Liquid Waterborne Printing Inks Market Size, Share, and Trends Analysis Report

CAGR :

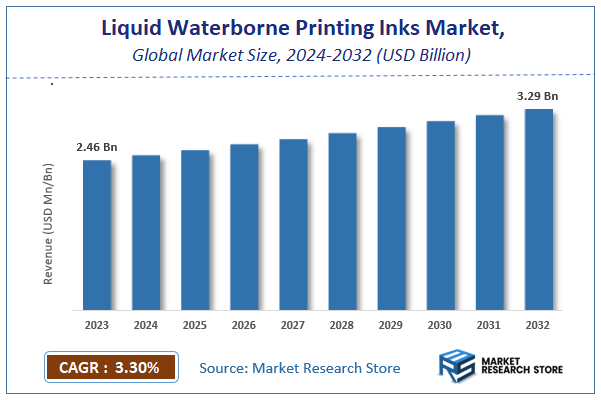

| Market Size 2023 (Base Year) | USD 2.46 Billion |

| Market Size 2032 (Forecast Year) | USD 3.29 Billion |

| CAGR | 3.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Liquid Waterborne Printing Inks Market Insights

According to Market Research Store, the global liquid waterborne printing inks market size was valued at around USD 2.46 billion in 2023 and is estimated to reach USD 3.29 billion by 2032, to register a CAGR of approximately 3.3% in terms of revenue during the forecast period 2024-2032.

The liquid waterborne printing inks report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Liquid Waterborne Printing Inks Market: Overview

Liquid waterborne printing inks are a type of printing ink formulated using water as the primary solvent or carrier. These inks are known for their low levels of volatile organic compounds (VOCs), making them an environmentally friendly alternative to solvent-based inks. They are widely used in various printing applications, including packaging, publishing, and commercial printing, as they offer excellent adhesion, fast drying, and vibrant color output. Additionally, waterborne inks are compatible with a wide range of substrates, such as paper, cardboard, and certain types of plastic, making them versatile and effective for diverse industries.

Key Highlights

- The liquid waterborne printing inks market is anticipated to grow at a CAGR of 3.3% during the forecast period.

- The global liquid waterborne printing inks market was estimated to be worth approximately USD 2.46 billion in 2023 and is projected to reach a value of USD 3.29 billion by 2032.

- The growth of the liquid waterborne printing inks market is being driven by increasing demand for eco-friendly and sustainable printing solutions.

- Based on the type, the flexography inks segment is growing at a high rate and is projected to dominate the market.

- In terms of substrate, the films segment is expected to dominate the market.

- On the basis of application, the industrial segment is projected to swipe the largest market share.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Liquid Waterborne Printing Inks Market: Dynamics

Key Growth Drivers:

- Growing demand for sustainable packaging: Consumers and businesses are increasingly concerned about environmental issues, leading to a surge in demand for eco-friendly packaging solutions. Water-based inks align with this trend due to their reduced environmental impact compared to solvent-based inks.

- Stringent environmental regulations: Governments worldwide are implementing stricter regulations on volatile organic compounds (VOCs) emissions to mitigate air pollution. Water-based inks have significantly lower VOC emissions, making them a preferred choice for printers.

- Rising e-commerce activities: The e-commerce boom has fueled the demand for packaging materials, including printed cartons, boxes, and labels. Water-based inks are well-suited for high-speed printing processes required to meet the demands of e-commerce logistics.

Restraints:

- Performance limitations: In certain applications, water-based inks may not always match the performance of solvent-based inks in terms of print quality, adhesion, and durability.

- Higher costs: Water-based inks can sometimes be more expensive than solvent-based inks, which can be a barrier for cost-sensitive businesses.

- Limited availability: In some regions, the availability of high-quality water-based inks for specific printing processes or substrates may be limited.

Opportunities:

- Technological advancements: Ongoing research and development are leading to improvements in water-based ink formulations, enhancing their performance and expanding their applicability.

- Expanding applications: Water-based inks are finding new applications in various industries, such as food packaging, pharmaceuticals, and textiles.

- Emerging markets: The growing economies in developing countries present significant opportunities for the water-based inks market.

Challenges:

- Maintaining print quality: Achieving consistent print quality with water-based inks can be challenging, especially for complex printing processes.

- Meeting specific performance requirements: Meeting the stringent performance requirements of certain applications, such as food packaging and medical devices, can be a challenge for water-based inks.

- Competition from solvent-based inks: Solvent-based inks continue to hold a significant market share, posing competition for water-based inks.

