LNG Market Size, Share, and Trends Analysis Report

CAGR :

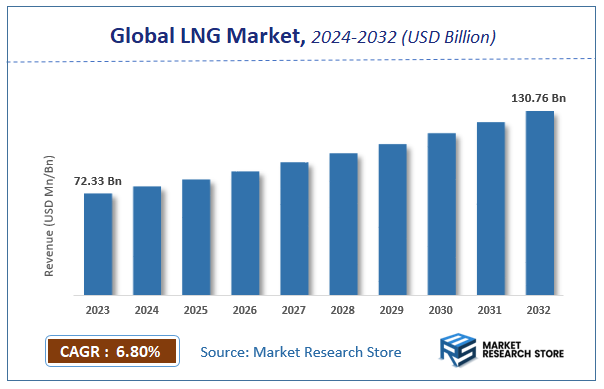

| Market Size 2023 (Base Year) | USD 72.33 Billion |

| Market Size 2032 (Forecast Year) | USD 130.76 Billion |

| CAGR | 6.8% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

LNG Market Insights

According to Market Research Store, the global LNG market size was valued at around USD 72.33 billion in 2023 and is estimated to reach USD 130.76 billion by 2032, to register a CAGR of approximately 6.8% in terms of revenue during the forecast period 2024-2032.

The LNG report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global LNG Market: Overview

LNG is natural gas—primarily composed of methane—that has been cooled to a liquid state at approximately -162°C (-260°F) for ease of storage and transportation. This liquefaction process reduces the gas volume by about 600 times, allowing it to be transported efficiently over long distances, especially where pipelines are not feasible. Once delivered, LNG can be regasified and used for residential, commercial, industrial, or power generation applications. LNG plays a crucial role in global energy markets as a cleaner-burning fossil fuel alternative. Compared to coal and oil, LNG emits significantly lower levels of carbon dioxide (CO₂), sulfur dioxide (SO₂), and nitrogen oxides (NOₓ), making it a strategic fuel in the transition toward lower-carbon energy systems.

The LNG market is expanding due to rising global energy demand, increased focus on reducing greenhouse gas emissions, and the need for flexible and secure energy supply chains. Technological advancements in liquefaction, shipping, and regasification infrastructure—such as floating LNG terminals and modular small-scale LNG plants—are enhancing the efficiency and accessibility of LNG. Moreover, emerging markets in Asia and the increasing use of LNG as a marine and transport fuel are driving further growth. As governments and industries seek to diversify energy sources while improving environmental performance, LNG continues to play a pivotal role in the evolving global energy mix.

Key Highlights

- The LNG market is anticipated to grow at a CAGR of 6.8% during the forecast period.

- The global LNG market was estimated to be worth approximately USD 72.33 billion in 2023 and is projected to reach a value of USD 130.76 billion by 2032.

- The growth of the LNG market is being driven by increasing energy demand, a global shift towards cleaner energy sources, and growing environmental concerns.

- Based on the product, the ethane segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the construction segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

LNG Market: Dynamics

Key Growth Drivers:

- Rising Global Energy Demand: Increasing population and industrialization, particularly in Asia, are driving the overall demand for energy, with natural gas and LNG being a significant part of the energy mix.

- Shift Towards Cleaner Energy Sources: As countries worldwide aim to reduce carbon emissions, LNG is increasingly favored over more carbon-intensive fossil fuels like coal and oil in power generation and industrial applications.

- Energy Security and Diversification: LNG offers nations a way to diversify their energy sources and reduce reliance on single suppliers or politically unstable regions, enhancing energy security.

- Growth in LNG Infrastructure: Increasing investments in liquefaction plants, regasification terminals, and LNG carriers are expanding the capacity and flexibility of the global LNG trade network.

- Technological Advancements: Innovations in liquefaction, transportation (including Floating LNG - FLNG), and regasification technologies are improving efficiency and reducing costs across the LNG value chain.

- Expansion of Gas-Powered Transportation: The adoption of LNG as a fuel for marine vessels and heavy-duty vehicles is a growing demand driver due to stricter environmental regulations in the transportation sector.

- Geopolitical Factors: Events such as the Russia-Ukraine conflict have led to a significant shift in gas supply routes, increasing Europe's reliance on LNG imports.

Restraints:

- High Infrastructure Costs: The development of liquefaction plants, regasification terminals, and specialized LNG carriers requires substantial upfront capital investment.

