LCD Market Size, Share, and Trends Analysis Report

CAGR :

| Market Size 2024 (Base Year) | USD 154.64 Billion |

| Market Size 2032 (Forecast Year) | USD 301.40 Billion |

| CAGR | 8.7% |

| Forecast Period | 2025 - 2032 |

| Historical Period | 2020 - 2024 |

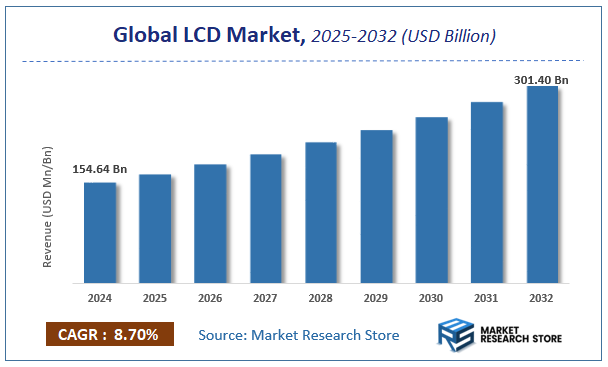

According to a recent study by Market Research Store, the global LCD market size was valued at approximately USD 154.64 Billion in 2024. The market is projected to grow significantly, reaching USD 301.40 Billion by 2032, growing at a compound annual growth rate (CAGR) of 8.7% during the forecast period from 2024 to 2032. The report highlights key growth drivers such as rising demand, technological advancements, and expanding applications. It also outlines potential challenges like regulatory changes and market competition, while emphasizing emerging opportunities for innovation and investment in the LCD industry.

To Get more Insights, Request a Free Sample

LCD Market: Overview

The growth of the LCD market is fueled by rising global demand across various industries and applications. The report highlights lucrative opportunities, analyzing cost structures, key segments, emerging trends, regional dynamics, and advancements by leading players to provide comprehensive market insights. The LCD market report offers a detailed industry analysis from 2024 to 2032, combining quantitative and qualitative insights. It examines key factors such as pricing, market penetration, GDP impact, industry dynamics, major players, consumer behavior, and socio-economic conditions. Structured into multiple sections, the report provides a comprehensive perspective on the market from all angles.

Key sections of the LCD market report include market segments, outlook, competitive landscape, and company profiles. Market Segments offer in-depth details based on Technology Type, Application, Size Type, End-User Industry, Panel Type, and other relevant classifications to support strategic marketing initiatives. Market Outlook thoroughly analyzes market trends, growth drivers, restraints, opportunities, challenges, Porter’s Five Forces framework, macroeconomic factors, value chain analysis, and pricing trends shaping the market now and in the future. The Competitive Landscape and Company Profiles section highlights major players, their strategies, and market positioning to guide investment and business decisions. The report also identifies innovation trends, new business opportunities, and investment prospects for the forecast period.

Key Highlights:

- As per the analysis shared by our research analyst, the global LCD market is estimated to grow annually at a CAGR of around 8.7% over the forecast period (2024-2032).

- In terms of revenue, the global LCD market size was valued at around USD 154.64 Billion in 2024 and is projected to reach USD 301.40 Billion by 2032.

- The market is projected to grow at a significant rate due to Growing demand for consumer electronics, rising adoption in televisions, smartphones, and monitors, and increasing use in automotive displays are driving the LCD market.

- Based on the Technology Type, the Twisted Nematic (TN) segment is growing at a high rate and will continue to dominate the global market as per industry projections.

- On the basis of Application, the Consumer Electronics segment is anticipated to command the largest market share.

- In terms of Size Type, the Small Displays segment is projected to lead the global market.

- By End-User Industry, the Electronics segment is predicted to dominate the global market.

- Based on the Panel Type, the Edge-Lit Panels segment is expected to swipe the largest market share.

- Based on region, Asia Pacific is projected to dominate the global market during the forecast period.

