Low Maintenance Chain Market Size, Share, and Trends Analysis Report

CAGR :

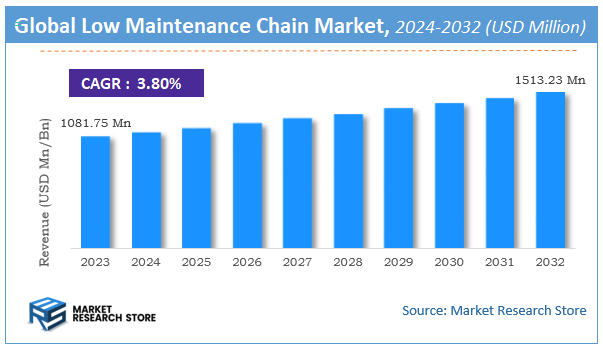

| Market Size 2023 (Base Year) | USD 1081.75 Million |

| Market Size 2032 (Forecast Year) | USD 1513.23 Million |

| CAGR | 3.8% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Low Maintenance Chain Market Insights

According to Market Research Store, the global low maintenance chain market size was valued at around USD 1081.75 million in 2023 and is estimated to reach USD 1513.23 million by 2032, to register a CAGR of approximately 3.8% in terms of revenue during the forecast period 2024-2032.

The low maintenance chain report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Low Maintenance Chain Market: Overview

Low maintenance chain is a specialized type of industrial or vehicular chain designed to operate efficiently with minimal lubrication, adjustment, or servicing over an extended period. These chains are engineered using advanced materials, specialized coatings, or built-in lubrication systems that reduce friction and wear, making them ideal for applications where regular maintenance is difficult, costly, or time-consuming. Low maintenance chains are commonly used in automotive systems, conveyors, agricultural machinery, packaging equipment, and heavy-duty industrial operations. The design of low maintenance chains often incorporates sealed joints, corrosion-resistant surfaces, and self-lubricating components, which prevent dirt and debris from interfering with performance. Some models use solid bushings and rollers to increase durability and reduce elongation over time.

The demand for low maintenance chains is increasing due to growing emphasis on operational efficiency, worker safety, and equipment uptime across various industries. As manufacturers and plant operators seek to minimize manual intervention and unplanned maintenance, the adoption of these chains is expanding. Technological advancements in materials science, such as the use of composite polymers and high-grade alloys, along with the integration of smart monitoring systems for predictive maintenance, are further contributing to the growth of the low maintenance chain market.

Key Highlights

- The low maintenance chain market is anticipated to grow at a CAGR of 3.8% during the forecast period.

- The global low maintenance chain market was estimated to be worth approximately USD 1081.75 million in 2023 and is projected to reach a value of USD 1513.23 million by 2032.

- The growth of the low maintenance chain market is being driven by increasing industrial automation and the need for reliable components that reduce downtime and operational costs.

- Based on the product, the lubricated segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the food segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Low Maintenance Chain Market: Dynamics

Key Growth Drivers:

- Demand for Reduced Downtime and Increased Productivity: Industries reliant on continuous operation seek components that minimize maintenance interruptions, as downtime can be costly. Low maintenance chains contribute to higher uptime and productivity.

- Focus on Lower Total Cost of Ownership (TCO): While the initial cost of low maintenance chains might be higher, their reduced need for lubrication, labor, and replacement parts often results in a lower TCO over their lifespan.

- Growing Automation and Remote Operations: Automated machinery and equipment operating in remote or difficult-to-access locations benefit significantly from low maintenance components like these chains, reducing the need for manual intervention.

- Stringent Safety and Environmental Regulations: Reduced or eliminated lubrication requirements in some low maintenance chains can contribute to safer working environments and minimize the risk of lubricant spills and environmental contamination.

- Advancements in Materials Science and Engineering: Innovations in self-lubricating polymers, surface treatments, and chain designs are leading to the development of more durable and effective low maintenance chains.

- Increasing Adoption in Specific Industries: Sectors like food processing, pharmaceuticals, textiles, and packaging, where contamination from lubricants is a major concern, are increasingly adopting low maintenance chain solutions.

- Demand for Extended Service Life: Low maintenance chains are often designed for longer service intervals, reducing the frequency of replacements and associated costs.

Restraints:

- Higher Initial Cost Compared to Standard Chains: Low maintenance chains typically have a higher upfront purchase price compared to conventional lubricated chains, which can be a barrier for budget-conscious applications.

- Potential Performance Limitations in Extreme Conditions: In very high-load, high-speed, or highly abrasive environments, some low maintenance chain designs might not offer the same performance or longevity as properly lubricated high-performance chains.

- Temperature and Chemical Compatibility: The self-lubricating materials or seals used in low maintenance chains may have limitations in terms of operating temperature range or compatibility with certain chemicals.

- Lack of Universal Standards and Clear Performance Metrics: The absence of widely accepted standards and performance metrics for low maintenance chains can make it difficult for users to compare different products and assess their suitability.