- Price Volatility: LNG prices can be volatile due to fluctuations in natural gas prices, geopolitical events, and seasonal demand variations.

- Long-Term Contractual Nature: The LNG market has historically been dominated by long-term contracts, which can limit flexibility and responsiveness to short-term market changes, although spot trading is increasing.

- Environmental Concerns (Methane Leakage): While cleaner than coal, the LNG supply chain faces scrutiny regarding methane leakage during production, transportation, and regasification, a potent greenhouse gas.

- Geopolitical Risks: Disruptions in major LNG producing or transit regions due to political instability or conflicts can significantly impact supply and prices.

- Regulatory Hurdles and Permitting: Obtaining necessary permits and complying with diverse regulations across different countries for LNG projects can be a lengthy and complex process.

- Competition from Renewable Energy Sources: The increasing competitiveness and deployment of renewable energy technologies pose a long-term challenge to the dominance of natural gas and LNG in the energy mix.

Opportunities:

- Growth in Emerging Markets: Countries in Asia (like China and India) and other developing regions are expected to significantly increase their LNG imports to meet their growing energy needs and environmental targets.

- Development of Small-Scale LNG (SSLNG): SSLNG projects cater to niche markets like remote power generation, bunkering for smaller vessels, and industrial use in areas not connected to gas pipelines.

- Expansion of Floating LNG (FLNG) Solutions: FLNG technology enables the development of offshore gas fields that would otherwise be uneconomical, unlocking new supply sources.

- Integration with Carbon Capture and Storage (CCS): Combining LNG with CCS technologies can further reduce its carbon footprint and enhance its role in a low-carbon energy future.

- Use of Bio-LNG and Synthetic LNG: The development and deployment of bio-LNG (produced from organic waste) and synthetic LNG (produced using renewable electricity and hydrogen) offer pathways to decarbonize the LNG sector.

- LNG Bunkering Market Growth: The increasing adoption of LNG as a marine fuel presents a significant opportunity for the development of LNG bunkering infrastructure and services.

- Strategic Partnerships and Collaborations: Collaborations across the LNG value chain can optimize projects, share risks, and open up new market opportunities.

Challenges:

- Balancing Energy Security and Climate Goals: Navigating the role of LNG as a transition fuel while simultaneously pursuing long-term decarbonization targets remains a key challenge for policymakers and the industry.

- Ensuring the Safety and Security of LNG Infrastructure: Protecting LNG facilities and transportation routes from physical and cyber threats is paramount.

- Managing the Transition to Lower-Carbon Alternatives: Adapting business models and investments to account for the eventual shift towards cleaner energy sources and potential decline in long-term LNG demand.

- Addressing Public Perception and Environmental Concerns: Effectively communicating the benefits of LNG as a cleaner alternative and mitigating environmental concerns related to methane emissions and project development.

- Securing Financing for Large-Scale Projects: Obtaining the necessary financing for multi-billion dollar LNG infrastructure projects can be challenging, especially with increasing scrutiny on fossil fuel investments.

- Interoperability and Standardization: Establishing greater standardization in LNG equipment and processes can improve efficiency and reduce costs.

- Adapting to Evolving Market Dynamics: Responding effectively to the increasing role of spot markets, shorter-term contracts, and the evolving needs of LNG buyers and sellers.

LNG Market: Report Scope

This report thoroughly analyzes the LNG Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | LNG Market |

| Market Size in 2023 | USD 72.33 Billion |

| Market Forecast in 2032 | USD 130.76 Billion |

| Growth Rate | CAGR of 6.8% |

| Number of Pages | 184 |

| Key Companies Covered | Air Products & Chemicals, BG, BP, Cheniere Energy, Chevron, ConocoPhillips, Exxon Mobil, Gazprom OAO, Inpex, Petroleos De Venezuela, Petronas |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

LNG Market: Segmentation Insights

The global LNG market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global LNG market is divided into ethane, propane, butane, and nitrogen.

Ethane dominates the LNG Market by product segmentation due to its significant role as a primary feedstock in the petrochemical industry, particularly for ethylene production. Ethane is often extracted from LNG streams and is heavily utilized in the manufacturing of plastics, antifreeze, and detergents. Its demand is driven by large-scale ethane cracker projects and growing downstream processing capacity in regions such as North America and the Middle East. Additionally, the availability of ethane-rich natural gas and the expansion of export infrastructure have strengthened its dominance in the LNG value chain.