LCD Market: Report Scope

This report thoroughly analyzes the LCD market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | LCD Market |

| Market Size in 2024 | USD 154.64 Billion |

| Market Forecast in 2032 | USD 301.40 Billion |

| Growth Rate | CAGR of 8.7% |

| Number of Pages | 219 |

| Key Companies Covered | Samsung, LG, Philips, HP, NEC, AOC |

| Segments Covered | By Technology Type, By Application, By Size Type, By End-User Industry, By Panel Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2020 to 2024 |

| Forecast Year | 2025 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

LCD Market: Dynamics

Key Growth Drivers :

The LCD (Liquid Crystal Display) market continues to be driven by persistent demand across various consumer electronics and industrial applications, despite the rise of alternative display technologies. Key growth drivers include the ongoing need for displays in budget-friendly smartphones, entry-level televisions, and a wide array of automotive displays, industrial monitors, and medical equipment. The continuous improvement in LCD technology, offering better contrast ratios, wider viewing angles, and enhanced power efficiency at competitive prices, ensures its sustained relevance. Furthermore, the expansion of commercial display applications, such as digital signage and public information displays, further fuels the market.

Restraints :

Despite its widespread use, the LCD market faces significant restraints, primarily from the aggressive competition posed by advanced display technologies like OLED (Organic Light Emitting Diode) and, more recently, Mini-LED and Micro-LED. OLEDs offer superior contrast, true blacks, and faster response times, capturing the premium segment of the smartphone and TV markets. Furthermore, the oversupply of LCD panels due to significant capacity expansion, particularly in China, often leads to price erosion and impacts the profitability of manufacturers. The inherent limitations of LCDs, such as backlight requirements and slower response times compared to OLEDs, also act as restraints.

Opportunities :

Significant opportunities in the LCD market are emerging from the continuous innovation in panel technology and the expansion into specialized applications. The development of advanced LCD technologies like IPS (In-Plane Switching) and VA (Vertical Alignment) continues to improve viewing angles and contrast, making them suitable for a broader range of uses. The automotive sector, with its increasing demand for multiple in-car displays (dashboard, infotainment, rearview mirrors), presents a substantial growth opportunity. Furthermore, specialized industrial and medical displays requiring high brightness, ruggedness, and long lifecycles continue to rely heavily on LCD technology, offering stable niche markets.

Challenges :

The primary challenge for the LCD market involves navigating intense competition from advanced display technologies and managing the cyclical nature of supply and demand which often leads to price volatility. Manufacturers must continuously invest in R&D to enhance LCD performance and reduce production costs to remain competitive. Furthermore, addressing environmental concerns related to the disposal of display panels and the energy consumption during manufacturing is becoming increasingly important. Adapting to rapid shifts in consumer preferences and technological trends, while dealing with global supply chain complexities, remains a persistent challenge for LCD market players.

LCD Market: Segmentation Insights

The global LCD market is segmented based on Technology Type, Application, Size Type, End-User Industry, Panel Type, and Region. All the segments of the LCD market have been analyzed based on present & future trends and the market is estimated from 2024 to 2032.

Based on Technology Type, the global LCD market is divided into Twisted Nematic (TN), In-Plane Switching (IPS), Vertical Alignment (VA), Advanced fringe field switching (AFFS), Organic Light Emitting Diode (OLED).

On the basis of Application, the global LCD market is bifurcated into Consumer Electronics, Televisions, Smartphones, Tablets, Laptops and Desktop Monitors, Automotive, Industrial Displays, Medical Devices, Signage and Advertising Displays, Aerospace and Defense.

In terms of Size Type, the global LCD market is categorized into Small Displays, andle; 27 inches, Medium Displays, 28 to 55 inches, Large Displays, andgt; 55 inches, Custom and Specialty Sizes.

Based on End-User Industry, the global LCD market is split into Electronics, Retail, Healthcare, Education, Transportation, Media and Entertainment, Gaming.

By Panel Type, the global LCD market is divided into Edge-Lit Panels, Direct-Lit Panels, Full Array Panels, Touch Panels, Flexible Displays.

LCD Market: Regional Insights

The Asia-Pacific region overwhelmingly dominates the global Liquid Crystal Display (LCD) market, accounting for over 80% of both production and consumption. This hegemony is centered in East Asia, with China, South Korea, and Taiwan housing the world's largest panel manufacturers (e.g., BOE, LG Display, Innolux) and controlling the vast majority of global Gen 10.5 fabrication capacity. The region's leadership is fueled by massive domestic demand from its consumer electronics and automotive industries, integrated supply chains, and significant government support, solidifying its unrivalled position despite slowing growth in the traditional television segment.