Liquid Waterborne Printing Inks Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Liquid Waterborne Printing Inks Market |

| Market Size in 2023 | USD 2.46 Billion |

| Market Forecast in 2032 | USD 3.29 Billion |

| Growth Rate | CAGR of 3.3% |

| Number of Pages | 140 |

| Key Companies Covered | DIC CORPORATION (Japan), Flint Group (Luxembourg), TOYO INK SC HOLDINGS CO., LTD. (Japan), Sakata Inx (India) Private Limited (India), Siegwerk Druckfarben AG & Co. KGaA (Germany), Hubergroup India Private Limited (India), T&K TOKA Corporation (Japan), Altana (Germany), TOKYO PRINTING INK MFG CO., LTD. (Japan), Wikoff Color Corporation (U.S.), Royal Dutch Printing Ink Factories Van Son (Netherlands), Dainichiseika Color & Chemicals Mfg. Co., Ltd. (Japan), Zeller+Gmelin (Germany), Sun Chemical (U.S.), Alden & Ott Printing Inks Co (U.S.), Gardiner Colours Limited (U.K.), MALLARD INK CO AND OFFSET BLANKET CO. Inc. (U.S.), INX International Ink Co. (U.S.), INKNOVATORS (India), and Avreon Chemicals India Private Limited (India) |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Liquid Waterborne Printing Inks Market: Segmentation Insights

The global liquid waterborne printing inks market is divided by type, substrate, application, and region.

Segmentation Insights by Type

Based on type, the global liquid waterborne printing inks market is divided into flexography inks and gravure inks.

Flexography inks dominate the liquid waterborne printing inks market due to their versatility and widespread adoption in packaging applications. These inks are highly suited for printing on a variety of substrates, including corrugated cardboard, flexible packaging, and labels. Their low viscosity and quick drying properties make them ideal for high-speed printing operations, particularly in industries like food and beverage packaging. Additionally, the environmental benefits of waterborne flexography inks, including lower volatile organic compound (VOC) emissions, have increased their popularity as companies prioritize sustainability. The growing e-commerce sector has further boosted the demand for flexographic printing in packaging, solidifying its position as the leading segment.

Gravure inks, while less dominant than flexography inks, play a significant role in high-quality and large-volume printing applications. These inks are preferred for their ability to produce fine details and vibrant colors, making them ideal for premium packaging, decorative printing, and publication materials. Gravure printing's high initial setup cost and slower production rates compared to flexography limit its application to specific niches, such as luxury product packaging and specialty printing. However, advancements in waterborne gravure ink formulations are gradually improving their eco-friendliness and reducing production costs, making them a competitive choice in certain market segments.

Segmentation Insights by Substrate

Based on substrate, the global liquid waterborne printing inks market is divided into films and paper & paperboard.

Films represent the most dominant substrate segment in the liquid waterborne printing inks market, primarily driven by their extensive use in flexible packaging. Industries such as food and beverages, personal care, and pharmaceuticals heavily rely on film substrates for their durability, barrier properties, and aesthetic appeal. Liquid waterborne inks perform exceptionally well on films due to their strong adhesion, vibrant color reproduction, and environmentally friendly nature, aligning with the growing demand for sustainable packaging solutions. The rise of e-commerce and advancements in flexible packaging technology further enhance the dominance of this segment.

The paper & paperboard segment holds a significant share but is less dominant compared to films. These substrates are widely used for applications such as cartons, labels, and point-of-sale displays, particularly in industries like retail and foodservice. Liquid waterborne inks are favored for paper and paperboard due to their compatibility with the porous surface, delivering excellent print clarity and eco-friendliness. Increasing consumer preference for biodegradable and recyclable packaging materials boosts the demand for paperboard substrates, supporting the segment's steady growth. However, their market share remains lower than films due to limitations in durability and barrier properties compared to flexible films.

Segmentation Insights by Application

On the basis of application, the global liquid waterborne printing inks market is bifurcated into industrial, construction, and manufacturing.

The industrial application segment is the most dominant in the liquid waterborne printing inks market. Waterborne inks are extensively used in the industrial sector for printing on a variety of materials such as metal, plastic, and wood. These inks are preferred for their durability, fast-drying capabilities, and resistance to chemicals and abrasions, making them ideal for labeling, branding, and product identification. Industries such as automotive, electronics, and machinery rely on high-quality, sustainable printing solutions for their products. Additionally, as environmental regulations become stricter, waterborne inks offer an eco-friendlier alternative to solvent-based inks, which further boosts their adoption in industrial applications.

In the construction segment, liquid waterborne printing inks are increasingly used for applications such as printing on materials like wood, cement, and other construction products. This segment benefits from the growing focus on sustainable construction materials, where waterborne inks are chosen for their low environmental impact. Printing on construction materials is essential for branding, safety labels, and product identification, and waterborne inks provide an excellent solution due to their strong adhesion to porous surfaces and non-toxic properties. However, the construction segment is smaller compared to industrial applications due to more limited use cases and a focus on other types of coatings and finishes.

The manufacturing segment also represents a significant portion of the market for waterborne inks, especially for product labeling, packaging, and branding. Liquid waterborne inks are widely used for printing on various materials in manufacturing, such as plastics, textiles, and metal products. Their eco-friendly nature, vibrant color output, and fast-drying properties make them ideal for applications requiring high-speed production lines. While the manufacturing segment continues to grow, it is slightly less dominant than the industrial segment, as it is more focused on packaging and labeling rather than the heavy-duty and durable applications seen in industrial environments.