- Perceived Risk and Lack of Long-Term Data in Some Applications: Some end-users may be hesitant to switch to low maintenance chains, particularly in critical applications, due to a lack of long-term performance data or concerns about reliability under demanding conditions.

- Difficulty in Visual Inspection for Wear: Sealed or self-lubricating components can sometimes make it more challenging to visually assess the degree of wear compared to traditional chains where lubrication films provide a visual cue.

Opportunities:

- Development of Chains with Enhanced Performance in Extreme Conditions: Research and development focused on improving the load-bearing capacity, speed rating, and resistance to harsh environments for low maintenance chains.

- Integration of Smart Monitoring and Predictive Maintenance Capabilities: Incorporating sensors and data analytics to monitor chain wear and predict maintenance needs, further reducing unplanned downtime.

- Customization for Specific Industry Requirements: Designing and manufacturing low maintenance chains tailored to the unique demands of specific industries, such as those with stringent hygiene or temperature requirements.

- Development of Retrofit Solutions for Existing Equipment: Offering low maintenance chain options that can be easily retrofitted onto existing machinery as replacements for traditional chains.

- Expansion into New Applications and Industries: Identifying and targeting new sectors where the benefits of reduced maintenance and clean operation can be particularly valuable.

- Focus on Sustainable and Environmentally Friendly Materials: Developing low maintenance chains using environmentally friendly materials and manufacturing processes.

Challenges:

- Balancing Performance, Cost, and Maintenance Reduction: The key challenge is to develop low maintenance chains that offer comparable or better performance than traditional chains without a significant cost premium.

- Ensuring Long-Term Reliability and Durability: Proving the long-term reliability and durability of low maintenance chains across a wide range of operating conditions.

- Overcoming User Skepticism and Promoting Adoption: Educating end-users about the benefits and proper application of low maintenance chains and overcoming any ingrained preferences for traditional lubricated chains.

- Developing Effective Wear Indicators and Monitoring Methods: Creating reliable ways to assess chain wear and predict replacement needs for low maintenance designs.

- Standardization and Performance Benchmarking: Establishing industry standards and clear performance metrics to facilitate product comparison and informed purchasing decisions.

- Adapting to the Diverse Needs of Different Applications: Providing a range of low maintenance chain solutions that can effectively address the varied requirements of different industrial and mechanical applications.

Low Maintenance Chain Market: Report Scope

This report thoroughly analyzes the Low Maintenance Chain Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Low Maintenance Chain Market |

| Market Size in 2023 | USD 1081.75 Million |

| Market Forecast in 2032 | USD 1513.23 Million |

| Growth Rate | CAGR of 3.8% |

| Number of Pages | 174 |

| Key Companies Covered | Allied Locke, Rexnord, Hitachi, Brewer, HKK, Renold, Morse, iwis, Peer, Union, Tsubaki, Wippermann, Kettenwulf Inc., KTN |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Low Maintenance Chain Market: Segmentation Insights

The global low maintenance chain market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global low maintenance chain market is divided into lubricated and lubricant-free.

Lubricated low maintenance chains dominate the market due to their widespread adoption in heavy-duty industrial applications that demand high load-bearing capacity, consistent performance, and extended operational life. These chains are pre-lubricated with high-quality lubricants and often come with sealed or encapsulated designs that minimize the need for frequent relubrication. Industries such as manufacturing, automotive, mining, and construction favor lubricated chains for their ability to withstand harsh operating conditions while ensuring minimal wear and reduced downtime. The dominance of this segment is also supported by continuous advancements in lubrication technology and material durability, which make lubricated chains more reliable over long-term use.

Lubricant-free chains are gaining traction, especially in environments where cleanliness is critical—such as food and beverage processing, pharmaceuticals, and cleanroom applications. These chains are typically constructed from self-lubricating materials or feature advanced coatings that eliminate the need for external lubrication. While their market share is currently smaller than lubricated chains, they are increasingly preferred in industries where contamination from grease or oil must be avoided. Additionally, their environmental benefits, including reduced use of chemicals and lower maintenance requirements, position them as a sustainable alternative, supporting their gradual market growth.

Segmentation Insights by Application

On the basis of application, the global low maintenance chain market is bifurcated into food, packaging, paper, textile, automobile, and others.

Food application segment holds significant dominance, driven by the low maintenance chain industry's stringent hygiene standards, automation requirements, and the need for continuous, high-speed operations with minimal downtime. In food processing plants, maintaining hygiene and minimizing contamination risk is paramount. Low maintenance chains, especially those made of stainless steel or equipped with self-lubricating bushings, are ideal in these environments as they eliminate the need for frequent lubrication, which can potentially contaminate food products. These chains are used in conveyor belts, filling lines, and packaging units. Their resistance to corrosion, ease of cleaning, and compliance with FDA and NSF standards make them essential components in meat processing, bakery, beverage bottling, and dairy production facilities.