LCD Market: Competitive Landscape

The LCD market Report offers a thorough analysis of both established and emerging players within the market. It includes a detailed list of key companies, categorized based on the types of products they offer and other relevant factors. The report also highlights the market entry year for each player, providing further context for the research analysis.

The "Global LCD Market" study offers valuable insights, focusing on the global market landscape, with an emphasis on major industry players such as;

- Samsung

- LG

- Philips

- HP

- NEC

- AOC

The Global LCD Market is Segmented as Follows:

By Technology Type

- Twisted Nematic (TN)

- In-Plane Switching (IPS)

- Vertical Alignment (VA)

- Advanced fringe field switching (AFFS)

- Organic Light Emitting Diode (OLED)

By Application

- Consumer Electronics

- Televisions

- Smartphones

- Tablets

- Laptops and Desktop Monitors

- Automotive

- Industrial Displays

- Medical Devices

- Signage and Advertising Displays

- Aerospace an

By Size Type

- Small Displays

- andle; 27 inches

- Medium Displays

- 28 to 55 inches

- Large Displays

- andgt; 55 inches

- Custom and Specialty Sizes

By End-User Industry

- Electronics

- Retail

- Healthcare

- Education

- Transportation

- Media and Entertainment

- Gaming

By Panel Type

- Edge-Lit Panels

- Direct-Lit Panels

- Full Array Panels

- Touch Panels

- Flexible Displays

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Frequently Asked Questions

Table Of Content

Table of Content 1 Report Overview 1.1 Study Scope 1.2 Key Market Segments 1.3 Regulatory Scenario by Region/Country 1.4 Market Investment Scenario Strategic 1.5 Market Analysis by Type 1.5.1 Global LCD Market Share by Type (2020-2026) 1.5.2 AMLCDs 1.5.3 TFT LCDs 1.5.4 PMLCDs 1.6 Market by Application 1.6.1 Global LCD Market Share by Application (2020-2026) 1.6.2 Television 1.6.3 Notebook PC/Tablet 1.6.4 Monitor 1.6.5 Mobile 1.6.6 Others 1.7 LCD Industry Development Trends under COVID-19 Outbreak 1.7.1 Global COVID-19 Status Overview 1.7.2 Influence of COVID-19 Outbreak on LCD Industry Development 2. Global Market Growth Trends 2.1 Industry Trends 2.1.1 SWOT Analysis 2.1.2 Porter’s Five Forces Analysis 2.2 Potential Market and Growth Potential Analysis 2.3 Industry News and Policies by Regions 2.3.1 Industry News 2.3.2 Industry Policies 2.4 Industry Trends Under COVID-19 3 Value Chain of LCD Market 3.1 Value Chain Status 3.2 LCD Manufacturing Cost Structure Analysis 3.2.1 Production Process Analysis 3.2.2 Manufacturing Cost Structure of LCD 3.2.3 Labor Cost of LCD 3.2.3.1 Labor Cost of LCD Under COVID-19 3.3 Sales and Marketing Model Analysis 3.4 Downstream Major Customer Analysis (by Region) 3.5 Value Chain Status Under COVID-19 4 Players Profiles 4.1 CSOT 4.1.1 CSOT Basic Information 4.1.2 LCD Product Profiles, Application and Specification 4.1.3 CSOT LCD Market Performance (2015-2020) 4.1.4 CSOT Business Overview 4.2 SHARP 4.2.1 SHARP Basic Information 4.2.2 LCD Product Profiles, Application and Specification 4.2.3 SHARP LCD Market Performance (2015-2020) 4.2.4 SHARP Business Overview 4.3 LGD 4.3.1 LGD Basic Information 4.3.2 LCD Product Profiles, Application and Specification 4.3.3 LGD LCD Market Performance (2015-2020) 4.3.4 LGD Business Overview 4.4 AUO 4.4.1 AUO Basic Information 4.4.2 LCD Product Profiles, Application and Specification 4.4.3 AUO LCD Market