Propane holds a substantial share in the LNG Market as a versatile product used across residential, commercial, and industrial applications. Propane serves as a fuel for heating, cooking, and backup power generation, and is also used as a petrochemical feedstock in the production of propylene. Its portability and clean-burning properties make it especially valuable in regions lacking pipeline infrastructure. The demand for propane is further supported by rising usage in agricultural applications such as crop drying and irrigation engine fuel, particularly in Asia-Pacific and rural North America.

Butane is another important product in the LNG Market, mainly used as a blending component in liquefied petroleum gas (LPG), as well as in the production of isobutane and butadiene for petrochemical processes. Butane's applications also include use in refrigeration, lighters, and as a gasoline additive to improve combustion efficiency. Seasonal demand fluctuations, particularly in colder climates where LPG is used for heating, influence the consumption of butane. Additionally, the growing petrochemical demand in emerging economies contributes to the steady rise of this segment.

Nitrogen, while not a hydrocarbon, is present in LNG as an inert component and plays a vital role in controlling the heating value and combustion characteristics of the final LNG product. It is often removed during liquefaction to meet specific quality standards, but controlled amounts may be retained to help moderate LNG’s energy content, depending on regional regulations and end-user requirements. Though its share in terms of volume is relatively small, nitrogen is critical in certain industrial and safety applications, including LNG facility operations and cryogenic processes.

Segmentation Insights by Application

On the basis of application, the global LNG market is bifurcated into construction, furnaces, fluid bed dryers, food processing, manufacturing, mining, power generation sector, and rotary kilns.

Construction dominates the LNG Market by application, fueled by rapid global infrastructure development and the increasing need for reliable, off-grid energy solutions. LNG is used in construction for power generation, heating, and fueling heavy-duty equipment such as cranes, concrete mixers, drilling rigs, and generators. It is especially valuable for large-scale or remote projects—such as highways, railways, airports, tunnels, and high-rise buildings—where connection to the national grid or pipeline gas infrastructure is either unavailable or too costly. LNG’s low emissions profile compared to diesel and heavy fuel oil aligns with the industry's growing commitment to sustainability, making it an ideal choice in urban development zones with strict environmental regulations. Additionally, the ease of transportation and storage of LNG in cryogenic tanks allows for efficient fuel logistics on job sites. Many construction firms are adopting LNG to meet green building standards, reduce fuel theft, lower operating costs, and ensure energy security throughout project lifecycles. This has made construction the fastest-growing and most revenue-generating segment in the LNG application market.

Power Generation Sector represents a major share of LNG application, particularly in emerging and island nations that are replacing coal-fired plants with LNG-powered combined cycle or open cycle gas turbines. LNG is valued for its clean combustion, high energy output, and flexibility in peak and base-load power supply. Small-scale LNG terminals and floating storage regasification units (FSRUs) are making LNG accessible in previously underserved markets, enabling decentralized power generation and grid stabilization. As countries pursue net-zero targets, LNG serves as a transition fuel, helping to reduce the carbon intensity of national power mixes.

Manufacturing industries use LNG extensively for thermal energy in sectors such as steel, glass, cement, chemicals, paper, and textiles. LNG-fired boilers, kilns, and furnaces are favored for their efficiency, fuel consistency, and emissions control. LNG ensures higher process stability, reduces fouling in heat exchangers, and helps manufacturers meet increasingly strict environmental standards. The shift from coal or fuel oil to LNG is prominent in countries like China and India, where industrial decarbonization is becoming a national priority. Additionally, LNG’s relatively stable pricing provides cost predictability in long-term manufacturing operations.

Furnaces rely on LNG for its high calorific value, precise temperature control, and clean flame characteristics. Industries such as metallurgy, ceramics, and petrochemicals benefit from LNG’s ability to maintain consistent combustion over long periods, which is critical for batch and continuous high-temperature processing. Compared to coal or oil-based fuels, LNG reduces slag formation and extends the service life of refractory linings and heat exchangers, cutting down maintenance costs and downtime.

Mining operations are increasingly integrating LNG to power heavy equipment, haul trucks, and onsite electricity generation—especially in remote locations where diesel fuel logistics are challenging. LNG offers a cleaner, cheaper alternative with lower sulfur and particulate emissions, improving air quality and safety conditions at mine sites. LNG-fueled microgrids are also being deployed to enhance energy resilience and reduce operational risks from fuel delivery disruptions. Countries like Australia, Canada, and Chile are at the forefront of LNG adoption in the mining sector as part of broader environmental and cost-efficiency strategies.