Liquid Waterborne Printing Inks Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific region dominates the liquid waterborne printing inks market, primarily due to its rapid industrialization and growing packaging industry. Countries such as China and India are driving this growth with increasing urbanization, rising disposable incomes, and evolving consumer preferences. The expanding e-commerce sector in the region has further boosted the demand for packaging materials, creating a robust market for waterborne printing inks known for their eco-friendliness and compliance with strict environmental regulations.

North America holds a significant share of the market, driven by stringent environmental policies aimed at reducing volatile organic compound (VOC) emissions. The adoption of waterborne inks has been particularly prominent due to the regulatory frameworks encouraging sustainable printing solutions. The region’s strong flexible packaging industry, coupled with consumer demand for eco-friendly products, has further bolstered the market.

Europe exhibits notable growth in the liquid waterborne printing inks market, supported by a strong emphasis on sustainability and strict environmental standards. The region's initiatives to promote a circular economy and reduce industrial emissions have increased the adoption of waterborne inks. Additionally, the focus on recyclable packaging and environmentally conscious products aligns with consumer preferences, further driving the market's expansion.

The Middle East and Africa region is gradually adopting liquid waterborne printing inks, influenced by the growing printing and packaging sectors. Economic development in several countries has spurred demand for high-quality printing solutions, while increasing environmental awareness encourages the shift to sustainable options like waterborne inks. Government policies supporting eco-friendly practices also contribute to the market's growth.

South America shows steady progress in the adoption of liquid waterborne printing inks, supported by the growth of the packaging and consumer goods industries. The region is experiencing a shift toward environmentally responsible practices, with manufacturers opting for waterborne inks to align with global sustainability trends and meet the demands of eco-conscious consumers.

Liquid Waterborne Printing Inks Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the liquid waterborne printing inks market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global liquid waterborne printing inks market include:

- DIC CORPORATION (Japan)

- Flint Group (Luxembourg)

- TOYO INK SC HOLDINGS CO., LTD. (Japan)

- Sakata Inx (India) Private Limited (India)

- Siegwerk Druckfarben AG & Co. KGaA (Germany)

- Hubergroup India Private Limited (India)

- T&K TOKA Corporation (Japan)

- Altana (Germany)

- TOKYO PRINTING INK MFG CO., LTD. (Japan)

- Wikoff Color Corporation (U.S.)

- Royal Dutch Printing Ink Factories Van Son (Netherlands)

- Dainichiseika Color & Chemicals Mfg. Co., Ltd. (Japan)

- Zeller+Gmelin (Germany)

- Sun Chemical (U.S.)

- Alden & Ott Printing Inks Co (U.S.)

- Gardiner Colours Limited (U.K.)

- MALLARD INK CO AND OFFSET BLANKET CO., INC. (U.S.)

- INX International Ink Co. (U.S.)

- INKNOVATORS (India)

- Avreon Chemicals India Private Limited (India)

The global liquid waterborne printing inks market is segmented as follows:

By Type

- Flexography Inks

- Gravure Ink

By Substrate

- Films

- Paper & Paperboard

By Application

- Industrial

- Construction

- Manufacturing

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global liquid waterborne printing inks market size was projected at approximately US$ 2.46 billion in 2023. Projections indicate that the market is expected to reach around US$ 3.29 billion in revenue by 2032.

The global liquid waterborne printing inks market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 3.3% during the forecast period from 2024 to 2032.

Asia Pacific is expected to dominate the global liquid waterborne printing inks market.

The global liquid waterborne printing inks market is driven by increasing demand for eco-friendly and sustainable printing solutions, stringent environmental regulations reducing VOC emissions, and the growing packaging industry, especially in e-commerce. Additionally, the shift toward recyclable and compliant packaging materials further boosts market growth.

Who are the leading players functioning in the global liquid waterborne printing inks market growth?

Some of the prominent players operating in the global liquid waterborne printing inks market are; DIC CORPORATION (Japan), Flint Group (Luxembourg), TOYO INK SC HOLDINGS CO., LTD. (Japan), Sakata Inx (India) Private Limited (India), Siegwerk Druckfarben AG & Co. KGaA (Germany), Hubergroup India Private Limited (India), T&K TOKA Corporation (Japan), Altana (Germany), TOKYO PRINTING INK MFG CO., LTD. (Japan), Wikoff Color Corporation (U.S.), Royal Dutch Printing Ink Factories Van Son (Netherlands), Dainichiseika Color & Chemicals Mfg. Co., Ltd. (Japan), Zeller+Gmelin (Germany), Sun Chemical (U.S.), Alden & Ott Printing Inks Co (U.S.), Gardiner Colours Limited (U.K.), MALLARD INK CO AND OFFSET BLANKET CO., INC. (U.S.), INX International Ink Co. (U.S.), INKNOVATORS (India), Avreon Chemicals India Private Limited (India), and others.

Table Of Content

Inquiry For Buying

Liquid Waterborne Printing Inks

Request Sample

Liquid Waterborne Printing Inks