Performance (2015-2020) 4.4.4 AUO Business Overview 4.5 Samsung 4.5.1 Samsung Basic Information 4.5.2 LCD Product Profiles, Application and Specification 4.5.3 Samsung LCD Market Performance (2015-2020) 4.5.4 Samsung Business Overview 4.6 LG 4.6.1 LG Basic Information 4.6.2 LCD Product Profiles, Application and Specification 4.6.3 LG LCD Market Performance (2015-2020) 4.6.4 LG Business Overview 4.7 Tianma 4.7.1 Tianma Basic Information 4.7.2 LCD Product Profiles, Application and Specification 4.7.3 Tianma LCD Market Performance (2015-2020) 4.7.4 Tianma Business Overview 4.8 BOE 4.8.1 BOE Basic Information 4.8.2 LCD Product Profiles, Application and Specification 4.8.3 BOE LCD Market Performance (2015-2020) 4.8.4 BOE Business Overview 4.9 Visionix 4.9.1 Visionix Basic Information 4.9.2 LCD Product Profiles, Application and Specification 4.9.3 Visionix LCD Market Performance (2015-2020) 4.9.4 Visionix Business Overview 4.10 Innolux 4.10.1 Innolux Basic Information 4.10.2 LCD Product Profiles, Application and Specification 4.10.3 Innolux LCD Market Performance (2015-2020) 4.10.4 Innolux Business Overview 4.11 Truly Semiconductors 4.11.1 Truly Semiconductors Basic Information 4.11.2 LCD Product Profiles, Application and Specification 4.11.3 Truly Semiconductors LCD Market Performance (2015-2020) 4.11.4 Truly Semiconductors Business Overview 4.12 EDO 4.12.1 EDO Basic Information 4.12.2 LCD Product Profiles, Application and Specification 4.12.3 EDO LCD Market Performance (2015-2020) 4.12.4 EDO Business Overview 4.13 CEC Group 4.13.1 CEC Group Basic Information 4.13.2 LCD Product Profiles, Application and Specification 4.13.3 CEC Group LCD Market Performance (2015-2020) 4.13.4 CEC Group Business Overview 5 Global LCD Market Analysis by Regions 5.1 Global LCD Sales, Revenue and Market Share by Regions 5.1.1 Global LCD Sales by Regions (2015-2020) 5.1.2 Global LCD Revenue by Regions (2015-2020) 5.2 North America LCD Sales and Growth Rate (2015-2020) 5.3 Europe LCD Sales and Growth Rate (2015-2020) 5.4 Asia-Pacific LCD Sales and Growth Rate (2015-2020) 5.5 Middle East and Africa LCD Sales and Growth Rate (2015-2020) 5.6 South America LCD Sales and Growth Rate (2015-2020) 6 North America LCD Market Analysis by Countries 6.1 North America LCD Sales, Revenue and Market Share by Countries 6.1.1 North America LCD Sales by Countries (2015-2020) 6.1.2 North America LCD Revenue by Countries (2015-2020) 6.1.3 North America LCD Market Under COVID-19 6.2 United States LCD Sales and Growth Rate (2015-2020) 6.2.1 United States LCD Market Under COVID-19 6.3 Canada LCD Sales and Growth Rate (2015-2020) 6.4 Mexico LCD Sales and Growth Rate (2015-2020) 7 Europe LCD Market Analysis by Countries 7.1 Europe LCD Sales, Revenue and Market Share by Countries 7.1.1 Europe LCD Sales by Countries (2015-2020) 7.1.2 Europe LCD Revenue by Countries (2015-2020) 7.1.3 Europe LCD Market Under COVID-19 7.2 Germany LCD Sales and Growth Rate (2015-2020) 7.2.1 Germany LCD Market Under COVID-19 7.3 UK LCD Sales and Growth Rate (2015-2020) 7.3.1 UK LCD Market Under COVID-19 7.4 France LCD Sales and Growth Rate (2015-2020) 7.4.1 France LCD Market Under COVID-19 7.5 Italy LCD Sales and Growth Rate (2015-2020) 7.5.1 Italy LCD Market Under COVID-19 7.6 Spain LCD Sales and Growth Rate (2015-2020) 7.6.1 Spain LCD Market Under COVID-19 7.7 Russia LCD Sales and Growth Rate (2015-2020) 7.7.1 Russia LCD Market Under COVID-19 8 