Food Processing facilities use LNG for various heat-intensive operations such as baking, drying, sterilization, pasteurization, and steam generation. LNG is preferred due to its clean combustion, which prevents contamination of food products and ensures compliance with hygiene and safety standards. Additionally, LNG supports cogeneration systems (CHP), providing both thermal and electrical energy efficiently, reducing utility bills, and contributing to the sustainability targets of food manufacturers.

Fluid Bed Dryers use LNG as a precise and clean energy source to dry granular materials such as pharmaceuticals, fertilizers, and food products. LNG’s stable flame and low emissions ensure uniform heat distribution and minimal product degradation. Its clean-burning nature also reduces internal fouling in dryer systems, improving productivity and lowering cleaning and maintenance needs.

Rotary Kilns, used in cement, lime, ceramics, and waste treatment, require high and consistent temperatures, often exceeding 1,200°C. LNG supports these conditions with minimal environmental impact compared to traditional fuels like coal or petroleum coke. It also facilitates the production of high-purity clinker in cement manufacturing, reduces CO₂ emissions, and allows better control of process parameters—key factors in industries subject to carbon taxes and air quality regulations.

LNG Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the LNG Market, led by the United States, which has become one of the largest exporters of LNG globally due to its abundant shale gas reserves and expansive liquefaction capacity. Facilities such as Sabine Pass, Corpus Christi, and Freeport LNG contribute significantly to the region’s export volumes. The U.S. benefits from strong infrastructure, stable regulatory policies, and proximity to both Atlantic and Pacific markets. Rising demand from Europe and Asia, especially post-2022 energy supply shifts, has further enhanced North America's prominence. Canada is also exploring LNG expansion, particularly on its west coast, to supply Asia-Pacific markets.

Europe is a key importer in the LNG Market, with rapidly increasing LNG demand due to diversification efforts aimed at reducing dependence on Russian pipeline gas. Countries such as Germany, France, Spain, and the Netherlands have been investing in LNG regasification terminals, floating storage regasification units (FSRUs), and infrastructure upgrades. LNG has become critical in meeting energy security needs, especially in the wake of geopolitical tensions and supply disruptions. Additionally, Europe’s focus on decarbonization and replacing coal with cleaner fuels positions LNG as a transitional energy source during its shift toward renewables.

Asia-Pacific region is the largest consumer of LNG globally, driven by rapidly growing energy demand, urbanization, and industrialization. Countries like China, Japan, South Korea, and India dominate LNG imports. Japan, a long-standing top importer, uses LNG extensively in power generation due to limited domestic energy resources. China has surged in LNG demand as part of its effort to reduce air pollution by switching from coal to gas. South Korea and India also remain critical markets due to energy diversification policies and strong industrial growth. The region’s increasing number of long-term contracts and infrastructure investments underline its critical role in the global LNG ecosystem.

Latin America plays a growing role in the LNG Market, with countries like Argentina, Brazil, Mexico, and Chile expanding LNG imports to meet fluctuating domestic gas demand. Seasonal consumption patterns, limited pipeline infrastructure, and declining domestic production drive LNG usage. Brazil uses LNG to supplement hydroelectric power during droughts, while Mexico uses it to fuel power plants and industrial operations. Some nations, like Argentina, are also exploring export opportunities, particularly from the Vaca Muerta shale formation, as production capabilities expand.

Middle East and Africa region is both a major producer and an emerging consumer in the LNG Market. Qatar remains one of the world’s largest LNG exporters, supported by vast reserves in the North Field and strong global partnerships. Other exporters include Oman, Egypt, and Nigeria, which leverage LNG as a strategic economic asset. African nations like Mozambique are emerging producers, attracting significant investment in liquefaction infrastructure. On the demand side, growing urban populations and power generation needs in African economies are increasing regional LNG consumption, albeit from a low base.

LNG Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the LNG market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global LNG market include:

- Air Products & Chemicals

- BG

- BP

- Cheniere Energy

- Chevron

- ConocoPhillips

- Exxon Mobil

- Gazprom OAO

- Inpex

- Petroleos De Venezuela

- Petronas

The global LNG market is segmented as follows:

By Product

- Ethane

- Propane

- Butane

- Nitrogen

By Application

- Construction

- Furnaces

- Fluid Bed Dryers

- Food Processing

- Manufacturing

- Mining

- Power Generation Sector

- Rotary Kilns

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

LNG

Request Sample

LNG