. The Middle-East and Africa 80 5.7.1. The Middle-East and Africa Private Hospitals Market size and forecast, 2015-2027 80 5.7.2. The Middle-East and Africa Private Hospitals Market, by Country, 2018 & 2025 (USD Billion) 80 5.7.3. The Middle-East and Africa Private Hospitals Market, by Hospital Type, 2015-2027 82 5.7.3.1. The Middle-East and Africa Private Hospitals Market, by Hospital Type, 2015-2027 (USD Billion) 82 5.7.4. The Middle-East and Africa Private Hospitals Market, by Size, 2015-2027 83 5.7.4.1. The Middle-East and Africa Private Hospitals Market, by Size, 2015-2027 (USD Billion) 83 5.7.5. The Middle-East and Africa Private Hospitals Market, by Location, 2015-2027 84 5.7.5.1. The Middle-East and Africa Private Hospitals Market, by Location, 2015-2027 (USD Billion) 84 5.7.6. Saudi Arabia 85 5.7.6.1. Saudi Arabia Market size and forecast, 2015-2027 (USD Billion) 85 5.7.7. UAE 86 5.7.7.1. UAE Market size and forecast, 2015-2027 (USD Billion) 86 5.7.8. Egypt 87 5.7.8.1. Egypt Market size and forecast, 2015-2027 (USD Billion) 87 5.7.9. Kuwait 88 5.7.9.1. Kuwait Market size and forecast, 2015-2027 (USD Billion) 88 5.7.10. South Africa 89 5.7.10.1. South Africa Market size and forecast, 2015-2027 (USD Billion) 89 5.7.11. Rest of Middle-East Africa 90 5.7.11.1. Rest of Middle-East Africa Market size and forecast, 2015-2027 (USD Billion) 90 CHAPTER 6. Private Hospitals market – Competitive Landscape 91 6.1. Competitor Market Share – Revenue 91 6.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players 93 6.3. Strategic Development 94 6.3.1. Acquisitions and Mergers 94 6.3.2. New Products 94 6.3.3. Research & Development Activities 94 CHAPTER 7. Company Profiles 95 7.1. MEOCLINIC GmbH 95 7.1.1. Company Overview 95 7.1.2. MEOCLINIC GmbH Revenue and Gross Margin 95 7.1.3. Product portfolio 96 7.1.4. Recent initiatives 97 7.2. Premier Healthcare Germany 97 7.2.1. Company Overview 97 7.2.2. Premier Healthcare Germany Revenue and Gross Margin 97 7.2.3. Product portfolio 98 7.2.4. Recent initiatives 99 7.3. Helios 99 7.3.1. Company Overview 99 7.3.2. Helios Revenue and Gross Margin 99 7.3.3. Product portfolio 100 7.3.4. Recent initiatives 101 7.4. St Francis Foundation 101 7.4.1. Company Overview 101 7.4.2. St Francis Foundation Revenue and Gross Margin 101 7.4.3. Product portfolio 102 7.4.4. Recent initiatives 103 7.5. Shouldice 103 7.5.1. Company Overview 103 7.5.2. Shouldice Revenue and Gross Margin 103 7.5.3. Product portfolio 104 7.5.4. Recent initiatives 105 7.6. Cambie Surgery Centre 105 7.6.1. Company Overview 105 7.6.2. Cambie Surgery Centre Revenue and Gross Margin 105 7.6.3. Product portfolio 106 7.6.4. Recent initiatives 107 7.7. Toulon Hyères Private Hospital 107 7.7.1. Company Overview 107 7.7.2. Toulon Hyères Private Hospital Revenue and Gross Margin 107 7.7.3. Product portfolio 108 7.7.4. Recent initiatives 109 7.8. Hospital Group Deaconesses Croix Saint 109 7.8.1. Company Overview 109 7.8.2. Hospital Group Deaconesses Croix Saint Revenue and Gross Margin 109 7.8.3. Product portfolio 110 7.8.4. Recent initiatives 111 7.9. London Bridge Hospital 111 7.9.1. Company Overview 111 7.9.2. London Bridge Hospital Revenue and Gross Margin 111 7.9.3. Product portfolio 112 7.9.4. Recent initiatives 113 7.10. Ramsay Health Care UK 113 7.10.1. Company Overview 113 7.10.2. Ramsay Health Care UK Revenue and Gross Margin 113 7.10.3. Product portfolio 114 7.10.4. Recent initiatives 115 7.11. HCA Healthcare UK 115 7.11.1. Company Overview 115 7.11.2. HCA Healthcare UK Revenue and Gross Margin 115 7.11.3. Product portfolio 116 7.11.4. Recent initiatives 117 7.12. Nuffield Health 117 7.12.1. Company Overview 117 7.12.2. Nuffield Health Revenue and Gross Margin 117 7.12.3. Product portfolio 118 7.12.4. Recent initiatives 119 7.13. Spire Healthcare Group plc 119 7.13.1. Company Overview 119 7.13.2. Spire Healthcare Group plc Revenue and Gross Margin 119 7.13.3. Product portfolio 120 7.13.4. Recent initiatives 121 7.14. Highgate Private Hospital 121 7.14.1. Company Overview 121 7.14.2. Highgate Private Hospital Revenue and Gross Margin 121 7.14.3. Product portfolio 122 7.14.4. Recent initiatives 123 7.15. Bupa 123 7.15.1. Company Overview 123 7.15.2. Bupa Revenue and Gross Margin 123 7.15.3. Product portfolio 124 7.15.4. Recent initiatives 125 CHAPTER 8. Private Hospitals — Industry Analysis 126 8.1. Private Hospitals Market – Key Trends 126 8.1.1. Market Drivers 127 8.1.2. Market Restraints 127 8.1.3. Market Opportunities 128 8.2. Value Chain Analysis 129 8.3. Technology Roadmap and Timeline 130 8.4. Private Hospitals Market – Attractiveness Analysis 131 8.4.1. By Hospital Type 131 8.4.2. By Size 131 8.4.3. By Location 132 8.4.4. By Region 134 CHAPTER 9. Marketing Strategy Analysis, Distributors 135 9.1. Marketing Channel 135 9.2. Direct Marketing 136 9.3. Indirect Marketing 136 9.4. Marketing Channel Development Trend 136 9.5. Economic/Political Environmental Change 137 CHAPTER 10. Report Conclusion 138 CHAPTER 11. Research Approach & Methodology 139 11.1. Report Description 139 11.2. Research Scope 140 11.3. Research Methodology 140 11.3.1. Secondary Research 141 11.3.2. Primary Research 142 11.3.3. Models 143 11.3.3.1. Company Share Analysis Model 143 11.3.3.2. Revenue Based Modeling 144 11.3.3.3. Research Limitations 144

Inquiry For Buying

Private Hospitals

Request Sample

Private Hospitals