Packaging industries heavily rely on low maintenance chains to achieve high-speed operations with minimal downtime. In packaging machinery—such as carton erectors, fillers, and labeling machines—chain performance directly affects production efficiency. Low maintenance chains ensure continuous motion without the need for frequent relubrication or adjustments, which is vital in fast-moving consumer goods (FMCG) and logistics environments. Their use contributes to reduced operational costs, extended machine lifespan, and improved throughput, particularly in automated and high-volume packaging lines.

Paper industry environments are typically harsh, with exposure to dust, pulp residues, moisture, and chemicals. Low maintenance chains are suited to these conditions due to their robust construction and resistance to wear and corrosion. They are commonly used in paper converting machines, corrugators, printing presses, and pulp handling systems. By reducing the need for manual intervention and lubricant application, these chains help maintain consistent performance, minimize maintenance labor costs, and reduce unplanned downtime, which is especially important in continuous production cycles.

Textile industry operations involve exposure to lint, fluctuating tension, heat, and moisture. Machines such as spinning frames, looms, and dyeing equipment benefit from low maintenance chains due to their ability to operate smoothly without frequent lubrication, which is crucial in environments where oil contamination can affect fabric quality. These chains also help maintain synchronization in high-speed machinery, contributing to better product quality and reduced material waste. Additionally, they support energy efficiency and enhance machine longevity, which are important factors in cost-sensitive textile manufacturing environments.

Automobile manufacturing and assembly lines are some of the most demanding operational environments for mechanical components. Low maintenance chains are extensively used in conveyor systems, robotic arms, paint shops, and machining centers. These chains support high load capacities, frequent start-stop cycles, and continuous operation. Their reduced maintenance needs result in less production interruption and lower total cost of ownership. In an industry that values precision, speed, and efficiency, low maintenance chains help OEMs and Tier-1 suppliers meet stringent production and quality requirements.

Low Maintenance Chain Market: Regional Insights

- North America is expected to dominate the global market.

North America dominates the Low Maintenance Chain Market, primarily driven by the region’s well-established industrial base, technological advancements, and high demand for durable, efficient, and low-maintenance solutions across various sectors. The United States and Canada have a strong manufacturing and automotive presence, where low-maintenance chains are increasingly used in industries like material handling, automotive, mining, and manufacturing. The adoption of low-maintenance chains is also supported by the focus on reducing downtime and maintenance costs in industrial operations. Furthermore, the region’s technological advancements, particularly in lubricants and advanced coatings, contribute to the growing demand for low-maintenance chain systems.

Asia-Pacific is experiencing rapid growth in the Low Maintenance Chain Market, supported by booming industrialization, expanding manufacturing bases, and increasing investments in automation and machinery. Countries like China, India, Japan, and South Korea are major contributors to the market. As industrial operations in the region scale up, there is a growing demand for high-performance, low-maintenance chains, especially in industries like automotive, logistics, and agriculture. The adoption of these solutions is also supported by the rising need to reduce maintenance downtime and operational costs in manufacturing plants and assembly lines. Japan, in particular, is a key player in developing innovative low-maintenance chain technologies.

Europe holds a significant share in the Low Maintenance Chain Market, driven by its strong industrial sectors, including automotive, food processing, and energy. Countries such as Germany, France, and the United Kingdom are major adopters, leveraging low-maintenance chains for efficiency, durability, and cost-effectiveness. The European Union’s emphasis on sustainability and reducing operational costs across industries further accelerates demand for such solutions. Additionally, the automotive and manufacturing industries in Europe increasingly rely on low-maintenance chains to meet stringent performance and operational efficiency standards, contributing to steady growth in the market.

Latin America presents moderate growth in the Low Maintenance Chain Market, with increasing adoption in countries like Brazil, Mexico, and Argentina. The region’s key industries such as mining, agriculture, and manufacturing are gradually recognizing the value of low-maintenance chains in improving operational efficiency and reducing maintenance costs. However, the market’s growth is somewhat hindered by economic volatility, limited access to advanced technologies, and lower industrial automation rates compared to more developed regions. Nonetheless, as the region’s industrial sectors modernize, there is growing interest in investing in durable, cost-effective machinery solutions, including low-maintenance chains.

Middle East and Africa region is an emerging market in the Low Maintenance Chain Market, with key growth drivers including infrastructure development, energy, and manufacturing industries. Countries such as Saudi Arabia, South Africa, and the United Arab Emirates are witnessing increasing demand for low-maintenance chains as part of their industrial modernization initiatives. The region’s focus on improving productivity, reducing downtime, and ensuring the longevity of industrial equipment is driving the need for more efficient chain systems. However, adoption is somewhat limited in rural areas due to infrastructure challenges and lower technology penetration.

Low Maintenance Chain Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the low maintenance chain market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global low maintenance chain market include:

- Allied Locke

- Rexnord

- Hitachi

- Brewer

- HKK

- Renold

- Morse

- iwis

- Peer

- Union

- Tsubaki

- Wippermann

- Kettenwulf Inc.

- KTN

The global low maintenance chain market is segmented as follows:

By Product

- Lubricated

- Lubricant-free

By Application

- Food

- Packaging

- Paper

- Textile

- Automobile

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Low Maintenance Chain

Request Sample

Low Maintenance Chain