Asia-Pacific LCD Market Analysis by Countries 8.1 Asia-Pacific LCD Sales, Revenue and Market Share by Countries 8.1.1 Asia-Pacific LCD Sales by Countries (2015-2020) 8.1.2 Asia-Pacific LCD Revenue by Countries (2015-2020) 8.1.3 Asia-Pacific LCD Market Under COVID-19 8.2 China LCD Sales and Growth Rate (2015-2020) 8.2.1 China LCD Market Under COVID-19 8.3 Japan LCD Sales and Growth Rate (2015-2020) 8.3.1 Japan LCD Market Under COVID-19 8.4 South Korea LCD Sales and Growth Rate (2015-2020) 8.4.1 South Korea LCD Market Under COVID-19 8.5 Australia LCD Sales and Growth Rate (2015-2020) 8.6 India LCD Sales and Growth Rate (2015-2020) 8.6.1 India LCD Market Under COVID-19 8.7 Southeast Asia LCD Sales and Growth Rate (2015-2020) 8.7.1 Southeast Asia LCD Market Under COVID-19 9 Middle East and Africa LCD Market Analysis by Countries 9.1 Middle East and Africa LCD Sales, Revenue and Market Share by Countries 9.1.1 Middle East and Africa LCD Sales by Countries (2015-2020) 9.1.2 Middle East and Africa LCD Revenue by Countries (2015-2020) 9.1.3 Middle East and Africa LCD Market Under COVID-19 9.2 Saudi Arabia LCD Sales and Growth Rate (2015-2020) 9.3 UAE LCD Sales and Growth Rate (2015-2020) 9.4 Egypt LCD Sales and Growth Rate (2015-2020) 9.5 Nigeria LCD Sales and Growth Rate (2015-2020) 9.6 South Africa LCD Sales and Growth Rate (2015-2020) 10 South America LCD Market Analysis by Countries 10.1 South America LCD Sales, Revenue and Market Share by Countries 10.1.1 South America LCD Sales by Countries (2015-2020) 10.1.2 South America LCD Revenue by Countries (2015-2020) 10.1.3 South America LCD Market Under COVID-19 10.2 Brazil LCD Sales and Growth Rate (2015-2020) 10.2.1 Brazil LCD Market Under COVID-19 10.3 Argentina LCD Sales and Growth Rate (2015-2020) 10.4 Columbia LCD Sales and Growth Rate (2015-2020) 10.5 Chile LCD Sales and Growth Rate (2015-2020) 11 Global LCD Market Segment by Types 11.1 Global LCD Sales, Revenue and Market Share by Types (2015-2020) 11.1.1 Global LCD Sales and Market Share by Types (2015-2020) 11.1.2 Global LCD Revenue and Market Share by Types (2015-2020) 11.2 AMLCDs Sales and Price (2015-2020) 11.3 TFT LCDs Sales and Price (2015-2020) 11.4 PMLCDs Sales and Price (2015-2020) 12 Global LCD Market Segment by Applications 12.1 Global LCD Sales, Revenue and Market Share by Applications (2015-2020) 12.1.1 Global LCD Sales and Market Share by Applications (2015-2020) 12.1.2 Global LCD Revenue and Market Share by Applications (2015-2020) 12.2 Television Sales, Revenue and Growth Rate (2015-2020) 12.3 Notebook PC/Tablet Sales, Revenue and Growth Rate (2015-2020) 12.4 Monitor Sales, Revenue and Growth Rate (2015-2020) 12.5 Mobile Sales, Revenue and Growth Rate (2015-2020) 12.6 Others Sales, Revenue and Growth Rate (2015-2020) 13 LCD Market Forecast by Regions (2020-2026) 13.1 Global LCD Sales, Revenue and Growth Rate (2020-2026) 13.2 LCD Market Forecast by Regions (2020-2026) 13.2.1 North America LCD Market Forecast (2020-2026) 13.2.2 Europe LCD Market Forecast (2020-2026) 13.2.3 Asia-Pacific LCD Market Forecast (2020-2026) 13.2.4 Middle East and Africa LCD Market Forecast (2020-2026) 13.2.5 South America LCD Market Forecast (2020-2026) 13.3 LCD Market Forecast by Types (2020-2026) 13.4 LCD Market Forecast by Applications (2020-2026) 13.5 LCD Market Forecast Under COVID-19 14 Appendix 14.1 Methodology 14.2 Research Data Source

Inquiry For Buying

LCD

Request Sample

LCD